Klaus Vedfelt

Main Thesis / Background

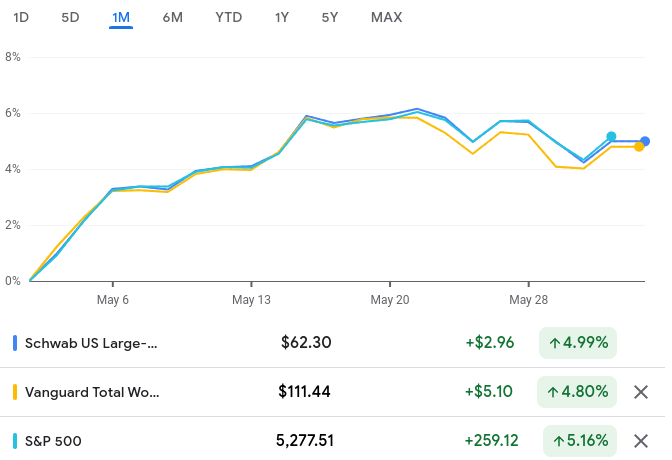

The purpose of this article is to discuss the border equity market and why I continue to believe in the value within large-cap US stocks. This is a follow-up to my review from a month ago when I covered this idea, and large-caps have indeed continued to perform well in the interim – as measured by both the S&P 500 and a large-cap index ETF:

1-Month Price Action (Google Finance)

As you can see, both have produced gains and both have beaten a “total world” ETF tracker (the Vanguard Total World Stock Index (VT)).

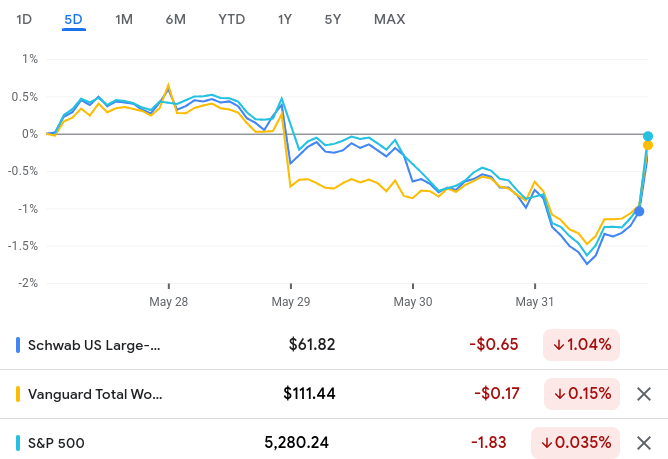

I saw an opportunity to reiterate this thesis as we are approaching the mid-year mark and equities as a whole saw some volatility over the past week. The uptick daily swings may have some readers feeling a bit uneasy – and who can blame them after the year we have already had!?

Last Week Price Action (Google Finance)

With this backdrop – strong gains but short-term weakness – I figured it was time to reassure my followers why I continue to believe in large-cap US stocks for the months ahead. I won’t let temporary price action dictate my long range planning and there are a host of reasons why I believe the S&P 500 (the most common large-cap benchmark) will be an alpha-generator compared to the rest of the world in the second half of the year. I will take each supporting reason in turn in the following paragraphs below.

*I own the Vanguard S&P 500 ETF (VOO) and it is my largest individual holding. That will continue to be the case for the foreseeable future. The Schwab U.S. Large-Cap ETF (SCHX) is also a great option with an identical expense ratio of .03%.

US Large-Caps Offer Plenty Of International Exposure

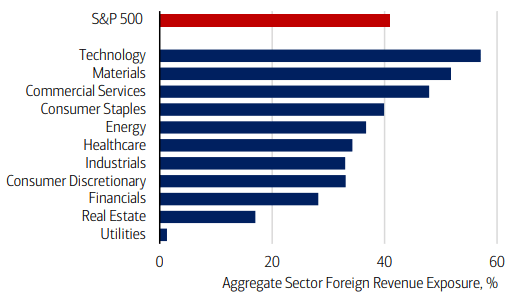

A key theme that has grown over time has been how large-cap US stocks have enhanced their non-US exposure. While this is not necessarily true across the board, it is absolutely true for the largest sector within this index – Information Technology – and other consumer-oriented arenas.

This is important because if one just buys an average large-cap stock, it may or may not have international exposure. Some companies (think many utility providers) are almost exclusively domestic-focused. But when one looks at a “large-cap” US index fund, the fact is this is dominated by the Mag 7 and Info Tech in particular. So unless one is getting more creative with their holdings, if they own a large-cap US stock ETF then they probably have a good bit of international presence even if they don’t realize it.

To put this in perspective, let us look at sources of revenue for each S&P 500 sector. The results vary but, as I mentioned, the biggest weightings in the index also have the largest contributions of non-US revenue to their overall revenue picture:

Share of non-US Revenue (By Sector) (Merrill)

Now, I am not here to say don’t invest in non-US stocks. I do and have written about the reasons why many times. But what I do want to emphasize is that even if one is getting concerned about negative headlines in the US – that shouldn’t necessarily steer you out of US equities. This is because the largest US corporations do plenty of business overseas and are more concerned about the global economy than they are about any one particular jurisdiction. Is America most important? I would say yes. But just because America may see a negative headline or two doesn’t mean all large corporations domiciled here are going to feel a lot of pain.

This reality provides built-in diversification. Not only that, but when the dollar drops as it has been in the last few months, that can actually improve US large-cap earnings because their overseas revenue (in foreign currency) can convert in to more USD:

USD Index (Bloomberg)

Ultimately, I see an environment where large-cap US stocks have some positive catalysts. They are positioned well for international growth and have a tailwind for a softening dollar in the hopes of Fed rate cuts at some point in the next 6-12 months. This makes it easy for me to “stay the course” with my S&P 500, Dow Jones, and NASDAQ 100 holdings.

**In addition to VOO, I own the SPDR Dow Jones Industrial Average ETF Trust (DIA) and the NASDAQ QQQ (QQQ).

This Isn’t A FOMO Rally

The next topic to cover is why I think there is support for current (and higher) equity prices going forward. It has to do with investor confidence or enthusiasm – which is often a contrarian indicator. Simply put, when I see markets making new highs (as they have been) and investor caution has been thrown to the wind, that is when I start to shift to cash, gold, munis, and other asset classes. I have done that consistently over the years when I feel investors are ignoring risks and getting too hyped-up. And it often works out to be advantageous.

The logic behind this is that often when exuberance takes hold of the market, the fall down can be hard. That is because when markets rise, those on the sidelines who were being patient can no longer stand it and dive in – often at the exact wrong time. This is known as “fear of missing out”. While it is easy to be cautious when the market is swooning, it is much harder to be when you are sitting in cash (or other less risky alternatives) and your friends and peers who are taking on more risk are being rewarded for it. This can bring in those on the sidelines near the top and, eventually, the buying fervor runs out because there is nobody left to buy! The inevitable drop happens.

I am highlighting this because it is not what I am seeing right now. If it was, I would not be out here writing a bullish review. Rather, investors are starting to get cautious and are almost anticipating a short-term pullback or larger drop. We can see this in the form of option’s activity. At time of writing, the cost of hedging against a 10% drop in the S&P 500 is now nearing the high set back in October last year:

Options Pricing (Yahoo Finance)

Now, this doesn’t mean in any way that markets are destined to see going forward. I think they are, but I could be wrong – I am not infallible. But the point I am trying to convey is there is plenty of caution out there in the market. Investors are paying up for protection against a crash. That could wind up being the right move on their part, but I see this as a positive because it means markets are acting rationally. When that stops happening, I get nervous, and for now I am pretty comfortable.

What If Something Bad Does Happen?

Naturally, there are risks to investing at these levels. I’m not going to sit here and proclaim a wildly bullish outlook and ignore current risks. The market has been on a roll for a while and that will inevitably correct at some point. I think the risk-reward proposition is favorable, but investing at all-time highs can be a mixed bag. We need to remember that markets are getting pricey (in both absolute terms and relative to history) so some levelheadedness is needed here. I am not suggesting investors go all-in or buy “hand over first”. I don’t think that kind of pumping serves anyone, and I will never engage in that type of hyperbole.

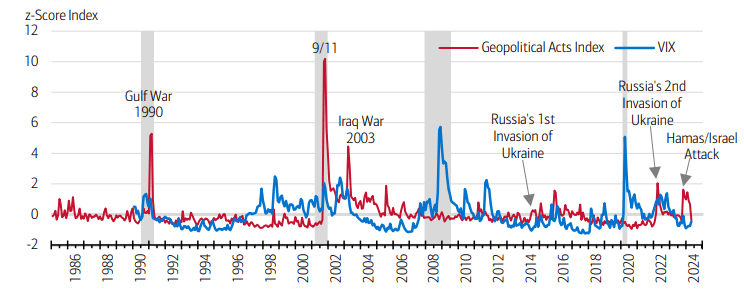

However, to balance out this review, let us be aware of some of the major headline risks that could pop up again and derail things. Many of these risks are geo-political and I wouldn’t “ignore” them now, but they have been ongoing for a while so I don’t see them as significant headlines. But forces like the Russia-Ukraine war, conflict in Gaza, potential for China to get more aggressive towards Taiwan, all of these have global implications. So while they look like regional conflicts, they are bringing in the world superpowers and that has the potential to spill into something bigger. So far, containment has been achieved, but that could change.

So what if that does change? Or a new conflict pops up all together? The result will probably be bad for stocks. But the good news is that “bad” tends to be fleeting. If we look back at history – including the recent conflicts I just mentioned – we see that their impact on US stocks tends to be short-lived:

Volatility During & After Geo-Political Events (Wall Street Journal)

This is essential to understand a long term plan. While we can’t predict with certainty when the next black swan event will happen, or the next military conflict, we can have assurance that those events tend to smooth out over time and present a buying opportunity. Sure, things like the GFC and Covid-19 caused major disruptions to equity markets. But we can’t invest like those types of events are right around the corner. Well, you can, but you will likely lose out on years of compounding and dividends if you do. For today, I can take comfort knowing that the next event to cause a spike in volatility will probably be a fleeting occurrence, as history tells us most are.

Be Tactical If You Move Outside The US

My final point takes a look at diversification. The benefits are well-known and I have amplified this reality in many reviews. I hold non-US exposure, this review that is positive about US stocks should not distract from the fact that I own and will continue to own shares outside my domestic borders. There is merit to it to round out a portfolio and to capture country-specific catalysts. That is the case today and will be tomorrow.

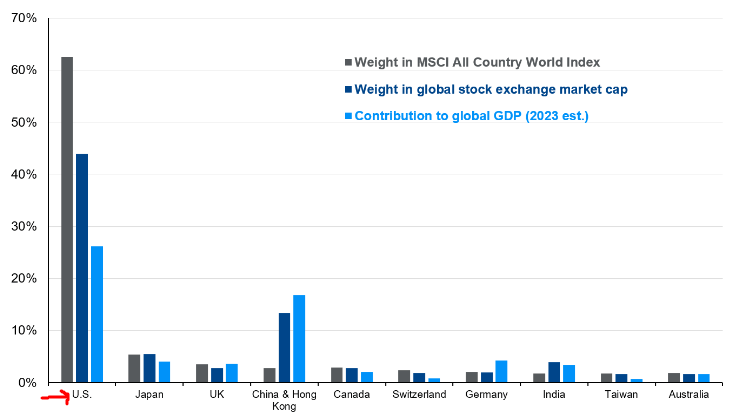

But I want to make clear that readers should look beyond funds with just “global” or “all world” in the name. Make sure to understand what you want to own and if the funds you are considering really offer it. For example, just because you picked a “global” fund or developed markets fund, you may wind up with more US exposure than you think. This may not be a bad thing inherently, but it is somewhat self-defeating if your reason for owning it is to get non-US exposure. I bring this up because many global indices tend to be US-heavy, as illustrated in the graphic below:

Weightings in Global Indices (By Nation) (JPMorgan)

This is not really meant as a word of caution but rather one to be critical of the funds you own, what you want out of them, and what they offer. If a “global” fund is dominated by US shares – is that really meeting an objective to diversify? This is simply a point to consider, but an important one at that.

**For non-US holdings, I own multiple country ETF. These include the iShares Canada ETF (EWC) and the iShares Mexico ETF (EWW). I also own the SPDR Euro STOXX 50 ETF (FEZ) for European large-caps and the Schwab International Equity ETF (SCHF) primarily for the Japanese and British exposure it offers.

Bottom-line

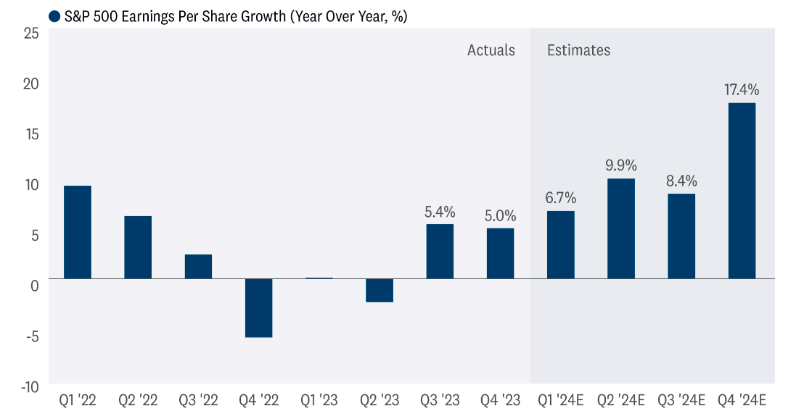

With the swings of the past week fresh on my mind, I thought it was an opportune time to reiterate why I continue to like large-cap US stocks in 2024. Are prices getting a bit carried away? Perhaps, but earnings are rising, which is the primary driver of share prices long-term:

S&P 500 Earnings Growth (By Quarter) (FactSet)

Also, there is plenty of caution in the market to suggest we aren’t in a euphoric state – which would leave me very concerned.

To sum it up, I remain an equity bull, especially with respect to large-cap US equities. While last week was a bit unnerving, the month of May was positive in its entirety. I expect the S&P 500 to build on this momentum going into the summer months ahead.

Q2 2024 Earnings Call Transcript")