Jeff Swensen/Getty Images News

Introduction

It’s time to talk about the United States Steel Corporation (NYSE:X), one of the cyclical steel stocks I have had on my radar for many years.

My most recent article on the stock was written on November 2, when I went with the title “U.S: Steel Is A Buy In Light Of Megatrends, M&A, And Strategic Investments.”

Since then, shares have returned 14%.

In this article, we’ll discuss the company’s risk/reward in light of very important developments that allow me to focus on two important aspects of my investment framework:

- Macroeconomics: United States Steel is a cyclical steel stock.

- Politics: Biden is getting involved, making it increasingly unlikely that the Pittsburgh-based corporation will be acquired by Japanese Nippon Steel (OTCPK:NPSCY).

Leo Nelissen – Investment Framework

So, as we have a lot to discuss, let’s get right to it!

What’s Going On With The Nippon Deal?

In 4Q23, United States Steel agreed to be bought by the Japanese Nippon Steel Corporation in a deal valued at $14.1 billion ($55/share – 100% cash).

The deal would add 20 million metric tons of annual steel production to Nippon’s portfolio, making it the world’s second-largest steel producer.

This also meant that Cleveland-Cliffs (CLF) wasn’t going to get its chance to buy its American peer, as I discussed in a recent article.

In that article, I also covered that CLF’s management believes that United States Steel made a mistake by agreeing to a deal that would not likely get approved.

Cleveland-Cliffs got a tailwind from former President Trump, who made clear that he would block the deal after a (potential) election win.

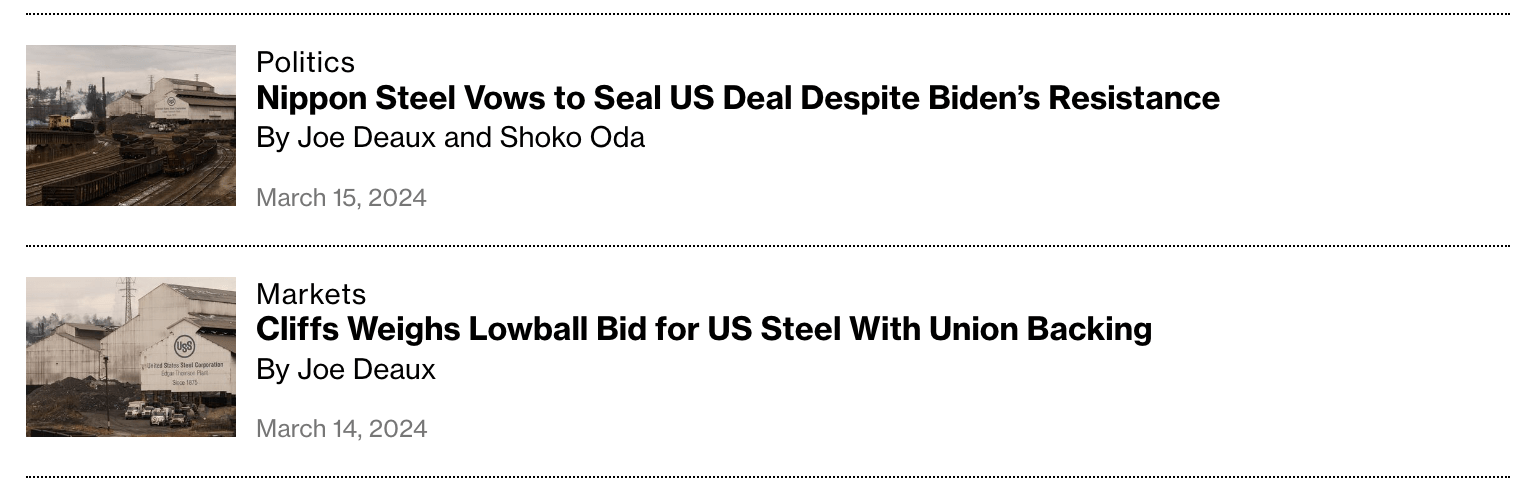

Reuters

Trump, whose protectionist “America First” policies were a hallmark of his tenure, said on Wednesday he would “instantaneously” block the deal if he wins the Nov. 5 vote. The Republican is set for a likely rematch with President Joe Biden, a Democrat. – Reuters

As it turns out, his contender, the current President of the United States, Joe Biden, is also getting involved.

On March 14, the Wall Street Journal wrote an article titled “Biden Opposition to Takeover of U.S. Steel Comes After Months of Lobbying.”

Wall Street Journal

After a few months of silence, Biden has come out against the deal, as both Republican and Democrat lawmakers have opposed the deal – supported by the United Steelworkers union.

According to the article, the Nippon deal is important for Biden’s industrial ambitions, as he is focused on the future of American manufacturing. I believe the Inflation Protection Act is a great example of this.

Although the case can be made that a takeover from Nippon could pressure China (which isn’t a bad thing for the U.S.), it also means that a critical supply chain player ends up in Japanese hands.

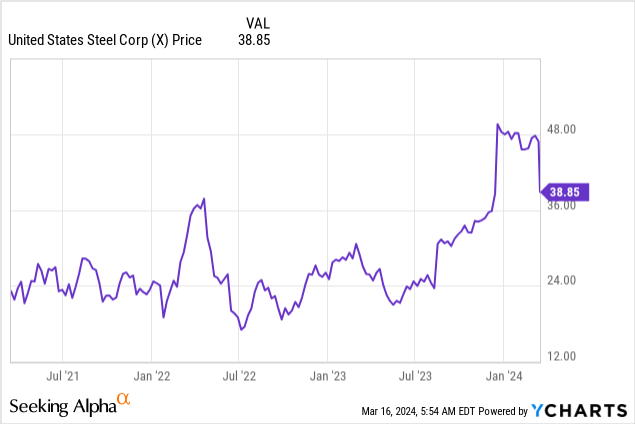

The result of Biden’s involvement was a decline in United States Steel’s stock price:

On top of that, if Biden pushes hard for the return of American manufacturing, he can take away some potential votes from candidate Trump.

Besides that, he wants to be seen as a very union-friendly president. Helping the United Steelworkers union in this “battle” would be a good sign.

The larger battle, then, is political. Steel is a preoccupation for both political parties. Trump placed tariffs on steel imports, while Biden has directed subsidies toward made-in-America metal. The two candidates are wooing steelworkers, and Biden has styled himself as the most pro-union president in history. – Wall Street Journal

With that said, I believe there is a very high likelihood that this deal will fail.

Both Biden and Trump would benefit from blocking the deal – especially with regard to the upcoming election.

On top of that, I cannot imagine that the current “America First” environment, which is supported by both Biden and Trump, will see a deal where Nippon buys United States Steel.

Furthermore, in general, the FTC has become much stricter when it comes to takeovers. In 2022, the Wall Street Journal reported that we’re in an environment where deals without obvious benefits for the economy will be blocked.

The Biden administration’s antitrust enforcers are throwing sand in the gears of Wall Street’s deal machine.

Under Chairwoman Lina Khan, the Federal Trade Commission is questioning mergers that likely would have gone unchallenged in years past—a change Ms. Khan says is needed to prevent companies from building up too much power and stifling competition.

So far, the market seems to agree with me. United States Steel trades at $38, which is 44% below the $55 offer from Nippon!

If the deal were likely to succeed, we would be looking at 44% “free money.”

Based on this context, both Nippon and Cleveland-Cliffs had responses. After all, one fears it is losing a major deal. The other sees an opportunity.

The screenshot from Bloomberg perfectly sums up what’s at stake for these companies:

Bloomberg

On March 15, Nippon came out making the case that the deal delivers benefits to the United States through good union jobs, investments in advanced technologies, and national security benefits, including putting both Japan and the United States in a better spot to “combat” China on the global steel market.

Nippon Steel is the right partner to ensure that U. S. Steel is successful for generations to come as an iconic American company. We are progressing through the regulatory review, including CFIUS, while trusting the rule-of-law, objectivity, and due process we expect from the U.S. Government. We are determined to see this through and complete the transaction. – Nippon Steel Corporation

What’s interesting is that Bloomberg reported that Nippon initially said in its statement that there would be no layoffs or plant closures until at least September 2026. That date was deleted to make the wording “more appropriate.”

So, what’s up with Cleveland-Cliffs?

As one can imagine, with Nippon having one foot out the door again, the Ohio-based giant is seeing an opportunity to push for a deal in the event of a takeover rejection.

CLF CEO Lourenco Goncalves, who I have been a fan of since the day he joined the company, is in a fantastic position. As reported by Bloomberg, he has the backing of the United Steelworkers union if he were to make an offer.

This puts him in a great spot to make an offer if the Nippon deal fails, “albeit at a significantly lower price than the existing offer.”

What does that mean?

According to the article, which cites Mr. Goncalves, CLF would be open to an offer in the $30s, which is where the company is currently trading.

I believe that would be a fantastic opportunity for CLF and X to combine two of the best steel assets in North America.

Thoughts On The Deal & Recent Events

While I may be wrong, I believe the Nippon deal will be blocked. Political risks are just too high. Especially in his fight for Rustbelt votes, I do not expect President Biden to allow Nippon to buy United States Steel.

He has support from Unions, a Trump-like America First agenda (with regard to supply chains), and the risk of handing Trump votes if he does not take action.

I believe a CLF takeover is much more likely. On top of that, we could see a situation where X remains a standalone company.

After all, as I have discussed in recent U.S. Steel articles, it has just finished an impressive business improvement, including new steel capabilities and higher earnings power.

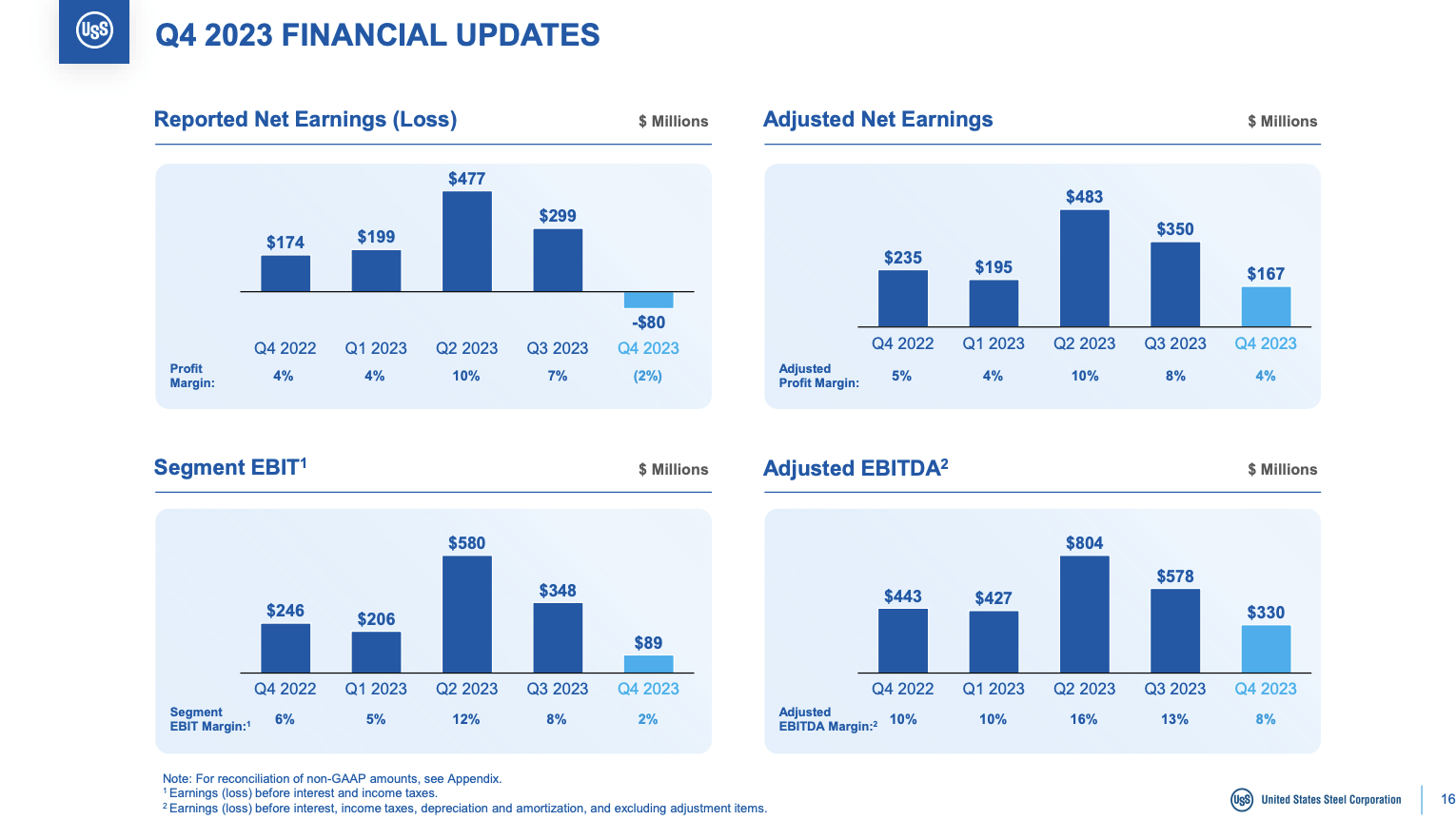

United States Steel

Looking at its latest result, in the fourth quarter of 2023, the company reported net earnings of $167 million. EPS came in at $3.56, while adjusted EBITDA reached $330 million.

United States Steel

Overall, 4Q23 was weaker. This was mainly driven by lower selling prices.

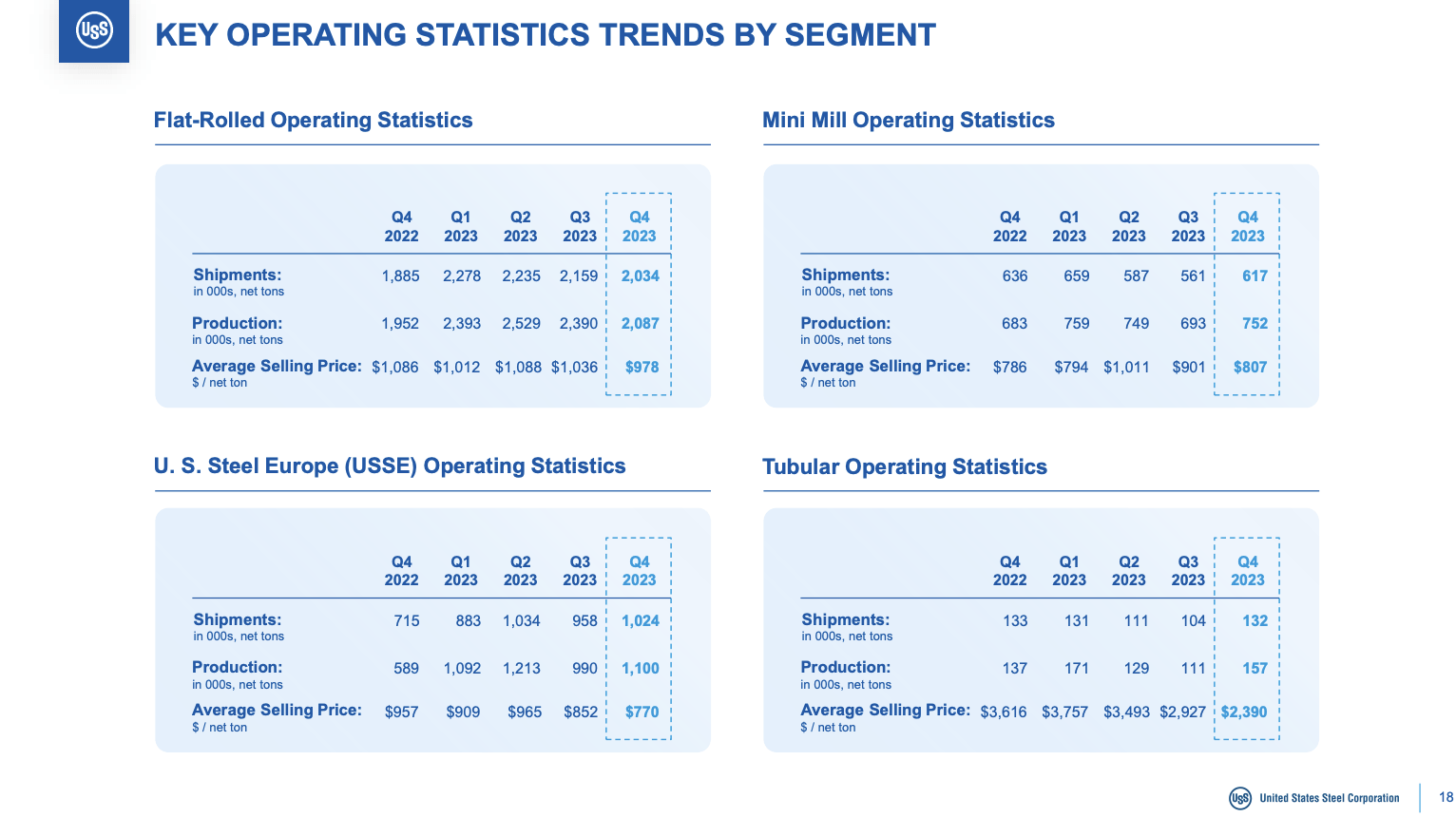

United States Steel

Moreover, despite a negative free cash flow of $244 million, the company maintained a strong balance sheet with $5.2 billion in total liquidity, including $2.9 billion in cash.

As a result, the company’s leverage ratio remained low at 2x adjusted gross debt to EBITDA, which is very healthy.

On top of that, Nippon will have to pay United States Steel a $565 million breakup fee if the deal fails. That’s 6.5% of its current $8.7 billion market cap!

With that said, I like the valuation of United States Steel – despite economic headwinds.

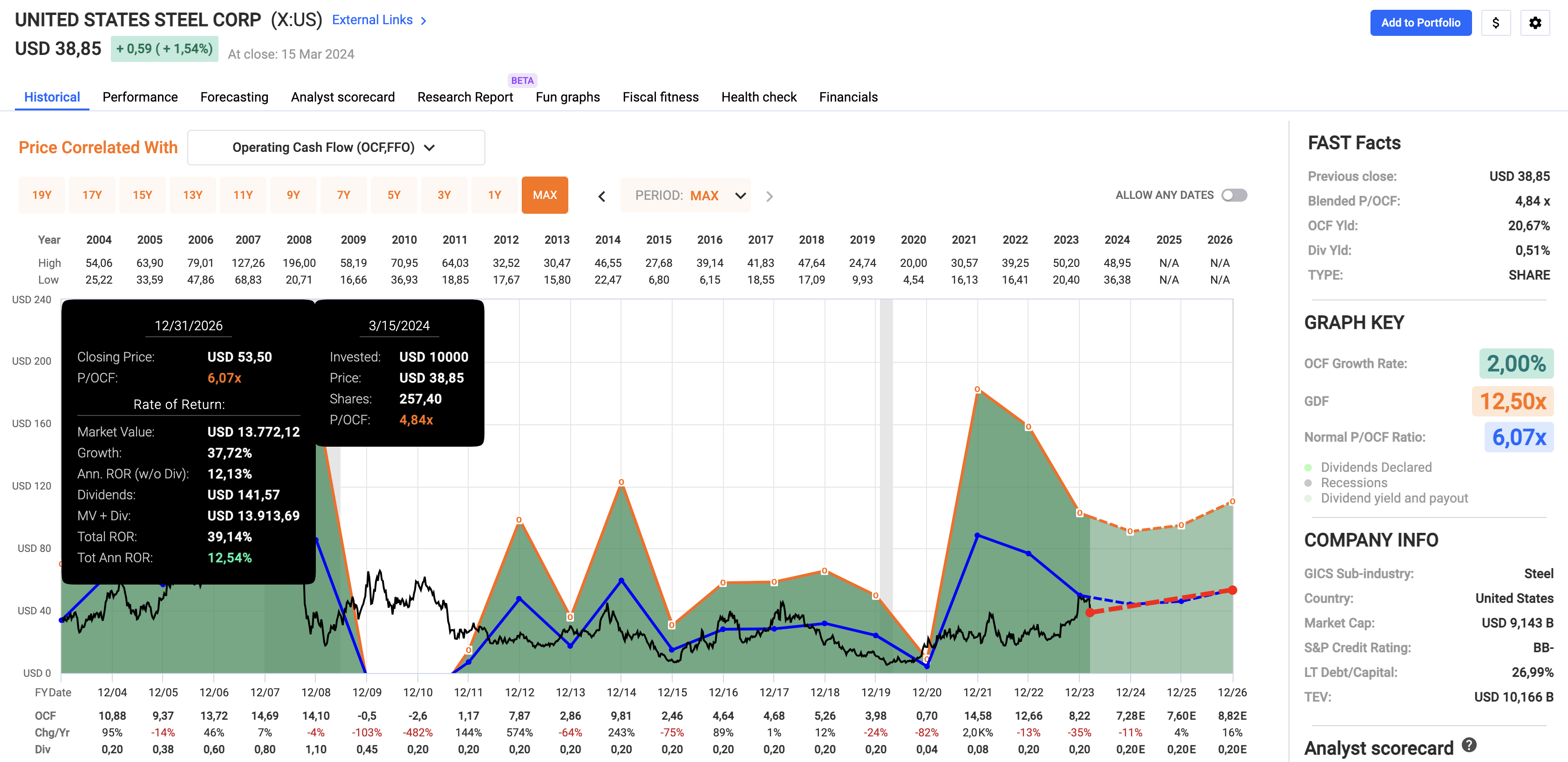

Using the data in the chart below, we see that analysts expect challenging economic developments (like subdued steel prices) to keep pressure on earnings.

For example, operating cash flow (“OCF”) per share in 2023 was $8.22. That number is expected to remain consistent through 2026.

Historically speaking, the stock has a normalized OCF multiple of 6.1x. This implies a fair price target of roughly $50. That’s below the offer from Nippon (which had to pay a premium for future growth) and significantly above a potential new offer from CLF.

FAST Graphs

The current consensus price target is $50 as well.

All things considered, if I were long United States Steel, I would not change anything.

If the Nippon deal fails, the company gets a huge breakup fee and a likely offer from CLF that should be close to its current price – I think it will be higher.

If the deal succeeds, investors get to sell my shares at a much higher premium.

Even if United States Steel were to continue as a standalone company, I’m very upbeat about its future.

Hence, I’ll stick to a Buy rating.

Takeaway

United States Steel faces significant political and regulatory hurdles with the proposed acquisition by Nippon Steel.

The involvement of both Biden and Trump adds layers of uncertainty, making the deal’s success unlikely.

However, this situation presents opportunities, particularly for Cleveland-Cliffs, which could capitalize on a failed deal.

Despite short-term volatility, United States Steel remains fundamentally strong and has impressive financials on top of a favorable valuation.

Whether as a standalone company or in a potential merger, the future looks promising.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")