Hiroshi Watanabe/DigitalVision via Getty Images

Intro & Thesis

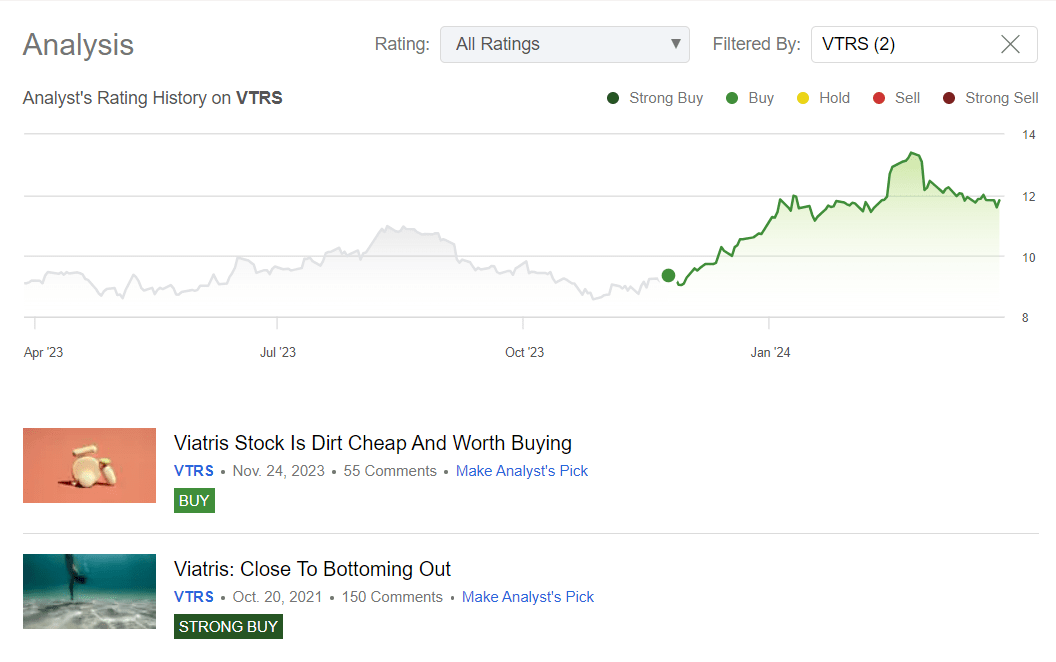

I initiated coverage on Viatris Inc (NASDAQ:VTRS) in October 2021, and then updated my bullish thesis a few months ago, stating that the stock looked dirt cheap. The VTRS stock rose significantly by 26.7% since my last update, outperforming the S&P 500 Index (SPX) (SP500):

Seeking Alpha, the author’s coverage of VTRS stock

Due to the abundance of new data that has emerged since November last year (the time of my last article), I believe it is justified to take a fresh look at the company and assess the medium-term growth potential of its stock.

Latest Financials And Developments Review

Let’s first understand what Viatris’s business looks like. It’s a global pharmaceutical company with around 38,000 employees in 165 countries, organizing its operations into 4 reportable segments:

- Developed Markets (primarily North America and Europe) – 60.12% of total net sales in FY2023;

- Greater China (China, Taiwan, and Hong Kong) – 14%;

- JANZ (Japan, Australia, and New Zealand) – 9.25%, and

- Emerging Markets (>125 countries with developing markets and emerging economies) – 16.58%.

In FY2023, Viatris’s total net sales amounted to about $15.4 billion, showing a YoY decline of 5.13% driven primarily by the unfavorable impact of foreign currency (Viatris generates ~77% of sales outside the U.S.) and divestitures (seems like a one-off event). Adjusted EBITDA dipped by >11% YoY, but what I like is the gross profit margin expansion from 39.95% in FY2022 to 41.74% in FY2023. Due to higher R&D expenses and the settlement of legal disputes, VTRS’s operating costs increased significantly (+16.19% compared to the previous year), which led to a 52.5% YoY drop in EBT.

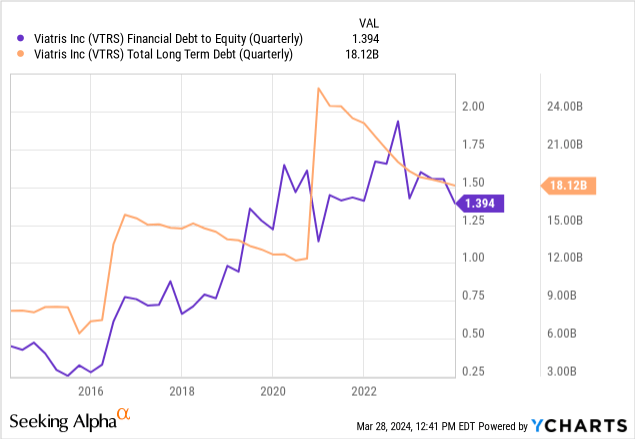

What I also like is that the company seems to be focusing on maintaining an investment-grade rating and keeping its debt burden tight: it has successfully reduced debt by $6.5 billion since its formation in 2020, meeting its 2023 goal. There is still a lot of work ahead, but judging by the latest dynamics, VTRS is moving in the right direction:

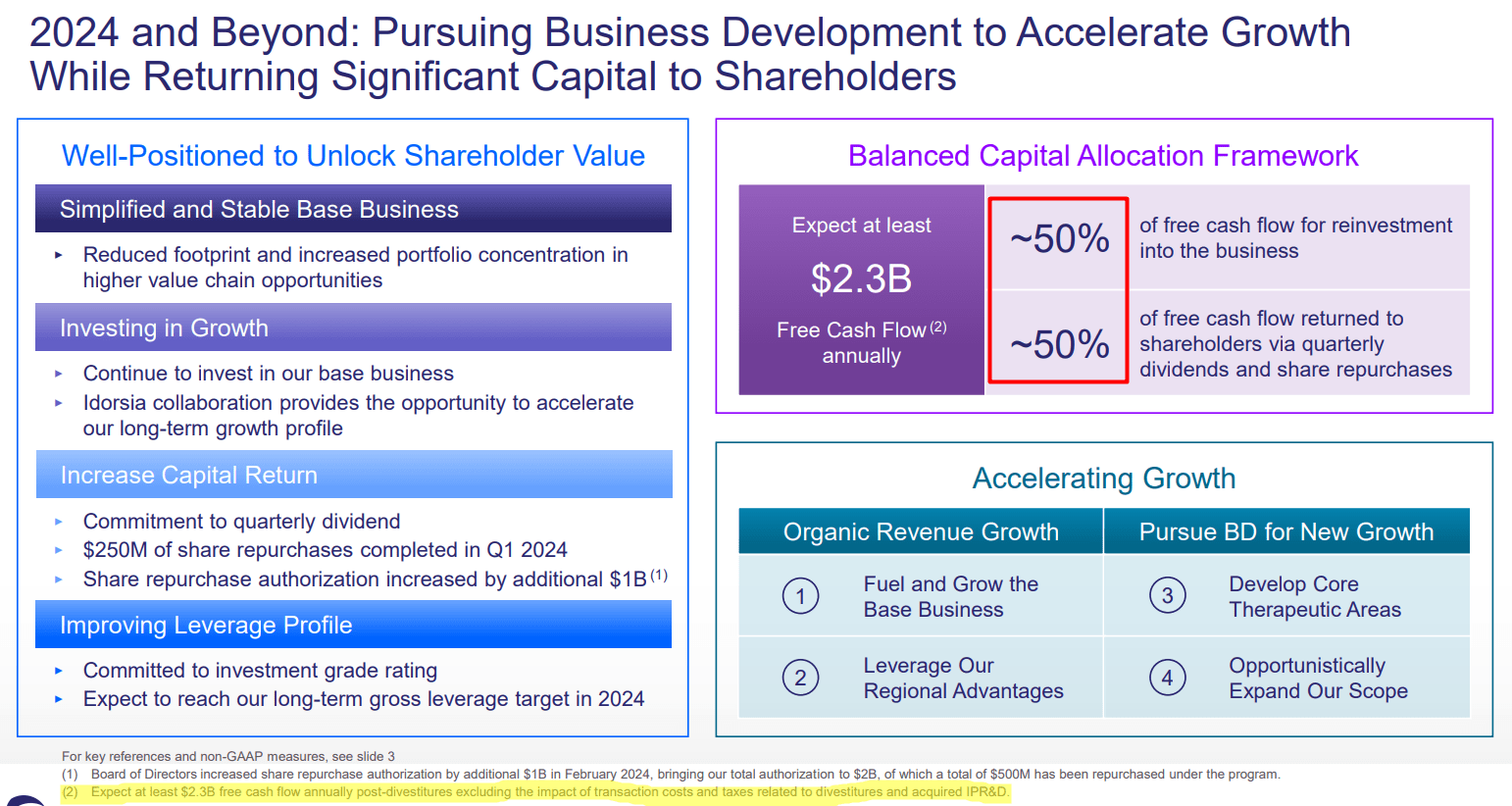

Be that as it may, a very bright spot in the company’s financial figures became the FCF of $2.4 billion – that’s about 17% of today’s market cap. And another important point: according to the IR presentation for Q4 FY2023, the company expects annual FCF of at least $2.3 billion after the divestitures, excluding the impact of transaction costs and taxes related to the divestitures and acquired IPR&D (~16% of market cap). In my view, management’s strategy of using 50% of this commendable free cash flow for reinvestment and the remaining 50% for buybacks and dividends seems fair and balanced:

VTRS’s IR materials, author’s notes

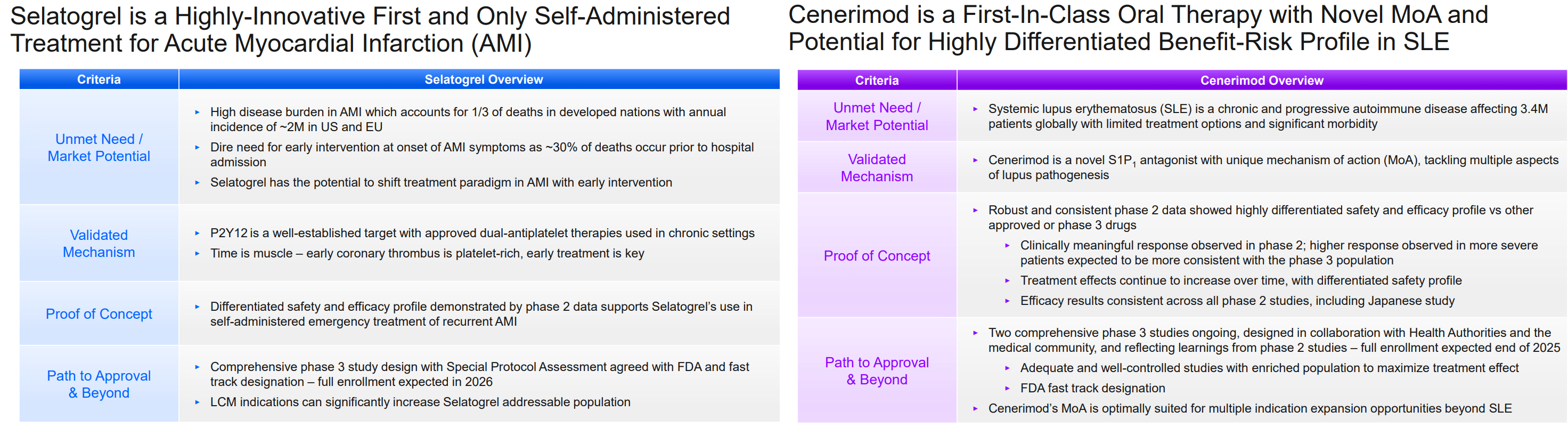

I think these plans are quite feasible as the company now has 2 new drugs ready for commercialization to reignite business growth – Selatogrel and Cenerimod. The recent R&D event was dedicated to them – Seeking Alpha provides a transcript for your convenience.

What I could understand without having a medical education:

- Selatogrel was developed to prevent blood clotting and minimize damage to the heart muscle during a heart attack. It is characterized by its subcutaneous administration and reversible effect. Having a rapid onset of action and a short duration of action, it may be suitable for emergency use in heart attack patients. The Initial data from Phase 2 studies show that Selatogrel achieves strong platelet inhibition within minutes of administration and has a favorable safety profile, according to the R&D event’s transcript.

- Cenerimod is another asset with significant potential, particularly in the treatment of SLE, a chronic autoimmune disease that can affect various organs and tissues in the body. According to The Business Research Company’s study, the systemic lupus erythematosus treatment market ( Cenerimod’s targeted end market) has seen rapid growth, increasing from $2.76 billion in 2023 to $3.06 billion in 2024, reflecting a CAGR of 10.7%. So I believe that Viatris’s new drug has great potential in the future.

VTRS’s R&D Event Presentation, author’s compilation

In general, I like what I have seen in terms of the future vision of the company’s development and the financial data. VTRS stock has continued to rise actively in recent months for a reason. I mean there were fundamental reasons for this, as I can see from my analysis. But is today’s price fair? What about the foreseeable upside potential?

Viatris Stock Valuation Update

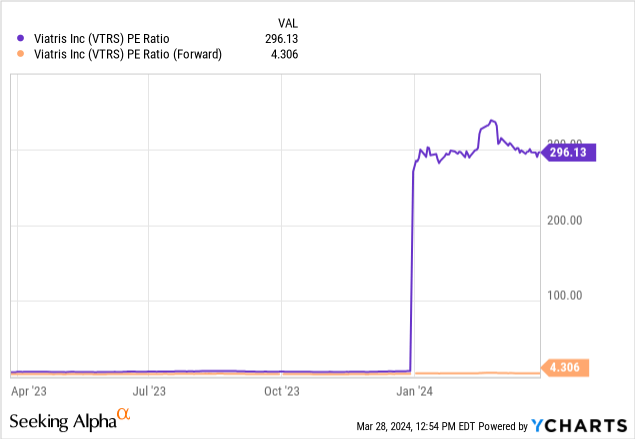

Back in November 2023, the VTRS stock was trading at a forwarding P/E multiple of 3.2x, pricing a ~49% discount to the TTM multiple of 6.2x at the time – in both cases, VTRS looked very cheap to me. However, in the FY2023 report, we saw a rapid decline in net profit due to essentially one-off events, which pushed the TTM P/E ratio to over 296x. What saves the situation with the company’s valuation is the forwarding P/E ratio, which assumes the company will return to a normal operating condition shortly.

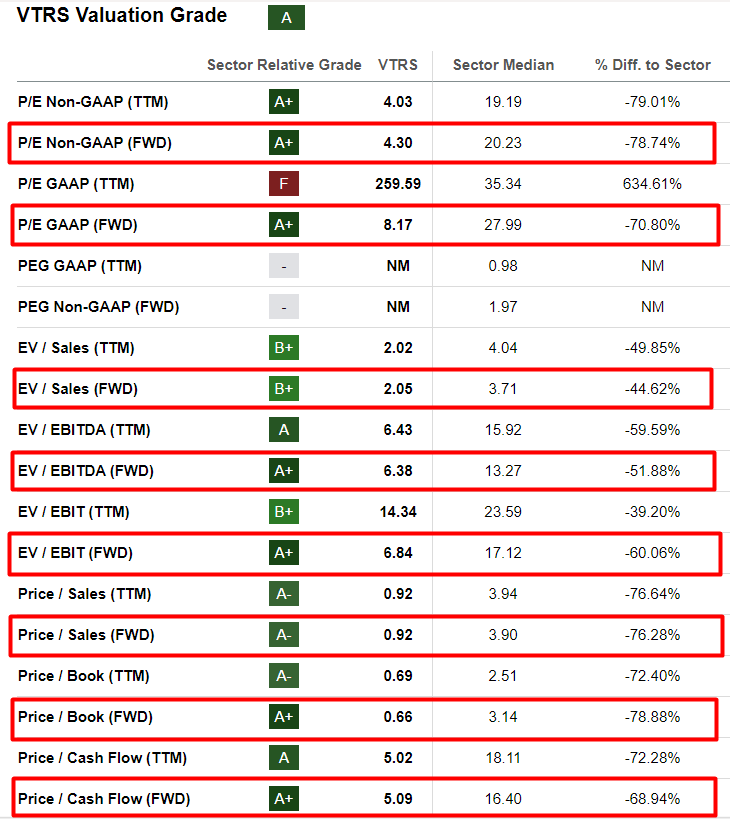

In fact, based on Seeking Alpha’s Quant system, VTRS may be undervalued by 79-44% depending on a chosen metric compared to the overall healthcare sector – and the TTM price-to-earnings GAAP ratio is the only “alarming” F-rated thing in the sample:

Seeking Alpha, VTRS, author’s notes

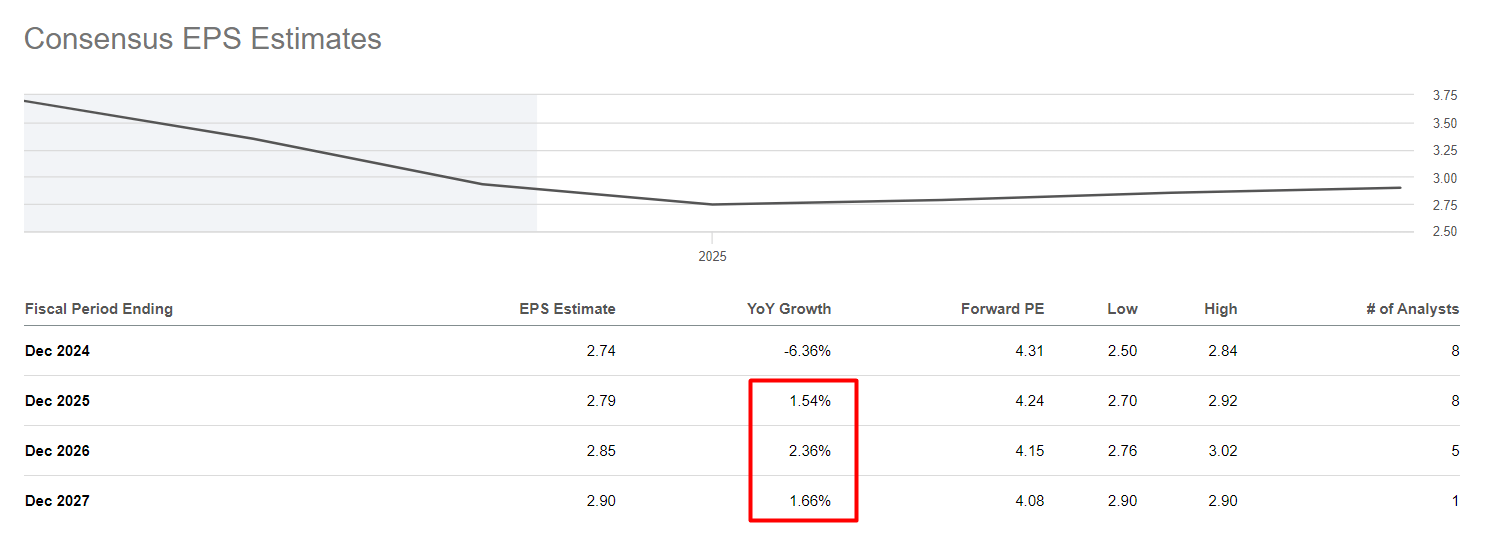

However, I do not believe VTRS will return to an 8-10 times P/E anytime soon – it is definitely hampered by low EPS growth rates that are going to occur as patents become obsolete and cannot be covered by new drug sales. The consensus agrees with me:

Seeking Alpha, author’s notes

However, I think VTRS should fall into the range of 5-6x of earnings – the fair share price in this case should reach ~$15.3 by mid/late 2025. That gives us almost 30% upside potential from the last closing price. So the growth potential I saw earlier has become less (30% now versus 55% last time), but I still think VTRS remains a good “Buy” at the moment.

Risk Factors To Consider

Of course, the risk factors that I cited for readers’ consideration last time haven’t disappeared. Factors such as patent expirations, pipeline setbacks, litigation, supply chain disruptions, currency fluctuations, and the complexity of post-merger integration all contribute to VTRS’s risk profile and still play a large role in determining the future direction of the stock.

Here we must also add the still quite high level of debt on the balance sheet: Yes, it’s falling from quarter to quarter, but the debt-to-equity ratio of almost 1.4 causes me some concern. Perhaps the 50/50 split of FCF between reinvestment and shareholder return, which the management talks about, should be revised more towards deleveraging.

It’s also important to note here that my findings regarding Viatris’ undervaluation could be wrong, as the stock could maintain its current discount if the market doesn’t want to reward the company for insufficient deleveraging (or anything else).

The Verdict

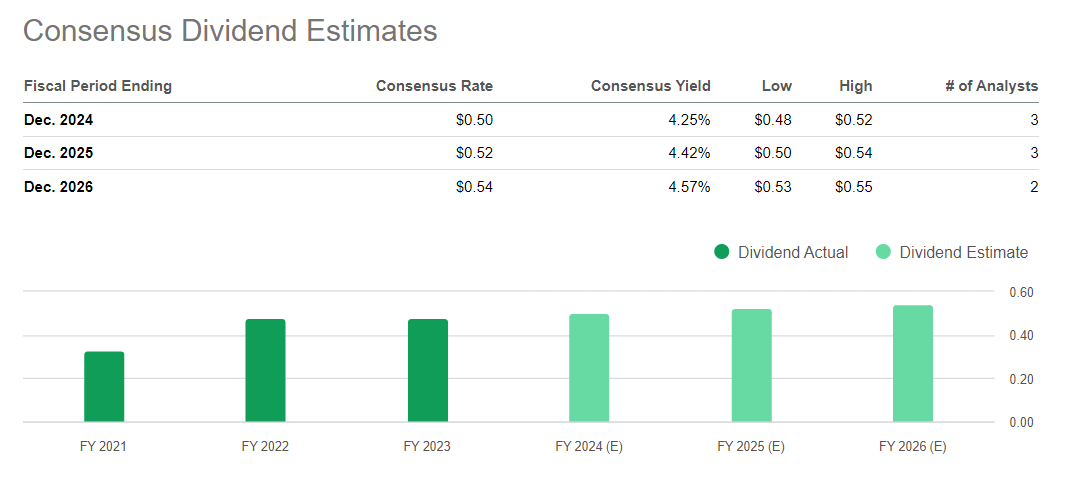

Despite the many risks, I like the way the company has developed recently. Although the latest financial results did not exceed analysts’ expectations (Viatris missed both sales and EPS consensus estimates), I think Viatris’ general direction of development is correct. The 55% growth potential I talked about earlier has now fallen to 30% – this is mainly because the stock has risen significantly in that time (roughly by the difference between these two upside potentials). But 30% undervaluation is still a lot. Also, the company pays a good dividend – over 4%. What’s more, the dividend is likely to rise further over the next few years:

Seeking Alpha, VTRS’s Dividend Estimates

Therefore, based on the combination of the factors described above, I am today reiterating my previous “Buy” rating for VTRS.

Thanks for reading!

Q2 2024 Earnings Call Transcript")