Luis Alvarez

Valvoline Inc. (NYSE:VVV) operates vehicle service centers in North America. VVV looks like a great buy right now. It has given a solid breakout, and the Q1 FY24 results were strong. In addition, the guidance suggests the management is expecting strong growth. So, I believe the market must have liked the results and future growth expectations, and as a result, its stock price has started to rise. I believe VVV can be rewarding; hence, I assign a buy rating to it.

Financial Analysis

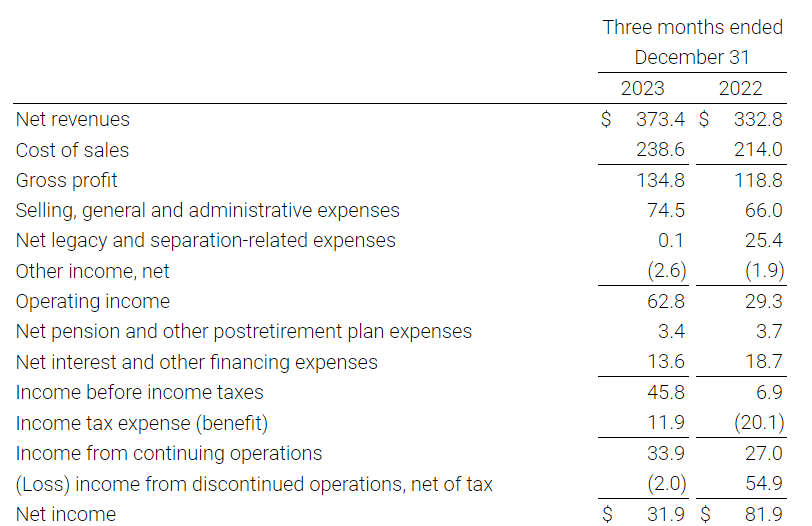

VVV recently posted Q1 FY24 results. The net revenue for Q1 FY24 was $373.4 million, a rise of 12.1% compared to Q1 FY23. The major reason behind the improvement was a 7.1% growth in its system-wide same-store sales. The company’s same-store sales grew by 6.1% in Q1 FY24 compared to Q1 FY23. The franchise same-store sales grew 8% in Q1 FY24 compared to Q1 FY23. The main reason behind the franchise’s growth was higher non-oil change revenue. The operating income margin in Q1 FY24 was 36.1%, which was 35.7% in Q1 FY23. The improvement in margin was mainly due to a low attrition rate and high pricing.

VVV’s Investor Relations

Its adjusted net income and EPS were 36% and 81% higher in Q1 FY24 compared to Q1 FY23. In my opinion, the quarterly results were solid because of the solid growth. The management is aggressively expanding its business. It added 38 new stores in Q1 FY24, which shows the growth intent of the company. In addition, the labor retention rates were high in this quarter, and if the labor-management continues to remain strong, then the margins in the coming quarters will be quite strong. If the retention rate is low, then the company has to bear extra expenses in terms of labor training and recruiting costs. So, considering its current situation, the scope for revenue and margin growth looks bright. Additionally, inflation seems to be under control in the U.S., which will be a tailwind for the company, and the penetration in the nonoil change service is proving beneficial for them as the company is seeing growth in this area. So, the penetration of the nonoil change service can benefit both the franchise and the company’s store sales.

2023 Investor Presentation

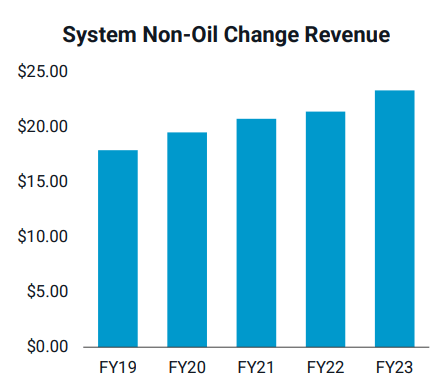

The above chart shows that the trend in the nonoil change revenue has been positive, and the management has stated that the nonoil change service was one of the major growth contributors in this quarter in the company’s same-store and franchise side as well.

Technical Analysis

Trading View

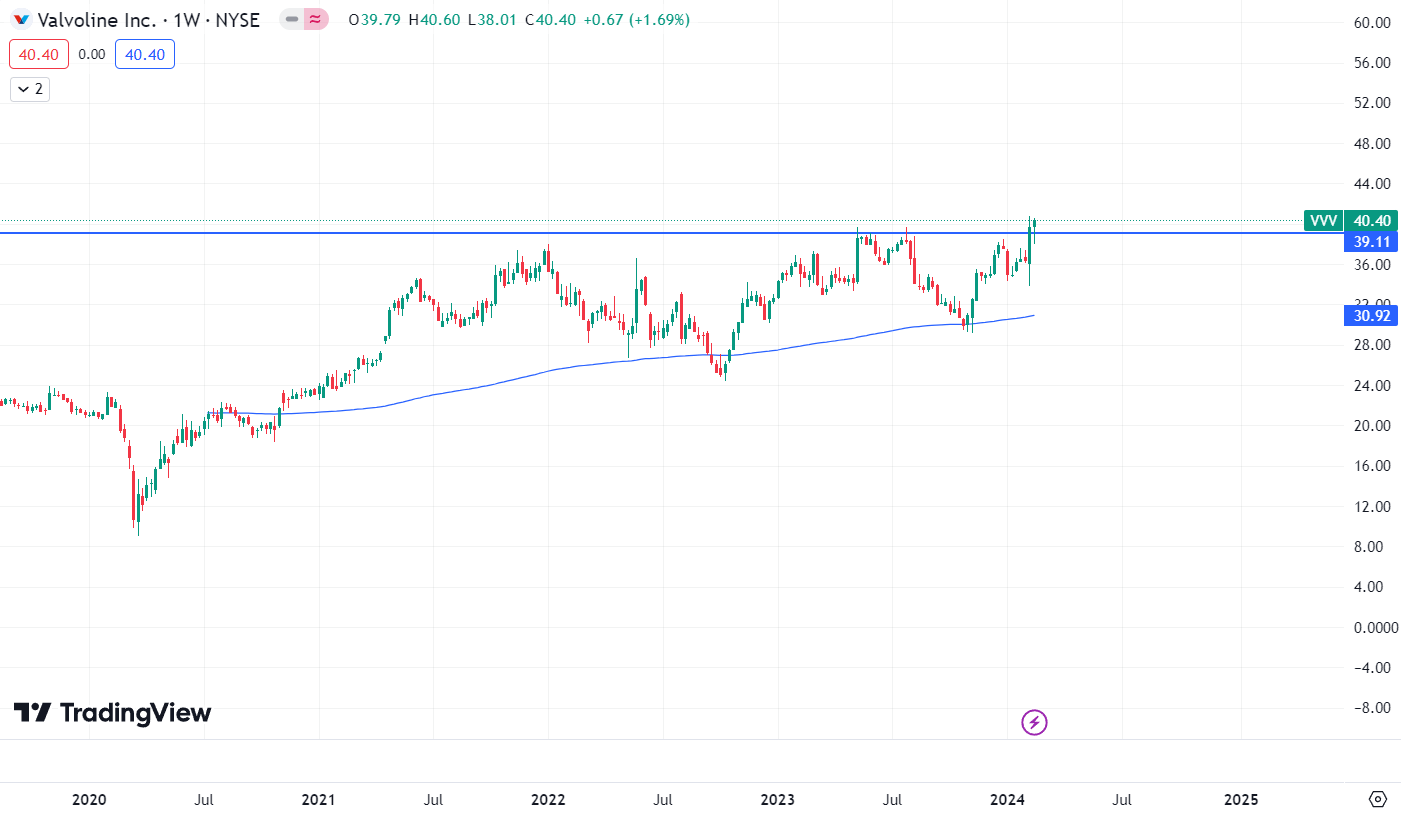

VVV is trading at $40.4. After looking at the chart of VVV, it seems like a big move is around the corner. This stock looks quite bullish because it is trading at its all-time high, and recently, the stock has broken the range of $39 after two years. So, a stock is likely to give a solid run-up if the breakout has happened after a long time, and in this case, the breakout has happened after two years. So, the stock might give a strong run-up. I wanted to publish this article last week because the breakout had occurred last week, but I waited for another week because I wanted to see if the breakout was genuine because several times, investors get trapped in a fake out. But in this case, after the breakout candle, the next candle was a green candle. Hence, it looks like the breakout is genuine, and looking at the price action, I think it can give solid returns. So, I am bullish on VVV.

Should One Invest In VVV?

The quarterly results were solid, and the technical chart also looks bullish. Now, looking at its valuation, VVV has a PEG [FWD] ratio of 0.65x, which is lower than the sector median of 1.59x. However, it trades at a higher P/E than the sector median. It has a P/E [TTM] ratio of 29.52x, and the sector median is around 17.89x. I believe the high P/E ratio is not a matter of concern because the revenue growth it is experiencing is strong, and the guidance suggests that the management is expecting solid growth throughout FY24. The revenue guidance for FY24 is around $1.65 billion, which is 14.5% higher than FY23 revenues. So, the solid growth expectations, along with healthy margins, can boost the EPS. So, I think we might see it trading at a lower P/E in the coming quarters. Now, if we compare VVV to its peers, we can see that it has been outperforming them. I will compare it to three similar companies: AN, ABG, and AAP. VVV has a revenue growth [YOY] of 15.80%, whereas its peers AN, ABG, and AAP have a revenue growth [YOY] of -0.13%, -4.09%, and 1.97%. So, the growth VVV is experiencing is solid because its peers have been struggling, whereas it has recorded solid revenue growth. Although VVV is trading at a higher P/E compared to its peers, I think VVV is aggressively expanding its business. Its total store count has reached 1890, and the management has stated that it has a goal to take this number to 3500. So, although its P/E might look a bit high now, I think it might not look expensive in the coming times due to the expansion of its business, not to mention that high-growth businesses generally trade at a higher P/E. Hence, considering the strong breakout, quarterly results, and positive guidance, I think VVV has solid potential and can be a great buy. So, I assign a buy rating on VVV.

Risk

A number of uncontrollable factors, such as the quantity and age of vehicles in use, regulations and laws, technological advancements in the automotive sector, and engine technology advancements—like the rate at which alternative or electric engine technologies are adopted, shifting OEM specifications for automobiles, and longer recommended service intervals—may have an impact on the demand for Valvoline’s services. Additionally, consumers may put off auto maintenance during downturns in the economy, such as recessions. Similarly, a decrease in miles driven could result in reduced wear and tear and a decrease in the need for maintenance, which could prompt customers to postpone using Valvoline’s services due to rising energy prices or other considerations. The issues above can negatively affect Valvoline’s overall financials by causing a drop in the demand for its services, as they impact measures like drain intervals and vehicles treated per day.

Bottom Line

VVV looks like a solid buy right now. It has broken its all-time high, and the stock price has started to sustain above the breakout level. In addition, its quarterly results were solid, and the future growth expectations are strong. So, considering these factors, I think VVV can be a great buy right now, which has the potential to deliver solid returns to its investors. So, I assign a buy rating on VVV.

Q2 2024 Earnings Call Transcript")