SOPA Images/LightRocket via Getty Images![]()

Investment Thesis

UiPath Inc. (NYSE:PATH) designs software robots to automate repetitive tasks for businesses, improving efficiency and reducing errors.

I argue that this stock is still reasonably priced, even though it operates in what’s arguably the hottest sector of the market.

As you’ll soon see from my reasoning, I strive to be very conservative with my assumptions to allow me plenty of room for error.

Accordingly, I believe that UiPath is an attractive stock, while it’s priced at 47x forward non-GAAP operating income. Here’s why.

Rapid Recap

A year ago, I wrote about UiPath in an analysis titled, “I Know It’s Bad, But So Do You“. Since then, the stock has been a very strong performer, up 71% vs. 25% for the S&P 500 (SPY).

Author’s work on PATH

I’ve remained bullish on this stock for the past twelve months and concluded my most recent analysis by stating:

With an emphasis on profitability, the company could achieve $250 million of operating income by 2025, resulting in a valuation of 31x. While not the most inexpensive option, the valuation seems justifiable, particularly considering the anticipated 20% growth in its topline next year and the compelling narrative driving investor interest in the tech sector.

As you’ll soon see, as is my practice, I had been too conservative in my estimates. I now no longer believe that 20% CAGR is on the cards, but in actuality low-20s% CAGR. And also, the business is going to be more profitable than I previously presumed. Hence why I’m bullish on this stock.

Why UiPath? Why Now?

UiPath provides a platform for automation, which means it helps businesses streamline and perform repetitive tasks using software robots. These robots mimic human actions on computers, allowing organizations to automate various processes, from data entry to complex workflows.

Moving on, UiPath’s strategic shift in its go-to-market approach, focusing on organizations with a long-term commitment to enterprise automation, has yielded positive results. This shift has increased UiPath’s visibility in the C-suite and strengthened its partnerships. The company’s success is further highlighted by its record number of fiscal Q3 2024 deals of over $1 million in ARR, a 31% increase y/y in ARR. Notable successes in the Federal sector and partnerships with key organizations like the United States Department of Agriculture exemplify UiPath’s impact on diverse industries.

However, UiPath also faces challenges. In fact, the competitive landscape in the automation market is evolving rapidly and in an effort to retain strong topline growth, its sales and marketing expenses saw a marked sequential increase in fiscal Q3 2024.

Indeed, for UiPath to stay at the forefront of innovation it will have to continually reinvest into newer technologies. For example, the integration of generative AI technologies incorporated into its UiPath Autopilot product is a step in the right direction, but its customer base will require constant updates in its product offering to address this very dynamic sector.

Given this context, let’s now discuss its fundamentals.

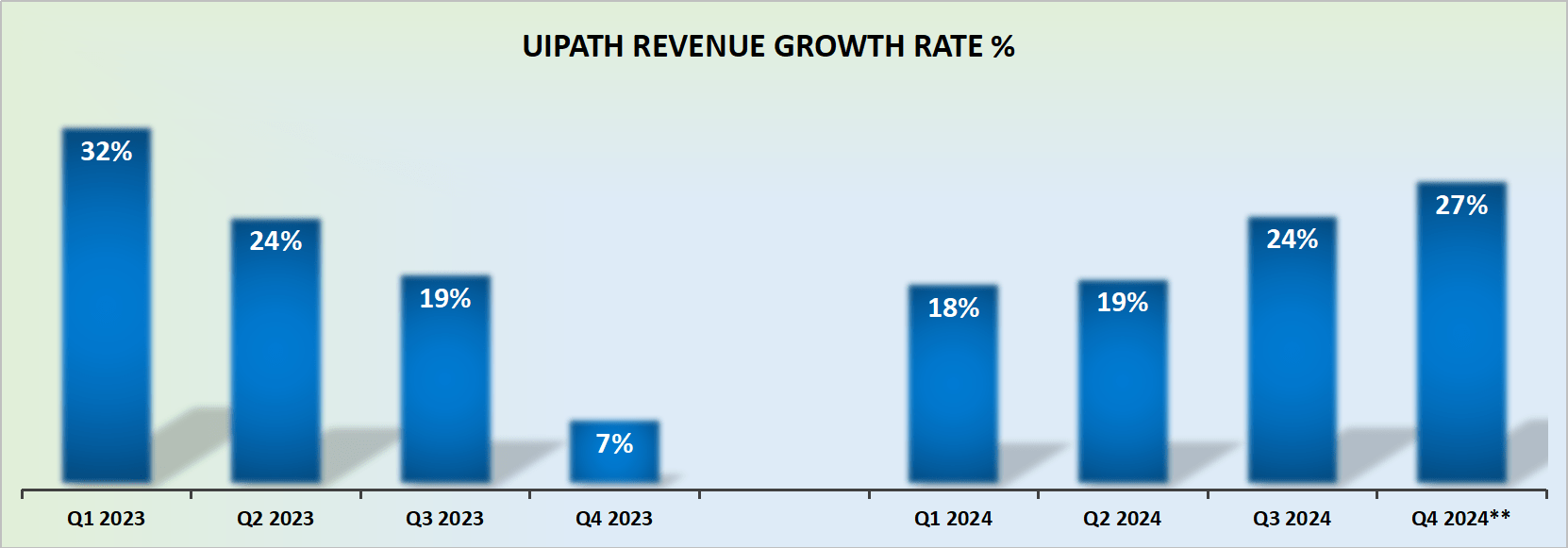

Revenue Growth Rates Stabilize at Low-20s%

PATH revenue growth rates

UiPath could end up delivering approximately low-20s% CAGR in fiscal 2025. That in and of itself is a fair and reasonable revenue growth rate. But what’s best of all, is that its strongest growth rates will take place in H1 2025, starting in this calendar month.

For investors, it will appear that UiPath is on a strong footing and has put its dismal performance of fiscal Q4 2023, of 7% y/y revenue growth rates in the rearview mirror.

Even though, what has, in fact, happened is that UiPath’s revenue growth rates have been moderating over the past couple of quarters. But perception is everything in investing. And here, there will be the perception that UiPath has stabilized its growth rates.

And what do investors truly crave, nearly above all else? Certainty! Investors want to know that the business they are backing isn’t going to lose their capital. Add to that some alluring futuristic story, and provided its valuation is reasonable, the stock can deliver a rewarding return. Indeed, we’ll discuss its valuation next.

PATH Stock Valuation — 47x Forward Non-GAAP Operating Income

Allow me to provide some context. When UiPath guided for fiscal Q3 2024, it guided for $32 million of non-GAAP operating income. But when its results came out, the non-GAAP operating income figure was approximately $44 million, a figure that is substantially higher than its original guidance.

Therefore, when UiPath guides for $78 million in non-GAAP operating income for fiscal Q4 2024, I believe that its actual reported figure will be close to $90 million.

Consequently, even though this is only a 100 basis points expansion in profitability compared with the same period in the prior year, it will be a 30% increase in absolute profits.

Following this reasoning, I believe over the next twelve months, UiPath could be on a forward run-rate of approximately $300 million of non-GAAP operating profits.

To be clear, this does not necessarily mean that UiPath will reach $300 million in fiscal 2025; rather, simply that at some point in the next few quarters its underlying profitability on a forward run-rate could reach this figure.

This would leave UiPath priced at 47x forward non-GAAP operating income – a figure that, I believe, is entirely justified given that UiPath is growing over the coming year in the low-20s% CAGR.

The Bottom Line

In conclusion, my investment thesis on UiPath remains optimistic given UiPath’s strong fundamentals; its revenue growth rates stabilizing at low-20s% especially instills confidence in me.

The integration of generative AI technologies and the potential for a forward run-rate of approximately $300 million in non-GAAP operating profits contribute to the attractiveness of the stock, even at a forward valuation of 47x.

The company’s ability to adapt, innovate, and deliver consistent profitability positions it well for future success, making UiPath a compelling investment option.

Q2 2024 Earnings Call Transcript")