photobyphm

Introduction

I had a sell rating on Verizon (NYSE:VZ) in my previous article. At the time, my argument was that Verizon was in a precarious position in the competitive telecommunications industry. Unlike the company’s competitors, Verizon was reporting net customer number reject for both post-paid and pre-paid wireless customers for multiple quarters spanning about two years. As such, I argued that Verizon will have to either boost promotion, cut service costs to entice customers or boost Capex to make Verizon’s products even more attractive. Today, despite my previous argument, I am upgrading Verizon for two major reasons. First, I have been wrong in assessing that Verizon will need to take action in order to address net customer losses. Second, macroeconomic conditions have developed to become extremely favorable for Verizon in the coming quarters as it became likely that interest rates have peaked. Therefore, I am revising my sell rating on Verizon to a buy.

Verizon’s Strategy

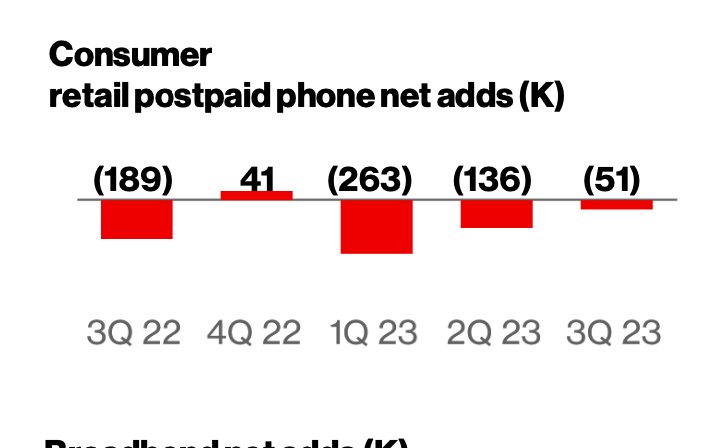

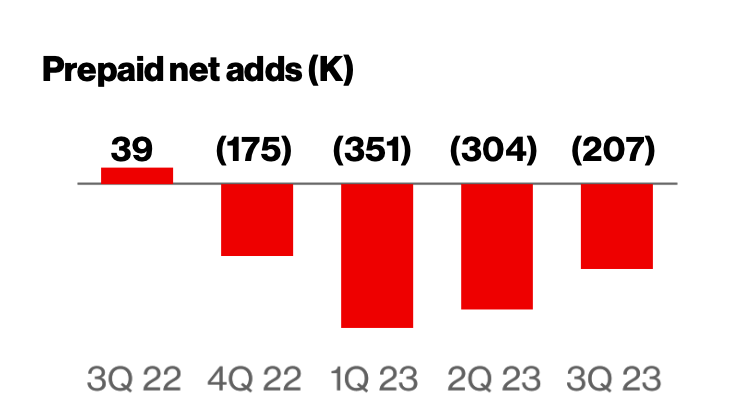

Verizon, for the past few quarters, has been losing customers in both post-paid and pre-paid. As the pictures below show, net losses have been an ongoing problem for Verizon.

Verizon

Verizon

On the other hand, AT&T (T) and T-Mobile (TMUS) have been gaining customers, and these competitors are continuing their customer gains. As such, I have been bearish.

However, I believe I was wrong to assume that the potentially temporary loss of customers was detrimental to Verizon. During the 2023 Q3 earnings call, Verizon’s management team hinted that the company will be expecting a reversal in this trend in 2024. The management team said that the company has made progress in reducing the net losses by saying that the company has “achieved sequential and year-over-year improvement in postpaid phone net adds” before saying that the company has “delivered positive consumer postpaid phone net adds in the month of September.” encourage, the company “expect[s] that [the] momentum will continue as [Verizon is] on track to exceed [the] postpaid phone net adds from Q4 of last year.”

This positive tone from the management team likely comes as a result of the company’s strategy that I failed to foresee. Instead of Verizon competing with its competitors with high promotion offerings, the company chose to focus on providing value to the company’s existing product offers. As the management team puts it, the company puts the “customer at the center [of] everything we do rather than engaging in aggressive promotional activity admire others in the industry.” This has led the company to accomplish a 2.6 net unsecured debt to consolidated adjusted EBITDA ratio showing the strong improvement in the company’s bottom line. In other words, by not chasing customers by throwing promotions, the company was able to reinforce its margins and balance sheet encourage as the customer losses were proven temporary.

Therefore, I believe I was wrong to assume that the declining customers would be sustained without a strong action from Verizon to contend with its competitors leading me to reverse my previous bearish stance on the company.

Macroeconomic Condition

In addition to easing concerns revolving around Verizon losing post-paid and pre-paid customers, macroeconomic conditions are expected to create an immense headwind for the company going forward for the foreseeable future due to the changing interest rate environment.

First, numerous organizations have started to forecast that the Fed will lower the federal funds rate by the end of 2024. The magnitude of the action differs depending on the organization, but unlike in the past few months, more and more organizations are forecasting a reversal as inflation slows, unemployment starts to tick up, and the economy starts to show early signs of cooling. Vanguard, Forbes, Bloomberg, and more organizations are forecasting this future.

It could be the case that the Federal Reserve does not lower the rates in 2024. However, although this is the case, the long-term treasury bond yields could reject significantly as a result of Mr. Market. If the market believes that the Fed will reduce rates in the coming quarters whether or not that is 2024 or not, the market could take into account these changes by driving up the prices of long-term bonds reducing the bond yields. Also, if the market expects the economy to slow or slip into a minor recession or maybe even a slowdown, this could be reflected in the bond market lowering the long-term treasury bond yields.

Whatever the provoke and reason may be, the market already seems to be cautiously expecting bond prices to boost in the near future lowering the long-term treasury yields.

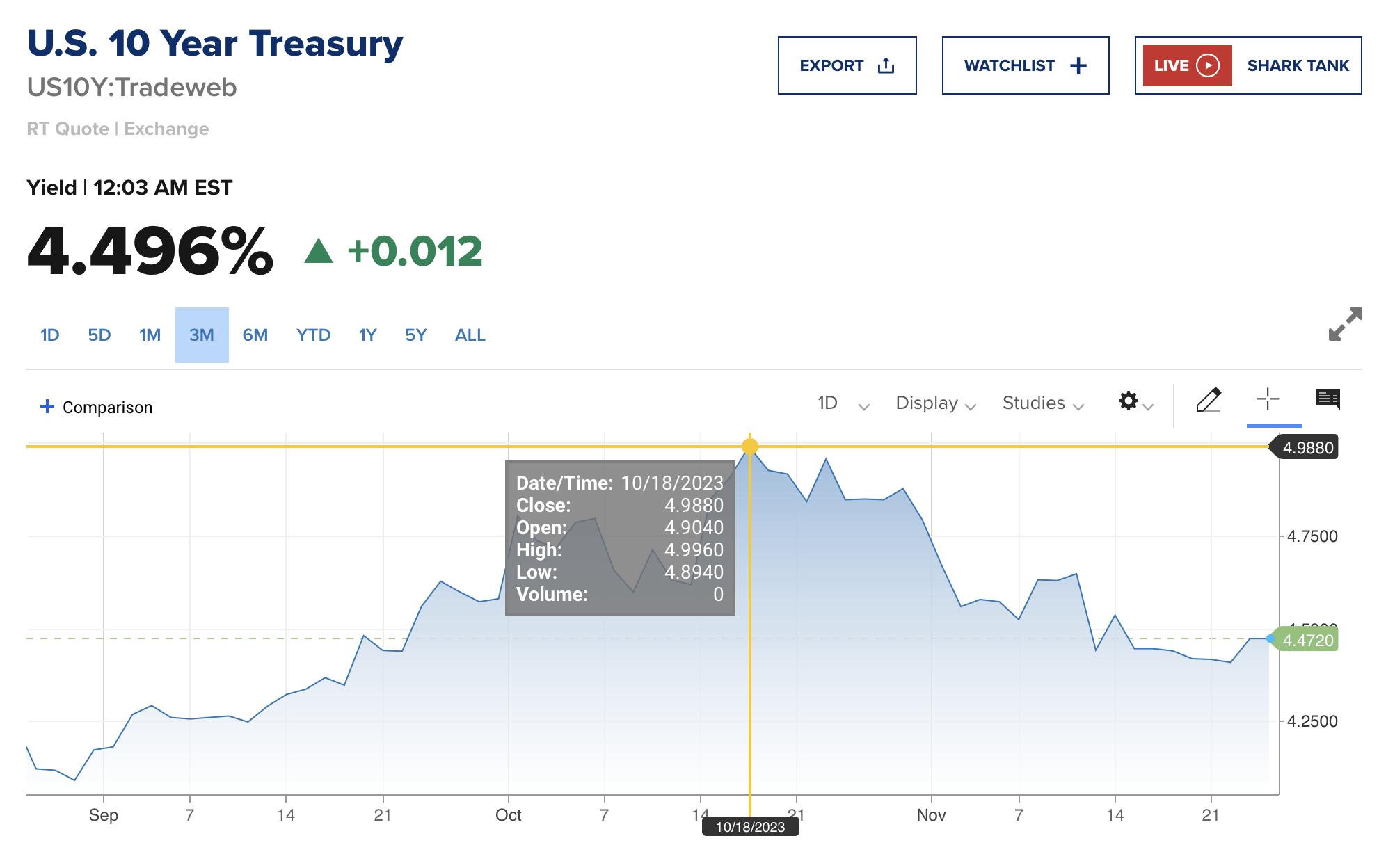

CNBC

As the picture above shows, since the 10-year treasury yield peaked at 4.988, the yield has since declined to about 4.472.

The reject in long-term treasury bonds creates a massive tailwind for Verizon. Both the bonds and Verizon pay coupons or dividends providing a stable cash flow for investors. Inevitably, both dividend stocks and treasury bonds will have to contend for investors’ money, and because it is the case that treasury bonds are safer than any dividend stocks, higher yields make dividend stocks less attractive. This was likely one of the biggest factors pushing down Verizon stock to its lows in the past few months as treasury yields significantly increased until October. Therefore, the potential of the long-term yields trending downward in the coming quarters creates a situation where dividend stocks admire Verizon become much more attractive at lower dividend rates or higher stock prices creating a massive likelihood of a tailwind for Verizon.

Valuation

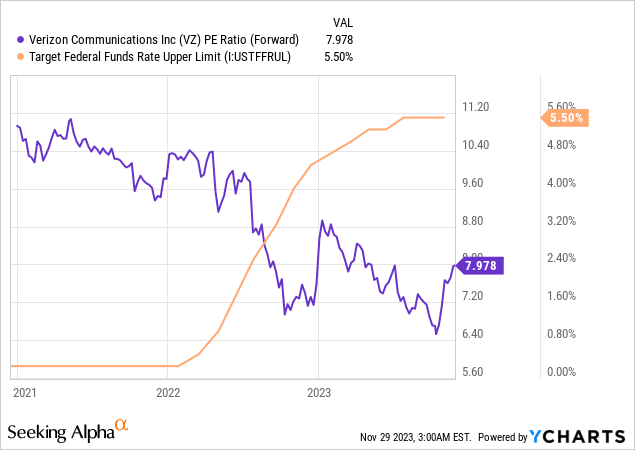

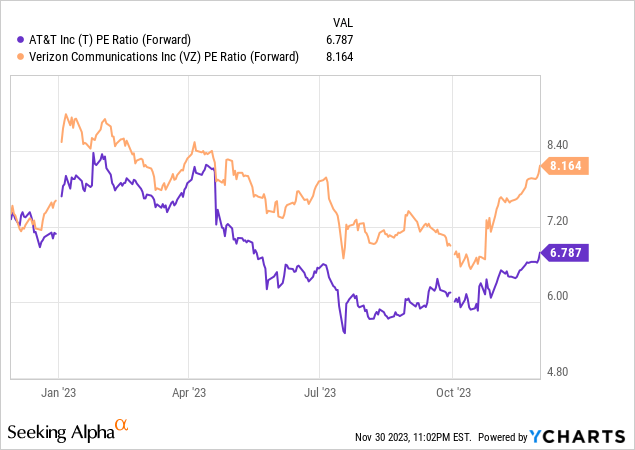

Considering the macroeconomic expectations discussed earlier, I believe Verizon is undervalued today. The company currently has a forward price-to-earnings ratio of 7.98. As the chart below shows, the valuation multiple has consistently trended downward as the interest rates rose following the pandemic.

Thus, I believe it is reasonable to argue that the company’s valuation multiple could return to levels seen before the Federal Reserve started hinting at raising interest rates, which was about 10. Apart from the chart shown above, historical price-to-earnings data also shows that the company’s valuation multiple has fluctuated near 10, a valuable multiple that I believe is achievable and reasonable.

encourage, as the chart below shows, Verizon is similarly valued to its industry peer AT&T. Both companies function a similar business model paying aggressive dividends. Verizon, on the surface, may look slightly more expensive than its peers; however, I believe the market is taking into account both companies’ balance sheets for the discrepancy. AT&T aims to accomplish net-debt to adjusted EBITDA of 2.5 by 2025 while Verizon already enjoys this net-debt to adjusted EBITDA today.

Risks

My bullish thesis heavily depends on the direction of the federal funds rate or the interest rate moving downward, which creates a situation where the Federal Reserve’s actions could significantly impact my thesis. If the Federal Reserve sees that the inflation is not over or that the economy continues to be too strong, it is highly unlikely that they will cut the federal funds rate, and because even renowned investors admire Warren Buffett advised against investing solely based on economic prediction, the unpredictable nature of the economic forecast poses risks to my thesis.

Summary

I was bearish on Verizon as the company was losing customers. I believe that the company will need to entice customers by spending more money to reverse the customer losses. However, this was not the case. Verizon was able to supply value to customers without a significant promotion leading to the management team forecasting a reversal in customer loss trend in 2024. encourage, as the bond yields are expected to show a declining trend in 2024, Verizon, a dividend stock, is expected to become favorable creating a strong tailwind. Therefore, I believe Verizon is a buy.

Q2 2024 Earnings Call Transcript")