onurdongel

Overview

Vermilion Energy (NYSE:VET) is a Canadian oil & natural gas producer, with production in North America, Europe, and Australia. The stock is listed in the U.S. & Canada (TSX:VET:CA), and the reporting currency is Canadian Dollars. I have covered Vermilion frequently over the last couple of years and those articles can be found here.

Figure 1 – Source: Vermilion Corporate Presentation

The company has just over half of its production coming from natural gas and the remaining portion from liquids. However, a significant percentage of the natural gas production is in Europe, where the margins are still relatively good, even though we are of course down substantially from the peak levels seen during 2022.

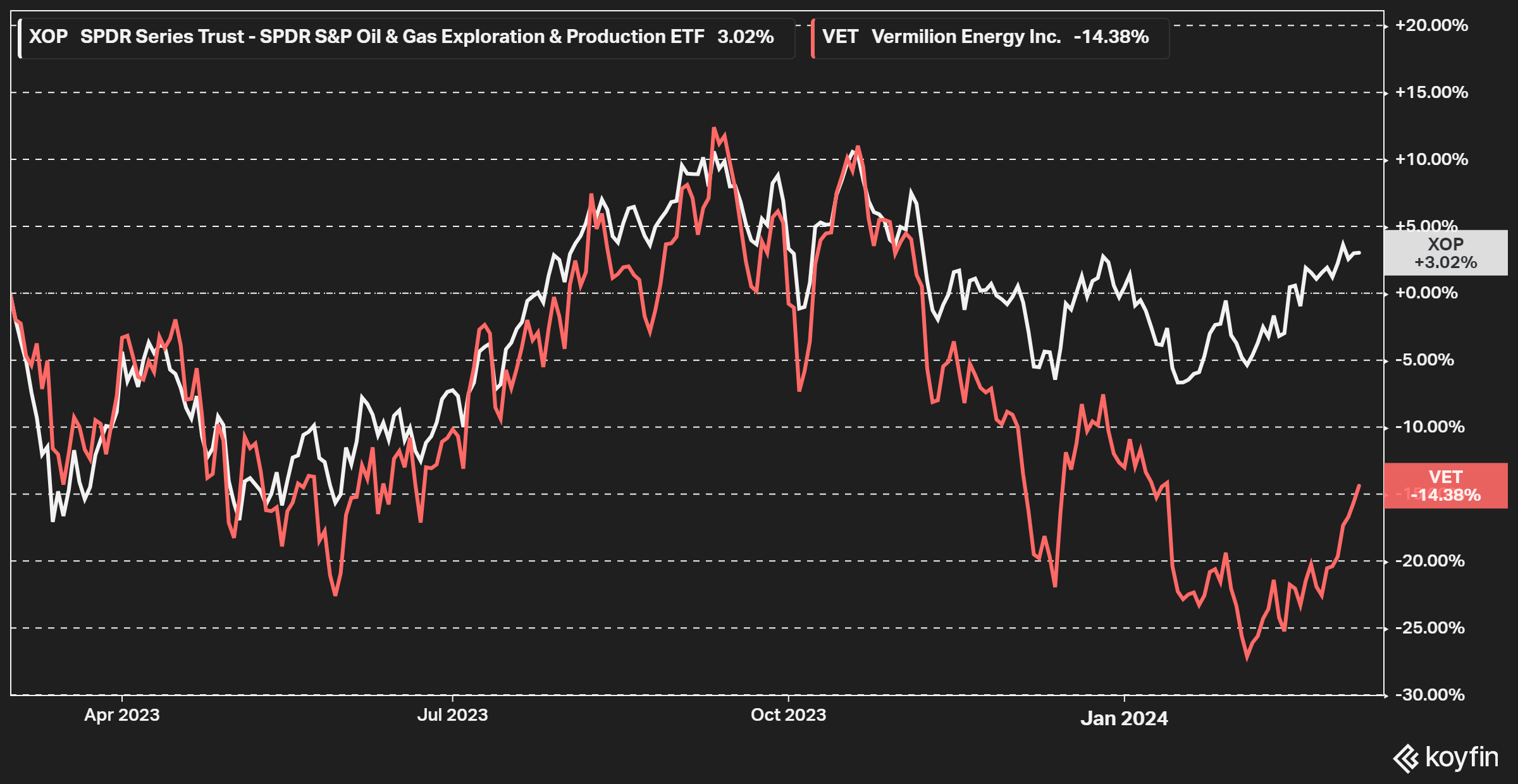

Figure 2 – Source: Koyfin

Vermilion has underperformed most peers a lot over the last year, where most of that underperformance has come in the last few months with weaker natural gas prices. The company has substantial exposure to natural gas, so some weakness is understandable, but the magnitude of the decline feels excessive given that almost half of the 2024 European natural gas production is hedged, with floors above current levels. Also, the company’s funds flow is far more sensitive to oil prices compared to North American natural gas prices.

Vermilion continues to trade with one of the more extreme free cash flow yields in the industry, and the company has now confirmed that 50% of excess free cash flow in 2024 will be distributed to shareholders. Excess free cash flow is defined as free cash flow minus payments to lease obligations & asset retirement obligations (“ARO”) settled. So, I continue to be bullish on the stock.

The company did yesterday after the close release its Q4-23 result and will host a conference call later today. This article will primarily be focused on the Q4 result and my general views on the company.

Q4-23 Result

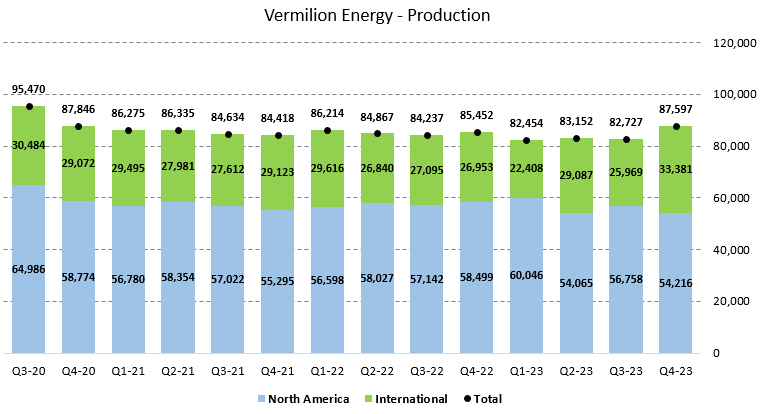

The production in Q4 was 87,597 boe/d compared to 82,727 in Q3. An increase was expected following the restart of the Australian production in late Q3, but the increase was slightly above my expectations. Q4-23 was the best quarterly production number since Q4-20.

The downtime of the Australian assets during much of 2023 and some maintenance in Ireland has otherwise weighed on the production in the prior quarters. The annual production in 2023 was 83,994 boe/d, within the latest 2023 guidance range. The 2024 guidance is 82,000-86,000 boe/d, so production in 2024 is expected to be roughly flat compared to 2023.

Figure 3 – Source: Quarterly Reports

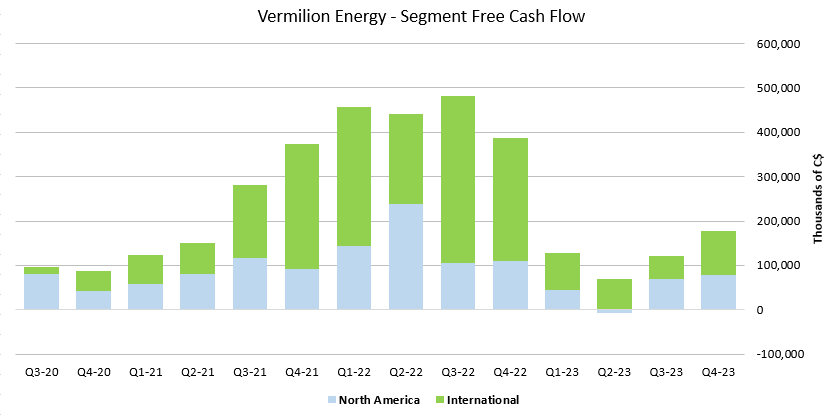

Vermilion reported a strong funds flow of C$372M in Q4 compared to the C$270M in the prior quarter. Free cash flow was C$229M compared to C$145M in Q3. The increase in cash flows was due to the higher production volume, a good sales price, a PRRT recovery in Australia, competitive costs, and a substantial hedging gain during Q4.

Figure 4 – Source: Quarterly Reports

The contribution to free cash flow from the international assets continues to be disproportionate in relation to their production volume, even if the levels are down from the peak quarters in 2022.

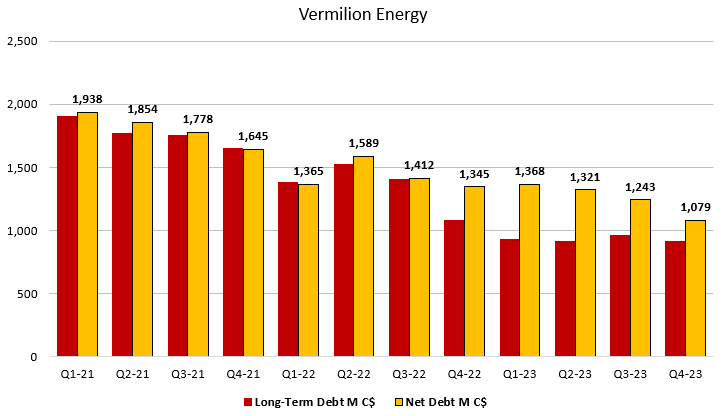

The net debt was C$1,079M at the end of 2023. The progress on the deleveraging has caused the company to accelerate the higher shareholder distributions to 50% of excess cash flow, for all of 2024, and not just from Q2-24 as previously announced. It was already known that the quarterly dividend from April would increase to C$0.12 per quarter from C$0.10, but we can now expect an uptick in the buybacks as well. The company has YTD repurchased 1.4M shares already.

Figure 5 – Source: Quarterly Reports

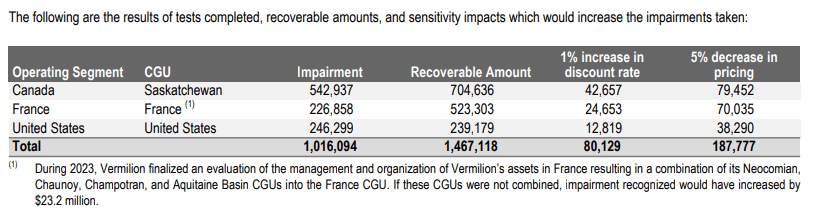

On the negative side, Vermilion reported a non-cash C$1B impairment of the company’s French and North American assets, following some changes to cost assumptions and technical revisions.

Figure 6 – Source: Vermilion Q4-23 Report

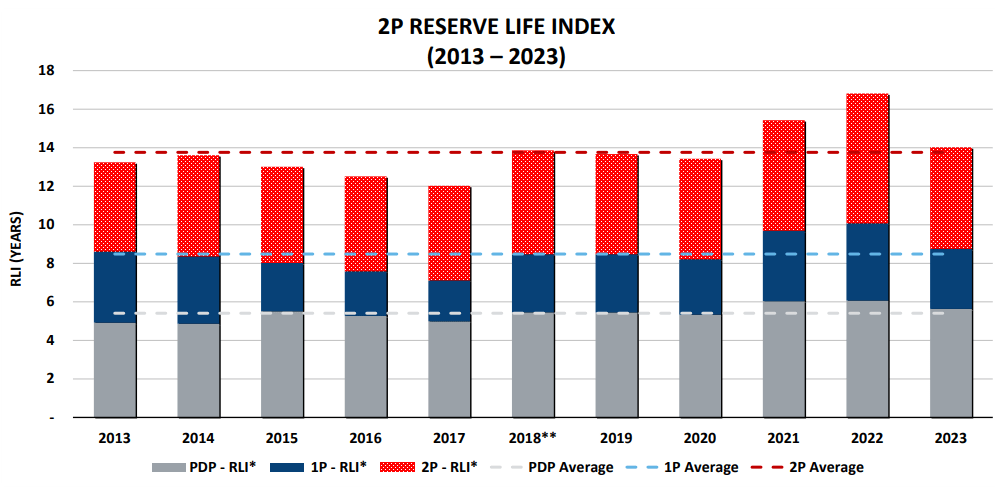

The company also reported a decrease on the reserve side, where proved developed producing reserves decreased by 8% and total proved plus probable reserves decreased by as much as 18%. These are certainly not encouraging numbers, even if part of the decrease is due to dispositions and capital allocation decisions. However, we can in the chart below see that the reserves are roughly in line with historical averages.

Figure 7 – Source: Vermilion Q4-23 Presentation

Valuation & Conclusion

Vermilion is presently trading with a very attractive free cash flow yield in the 20-25% range, using market cap and strip prices for WTI, natural gas in Europe and North America. So, if we deduct ARO settled & payments to lease obligations, the yield is around 20% or just below.

Vermilion has a diversified asset base, relatively low operating costs & financial leverage, and the shareholder distributions are now improving. So, the current depressed valuation feels unjustified in my view. The valuation has been depressed for a couple of years though, so some more patience might be needed.

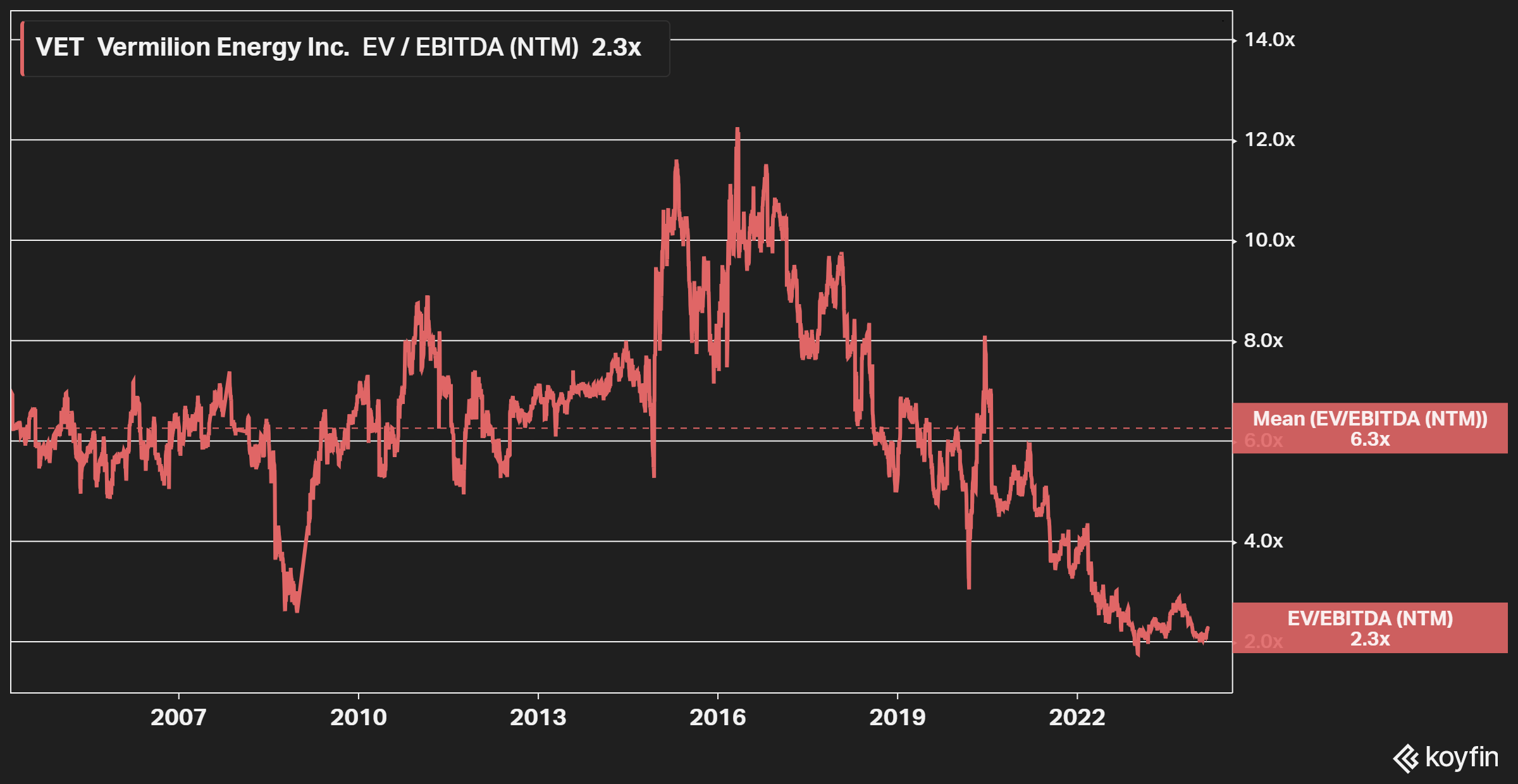

Figure 8 – Source: Koyfin

I don’t necessarily think we will re-rate to a 20-year average EV to EBITDA multiple, but I do think a bounce from current levels is highly likely. The lower the debt level gets and the higher the shareholder distributions will become, the more unsustainable the current valuation will be. The company will distribute roughly 10% to shareholders in 2024, which is a relatively competitive figure among peers, around 3% will be in the form of a quarterly dividend and the remaining portion is likely to be via buybacks.

The windfall profit taxes in Europe are no longer a factor, and I do think energy prices would need to be very extreme in Europe for them to be implemented again. My main concern with an investment in Vermilion is probably another acquisition instead of buybacks and further deleveraging, which would be the low-risk option that the market is looking for given the current valuation.

Q2 2024 Earnings Call Transcript")