JHVEPhoto

Since I presented my ‘Strong Buy’ thesis for Veeva Systems (NYSE:VEEV) in June 2023, their stock price has surged by 21%. I discussed their data analytics and AI capabilities in the healthcare industry. They guide 15.5% revenue growth and 27% adjusted operating income growth for FY25. Veeva clinical platform connects clinical operations and data management, supporting healthcare customers in navigating trial collaborations. I think it is an untapped market and could generate long-term growth for Veeva. I reiterate ‘Strong Buy’ rating with a one-year target price of $300 per share.

Untapped Development Cloud Growth Opportunity

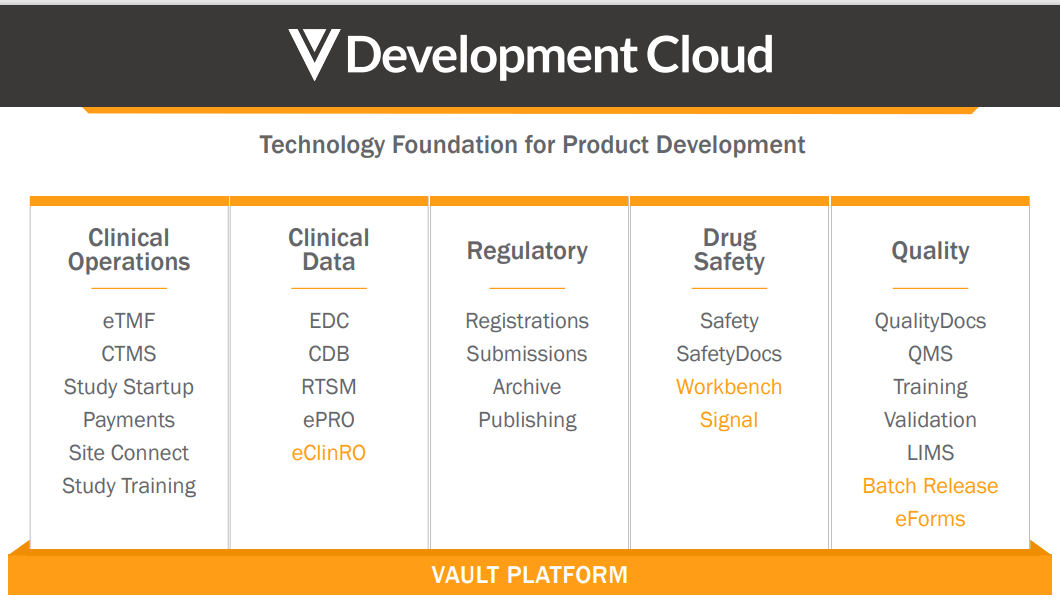

Veeva estimates that the size of its total addressable market is around $20 billion, with Development Cloud accounting for 65% of total opportunities. Currently, Development Cloud represents half of their group revenue, making a significant increase from the 5% level ten years ago. The Development Cloud comprises applications for the clinical, regulatory, quality, and safety functions of life sciences companies. These applications liberate life science companies from traditional Word/Excel spreadsheets. For example, their clinical Veeva Vault Clinical advances trial execution by providing a comprehensive software solution, thereby streamlining the clinical trial process. Their clinical software connects patients, physicians, regulators, and life science companies, and more importantly, Veeva is the sole provider of clinical trial software to life science companies.

I think their Development Cloud could sustain a revenue growth of 20%+ in the near future. The reasons are as follows:

Firstly, the market remains underpenetrated, with Veeva estimating that they have only reached 12% of total addressable market. This suggests a substantial growth runway, particularly in the regulatory/safety, quality, and clinical trial segments.

Secondly, Veeva has been investing heavily in its R&D to develop more applications under its Vault platform, as illustrated in the slide below. These applications have the potential to facilitate the digitalization of day-to-day operations for life science companies, consolidating all data into the Development Cloud. In today’s data analytics landscape, digitalization and IT modernization are quite important for life science industry, in my view.

Veeva Investor Presentation

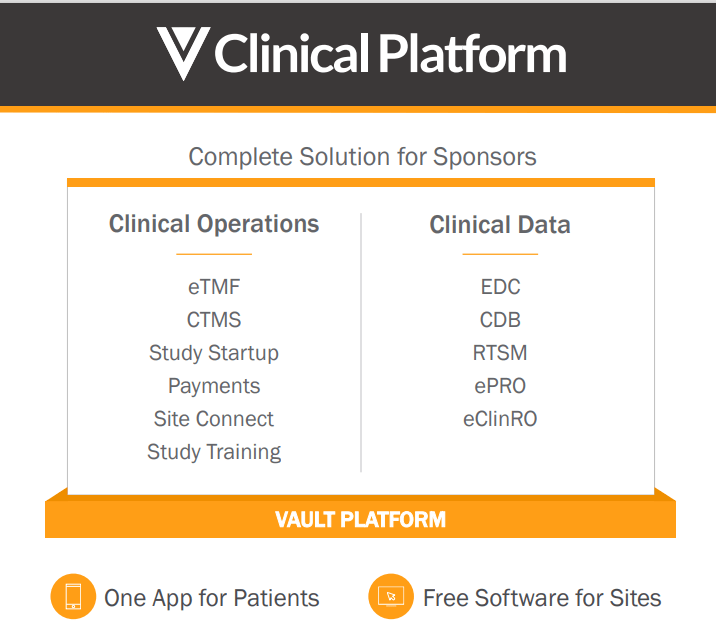

Lastly, I consider Veeva Clinical Platform to be a hidden gem, given Veeva’s monopoly in this sector. Veeva has been rolling out comprehensive solutions for major sponsors, encompassing both operations and clinical data. The unified platform seamlessly connects operations and clinical data, potentially saving significant time in the drug development process. Veeva estimates the total addressable market for clinical to be around $7 billion currently, and they are just beginning to penetrate this market.

Veeva Investor Presentation

Recent Result and FY25 Outlook

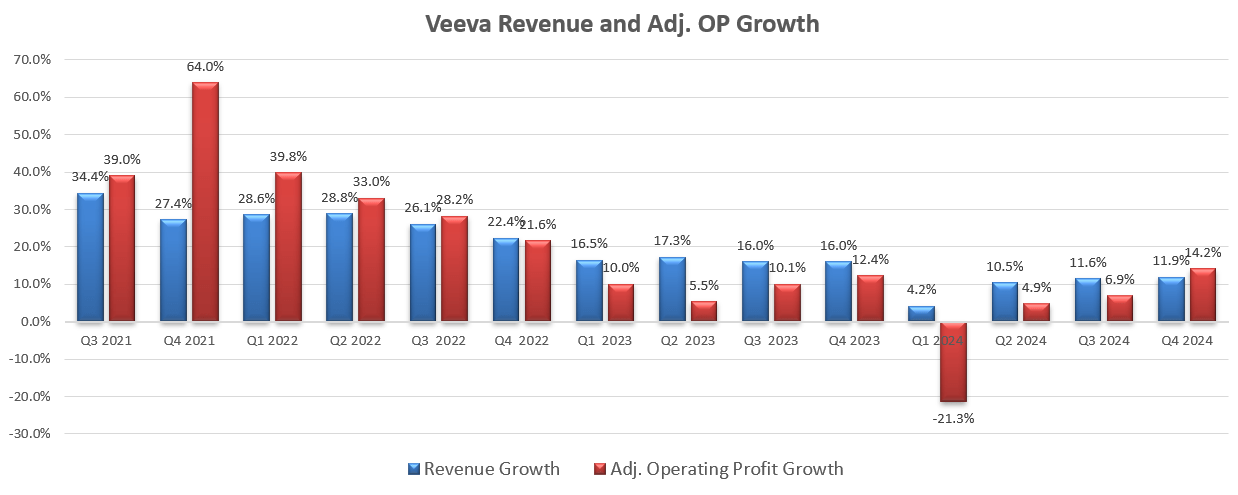

Veeva released its Q4 FY24 result on February 29th, delivering 11.9% revenue growth and 14.2% adjusted operating profit growth. Currently, more than 85 customers have both a clinical operations and clinical data management product from Veeva, as disclosed in the earnings report.

Veeva Quarterly Results

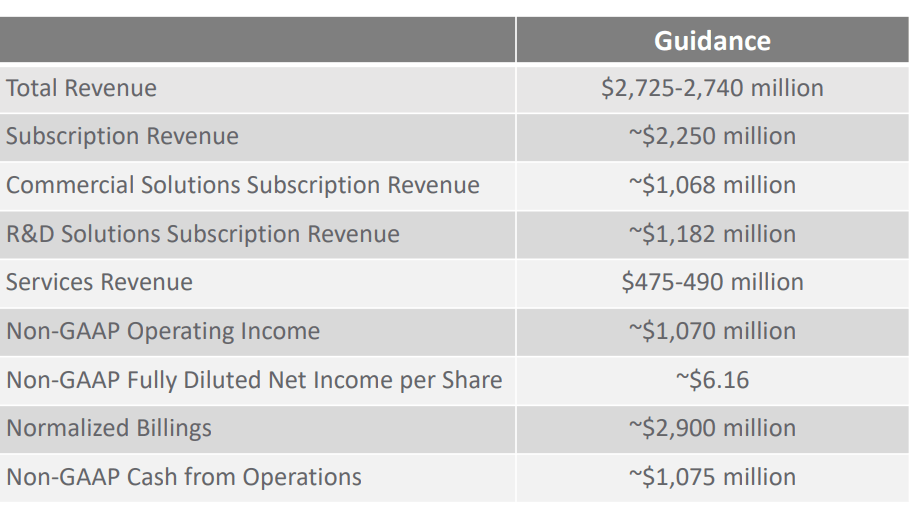

The company ended FY24 with a robust $4 billion cash, equivalents, and short-term investments on its balance sheet, without any debt balances. They generated $885 million in free cash flow in FY24, and all the cash flow has been reinvested back into their business. There is no dividend and share repurchase, quite typical for high-growth companies. For FY25, they guide 15.5% revenue growth and 27% adjusted operating income growth, as detailed in the slide below.

Veeva Q4 FY24 Result

Here is how I think about their near-term growth:

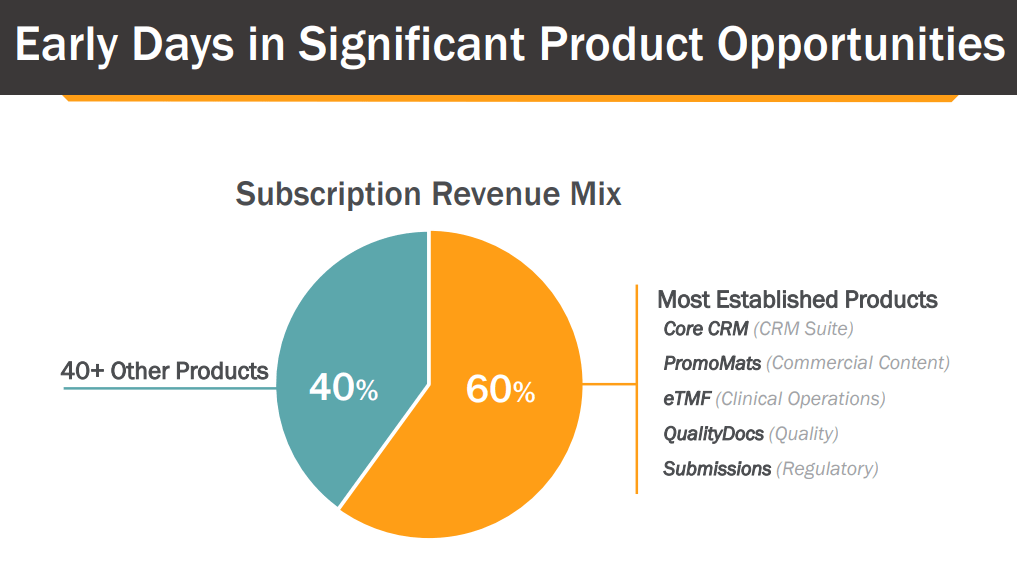

Veeva possesses several established software suits with relatively high market share, including CRM, commercial content, clinical operations, quality, and regulatory. However, there are 40+ other products in early stages of development, with relatively low penetration rates.

Veeva Investor Presentation

Veeva has been strategically investing in expanding its workforce and dedicating resources to R&D, aiming to expand the 40+ products offering under its unified IT platform. These new products could contribute significant growth for Veeva in the near future, in my opinion.

In terms of the end market, biopharma accounts for 94% of Veeva’s total revenue and small biopharma companies represent 25% of biopharma revenue. Consequently, small biopharma accounts for 24% of group revenue. Due to the current high interest rate, many small biopharma companies had to cut operating expenses and reduce headcount hirings. Charles River Laboratories (CRL) specializes in preclinical and clinical outsourcing services to global pharma and biopharma companies. During their latest earnings call, their management expected spending in large biopharma companies to remain stable in 2024, while small and mid-sized companies may continue to spend cautiously due to funding constraints. As such, Veeva’s exposure to small biopharma could pose some growth headwinds in FY24.

Veeva has demonstrated an impressive average revenue growth of 22.6% over the past five years. I anticipate their FY25’s revenue growth rate may be slightly lower than the historical average, mainly due to the challenges posed by small biopharma companies. Having said that, I maintain optimism regarding the long-term growth potential of the biopharma market. The funding environment could potentially improve once the Fed begins to cut the interest rate. Mordor Intelligence forecasts that global biopharma market to grow at a CAGR of 8.07% from 2021 to 2029, driven by stem cells, gene therapies, and other innovative technologies.

In summary, I anticipate Veeva will achieve an 18% revenue growth in the near term, considering the underpenetrated markets, new product offerings, monopoly in clinical trial market, and some headwinds from small biopharma customers.

Valuation

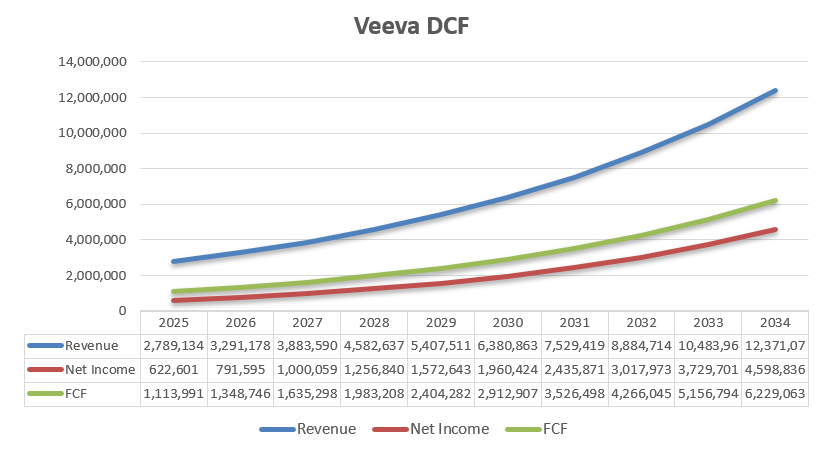

As discussed, I assume 18% revenue growth in the model, leading to an anticipated total revenue of $12.3 billion by FY34 for Veeva. Considering the current TAM of around $20 billion, I believe the revenue growth assumptions are quite conservative.

The gross margin is more likely to expand driven by the increasing mix towards subscription-based services. It is quite common for subscription services to reach gross margin above 90% for mature tech companies. Veeva’s gross margin was only 71.3% in FY24, and I believe their gross margin could improve notably when their business scales. Veeva has been allocating around 25% of total revenue towards R&D, and I don’t expect they are going to reduce their R&D allocation in the near future, as the company is still in the early expansion stage. Putting all the operating expenses together, I project an annual margin expansion of 80 basis points from gross margin, 30bps from sales and marketing leverage, and another 30bps from G&A expenses.

Veeva DCF- Author’s Calculation

The free cash from equity (FCFE) can be calculated as detailed in the following table.

Veeva DCF- Author’s Calculation

The cost of equity is calculated to be 13.5% for Veeva with the following assumptions: risk-free rate: 4.22% (U.S. 10-year gov yield); market risk premium: 7%; Beta: 1.33 (SA’s 24-month data).

Discounting all the FCFE at a discount rate of 13.5%, the one-year price target is estimated to be $300 per share for Veeva in the DCF model.

Key Risks

Stock-based compensation: similar to other high-growth companies, Veeva has been allocating more than 16% of total revenue towards stock options. The SBC expenses as a percentage of group revenue have seen a significant increase from 8.9% in FY19. Investors need to monitor their stock-based compensation going forward, as these SBC expenses could affect their reported operating margin.

IQVIA (IQV): Veeva is competing against with some legacy players like IQVIA in the commercial cloud and data cloud markets. Veeva filed antitrust lawsuits against IQVIA in 2017, as IQVIA prohibited customers from uploading healthcare data to Veeva Network Customer Master system. The ultimate outcome of this lawsuit remains uncertain at this moment and I expect it will take years for the final settlement.

Dear Readers:

I’ve been a shareholder of Veeva for over 7 years now. One of my friends asked me what stock you will own if the market is going to be closed for ten years. I answered Veeva without any hesitation. I am confident that they are going to thrive in the attractive pharma and biopharma markets, and I believe their software applications have the potential to set the golden standard in the life science industry. I reiterate ‘Strong Buy’ rating with a one-year target price of $300 per share.

Q2 2024 Earnings Call Transcript")