Robert Way

Investment action

I recommended a hold rating for Victoria’s Secret (NYSE:VSCO) when I wrote about it the last time (Early Jan 2023), as I saw no improvements in the turnaround situation yet, despite the valuation seemingly pricing in a successful turnaround in the near term. Indeed, VSCO showed no improvements since, and the share price fell after the 4Q24 results. Based on my current outlook and analysis, I am sticking to a hold rating. The key update in this post is that the stock is now fully in “show me” territory. Management has failed to deliver against expectations set out in 3Q24 as SSSG remained weak in 4Q24 and into 1Q25. In order for me (and I believe the market) to gain confidence in the business, VSCO will need to print consecutive quarters of SSSG improvements.

Review

Overall P&L for 4Q24 seems positive on a headline basis, revenue grew 3% and gross margin expanded to ~40% with EBIT margin mostly flat (30bps decline). However, if we compare this to FY19 (pre-covid), 4Q24 revenue is actually down by ~4% CAGR. VSCO ended 4Q24 with $270 million in cash and $145M in debt. Inventories were down 6% with core VS/PINK down 3%. In addition, management announced a new share repurchase program of up to $250M.

Importantly, VSCO showed disappointing fundamental outlook in its 4Q24 results (7 March). The main metric to track is same-store-sales growth [SSSG] (down 6% in 4Q24) because it best represents demand, which was the same as the 4Q23 decline of 6%, suggesting no major improvements at all. In fact, I view the 6% decline in 4Q24 as worse than last year because it was compared against a weak base (4Q23 was compared against -2% SSSG in 4Q22). Although this was a sequential improvement, I don’t think it calls for a celebration given that 4Q was the holiday season, which boosts sales. Importantly, SSSG performance appears to have remained weak in 1Q25 (Feb to May), where management cited no improvement in same-store sales trends observed in February and quarter-to-date (as of March 7, 2024). This is really bad, as this comment comes at a time when VSCO has rolled out three growth initiatives (the Valentine Day product launch, the relaunch of the #1 bra collection, and the Pink Apparel Spring campaign).

At this point, I have increasing doubts about whether VSCO has the right strategy in place to stay relevant to consumers’ preferences. I would’ve imagined Valentine’s Day to sort of boost sales, but even that didn’t help at all. Management’s comment was particularly discouraging in that they called February a challenging and promotional month (note the word “promotional,” which made the situation worse as sales did not see any improvement). In addition, for the bullish investors that were happy about the sequential improvement in SSSG in 4Q24 vs. 3Q24, that trend is unlikely to continue through 1Q25 given that management expectations for North America sequential improvement into February did not come to fruition. North America is a large part of revenue (international is only 11% of FY24 revenue), so this effectively implies that 1Q25 SSSG is going to be weaker than -6%.

The macro environment is certainly not in favor of VCSO as well. Because of the sticky inflation and weak consumer spending environment, more consumers have turned to more value purchases, causing VSCO’s intimates market to be down mid-single-digits in 4Q24. While I am not a macroeconomic expert, the factual data we have today shows that inflation remains sticky, the US housing undersupply situation will take some time to fix, and the US economy remains strong. In my opinion, there is little reason for the Fed to cut rates anytime soon. As rates stay higher for longer, consumers budgets for spending are likely to remain tight, impacting demand for VSCO goods.

From a market perspective, sales for the intimate market in North America as a whole decreased mid-single digits in the quarter compared to last year, which was the fourth consecutive quarterly year-over-year decline. 4Q23 call

Aside from the business fundamentals, I am not a fan of stock sentiment currently as VSCO becomes more of a “show me” story, and until VSCO actually shows positive growth inflection in SSSG, I think the stock is going to stay rangebound. I believe the market has lost faith in management’s guidance as they failed to deliver against what was guided in 3Q24, where management indicated it viewed 3Q as a potential inflection point (this drove the stock upwards from $14 to high-$20s at one point). The recent performance basically resets all expectations and further reduces market confidence in VSCO’s turnaround achievability. Also, this negative performance tends to feed more data to support a more bearish narrative, such as VSCO growth becoming structurally impaired as it is now less relevant than in the past. In the past, VSCO was a force to be reckoned with (management still claims they have the largest market share in Intimates in their 4Q24 earnings call). Fast forward today; this “sexy” image seems to have lost its footing, and this is a large part of VSCO’s competitive advantage. Removing this would mean that VSCO has less to stand out against its peers. Hence, VSCO may not be able to capture the next generation of consumers as easily as it did in the past.

Valuation

Author’s work

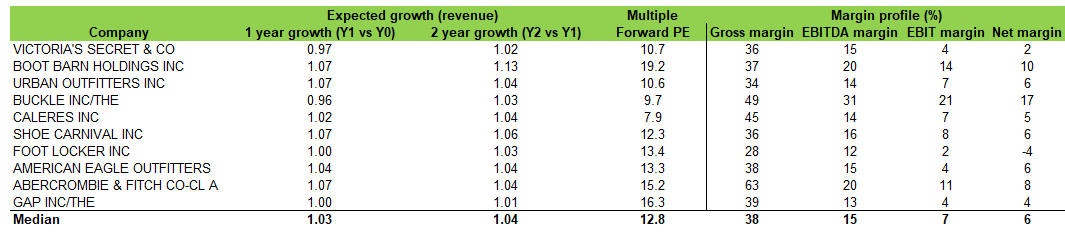

Until VSCO has shown more credible signs of positive inflection, I think the stock price is going to stay rangebound in the near term. VSCO currently trades at 11x forward PE, a discount to peers’ average of 13x forward PE, which I expect to persist given its growth outlook is much poorer than peers (200 to 600bps poorer). Suppose VSCO were to successfully turnaround the business, driving growth to peers’ levels; valuation should follow accordingly, representing ~20% upside simply on valuation rating (12.8/10.7x).

However, if VSCO growth continues to stay poor, signifying structural growth impairments, we could see valuation fall back to the previous low of mid-single-digits forward PE (i.e., 5x), implying a downside of >50% (5/10.7x). Hence, I continue to recommend a hold rating for VSCO until I see solid signs of improvement.

Final thoughts

My recommendation remains a hold. Disappointing same-store sales growth suggests a weak business turnaround, and a challenging macro environment further hinders the turnaround efforts. The stock is deep in the “show me” territory as management failed to deliver against its positive guide in 3Q24, and as growth continues to stay weak, it provide more data point to support bearish narrative, likely putting more pressure on the stock price and valuation. While a successful turnaround could lead to valuation upside, I prefer to wait for VSCO to show clear path to recovery.

Q2 2024 Earnings Call Transcript")