LumiNola

Over the past year, I have found myself looking deeply into the financial sector, especially focusing on commercial regional banks. One of the larger players that I ended up analyzing is a company by the name of United Bankshares (NASDAQ:UBSI). With a market capitalization of $4.63 billion as of this writing, the firm is not exactly a giant in the banking sector. But it’s far from small. In an article that I wrote about it in August of 2023, I acknowledged that shares had not recovered most of the downside that they experienced during the banking crisis earlier that year. But after digging deeper, I recognized that shares were trading at rather lofty multiples. This led me to rate the business a ‘hold’ to reflect my view that the stock would be unlikely to outperform the broader market for the foreseeable future.

Since then, things have gone quite well for the institution. Management has reduced debt and deposits have continued to increase. The bottom line for the company has suffered to some extent, but the overall fundamental picture shows improvement quarter after quarter and year after year. As a reward for this continued fundamental growth, the market has pushed shares up, giving shareholders upside of 21%. That’s above the 15.7% increase seen by the S&P over the same window of time. Clearly, my call on the business has been wrong to this point. But digging in again, I don’t see any reason to be optimistic about further market beating performance. Relative to similar firms, shares look to be more or less fairly valued. And on an absolute basis, there are definitely reasons to not like the enterprise. Because of this, I’ve decided to keep the company rated a ‘hold’ for now.

I’m not banking on this one

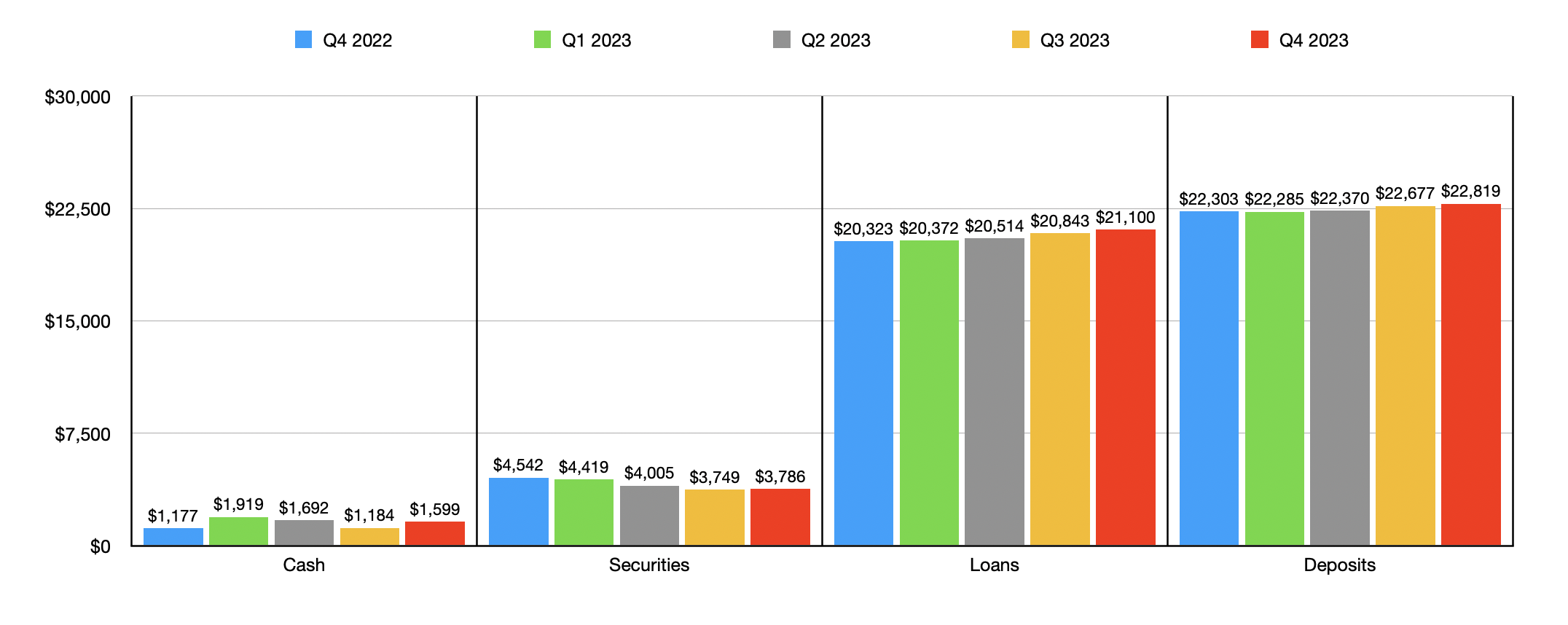

Perhaps the best place to start when it comes to United Bankshares is the balance sheet data. A massive liability for any bank would be the deposits on its books. While liabilities are typically something you want to see less of, deposit growth shows that the institution itself is growing and it means the firm has additional capital with which to grow and generate interest income from. By the end of 2023, overall deposits came in at $22.82 billion. This is up from the $22.37 billion that the company had during the second quarter of 2023, which was the most recent updated data available when I wrote my prior article on it. It’s also higher than the $22.30 billion on the books at the end of 2022. It’s nice to see a rise in deposits. Another good thing is that uninsured deposit exposure has declined, falling from 30% when I last wrote about the company to 28% today. As a rule of thumb, I like to see a reading of 30% or lower, with the lower it is the better off things are. So this is great.

Author – SEC EDGAR Data

There have been other areas of growth for the institution. Shifting to the asset side of the balance sheet, we get loans of just under $21.10 billion. That’s up from the $20.51 billion that the company had at the end of the second quarter of last year and it stacks up nicely against the $20.32 billion that the bank had at the end of 2022. This isn’t to say that everything has increased over this window of time. For instance, the value of available for sale securities dropped from $4.01 billion in the second quarter of last year and from $4.54 billion at the end of 2022, down to $3.79 billion today. Cash has been a bit mixed. As of the end of the most recent quarter, it totaled $1.60 billion. That’s down from $1.69 billion two quarters earlier but is up from the $1.18 billion reported at the end of 2022.

Author – SEC EDGAR Data

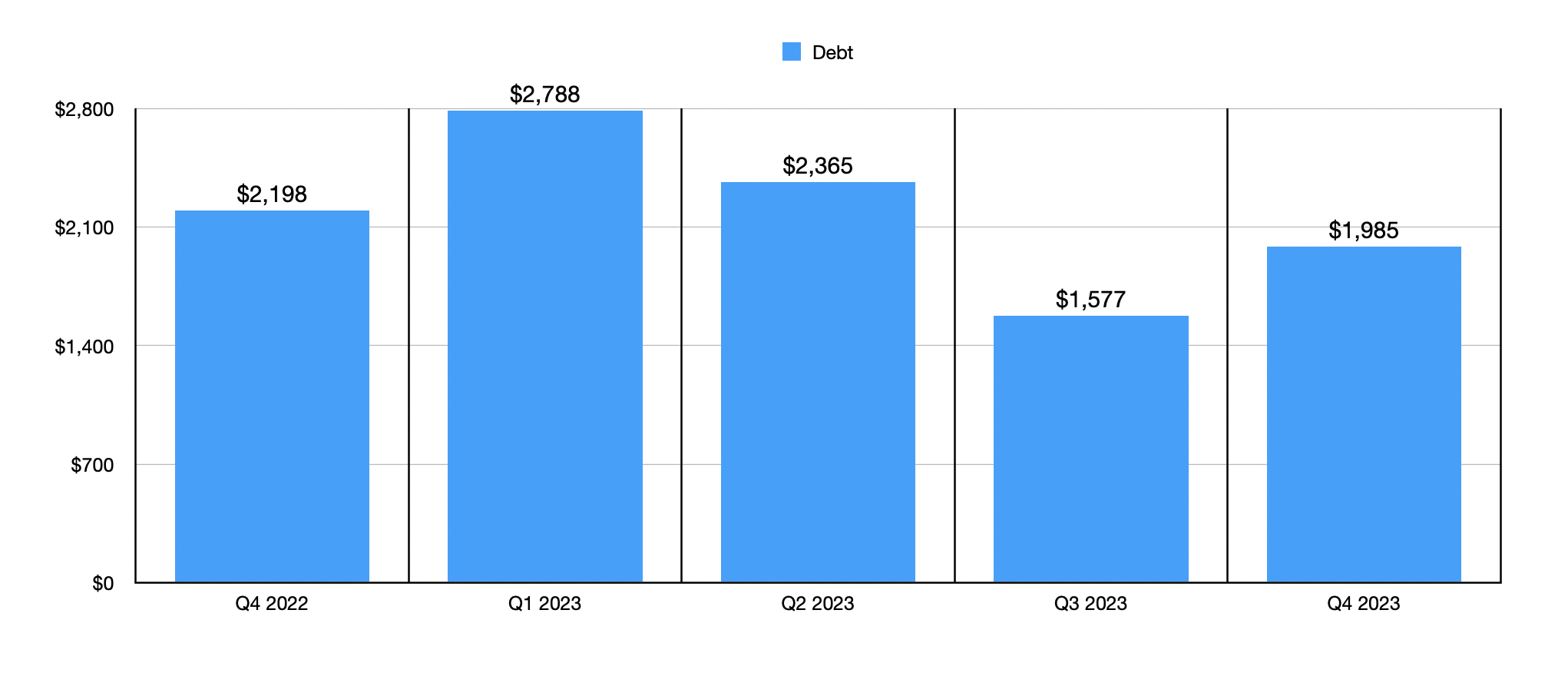

Other important metric to pay attention to is debt. Cash, securities, and loans, can increase if the company is taking on debt and using the capital in that way. During the scariest times of the banking crisis, almost all of the financial institutions that I analyzed at the time drew down on their borrowing capacity in order to boost liquidity. With high interest rates, this resulted in significant hikes in total interest expense for the institutions. But that was a price they deemed willing to pay in order to keep cash on the books. At the end of 2022, debt totaled just under $2.20 billion. This managed to rise to $2.37 billion when I initially wrote about the company. But we have seen a decline since then. Although not as low as the $1.58 billion in debt that the company had at the end of the third quarter, it did boast that of $1.99 billion at the end of last year.

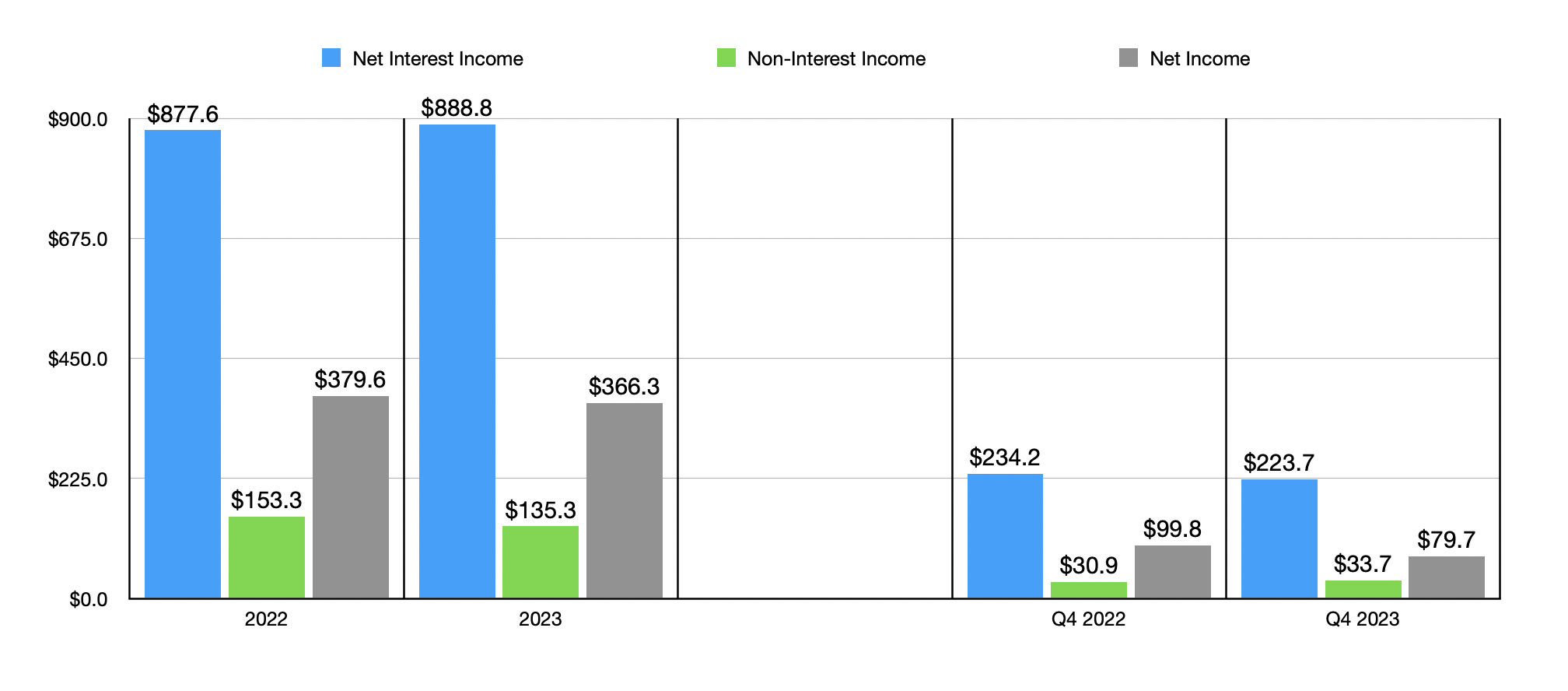

The overall growth in the institution Mike you have the impression that the bank has been growing from an income statement perspective as well. But this is not exactly the case. From 2022 to 2023, net interest income rose modestly from $877.6 million to $888.8 million. A very small increase in average asset values, combined with a slight improvement in the net interest margin from 3.50% to 3.56%, was responsible for this. But as the chart below illustrates, net interest income in the final quarter of 2023 was a bit lower than what it was the same time one year earlier. This was largely the result of a decline in the net interest margin from 3.87% to 3.55%. A decline in the return on average assets seems to be one of the culprits here.

Author – SEC EDGAR Data

There are, of course, other things that we need to be paying attention to. A big weakness for the company involved its non-interest income. This fell from $153.3 million in 2022 to $135.3 million in 2023. This was in spite of a small improvement in the final quarter of last year compared to the final quarter one year earlier. A weak housing market caused most of this pain, with mortgage banking activities revenue dropping from $42.7 million to $26.6 million. This was instrumental in pushing net profits for the year down slightly from $379.6 million to $366.3 million, with a good portion of that downside occurring in the final quarter.

Author – SEC EDGAR Data

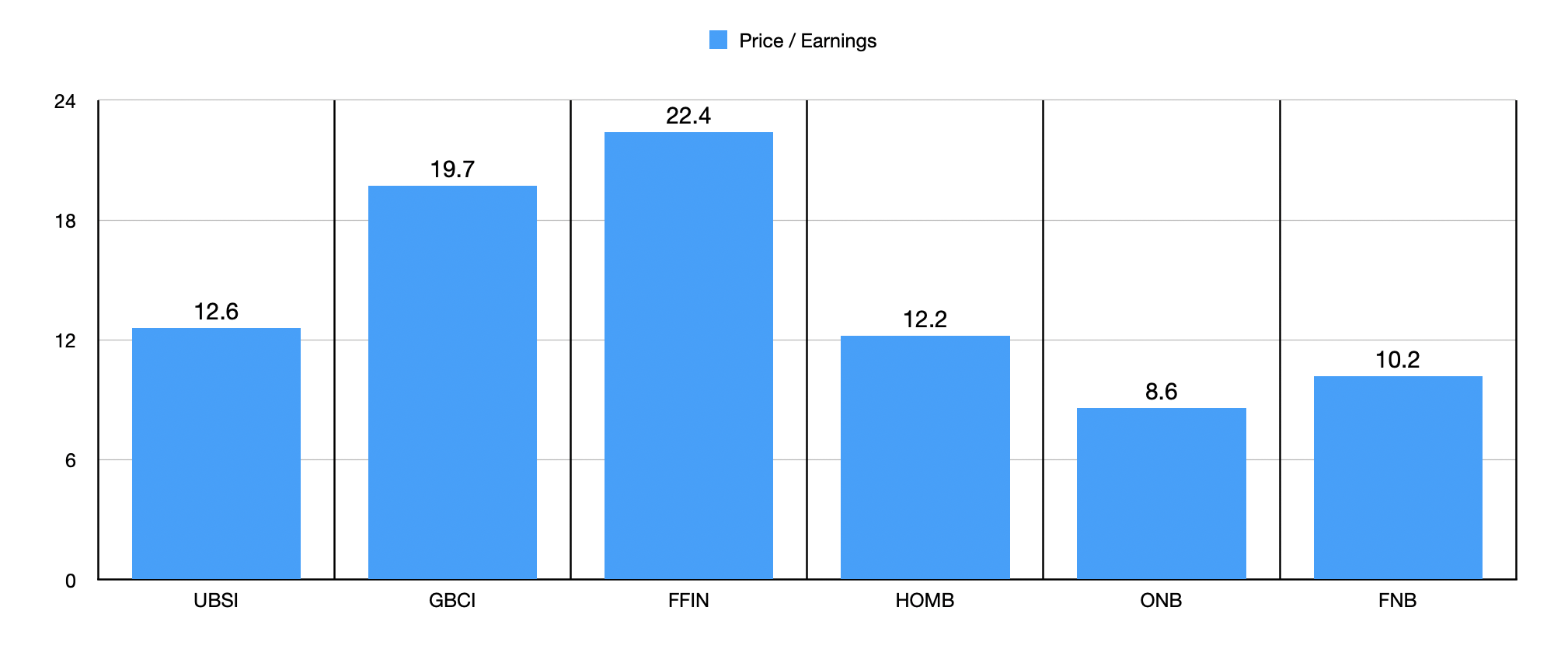

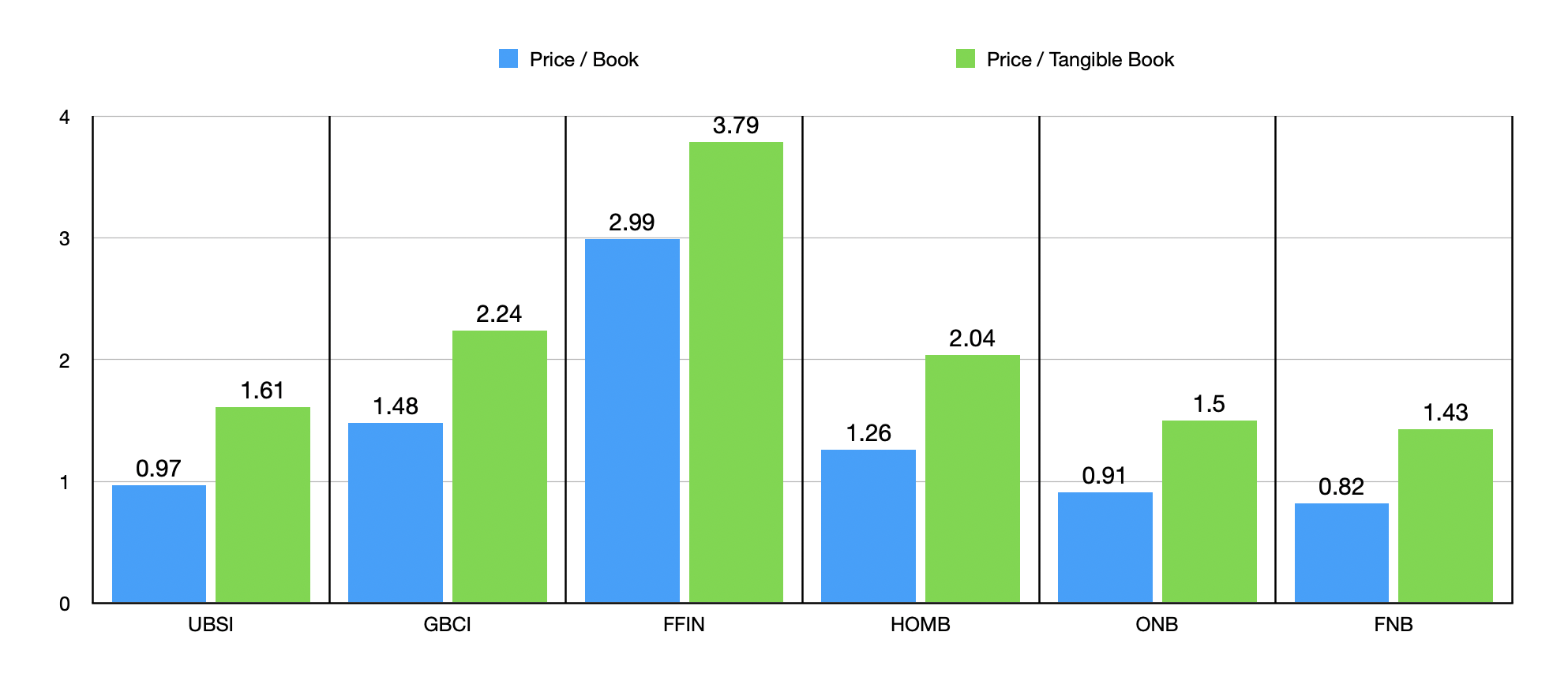

Even in spite of the downturn experienced, the firm is still generating plenty of profit. But this doesn’t make it an attractive investment. As you can see in the chart above, I compared United Bankshares to five similar firms using the price to earnings multiple. In this case, three of the five companies ended up being cheaper than it. I would also like to note that the 12.6 multiple for the institution is quite a bit higher than I look for in this space. I am generally not all that interested unless the bank is trading at a multiple of 10 or lower. In the chart below, meanwhile, I compared United Bankshares to the same five companies using both the price to book approach and the price to tangible book approach. In both instances, two of the five firms ended up being cheaper than it.

Author – SEC EDGAR Data

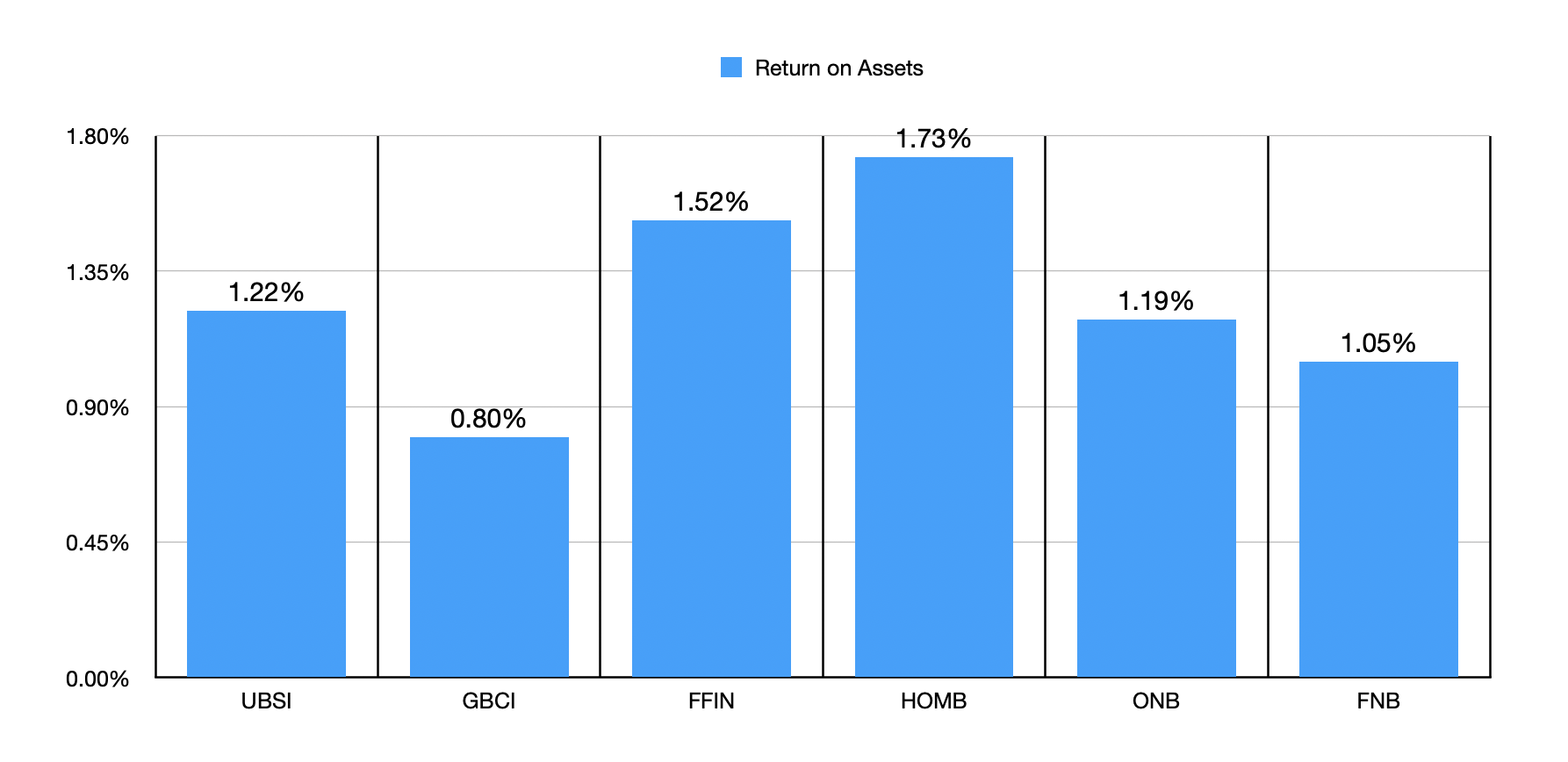

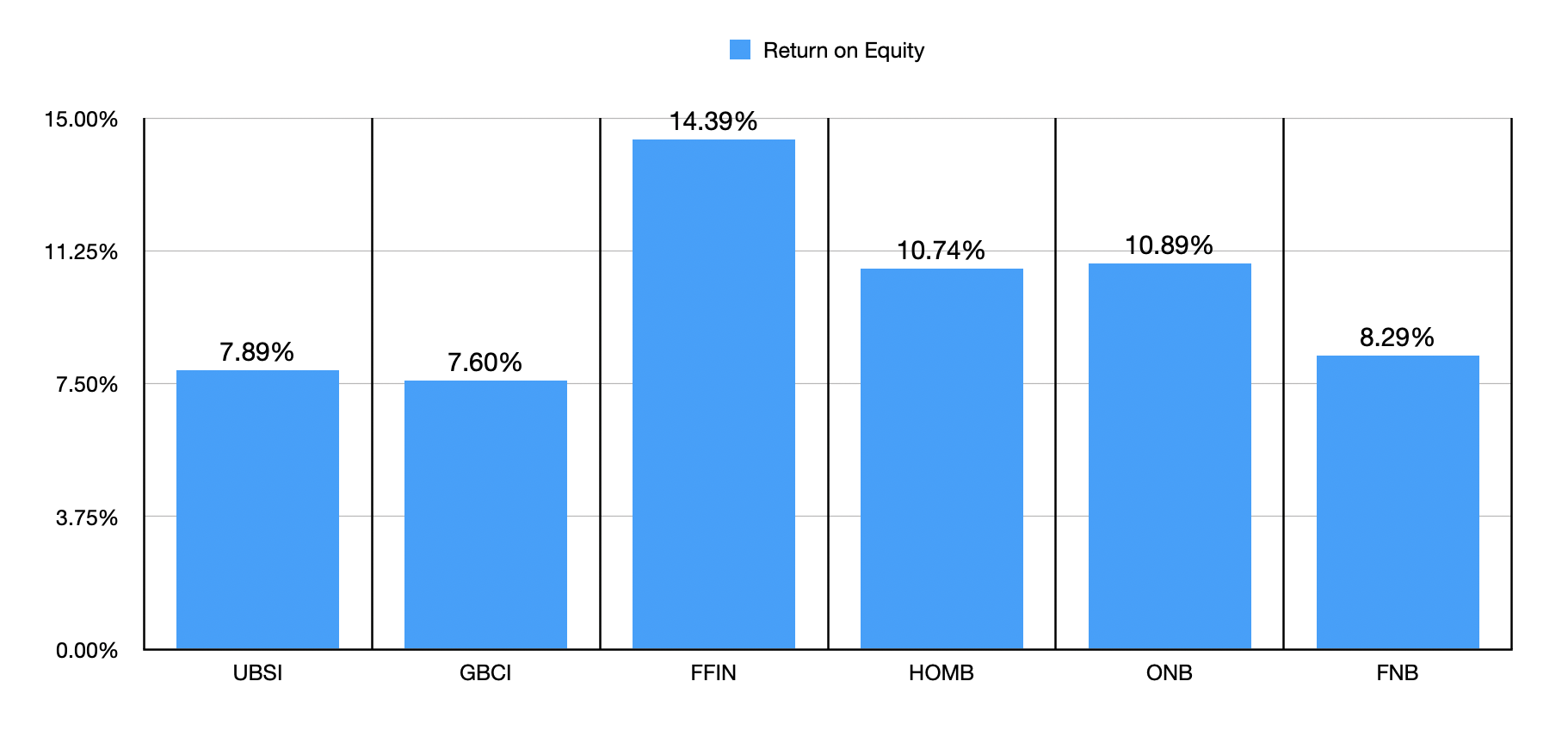

We should also be paying attention to the quality of the assets that we are dealing with. That’s why, in the first chart below, decided to look at the return on assets, not only for United Bankshares, but also for the same five comparable businesses. In this case, three of the five companies had readings that were lower than what United Bankshares had. And in the chart below that, you can look at the return on equity of each institution. This is one area where United Bankshares thrives. Only one of the five ended up being lower than it.

Author – SEC EDGAR Data Author – SEC EDGAR Data

Takeaway

From all that I can tell, United Bankshares remains a solid company and it will likely do well for itself and its investors in the years to come. But as they vary investor, I prioritize only the best opportunities that are out there. Relative to earnings, shares are pricey on an absolute basis. And with the exception of the return on equity, there’s nothing that really distinguishes it in any special way from those other firms that I compared it to. Given these facts, I’ve decided to keep it rated a ‘hold’ for now.

Q2 2024 Earnings Call Transcript")