mysticenergy

For some background, we first wrote up Black Stone Minerals (BSM) in early 2019. We added to it throughout the pandemic and continue to recommend the units to investors.

We have more recently discussed for subscribers Healthcare Realty (HR), a medical office building REIT that looks like a terrific name to hold in a recession. These are stable assets that would perform well even in a downturn. We like HR equity as it appears quite oversold, trading at a discount to private valuations with a near 8% yield. Historically, HR traded between a 3% and 5% yield.

We purchased Healthcare Realty shares just last December here.

Black Stone Minerals

For the March quarter, Black Stone Minerals beat estimates nicely, with EBITDA of $104 million (vs $93 million Street estimates). The company earned Distributable Cash Flow (DCF) of $0.46 per share. That was down from $0.59 in the fourth quarter of 2023.

The company cut the distribution by 22%, but we generally knew that between 1) lower natural gas prices and 2) some expiring gas hedges, that earnings and the distribution would fall.

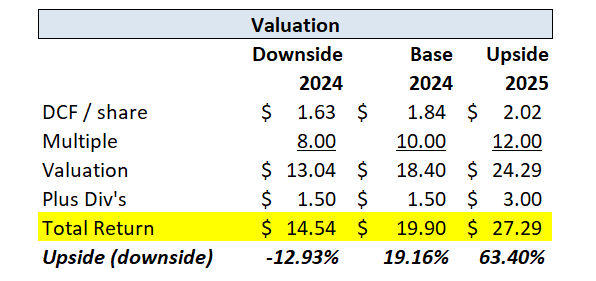

With coverage now at 1.22x and a 9% yield, we continue to like Black Stone units (yes, it is an MLP). We had earlier modeled that DCF per share could fall to $1.63 in 2024 from over $2.14 in 2023. Run rate figures at $1.84 look impressive today, and BSM has begun to hedge out 2025 production too at around $3.65 per mcf.

Sensitivity to oil and gas prices does not look too bad right now. At $2 gas and $60 oil, a downside case, BSM would earn about $1.55 in DCF per share, still enough to cover the current $1.50 distribution.

At current prices, $2.50 gas and $78 WTI oil, we calculate $1.71 of DCF per share. This does include the $12.5 million of lease bonuses, or $0.06, so that could go away in a downturn. Production might also fall, but is currently expected to move higher by 6% in 2024 compared to last year.

For the quarter, production volumes fell 2% YoY and realized prices fell 12%. Seems like earnings are at a trough now, and any jump in natural gas off of its recent lows could really help this stock.

Author’s spreadsheet

We upgrade BSM to a buy here (as we’ve mostly been holding units as gas prices have normalized). Long term, it is a great inflation hedge and even if the company does not grow, then ~9% annual returns are fine by us. We had thought last year that a lower distribution might entail some pressure on the units. But now their distribution coverage is higher than is typical, and therefore, distribution cut risks behind us.

Healthcare Realty

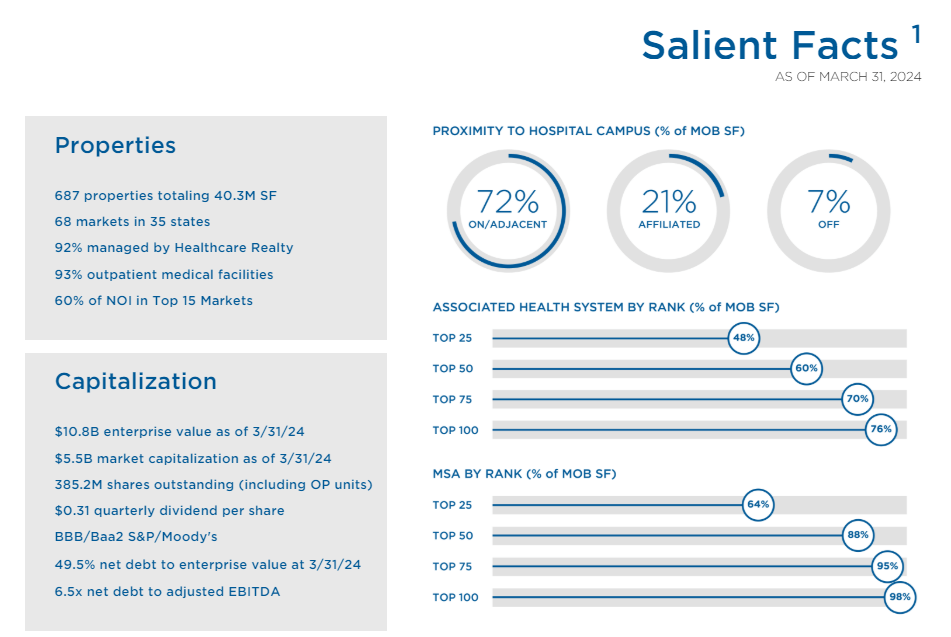

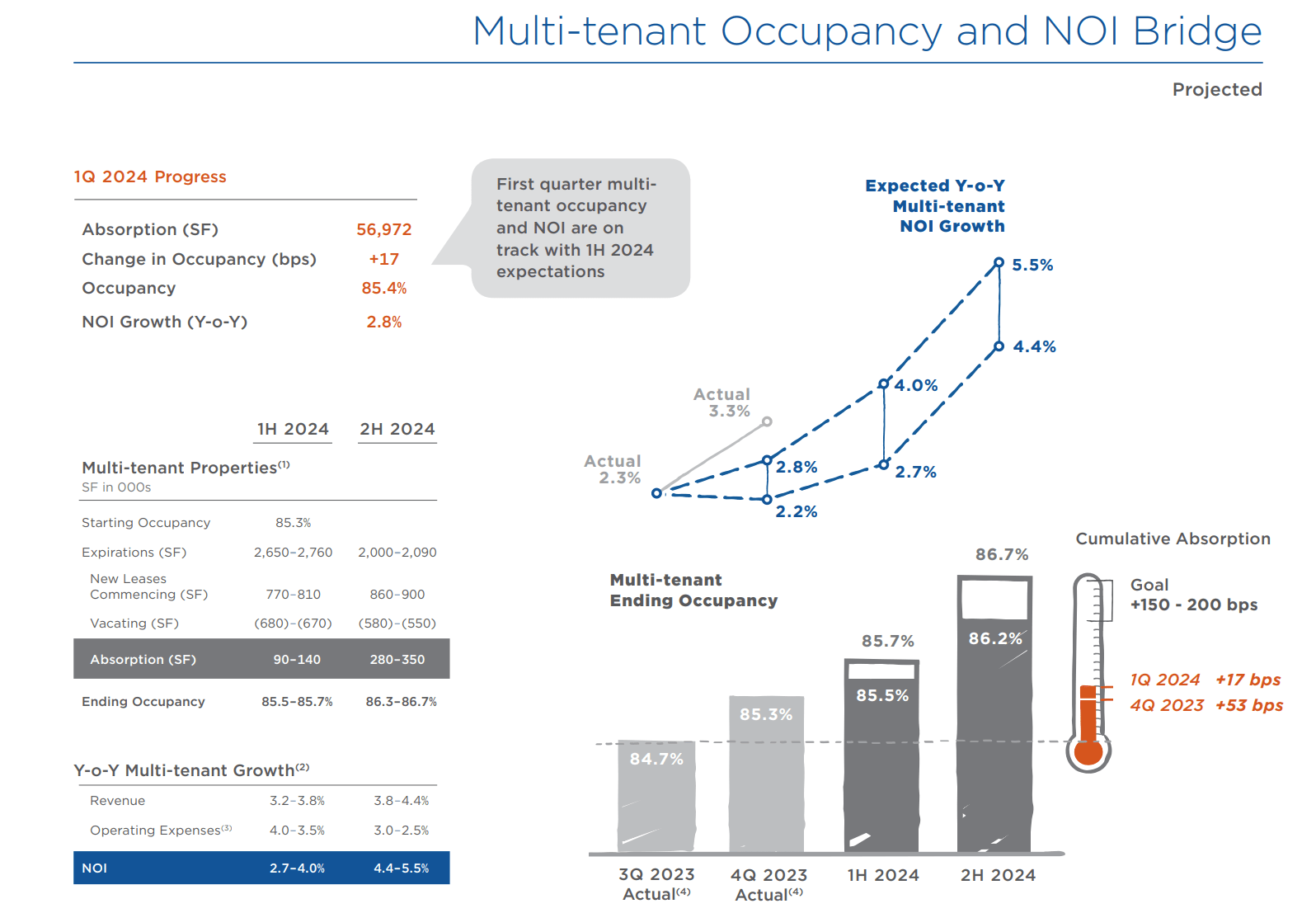

Below is a relevant slide to Healthcare Realty as of the end of March.

HR investor relations

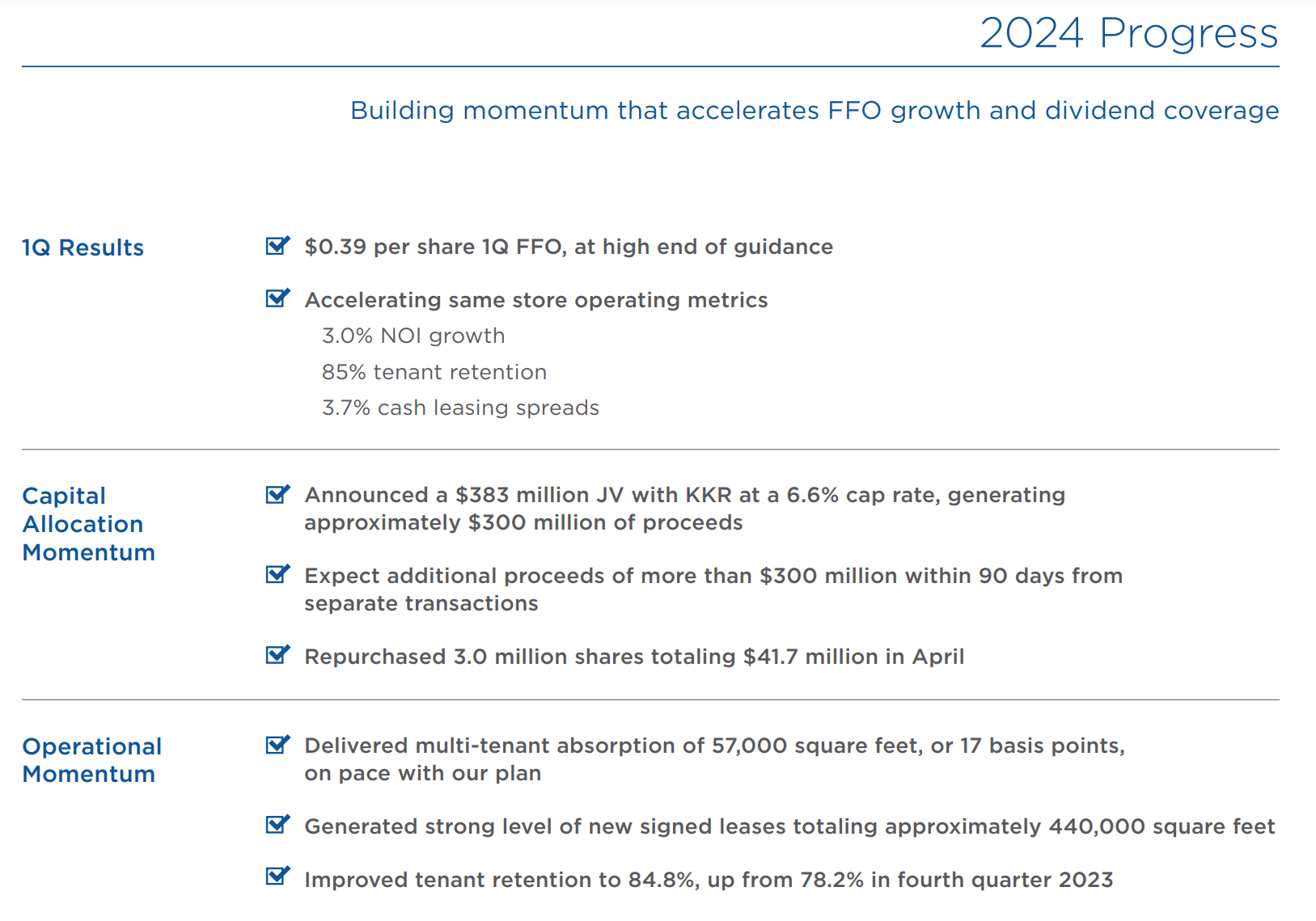

For the March quarter, Healthcare Realty beat AFFO per share estimates by 1c at 39c. Guidance for Q2 is 38-39c and estimates are 39c. Guidance was reaffirmed at $1.54 for 2024 in AFFO per share terms.

Company Investor Relations

Pretty stable business. Recall that HR has kept the dividend flat at either 30c or 31c per quarter since cutting it in 2010 (from 39c per quarter).

HR also announced a new joint venture with KKR, selling an 80% stake in 12 different assets for roughly $300 million. The 6.6% cap rate seems a solid valuation and is exactly in line with asset sales last year. The company also announced another $300 million in pending asset sales (letters of intent at this stage) likely in the 6.5-6.75% cap rate range.

We discussed HR here most recently.

We would re-iterate that a 6.6% cap rate implies a stock worth $19.85 per share. A 7% cap rates implies a $17 stock. HR closed at $15.87 last week.

Management intends to use excess capital (after paying down some debt that costs around 6.25%) to buy back shares. Finally, HR is willing to sell assets at a low cap rate and buy back shares at a higher cap rate.

This should be accretive, but management on the call would not quantify the level of accretion. Of course, it is impossible to know at what price the company will buy back shares. But current Q2 and 2024 guidance ($1.52 to $1.56 in AFFO) have not yet factored in these asset sales or any repurchases.

So we think there is likely upside here.

A key element to the turnaround story here is occupancy.

Company Investor Relations

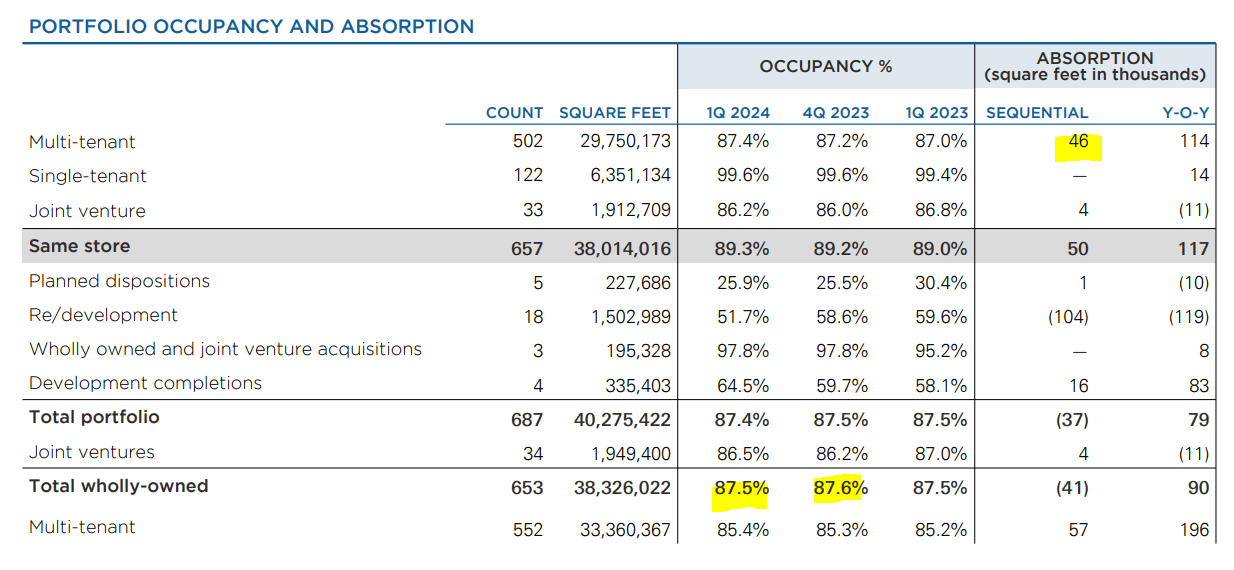

Improving occupancy is key to improving net operating income. Above, we can see that same store occupancy improved by 50 bps in Q1. Last year, NOI grew only 2.3%. In Q1, NOI growth was better at 3.0%. The company though has a goal to grow NOI by 4.4-5.5% in 2024. Seems a stretch, but the trend is not bad.

Here is their progress.

Company Investor Relations

As for expiries, new leases were done in the March quarter at 3.7% higher rent rates. Contracted rent increases are 3.0%.

The buyback plan is now $500 million, which is large at 8% of the shares outstanding. We think the company can buy back $350 million of stock at least post-closing the KKR deal and other $300 million asset sales. This assumes NOI of $41 million on $600 million of asset sales, a 6.75% cap rate, less 6.5x EBITDA for debt repayment (or $250 million of debt repayments which leaves the balance for share buybacks).

That could boost AFFO per share from guidance of $1.56 to a run rate of $1.65.

Funds available for distribution (FAD) look a little better in 2025 than our prior estimates, with a payout ratio of 0.99x (5% improvement from our figures in Q4).

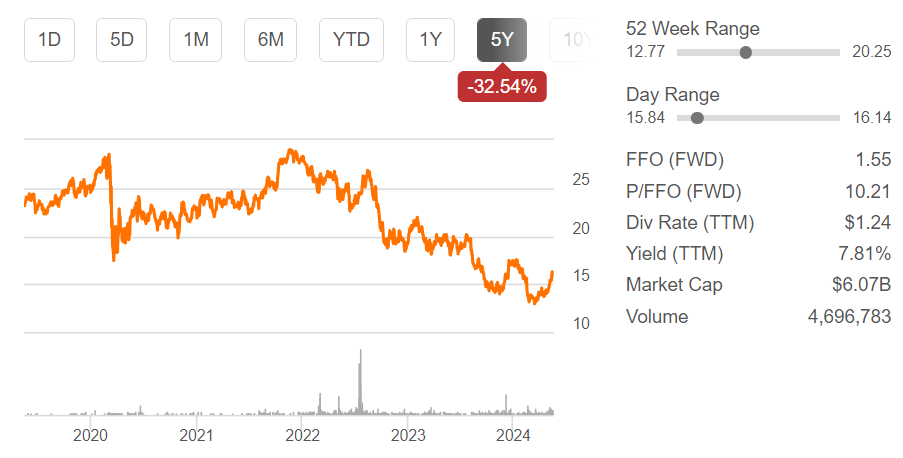

Last quarter, we thought that HR could be a $10-20 stock. A dividend cut now seems unlikely given the asset sales. We’d call the range now $12-20, with recent management moves encouraging.

The stock will admittedly be rate-dependent but does seem to have a pretty big margin of safety. Currently, the stock is trading at a 7.3% cap rate.

Note that HR equity has been mauled in the past five years, despite AFFO holding up well amidst much higher interest rates (AFFO per share was $1.53 in 2017).

Seeking Alpha

Finally, while higher rates have been tough on REITs, generally speaking, real estate values improve alongside inflation. Healthcare assets continue to be in demand and this could be a nice play even in an inflationary environment, as long as HR manages the balance sheet intelligently and demand for medical office buildings remains intact.

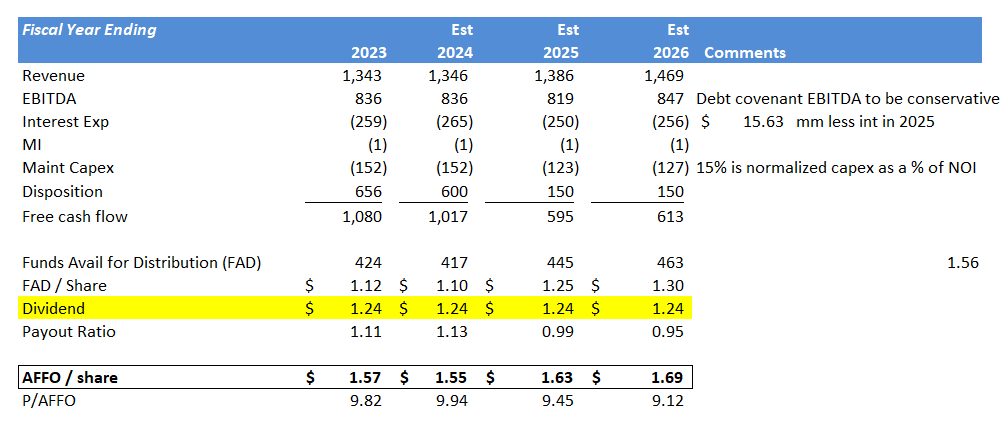

Below is our summary model on AFFO per share over the next couple of years.

Author’s Spreadsheet

Holding here, but the trends are improving, and we’d add shares below $15 given the asset sales.

Q2 2024 Earnings Call Transcript")