Jacob Wackerhausen

Varonis (NASDAQ:VRNS) provides a comprehensive platform that empowers organizations to secure their critical information, addressing various threats through its software suite, including unauthorized access, insider threats, and accidental leaks. Varonis achieves this by classifying data, controlling access, monitoring user activity, detecting threats, and preventing leakage.

The company went public on NASDAQ in 2014 at $14.67 on debut day. Share performance has been volatile, though trending up overall. The all-time return measured today stands at 210%, with the stock trading at $45.5. Since last year alone, VRNS has appreciated by 74% due to positive market sentiment. The momentum appears to have continued YTD, where VRNS has posted a 2.3% return.

I initiate my coverage with a buy rating. My modeled target price indicates that VRNS is undervalued at its current price of approximately $48.6.

Catalyst

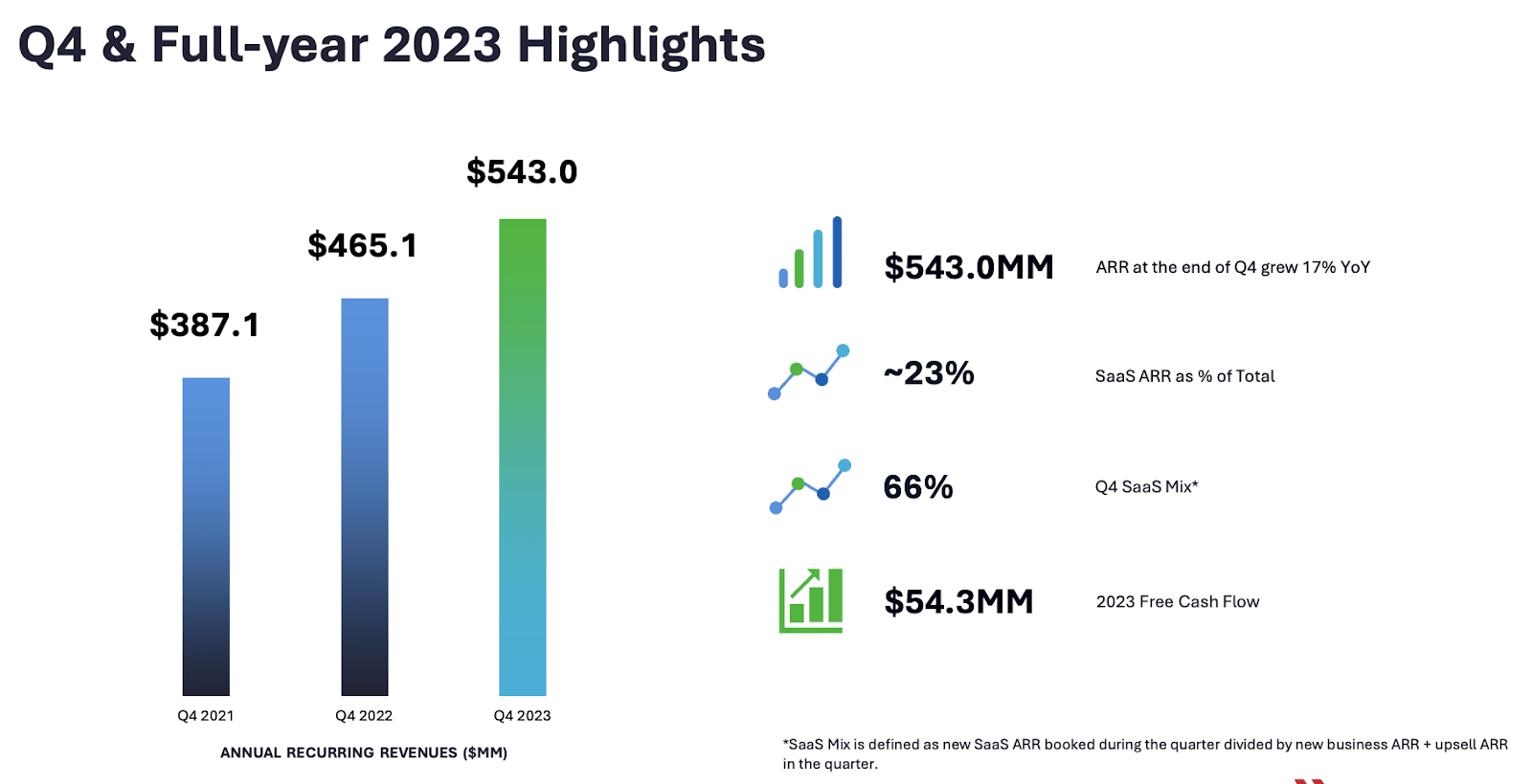

There are a few catalysts on the stock into FY 2024 and beyond. As a start, I believe that the fundamentals are decent. Despite the challenging macro situation, ARR / Annual Recurring Revenue still grew by 17% in FY 2023. Annual FCF / Free Cash Flow has also been on a significant upward trend, going from -$36 million post-pandemic to a breakeven in FY 2022. For FY 2024, VRNS will even expect $70-75 million of FCF.

balance sheet (10-K)

The liquidity position is relatively strong, with cash and short-term investments of over $700 million as of FY 2023. Aside from over $60 million of tax payments related to equity awards and share repurchases, there has not been any sizable use of cash that has been out of the ordinary over the past two years.

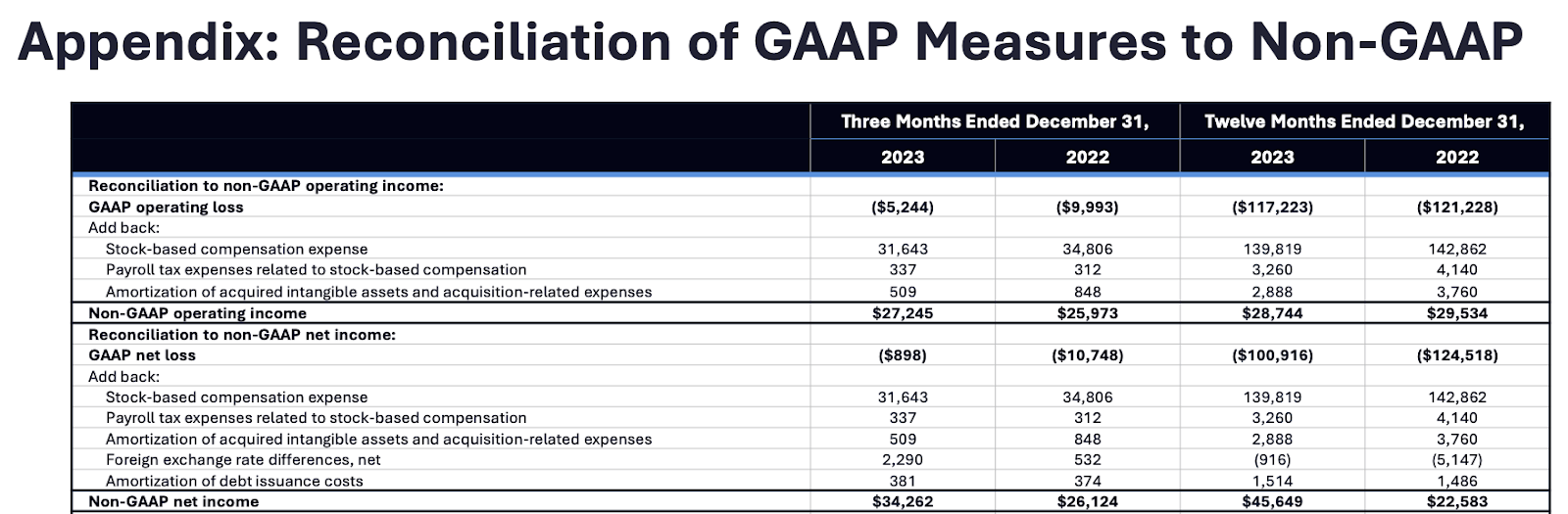

GAAP and non-GAAP (company presentation)

Profitability has improved, though still a bit far from breakeven. The 18% narrowing loss in GAAP net income has also lifted the net margin, which also saw a YoY improvement in FY 2024.

Into 2024 and beyond, I believe that VRNS’ growth, profitability, and cash generation will improve further due to the growing demand for its offerings, driven by the following factors: 1) sustained trends in enterprise hybrid deployments which will benefit SaaS adoptions, 2) increasing enterprise data usage, and consequently cyber threats, due to secular growth trends in generative AI, and 3) more stringent regulatory environment regarding disclosure on cyber security threats and breaches.

Q4 and FY highlights (company presentation)

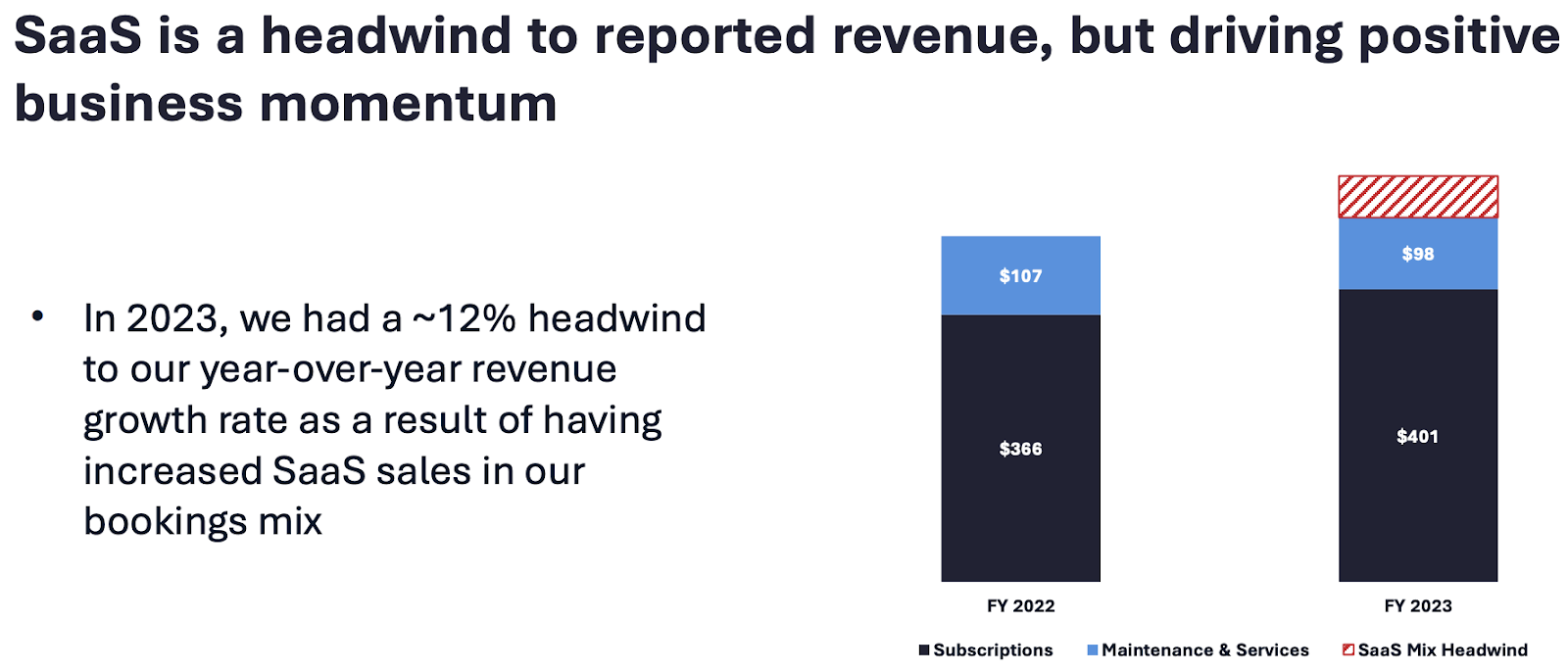

Since announcing the SaaS transition in 2022, VRNS has grown its SaaS share of ARR to 23%, with the SaaS mix making up 66% in Q4. Overall, this highlights the growing demand for SaaS by VRNS’ enterprise clients, which is driven by the need to be more agile and cost-efficient.

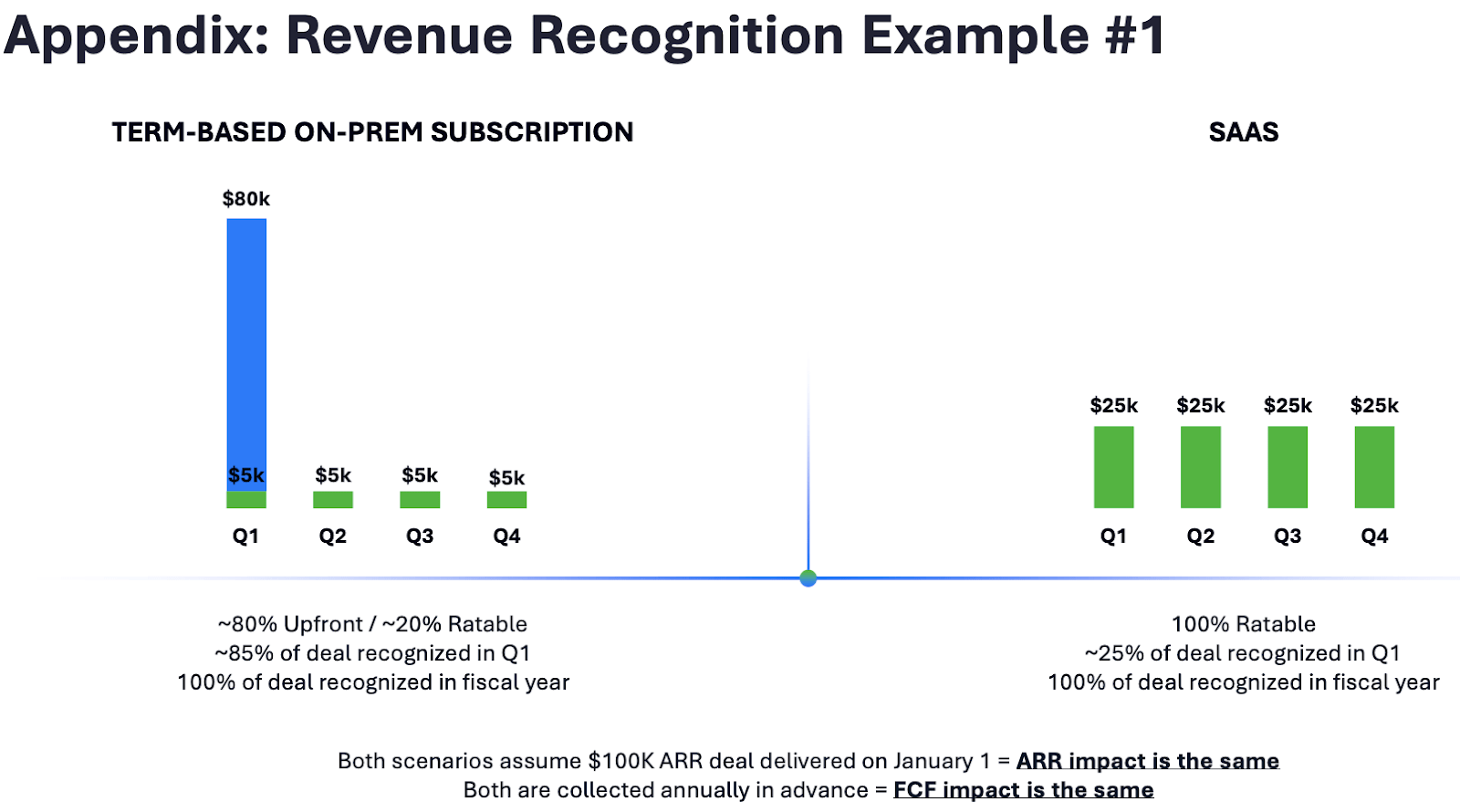

revenue recognition (company presentation)

SaaS are often billed on a pay-as-you-go basis, which can help businesses reduce upfront capital expenditures and ongoing maintenance costs. It also provides enterprises a flexibility to have low-friction access and trial of new innovations, benefiting from future products of VRNS. Therefore, with increasing SaaS adoption, I believe that VRNS’ $1 billion ARR target in 2026 should be achievable, fueled by more cross-sell and upsell opportunities and TAM expansion. Given the low-friction access, VRNS will also benefit from lower renewal costs, which should drive margin expansion.

The recent launch of its MDDR (Managed Data Detection and Response) offering, for instance, also presents immense potential to boost both sales and margin expansion, particularly in regions with limited IT security expertise, in my view. Its pricing structure seamlessly integrates with existing margins, further enhancing its appeal:

It can help with the opportunity to upsell additional platforms that a customer would see the value and would want to be protected on multiple platforms. And at the same time, it’s so appealing and for customers that it can actually help with closing rates. So I think the MDDR has an option on all of those fronts. The way we’ve structured the comp plan in 2024 makes it a no-brainer for our reps to introduce it to our customers. So I expect the adoption to be extremely healthy this year. And I think it’s a benefit for our customers, but also a significant benefit for us as an organization.

Source: Q4 earnings call.

VRNS platform (company presentation)

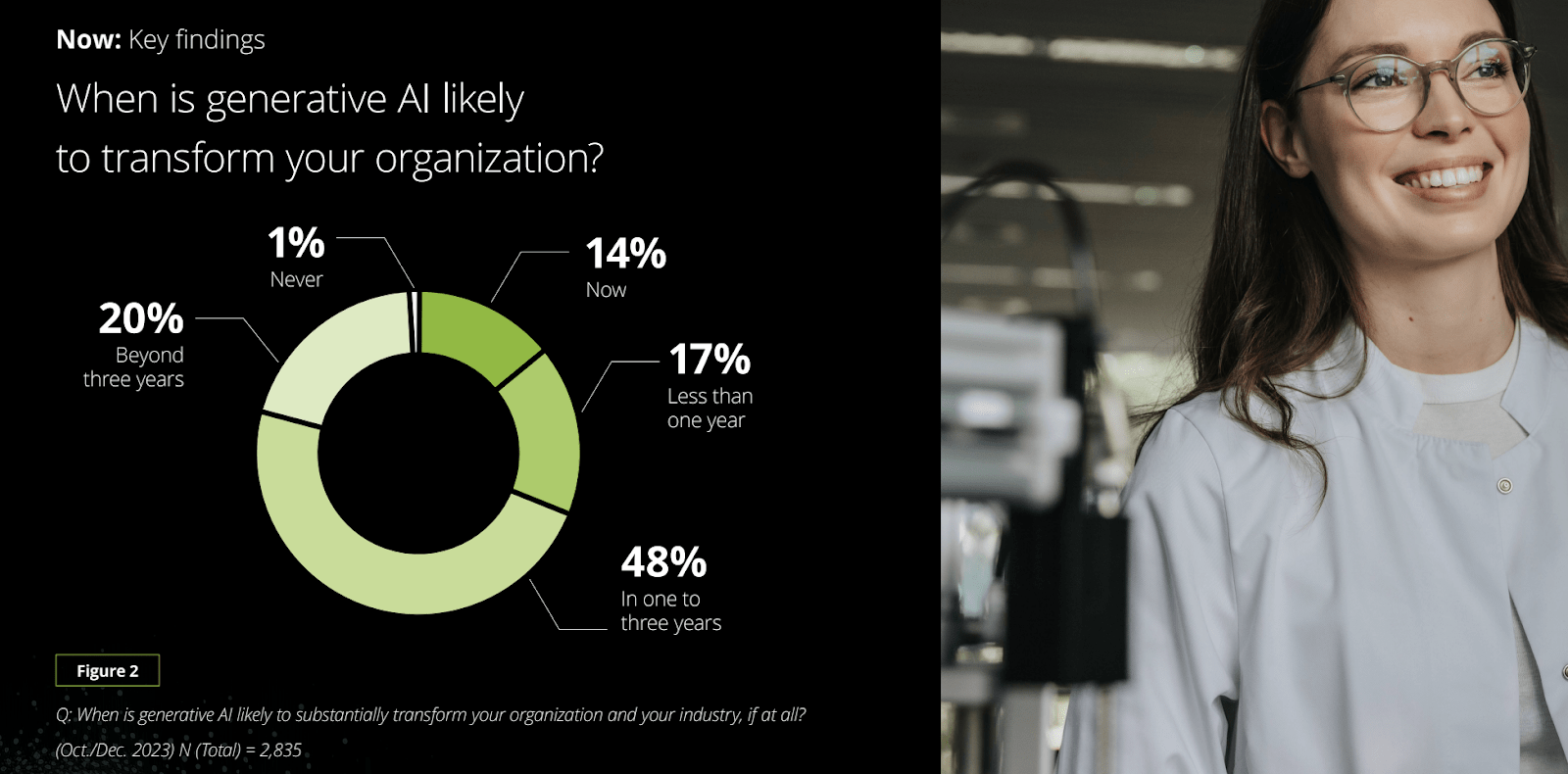

Meanwhile, I expect enterprise data usage to increase substantially into the next decade, driven primarily by the growing adoption of generative AI features across various enterprise work applications. Enterprise will look to mitigate potential cyber threats from the pile of unstructured data from these applications. This will create demand for VRNS’ offerings, which aim to solve exactly those problems.

enterprise AI trend survey (Deloitte)

The demand will come sooner than later. A survey by Deloitte in its report about enterprise generative AI trends in 2024 suggests that almost half of enterprises surveyed will expect to adopt generative AIs in the next 1 to 3 years, in line with VRNS’ $1 billion ARR target.

In the end, I expect the increasingly stringent SEC regulations about cybersecurity breach disclosure to serve as another latest catalyst for VRNS. In short, the new SEC rule announced in December 2023 requires public companies to report major cyberattacks within four days and also explain their overall cybersecurity plan every FY.

This creates a significant tailwind for VRNS offerings, as evidenced by a recent customer win in Q4 – a real estate company impressed by VRNS’ automatic data protection capabilities compared to competitors. This incident also highlights the potential for larger deals driven by regulatory pressure on publicly-traded companies.

Risk

In my opinion, while the secular growth prospects have made VRNS appealing, investors must be mindful of certain risks.

First off, I believe that data security is a broadly defined market with fierce competition, with established players like McAfee and emerging players like CrowdStrike (CRWD) vying for market share with their differentiated solutions in specific areas. While CRWD is well-known for its endpoint protection products, it has also been actively expanding into data protection, an area within VRNS’ target domain. Meanwhile, there is also a threat from a cloud ecosystem-specific player like AvePoint (AVPT), which appears to compete more closely with VRNS in the data protection space.

Another thing to watch is VRNS’ bottom-line performance. While operating and net loss have narrowed in FY 2024, I expect VRNS to maintain its offensive stance to gain market share, which may impact its bottom-line. What we have observed in its financial performance is also reflected in VRNS’ overall position on strategic direction:

So when you look at kind of our philosophy over the last couple of years, we’ve been very focused on the top line growth and wanted to make sure that we show margin leverage and free cash flow generation.

Source: Q4 earnings call.

In my opinion, while investments in growth are necessary, there is a risk that it would leave VRNS vulnerable. The company’s reliance on large deals makes it particularly susceptible to such headwinds. As seen in Q4, while VRNS has benefited strongly from the secular catalysts, the ongoing macro slowdown still resulted in a longer sales cycle for VRNS in FY 2023. I found it unlikely for the macro situation to change drastically in FY 2024, suggesting the need for a more disciplined approach, which VRNS needs more today to avoid sales execution issues that may lead to any top-line guidance miss or challenging share performance.

Additionally, share dilution due to stock-based compensation has been significant, and VRNS may struggle to justify this dilution if growth falters. On a diluted basis, the number of shares outstanding is already over 16% higher than those of basic shares.

Valuation/Pricing

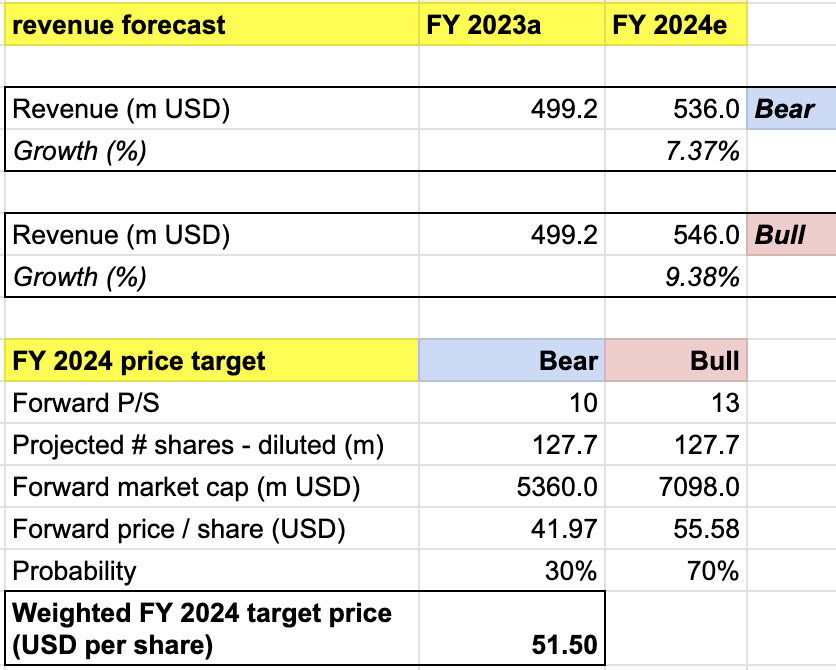

My target price for VRNS is driven by the following assumptions for the bull vs bear scenarios of the FY 2023 projection:

-

Bull scenario (70% probability) assumptions – VRNS to achieve the high end of its FY 2024 guidance of $546 million of revenue, representing a 9.4% growth. I believe that this performance could reward VRNS a 13x P/S, the peak valuation multiple since the beginning of 2022. This situation presents the best-case outlook for VRNS.

-

Bear scenario (30% probability) assumptions – VRNS to deliver a revenue of $536 million in FY 2024, a 7.4% growth. I would expect growth to slow down in FY 2024 due to sales execution issues or lengthened sales cycle due to worsening macro situation. I assign VRNS a P/S of 10x, where it is currently trading.

target price model (own analysis)

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of $51.5 per share, suggesting an over 6% upside from the current price level.

ARR (company presentation)

I rate the stock a buy. Despite the seemingly minimal upside, there is an important consideration. Due to VRNS’ SaaS transition, the reported revenue growth will appear slower than the actual momentum experienced by the business. In this case, looking at ARR growth may be more indicative of VRNS’ performance.

So far, the 17% YoY ARR growth in FY 2023 and the projected 14% – 15% ARR growth in FY 2024 are relatively solid, in my opinion, especially under a weak macro situation. Plugging in 14-15% FY 2024 growth to revise my model yielded an upgraded upside of over 11%.

Conclusion

Taking the overall macro outlook and the fundamentals of VRNS into account, I conclude that VRNS is a decent buy. The company boasts impressive share price gains (210% all-time, 74% last year) and continues to thrive in 2024 with projected ARR growth of 14-15%. My 1-year target price model projects 11% upside, making the stock appear undervalued today amidst market weakness. There are several minimal risk factors, but VRNS will continue to benefit from secular growth trends, making it an attractive long-term investment.

Q2 2024 Earnings Call Transcript")