Rupak Ghose is an adviser to fintech companies and a former financials research analyst with Credit Suisse.

We’re told that the UK needs to celebrate its success stories. As they like to say in the VC community, “pessimists sound smart, optimists make money”. So, let’s take a look at the UK neobanks.

These much-touted UK fintechs — Revolut, Monzo, Starling, OakNorth, and Wise — have been crushing it recently. Yes, valuations are down but revenue growth has remained healthy and in some cases has accelerated.

Moreover, with the exception of Monzo all these so-called challenger banks are profitable. You can’t say that of the Forbes 30 under 30 payments crowd on the other side of the pond:

But here’s the thing. If you’re an investor, how do you exit?

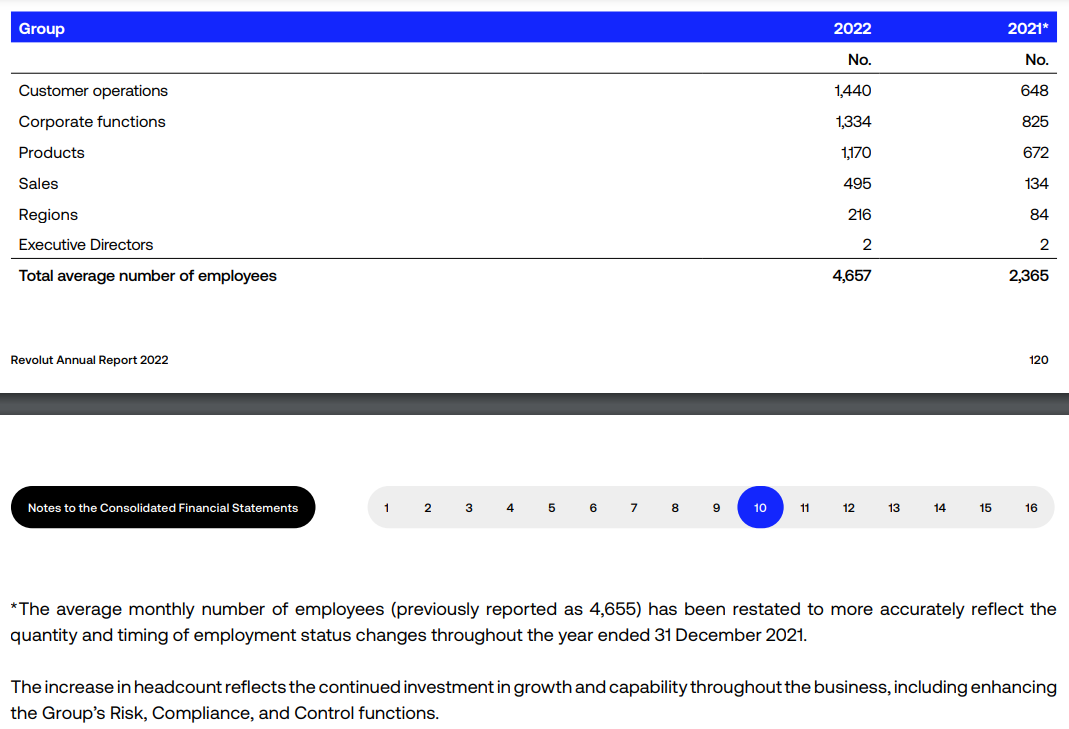

The natural route is an IPO. But public investors want disclosure, and around reporting accuracy not all neobanks are flawless. It’s a bad look for example to revise 2021 average headcount from 4,655 to 2,365, like Revolut did in its 2022 annual report. Stock investors and the financial press will pay more attention to that sort of mistake than the social media influencers and VC cheerleaders.

M&A is possible, but difficult given different strategic preferences among stakeholders. Is management’s plan to expand the lending book (profitable, but tradfi) or would they rather focus on a superapp story, which might attract higher valuation multiples but has so far only really succeeded in China?

The challenge for the neobanks is that they want to benchmark against tech growth stocks and have a similar growth profile, but how they make money is more like a brick-and-mortar bank.

Let’s start with the listed peer group. Nu Holdings, the owner of Brazil-based Nubank, is the gold standard in the sector. The Warren Buffett-backed company went public on NYSE in 2021 and, after a sharp sell-off, its stock is back above the IPO valuation of $40bn. Customer numbers doubled over the last 2 years to 90mn, primarily in Brazil. Revenues grew by 50 per cent year-on-year in 2023’s third quarter, albeit predominantly driven by interest income and gains on financial instruments. Fees such as interchange on cards grew by 20 per cent year-on-year and were only 20 per cent of gross revenues. Net income is annualising at $1.4bn, implying a PE multiple of 29x.

Wise has been on a similar round trip, with a sharp share price sell-off following a direct listing in 2021 and now a recovery back to that valuation of around £8-9bn. Like Revolut, Wise is regulated in the UK as an electronic money institution rather than a bank. It makes around 60 per cent of revenue from FX transactions and less than 20 per cent from interchange fees on cards. On the current run-rate Wise is trading on 6x revenues and 25x net income.

The main difference between banks the latter is its greater dependence on interchange fees from the use of debit and credit cards and currency exchange. Nevertheless, this is hardly the annual-recurring-revenue business model VCs typically invest in.

Neobanks are growing their customer count by 20-40 per cent every year as cash usage continues to decline. But eventually they will run out of new countries to launch into, and if we ever get a slowdown in consumer spending their income will be exposed as cyclical. It’s all very different to multiyear enterprise software deals or unique social networks.

UK neobanks are rarely the main bank account for their customers, unlike Nubank, but even small numbers add up. Revolut, for instance, has deposit sizes of a couple of hundred pounds for tens of millions of clients.

And a key driver for their acceleration of revenue growth in recent years has been the rise in interest rates, with neobanks passing on very little to their customers:

Moreover, the amount of lending most of these banks are doing is small. Customer deposits are being placed at central banks, commercial banks, or invested in short-term government bonds that are now generating attractive yields. This is a low-valuation-multiple earnings stream given its cyclicality, especially at a time of rising interest rates. Bank investors typically discount these peak net-interest margins to reflect the likelihood of rates falling again.

Revolut has said 2023 was another stellar year for growth, with revenue up 75 per cent to around $2bn. After many years of no operational leverage, it has guided for double-digit percentage net profit margins. Subscription revenues are still a small proportion of overall revenues, and crypto trading remains a wild card, but progress is being made.

Revolut 2023 regulatory filing might not arrive until late this year, however, and it will be interesting to see how much growth is the mechanical impact of higher interest income, which Revolut books in revenue on a gross rather than net basis. How profitable will it be once rates decline, or if it has to pass on some of this interest income to clients?

Monzo’s revenue growth for the year ending March 2023 was 130 per cent and it finally hit positive underlying profitability but took a substantial provision for future potential loan losses, showing lending is a tougher business than merely parking cash at the Bank of England. Monzo has started marketing customer loans, following the same path taken by Starling and SME-focused specialist OakNorth.

As these UK neobanks line up to become public companies, they shouldn’t assume near-term growth or headline profitability alone will drive valuation. The hard questions from public market investors will be about earnings quality.

Q2 2024 Earnings Call Transcript")

{kind=link}