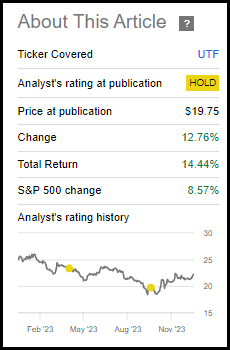

Written by Nick Ackerman, co-produced by Stanford Chemist.

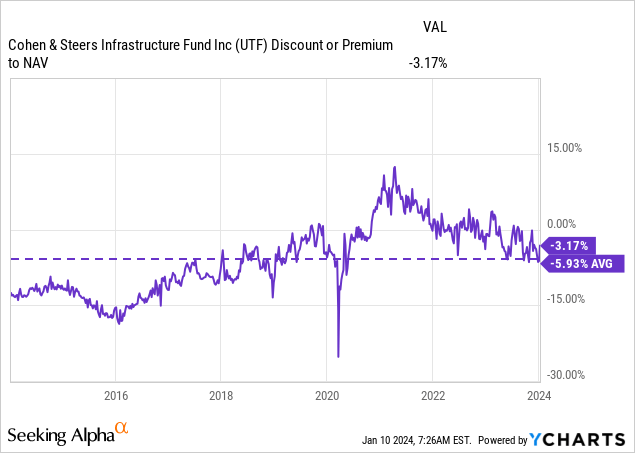

The last two months of 2023 were good for the overall equity space. Cohen & Steers Infrastructure Fund’s (NYSE:UTF) share price was lagging behind the fund’s underlying performance, and that created quite an attractive discount. However, that discount recently has started to close thanks to a much stronger share price performance in the last couple of days.

Over the long term, UTF still remains a solid closed-end fund, or CEF, worth considering for infrastructure/utility exposure. However, those willing to be more patient may benefit from waiting to pick up shares at a larger discount. If we get some market disruption after such a strong run, that could create further potential opportunities.

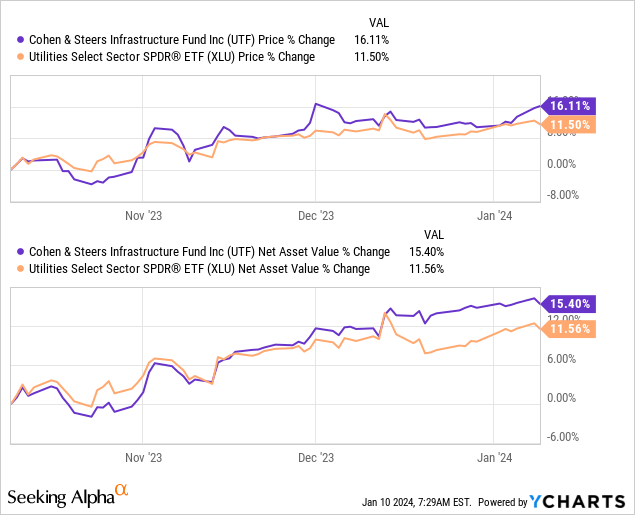

Since the last time we covered the fund, it was during the last October market swoon, and it has performed quite well. The current discount is slightly wider than it had been in our previous update.

UTF Performance Since Prior Update (Seeking Alpha)

“total return, with an emphasis on income through investment in securities issued by infrastructure companies.” They define infrastructure companies as those that; “typically provide the physical framework that society requires to function on a daily basis and are defined as utilities, pipelines, toll roads, airports, railroads, marine ports and telecommunications companies.”

They aren’t limited to where they can invest globally or in what part of a company’s capital stack. That gives them both geographic exposure and asset class flexibility to invest where they see fit. The fund also employs leverage, which adds to volatility and risk. However, it can also add to the potential upside.

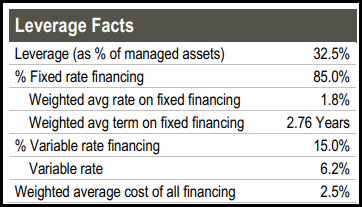

This leverage does come with a cost, and when that is included, the fund’s total expense ratio climbs to 3.72%. That was as of their last semi-annual report, and that was also a climb from the 2.44% total expense ratio for the year-end 2022.

Interest rates look set to be cut by the Fed in this coming year, which could provide some relief for the costs of leverage for UTF. On the other hand, they never really felt the full brunt of the higher-rate environment anyway. This management team smartly hedged the majority of their interest rate costs through interest rate swaps. In fact, they are still hedged for several more years without having to worry significantly about the higher costs of borrowing.

UTF Leverage Stats (Cohen & Steers)

Solid Long-Term Fund, But Catch It At A Better Discount

When the equity market started to rally from the October market correction, it took a lot of interest-rate sensitive sectors with it, such as utilities and real estate sectors. Of course, this broad rally was the primary result of expecting the Fed to have essentially announced that the pivot has happened. They are no longer anticipating rate increases but decreases coming in the next year. That sent the risk-free Treasury Rates tumbling. Therefore, it allows other income-oriented investments to rally and makes equities look more appealing overall.

That being said, UTF’s recovery did stall out more recently – not its underlying portfolio but the fund’s actual share price. The fund’s underlying portfolio had been able to outperform the Utilities Select Sector SPDR® Fund ETF (XLU) for the last three months during its recovery. Still, its actual share price followed more closely with XLU. UTF is much more than XLU. XLU has a narrow focus of mostly larger U.S. utilities only, but this can still provide some good context for the infrastructure space in general.

When this occurs in a CEF, we naturally see a discount start to open up. That’s often a time to exploit the opportunity and initiate or add to one’s position. The discount has narrowed since and it didn’t take long for that discount to shut, that sometimes is the case, but a “Buy” level for me would be watching for a 5% or greater discount.

Therefore, while this is a solid fund, I wouldn’t necessarily look at being overly aggressive with adding at this time. Most investors who are already holding may hold off adding more for now unless you are looking to beef up more infrastructure in your portfolio overall. The last several years were more of the outlier as well, where it traded at some premium pricing.

What also helps my more optimistic viewpoint is that I suspect utilities will do better throughout 2024. They were the worst-performing sector of 2023. Energy and consumer staples also produced negative results, but utilities declined by more than double, even those weak-performing sectors.

The sector is primarily weighted toward NextEra Energy (NEE) at an over 13% weighting in XLU. So, if NEE performs well, it will mean a stronger sector performance overall. NEE is also the largest holding of UTF.

In particular, a couple of catalysts for the sector to perform better rather than simply because it’s cheaper now would be a weaker economy. If the Fed is cutting rates, it’s likely due to a weaker economy. Utilities and other infrastructure exposure are often seen as defensive sectors because they are critical to society.

An additional benefit from the Fed cutting rates is that it does make yield instruments more appealing to income investors. Yields can drop on risk-free rates further and drive investors to pick up riskier types of securities for higher yields. That’s not even to mention that most infrastructure relies on significant amounts of debt to fund their large CAPEX-intensive projects. Cheaper debt for these companies can also mean potentially better growth due to lower cost of capital.

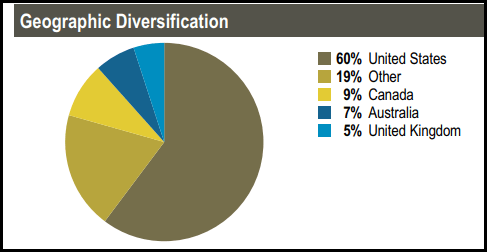

I also view UTF’s global exposure as a positive for the fund with relatively cheaper valuations around the globe. That doesn’t mean that they can’t continue to underperform and remain relatively cheaper, but they certainly have much lower expectations relative to their U.S. counterparts. Meaning that more has to go right for the U.S. market, and globally, it just has not to be as bad as expected. That being said, it would be even better for UTF if the whole globe experienced positive results, as they are still showing a 60 allocation to U.S. securities.

UTF Geographic Exposure (Cohen & Steers)

Historically speaking, UTF has performed well against its benchmark. They measure against a blended index that includes an appropriate allocation to fixed-rate preferred securities. As mentioned under the basics, this fund can invest anywhere in the capital stack and often has around a 20% allocation to preferred and other fixed-income instruments.

UTF Annualized Performance (Cohen & Steers)

Steady And Reasonable Distribution

Investing in UTF also means you are getting a monthly distribution. They had previously paid a quarterly payout for several years after the Global Financial Crisis but switched back to a monthly schedule. This is often more appealing to income investors.

At the current rate, the fund’s NAV distribution comes to 8.09%. There is a bit added to the distribution yield on a market basis due to the slight discount, which comes to 8.35%.

UTF Distribution History (CEFConnect)

If investing in UTF, it is important to have a more optimistic view of the infrastructure landscape going forward because the fund relies significantly on capital gains to fund its payout. The fund’s net investment income coverage comes to around 27%.

Therefore, without capital gains going forward, the fund’s NAV would inevitably fall. That would create a situation where the yield gets higher and higher but also more and more unlikely to be sustainable. A cut isn’t always a bad thing if needed to help provide stability to the NAV, but it is still harshly punished by investors. It often creates a situation where the fund plunges to an even wider discount. We saw a few examples of that playing out in 2023.

Given that I do have a generally favorable view of the sector going forward, I don’t see the current rate as a problem. I expect them to be able to hold steady while the rate right now is quite reasonable.

UTF Semi-Annual Report (Cohen & Steers)

We had discussed the tax classifications for the fund’s distribution earlier this year. Here is a recap:

Most of the fund’s distribution was considered long-term capital gains. However, even better for investors holding in a taxable account, the portion classified as dividends have all been qualified in the year 2022.

UTF Distribution Tax Classifications (Cohen & Steers (highlights from author))

We should get the 2023 distribution classifications before too long as we enter 2024.

UTF’s Portfolio

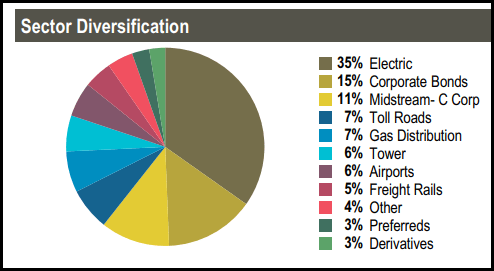

The fund remains most heavily invested in electric utilities, followed by corporate bond securities. Midstream C-corps also take the third largest allocation of the fund, which is quite similar to the positioning of the fund in the prior update. There were only some marginal gyrations between the allocations, but nothing dramatic.

UTF Sector Breakdown (Cohen & Steers)

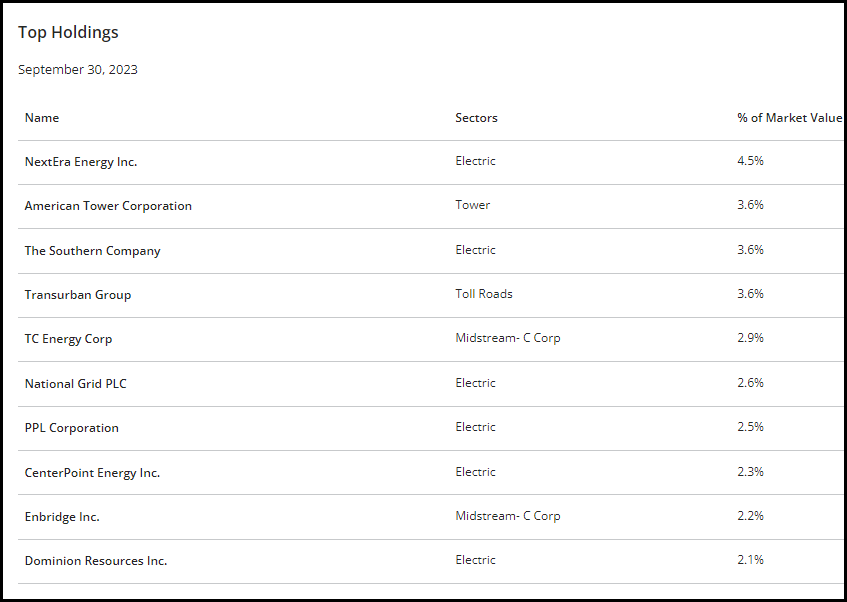

Unsurprisingly, similar to the fund’s marginal shifts for sector diversification, the actual top ten holdings for the fund haven’t shifted materially either. In total, the fund listed 235 for the number of holdings, but the top 10 make up nearly 30%.

NEE remains in the largest position, and American Tower Corp (AMT) slid into the second spot. That booted out Transurban Group (OTCPK:TRAUF) as the second largest holding, which was also surpassed by The Southern Company (SO) in terms of weighting allocation to UTF’s top positions.

UTF Top Ten Holdings (Cohen & Steers)

TRAUF is traded over the counter and is headquartered in Australia. However, they are a toll road operator and manage toll roads around the globe. It has really been a consistent staple of the fund, comprising a top position through all of our prior updates over the last couple of years. That also includes the positions in NEE and AMT, which consistently make an appearance as some of the largest positions for the fund. In fact, it even includes the first time I had ever written an article on UTF where we were looking at the holdings as of the end of 2017.

Conclusion

UTF remains a solid long-term infrastructure play for investors who are also looking to add monthly cash flows to their portfolios. While it isn’t any screaming deal, it is at a level where I believe it’s at roughly fair value. Ideally, I’d want to see a greater than 5% discount before flipping to a “Buy” level – which is where it was up until a few days ago. Even more ideally, where I’d buy aggressively would be at a greater than 10% discount.

Cohen & Steers Infrastructure Fund’s distribution, in my opinion, looks set to continue undisturbed at the current rate, barring any prolonged black swan event. A solid distribution can make it significantly easier to hold a position while waiting for a recovery, which I do suspect that utilities and infrastructure can do well in this new year.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")