KE ZHUANG

Summary

I believe that meeting net zero and achieving a viable energy transformation can be much better achieved with nuclear energy. To this end, I wrote about the uranium market when I analyzed the Sprott Uranium Miners ETF (URNM) in December and came away with a positive view but looking for a pullback to go overweight the sector. Today I take a deep dive into Global X Uranium ETF (NYSEARCA:URA), which has lower exposure to uranium mining but similar upside potential, and rate it a BUY.

Performance

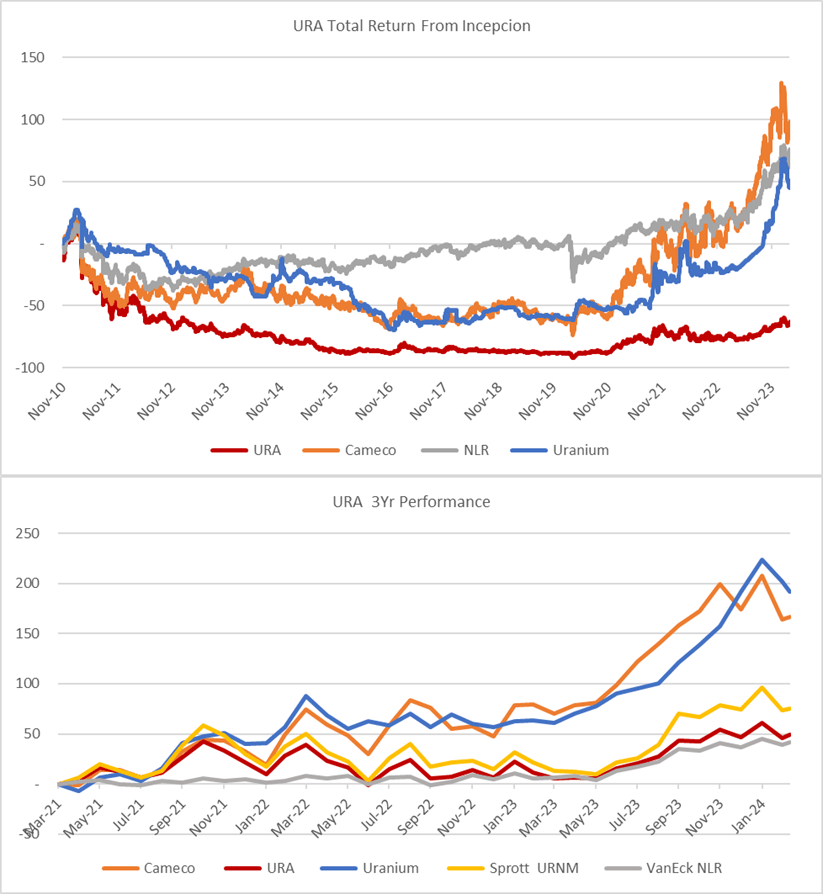

It is good that past performance is not indicative of future gains given the abhorrent return URA has posted since inception in 2010. The ETF has dramatically underperformed uranium spot prices, Cameco (CCJ) the biggest holding as well as other peers. In the last three years, URA has done far better up about 50% capturing part of the underlying uranium spot prices much in line with ETF peers and despite the large stake in Cameco.

URA Performance (Created by author with data from Capital IQ)

ETF Comparison

There are few ETFs focused on Uranium production with URA and URNM being the largest followed by VanEck Uranium+Nuclear Energy (NLR) which has a wider focus and includes utility holdings. Given the high concentration of uranium mining in just two companies the logic of diversification into small miners, many pre-operational or exploration stocks may create far more volatility and risk as well as reward. URA seems to strike a good balance of exposure in mining uranium with additional holdings in related activities such as construction and equipment companies like NuScale Power (SMR) which is seeing high growth.

URA ETF Comps (Created by author with data from Capital IQ)

The Case for Uranium

The investment case for uranium requires three key drivers. The first is a nuclear renaissance, despite the demand coming from Asia, both the US and Europe need to begin to build or at least talk about building new Nuclear power capacity. The second driver is the uranium mining cost curve that requires over US$100lb for many new mines to be profitable. Uranium is an abundant mineral but is highly de-concentrated and requires massive ore mining and processing to gather a small amount and this makes it expensive to mine. Finally, discipline at Kazatomprom (40% of global supply) and Cameco (20% supply) i.e. increasing production with demand and not flooding the market to retain share or deter new entrants.

Global X Funds

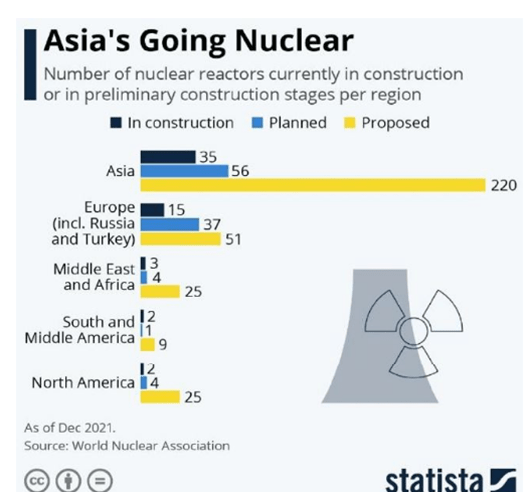

Asia Going Nuclear

Today there are about 440 nuclear power reactors operating in 32 countries plus Taiwan, with a combined capacity of about 390 GWe. In 2022 these provided 2545 TWh, about 10% of the world’s electricity. That number may grow 50% in the next 15 to 20 years driven by Asian capacity increase.

Asia Nuclear Demand (Statista)

Uranium Mining Risk

With a large portion of the AUM in small mining stocks or pre-operational and prospecting companies it is relevant to explore the risk in uranium mining. According to research from the Nuclear Energy Agency, International Atomic Energy Agency, and World Nuclear Association, new mines can take 10 to 15 years to enter production with environmental licensing one of the most stringent due to the radiation effects of concentrated uranium can have on workers and communities if not correctly processed and stored correctly. This means over 30% of AUM may never come into production.

However, since many juniors placed mines care & maintenance in the last 15 years as the extraction costs were above sales prices, these mines can come back online in a few years. Paladin Energy (OTCQX:PALAF), Energy Fuels (UUUU) and Boss Energy (OTCQX:BQSSF) are good examples with production and revenue estimated to increase 3x from 2023 to 2025.

Portfolio Overview

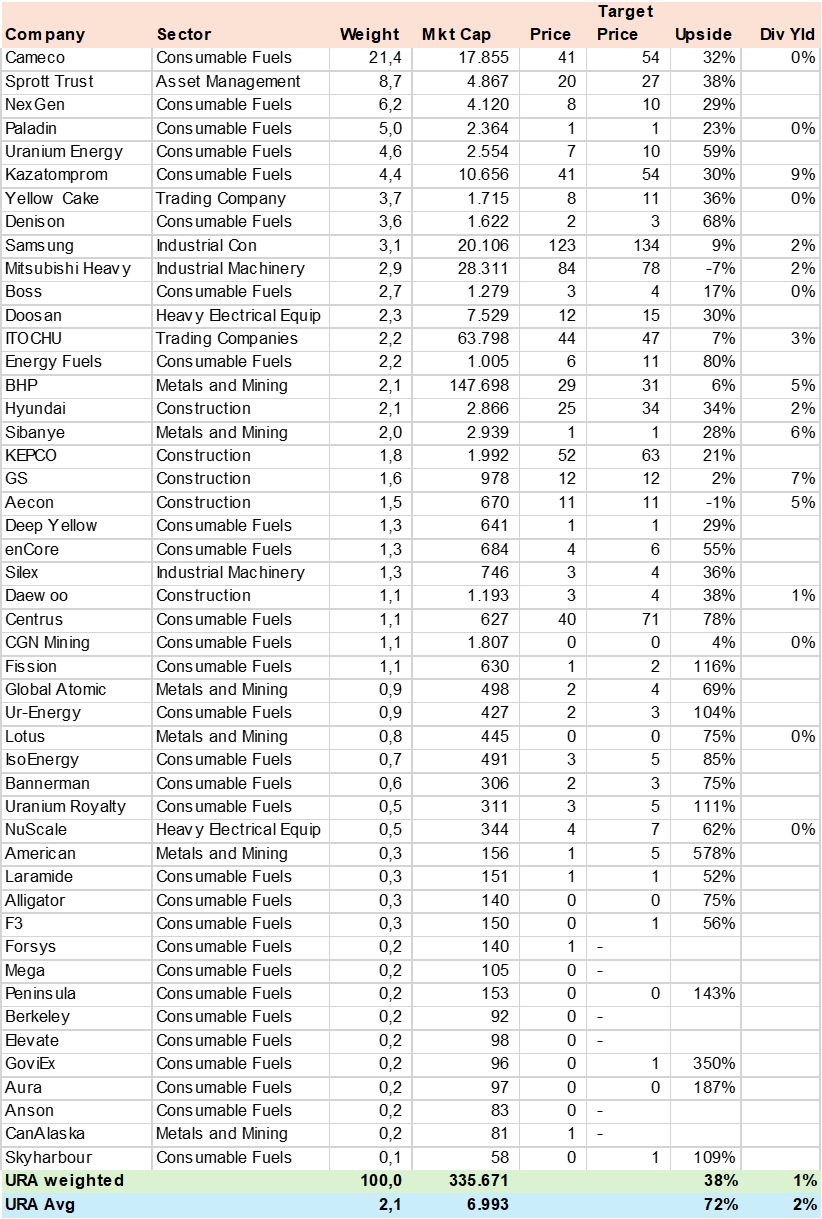

I gathered consensus estimates on all the holdings and arrived at an upside potential of 38% using price target estimates for 2024. As can be seen, the portfolio has a very large weight in Cameco followed by the Sprott Physical Uranium Trust (U.UN:CA). About 36% of AUM is in small mining companies, pre-operational, or in the exploration stage that do not have revenue or earnings estimates. Still, analysts assign a valuation based on resource or reserve potential, which is quite speculative in my view. The ETF also has exposure to companies in diversified mining, equipment manufacturing, construction, and trading. The combination may reduce overall volatility and risk at the expense of performance if the Uranium price continues to climb.

URA Consensus Price Target (Created by author with data from Capital IQ)

Revenue and Margins

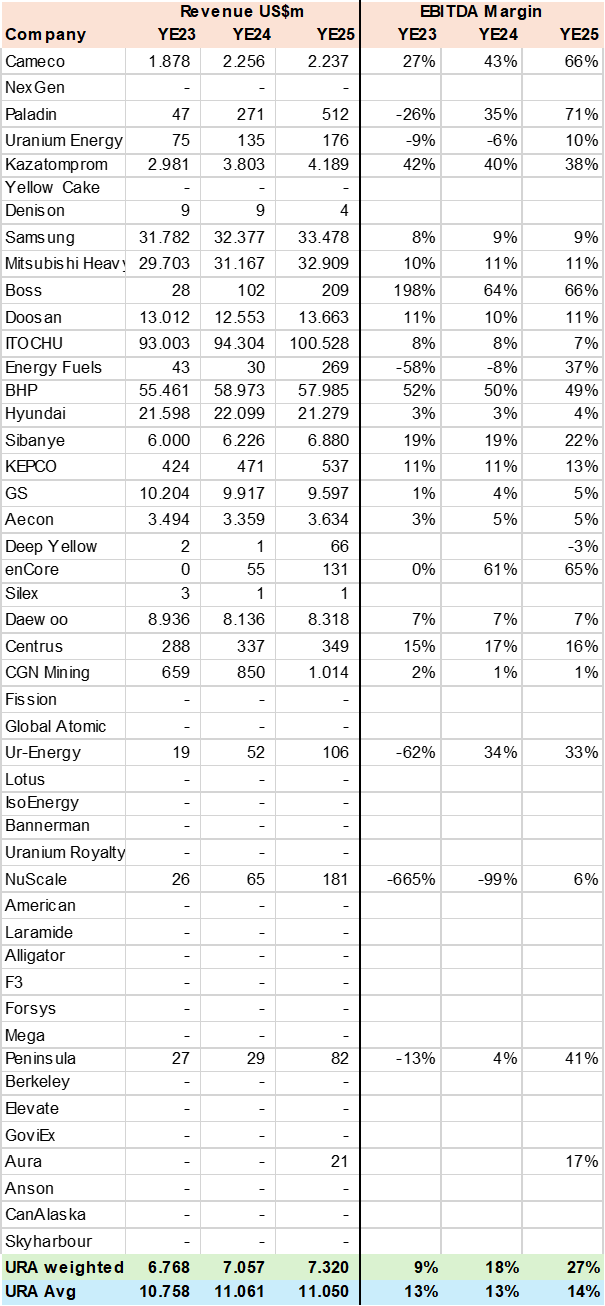

In this section, I normally focus on revenue growth and net margins. Still, in the case of this portfolio, I thought it more valuable to highlight the actual consensus revenue estimate and EBITDA margin to highlight the large number of holdings with no discernable revenue estimated for 2025. In addition, it is evident the low growth contribution that large and somewhat related stocks such as Samsung and BHP have on the portfolio. The portfolio margin expansion estimates from 9% to 27% in 2025 is driven by primality by Cameco which sees its EBITDA margin increase from 27% to 66% according to consensus estimates.

URA Revenue & Margins (Created by author with data from Capital IQ)

Valuation

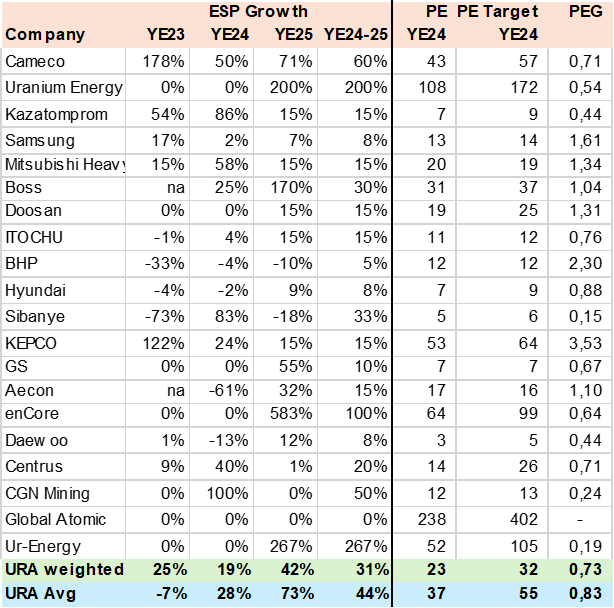

Valuing a portfolio with many stocks that do not have earnings is quite difficult and hence I stripped these companies from the PEG ratio analysis. As can be expected Cameco is a key driver and despite its 43x PE on YE24 estimates it is relatively inexpensive with PEG of .7x in line with the ETF weighted average. The most expensive relevant stock is BHP Group (BHP) at 2.3x due to very low long-term growth. The ETF’s 36% of AUM in small and not profitable mining stocks is lower than peer URNM and may offer some reduced volatility and risk offset by upside if and when those companies are acquired or eventually begin production.

URA EPS Growth & Valuation (Created by author with data from Capital IQ)

Conclusion

I rate URA a Buy. I believe in the bull case for uranium and nuclear energy as a long-term solution for clean energy, the net-zero targets, and climate change. The portfolio offers a good risk-reward balance mix of physical uranium, large miners such as Cameco, related supply chain companies, and more speculative junior mining companies. At the same time, the modest pullback in uranium prices provides a better entry level in my view.

Q2 2024 Earnings Call Transcript")