Stay informed with free updates

Simply sign up to the US economy myFT Digest — delivered directly to your inbox.

Sentiment analysis is tablestakes quant stuff these days. Any slack-jawed yokel with a Bloomberg terminal can now systematically parse and trade central banker comments or newspaper chatter.

However, most only use exhaust from social media, maybe 10-20 years worth of earnings call transcripts and central bank bloviation, and not much more of online newspaper reports.

In a paper published by NBER this week, Jules van Binsbergen, Svetlana Bryzgalova, Mayukh Mukhopadhyay and Varun Sharma go further. Much much much further.

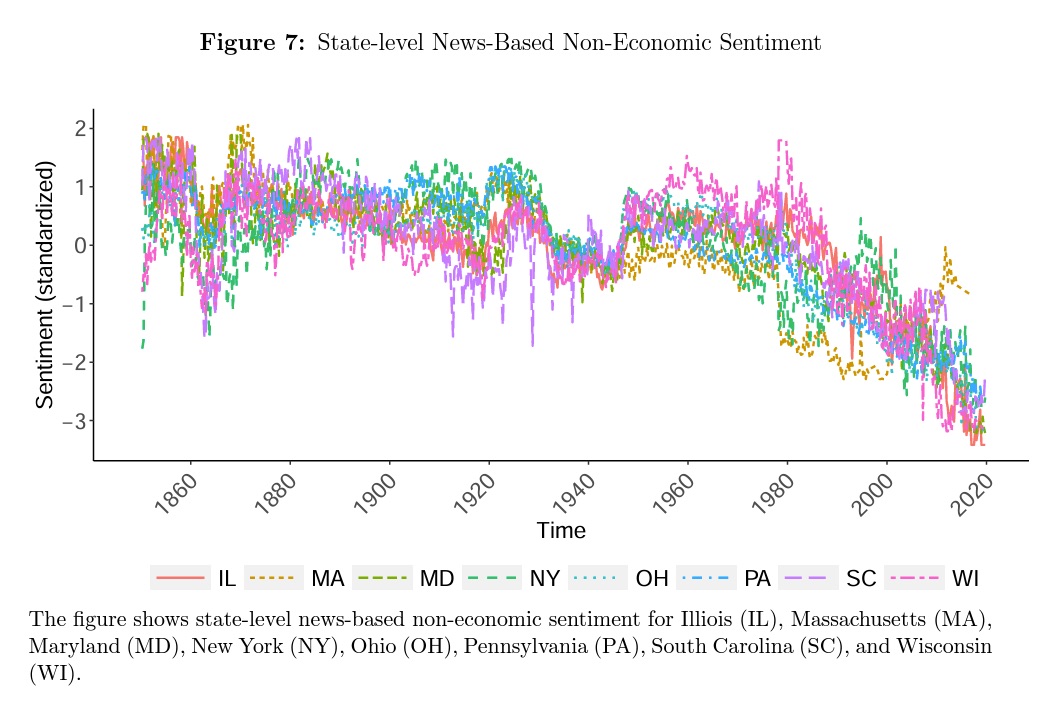

We use a historical collection of 170 years of digitized newspapers, which includes the text of 200 million newspaper pages from 13,000 local newspapers. Our corpus includes approximately one billion newspaper articles, a major increment over the Wall Street Journal corpus, a much-used source of text data in economics and finance that contains about 1 million articles. In fact, our data is about 95 times larger than the total number of English-language Wikipedia entries combined. By leveraging the collection of local newspapers, we can measure sentiment at a higher degree of granularity, such as the county or state level.

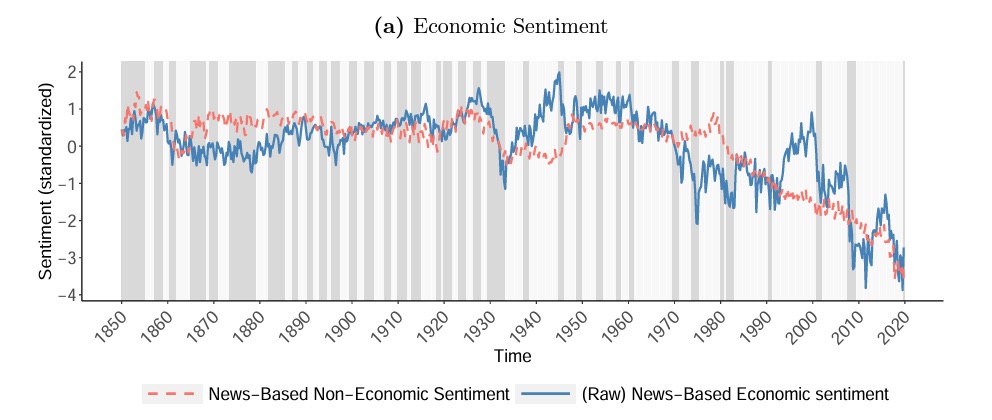

To be fair though, almost two centuries of textual sentiment analysis is pretty cool. Using a natural language processing algorithm called Word2vec they say they’ve been able to produce continuous (and predictive!) measures of economic and non-economic sentiment since 1850.

It appears that the two measures have opposite effects. Economic sentiment positively predicts growth (and the signal is getting stronger) while non-economic sentiment predicts it negatively (and is getting weaker).

The results they claim are striking, with a one-standard deviation increase in sentiment leading to a 2 percentage point increase in economic growth the following year.

Our measure predicts GDP (both nationally and locally), consumption, and employment growth, even after controlling for commonly used predictors, as well as monetary policy decisions. Our measure is distinct from the information in expert forecasts and leads its consensus value.

This would suggest that sentiment drives economic growth more than economic growth drives sentiment — something that’s been a big topic year.

But to Alphaville’s eyes the most interesting aspect is how both economic and non-economic sentiment has collapsed over the past 50 years, despite far fewer economic setbacks (zoomable version).

So the current debate about the gap between the actual economic data and how dour Americans are should probably be seen in light of this half-century secular trend.

You can see the same pattern in the state level sentiment analysis (zoomable version):

Given the starkness of the deteriorating sentiment trend since the 1970s the researchers had to adjust for it in their models — or “de-bias” it for the secular increase in media gloom versus the actual economic data — and spent some time discussing the potential drivers:

Because the public needs to be aware of important risks in society, a certain level of general negative bias in news coverage is expected, particularly if one adheres to the view that traditional media fulfills a watchdog/surveillance function. Although this argument could explain the average level of negativity in news reporting, it does not address its increasingly downward trend. What factors could speak to it? The world of news, especially that of printed newspapers, has become increasingly competitive over the years. Therefore, it is natural to expect that to attract a larger audience, many outlets have been increasingly focusing on negative news. It is well-known that people are more responsive to negative information. Fighting the media negativity bias, the local Russian newspaper City Reporter decided in 2014 to report only positive news for a day and lost two-thirds of its readers.

Sadly, that doesn’t seem unreasonable. It also meshes with what our colleague John Burn-Murdoch wrote recently, looking at the evidence of more angst-ridden versus optimistic books since 1500.

But eyeballing the chart above, it seems like the falling frequency of recessions might have meant that the sentiment impact of each economic downturn is actually far sharper, and is slower to recover afterwards.

Or in other words, when recessions were just part of the weather, people shrugged them off more easily, but nowadays every one is cause for existential national angst. Perhaps we’ve all just become economic snowflakes?

Further reading:

— Is the vibecession really over? (FTAV)

— Should we believe Americans when they say the economy is bad? (FT)

Q2 2024 Earnings Call Transcript")

{kind=link}

{kind=link}