seruvenci

Intro

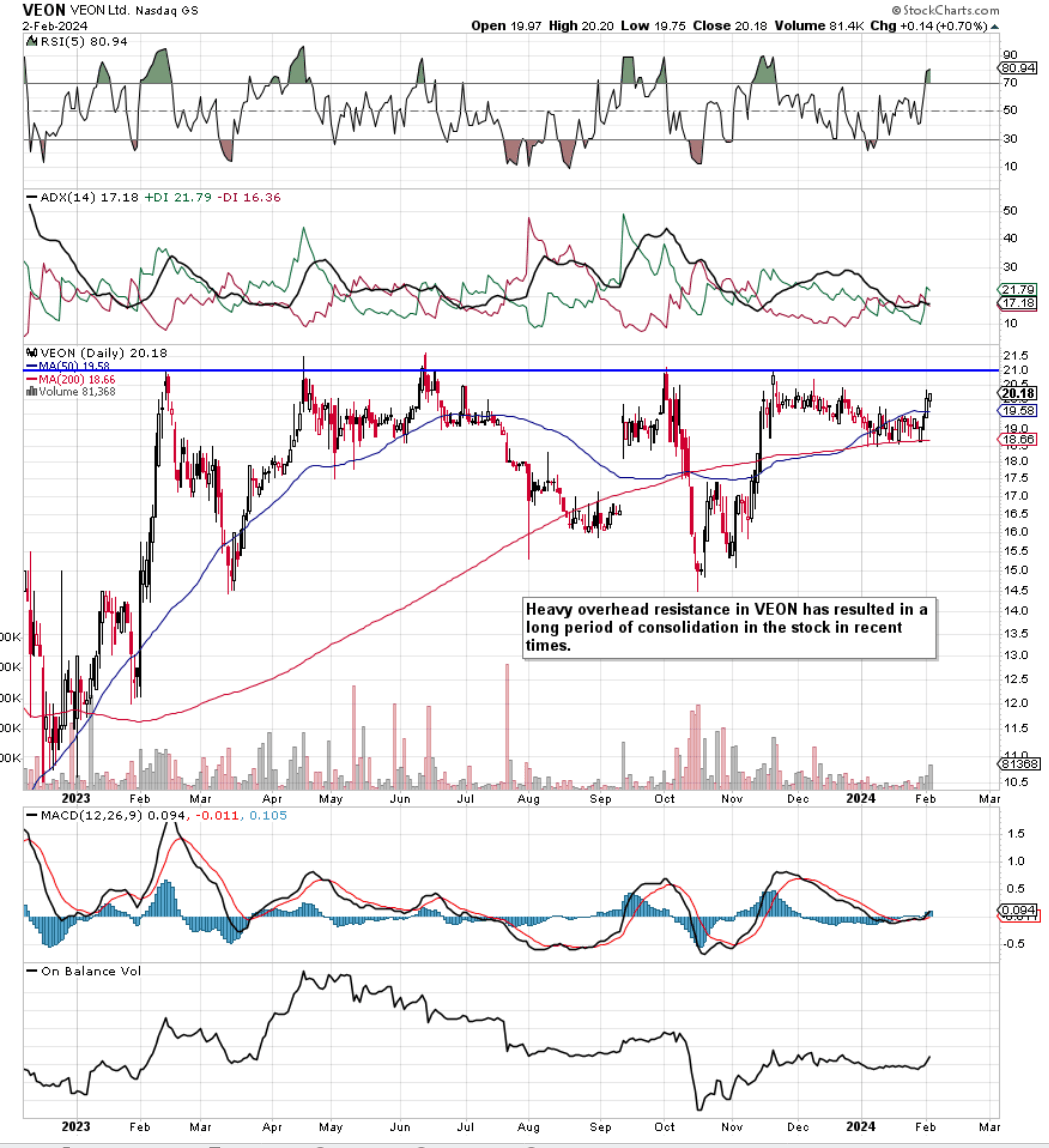

We wrote about VEON Ltd. (NASDAQ:VEON) in June of last year when we downgraded our rating in the stock from a Buy to a Hold employing a technical analysis piece. Although our initial Buy rating in November of 2022 was the right call (shares were trading at $11.63 at the time) pointing to strong upside at the time, the subsequent downgrade in June of 2023 (the stock was trading at $19.74 per share) was also the right call as shares have only managed to increase by approximately 2.2% since that commentary. Although encouraging trends (regarding VEON’s pivot to an asset-light model) were witnessed once more in June of last year, the stock’s technicals pointed to sustained consolidation and that is what has essentially played itself out in the stock over the past 7+ months. As we see below, shares look primed to test the $21 level (approx) once more in due course. Therefore, let’s review VEON’s recent fundamental trends to see if the international digital operator can break through on its next upside attempt.

VEON Technical Chart (Stockcharts.com)

Encouraging Forward-Looking Fundamentals

Given the keen valuation VEON currently trades at, we believe that as long as the company can continue to report sufficient sales, thereby resulting in positive earnings & cash flow, then this very same cash flow can be used to keep on doubling down (investing) aggressively on earmarked growth areas. When looking at core local growth rates, for example, top-line sales grew by close to 20% in the recent third quarter, whereas EBITDA growth was close to the 30% mark. Here straight away, we see margin gains which are a result of effective cost management as well as operating leverage.

Through the effective expansion of 4G combined with the effective rollout of value-adding digital services, the number of more profitable multiplay users continues to increase over time. Furthermore, the retention of these customers is much better, lending itself to much higher growth rates compared to the standard telco operator.

Given Ukraine’s circumstances, for example, VEON looks to be reaping the benefits of continuing its investment in this region through the down cycle. Although capital spending was obviously lower in Q3 (-11%), VEON through Kyivstar was still able to report double-digit EBITDA growth where 4G penetration remains in its initial innings. Furthermore, the success of ‘Jazz’ in Pakistan is a good read on how VEON has reinvented itself in recent times concerning its digital operator strategy. Through popular offerings such as JazzCash & Tamasha, VEON has been able to attract hoards of new users, which continue to drive top-line sales forward. Moreover, Kazakhstan & Bangladesh continue to report growth as a result of sustained 4G penetration & market-share gains.

Excellent growth fundamentals in practically all of VEON’s jurisdictions led management to raise its full-year guidance (where full-year EBITDA growth is now expected to be in the region of 19%) for the second time in November of last year. Suffice it to say, if present growth rates continue, we would be surprised if shares do not break out above the $21 level sooner rather than later. We base this premise on VEON’s present valuation which has changed for the better in recent times.

Balance Sheet Strength

Assets are essentially the roots that birth the tree which means the respective book multiple is the first valuation metric we look at when deciphering VEON’s future potential concerning profitability. VEON’s trailing book multiple comes in at 1.33 which compares favorably with the sector (1.76). Furthermore, given how the company’s capital structure has been overhauled in recent times, VEON’s new asset-light model should lead to further balance-sheet strengthening due to elevated levels of free cash flow being generated as a result.

The sale of the Russian assets transformed VEON where the balance sheet is now much leaner with far less debt compared to before. If we take into account, the Russian operations sale as well as the removal of the company’s October’2023 notes, net debt fell by $5.5 billion at the end of the third quarter of fiscal 2023. Furthermore, the majority of the company’s debt maturities have been rolled out to 2025 and the reported cash position of the company at the end of Q3 came in at $2.2 billion.

Therefore, given the company’s excellent cash position and continued asset sales (approximately 30% of the company’s tower portfolio has been subsequently sold in Bangladesh), we would give VEON the benefit of the doubt here regarding its balance sheet. The company’s net interest expense still comes above 50%, so the balance sheet warrants attention, although debt reduction is certainly trending in the right direction.

Sales Growth

One could state that VEON’s sales metrics look even more attractive as the company’s trailing sales multiple of 0.38 compares favorably with the sector median (1.26). Furthermore, the key here is VEON’s 4G-led multiplay strategy where it believes it has a long runway for growth due to low 4G penetration and strong takeup of the company’s numerous digital platforms. To this point, the CEO made the following points concerning VEON’s growth path which illustrate sustained growth in multiple verticals. Consensus is expecting almost a doubling of bottom-line profits ($6.75 per share) next year.

There are four key additional verticals from our existing self-care applications: education, healthcare, entertainment, and financial services. In each market, we have a variety of applications catering to the needs and desires of our customers. In Q3, we hit 93 million monthly active users, and I’m happy to share that at the end of October, 93 million user number is now above 100 million monthly active users, which shows the dynamism in this vibrant space.

Specifically, we focus in on financial services, entertainment, and self-care app segments. In Kazakhstan, Simply, the country’s only branchless neobank recorded a 2x year-on-year increase in monthly active users. In Pakistan, fintech JazzCash maintains its leading position, boasting 15.4 million monthly active users and a total transaction value of 1.4 trillion rupees, up 39% year-on-year. The decline in monthly active users and number of transactions at JazzCash was due to the post-pandemic era, and discontinuation of zero or negative value accounts, which were impacting profitability negatively.

Our two major entertainment platforms have delivered another quarter of positive user growth. In Pakistan, monthly active users of our Tamasha platform grew 4.4x year-on-year, while Bangladesh’s Toffee recorded a 72.2% increase. We have also smaller entertainment platforms in Kazakhstan, albeit they’re all number one in the countries that they are serving. BeeTV goes from strength to strength, with monthly active users reaching 800,000, a rise of 24.1%.

Moving to our self-service applications, our super app in Bangladesh, MyBL delivered another quarter of double-digit year-on-year monthly active user growth, rising 43% to reach 7.6 million users. We also highlight ongoing penetration gains, app users’ growth, and engagement improvements across all our service platforms, specifically noting 20%-plus growth in monthly active users at MyBeeline Kazakhstan, and Uzbekistan.

Conclusion

To sum up, given VEON’s strong growth curve and strengthening balance sheet, we reiterate that it should only be a matter of time before shares break out above long-term resistance. We are maintaining our ‘Hold’ rating however until overhead resistance gets taken out to the upside. We look forward to continued coverage.

Q2 2024 Earnings Call Transcript")