We Are

We previously covered Taiwan Semiconductor Manufacturing Company Limited (NYSE:TSM) in October 2023, discussing the promising bottoming of the semiconductor cycle, further aided by the timely PC/ server/ smartphone refresh cycles since the pandemic boom.

Thanks to the robust demand for Generative AI and growing global footprint, we believed the foundry’s prospects appeared to be brighter, warranting our Buy rating then.

In this article, we shall discuss TSM’s impressive performance in the recent FQ4’23 earnings call, with the optimistic FY2024 guidance further cementing the semiconductor investment thesis, as generative AI provides the long-term growth tailwinds over the next decade.

Combined with the stock’s attractive risk/ reward ratio, we continue to rate the stock as a Buy, preferably at its previous support levels of $100s for an improved margin of safety.

TSM’s Foundry Investment Thesis Remains Robust

For now, TSM has delivered a mixed FQ4’23 earnings call, with revenues of $19.62B (+14.4% QoQ/ inline YoY) and adj EPS of $1.44 (+13.1% QoQ/ -19.2 YoY).

The impacted profitability is mostly attributed to the growing operating expenses of $2.24B (+4.2% QoQ/ +10.9% YoY), resulting in its moderating operating margins of 41.5% (-0.2 points QoQ/ -10.4 YoY), though still improved compared to FY2019 margins of 35.2% (-2.4 points YoY).

However, with TSM still generating robust FCF profitability of $7.17B in the latest quarter (+230% QoQ/ +50% YoY) or $9.37B in FY2023 (-44.2% YoY), we are not overly concerned for now.

In addition, readers must also note that the intensified operating and capital expenditures are mostly attributed to the management’s sustained investments in the 3nm/ 2nm development and increased footprints in Japan/ Arizona, respectively.

These efforts will eventually be accretive to TSM’s foundry expertise and manufacturing capabilities as well, ensuring that it can maintain its competitive edge in an intensifying market competition, as Intel (INTC) ramps up its foundry ambitions over the next few years.

For example, TSM already generates 50% of its FQ4’23 revenues from 3nm and 5nm technologies (+7 points QoQ/ +18 YoY), indicating the increased demand for its leading-edge offerings.

At the same time, the North American region increasingly comprise a larger portion of the foundry’s revenues at 72% (+3 points QoQ/ YoY), securing its top/ bottom line performance ahead, no matter the ongoing trade war and uncertain geopolitical issues.

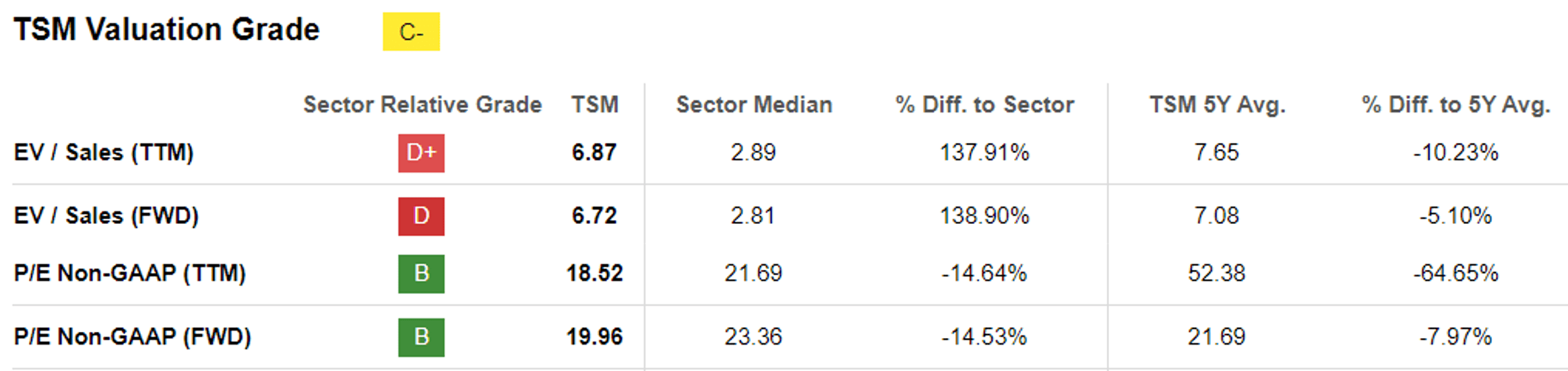

TSM Valuations

Seeking Alpha

As result of the ongoing tailwinds, TSM’s FWD P/E valuation of 19.96x appears to be justifiable, after the much needed recovery from its 1Y mean of 15.74x, though slightly elevated compared to its 3Y pre-pandemic mean of 18.00x.

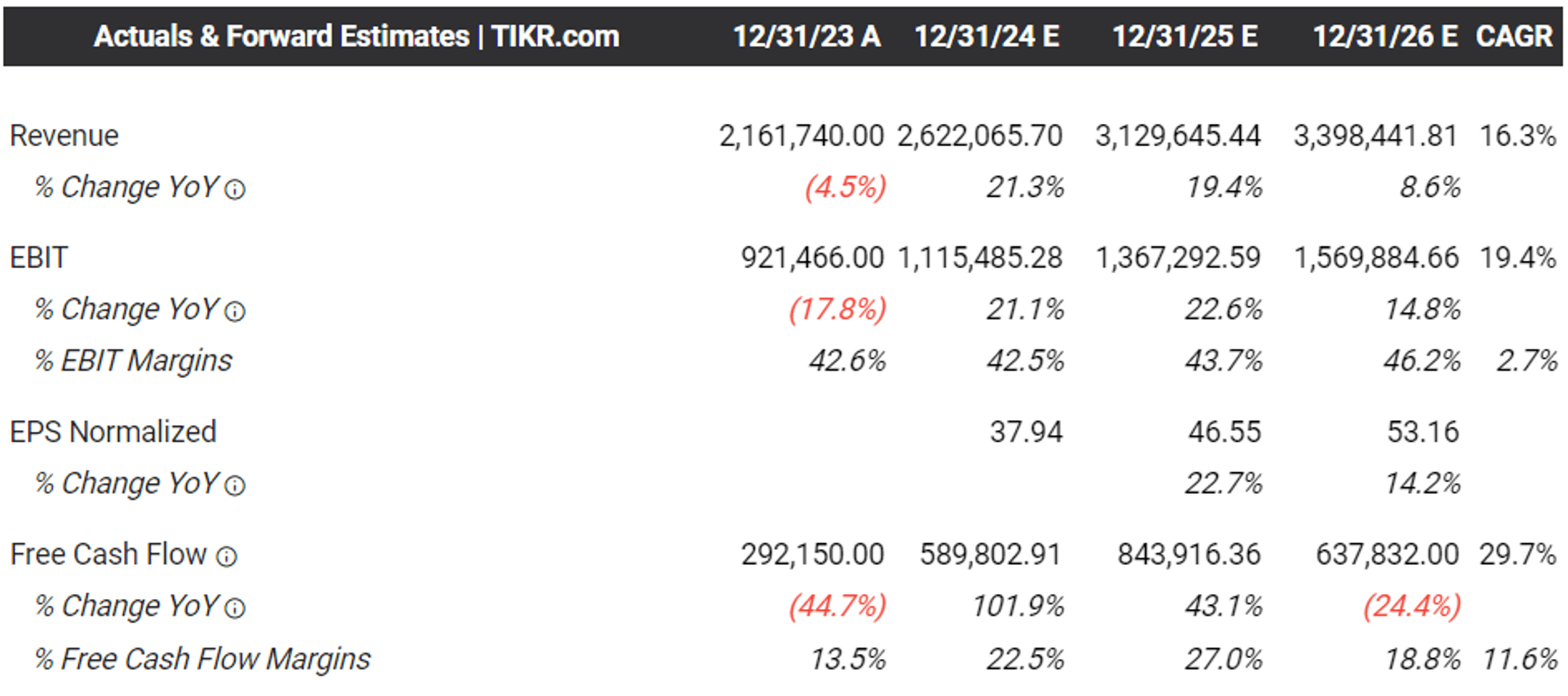

The Consensus Forward Estimates (In NTD)

Tikr Terminal

Perhaps its growth premium valuations are attributed to the promising consensus estimates, with TSM expected to generate an improved top/ bottom line expansions at a CAGR of +16.3% and +18% through FY2026.

This is compared to the previous estimates of +13.5%/ +16% and the normalized top/ bottom line growth at a CAGR of +12.5%/ +14% between FY2016 and FY2023, respectively.

The raised estimates indicate the foundry’s robust tailwinds from the increased adoption of cloud computing, generative AI hype, and Metaverse/ spatial computing platforms.

This optimistic trend is likely aided by TSM’s optimistic FY2024 guidance as well, with the management expecting over +20% in revenue growth, further aided by the “strong ramp up of its industry leading 3nm technology and strong demand for the 5nm technology.”

With FQ1’24 revenue guidance of $18.4B at the midpoint (-7.1% QoQ/ +10.7% YoY), it is apparent that the growing generative AI demand is more than sufficient to offset the handset and automotive weaknesses thus far.

Combined with the cooling inflation and the Fed’s potential pivot from Q1’24 onwards, it is apparent that TSM only stands to benefit in the long-term, as generative AI demand grows and tech spending ramps up.

The same has been recently reported by Super Micro Computer (SMCI), a company that offers complete server assembly, system integration, and related infrastructure services for five key partners, including Nvidia (NVDA), Intel Corporation, Advanced Micro Devices (AMD), Samsung Electronics (OTCPK:SSNLF), and Micron Technology (MU).

SMCI has further raised its FQ2’24 midpoint guidance to revenues of $3.625B (+71.8% QoQ/ +101% YoY) and adj EPS of $5.475 (+59.6% QoQ/ +67.9% YoY), compared to the prior guidance of $2.8B (+32.7% QoQ/ +55.5% YoY) and $4.64 (+35.2% QoQ/ +42.3% YoY).

This builds upon the optimistic FQ4’24 guidance previously offered by the market leader for AI chips, NVDA, with revenues of $20B (+10.3% QoQ/ +230.5% YoY) and GAAP gross margins of 74.5% (+0.5 points QoQ/ +11.2 YoY).

We reckon that NVDA may very well smash its own guidance in the upcoming earnings call on February 21, 2024, as well, as it has in the previous earnings call.

This further underscores the inherent importance of the world’s leading foundry, TSM, as a new market opportunity opens up with the TAM for Generative AI Hardware projected to grow from $37.97B in 2022 to $641.73B in 2032, expanding at an impressive CAGR of +32.6%.

So, Is TSM Stock A Buy, Sell, or Hold?

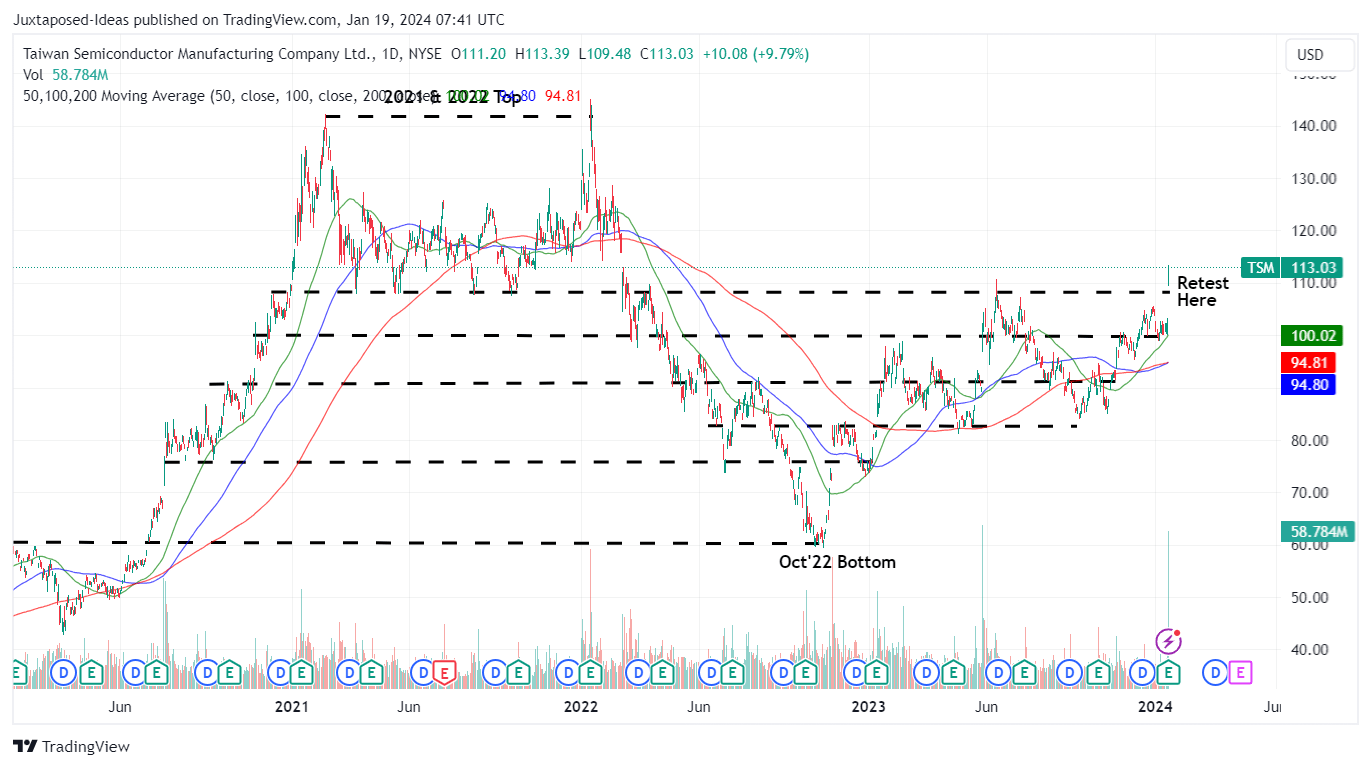

TSM 3Y Stock Price

Trading View

For now, TSM has rallied drastically since the recent earnings call, with the stock rapid breaking out of its 50/ 100/ 200 day moving averages since the October 2023 bottom and currently retesting its 2022 resistance levels of $110s.

Based on its FY2023 adj EPS of $6.57 (+59.4% YoY) and its FWD P/E valuation of 19.96x, the stock is also trading below its fair value of $131.10. Based on the consensus FY2026 adj EPS estimates of $8.91, there appears to be an excellent upside potential of +57.3% to our long-term price target of $177.80 as well.

While geopolitical concerns persist, with TSM delaying part of its production plans in Arizona through 2028 (compared to the original guidance of 2026), we are not over concerned, thanks to the thawing US and China relations as trade and travel restrictions lift.

Assuming so, we may see the October 2023 bottom hold, allowing the Chinese-based ADR to further rally as its FWD P/E valuations hold stable at current levels.

Combined with the robust long term tailwinds and profitable growth trend, we continue to rate TSM as a Buy, though with no specific entry point since it depends on individual investor’s dollar cost averages and risk appetite.

Interested investors may want to wait for a moderate retracement to the previous support levels of $100s for an improved margin of safety, since it remains to be seen if the stock may be able to retain much of its one day gains of over +12%.

Only time may tell.

Q2 2024 Earnings Call Transcript")