Dimensions/E+ via Getty Images

Amid an ultra-high market environment where the S&P 500 is still sitting at the ~5,000 watermark in spite of recent concerns about the pace of Fed rate decreases, it’s a great time for investors to be extra selective in their stock-picking. I, in particular, am favoring rebound plays: companies that had weaker 2023 but have strong catalysts for a turnaround this year.

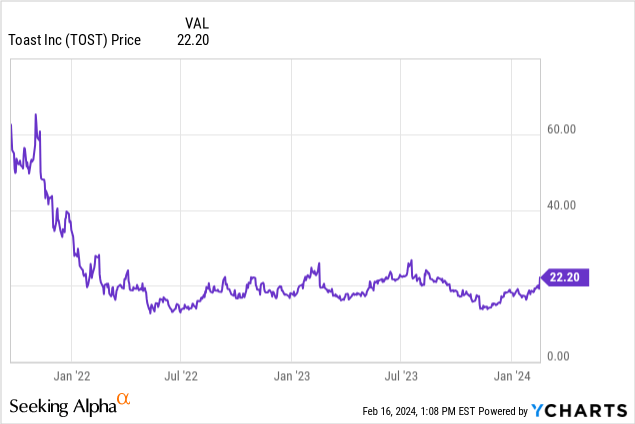

Toast (NYSE:TOST), meanwhile, is one of my top picks in this bucket. This PoS software company continues to expand rapidly across the U.S. while diversifying its product portfolio and achieving leverage on its bottom line. The company just released strong Q4 results, and combined with a robust outlook for the year ahead, the stock has soared more than 20% year to date. In my view, there’s more upside to go.

I last wrote a bullish note on Toast in November, when the stock was trading in the high teens. Since then, on top of a strong Q4 earnings cycle, the company has also announced a broad layoff of 550 employees (more than 10 of its workforce) as the company turns its focus toward profitability. In addition to this, Toast also announced a new $250 million share buyback program, which makes great use of the company’s cash war chest ($588 million on its most recent balance sheet, against no debt) and can take advantage of share prices that are still well below post-IPO highs above $50.

Though I’ve enjoyed the sharp rally over the last few months, I remain quite bullish on Toast’s prospects throughout the remainder of the year and am content to hold onto my position. On top of these more near-term catalysts of share buybacks and workforce reductions, here’s a reminder as to my full long-term bull case for Toast:

- Dramatic opportunity to expand both geographically and horizontally. Toast is no longer just a specialized PoS system for restaurants; the company is aiming to be the software management platform of choice for restaurants, which positions it well versus more generalized competitors like Square. Overall, Toast has estimated its TAM at $110 billion, which indicates less than 1% current penetration.

- Cross-selling momentum is deepening. More to the point above, more than 40% of Toast customers are now using six or more Toast products, versus a rate in the mid-20%s two years ago.

- Holistic platform that empowers hybrid service models. Toast no longer serves only dine-in, either. The company’s software helps businesses manage takeout orders and even larger corporate catering events.

- Reaching the cusp of profitability. Greater revenue mix into software as well as growing economies of scale are also helping Toast approach adjusted profitability for the first time.

All in all, it remains a great time to be invested in Toast while the company is enjoying tailwinds from its current growth expansion plus is expected to benefit from greater economies of scale this year as gross profit growth exceeds revenue growth, and with additional efficiencies from opex reductions. Stay long here and continue to ride this rebound upward.

Q4 download

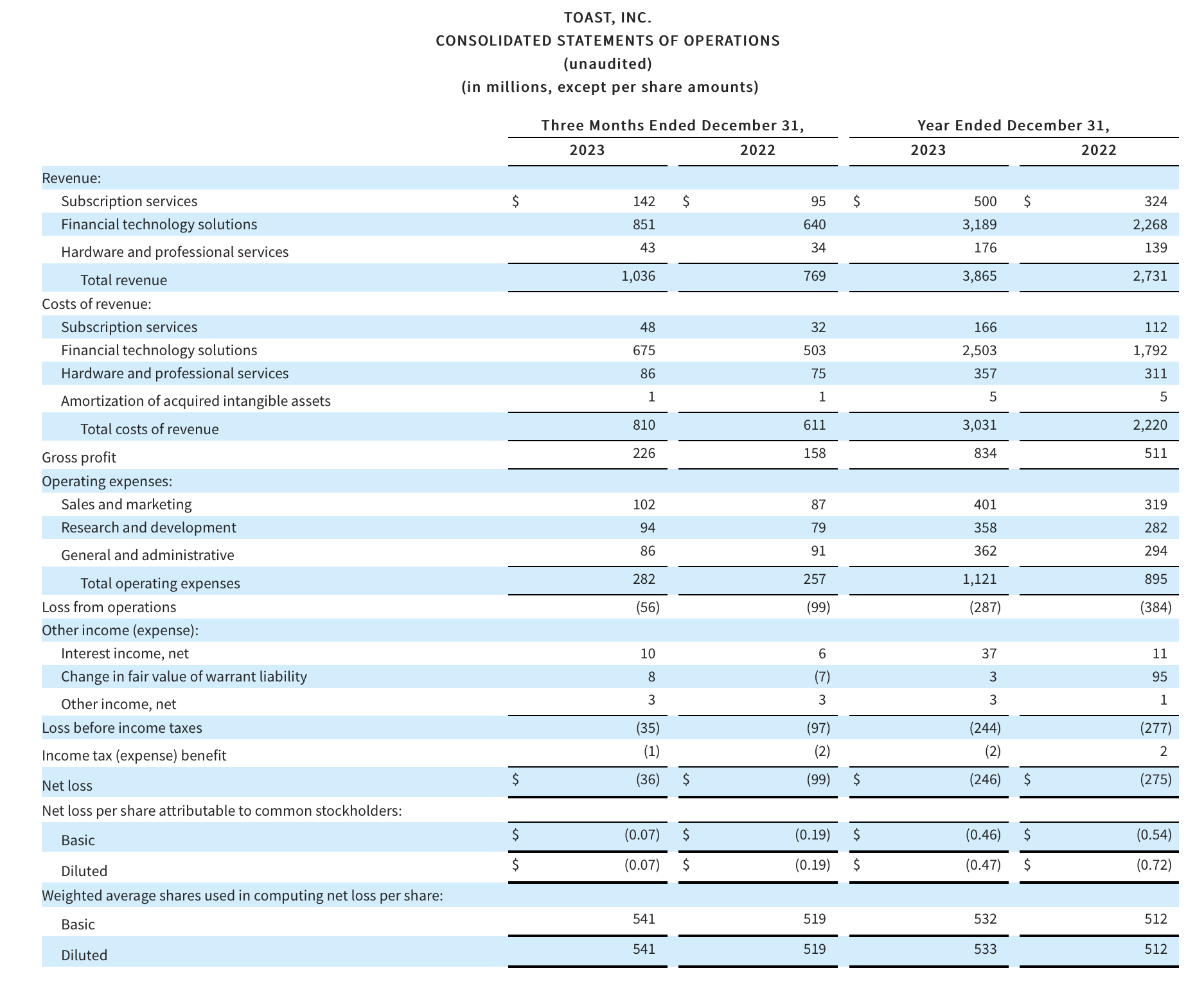

Let’s now go through Toast’s latest quarterly results in greater detail. The Q4 earnings summary is shown below:

Toast Q4 results (Toast Q4 earnings deck)

Toast’s revenue grew 35% y/y to $1.04 billion in the quarter, ahead of Wall Street’s more modest expectations of $1.02 billion (+32% y/y). Note as well that revenue growth largely kept pace with Q3’s 37% y/y growth rate.

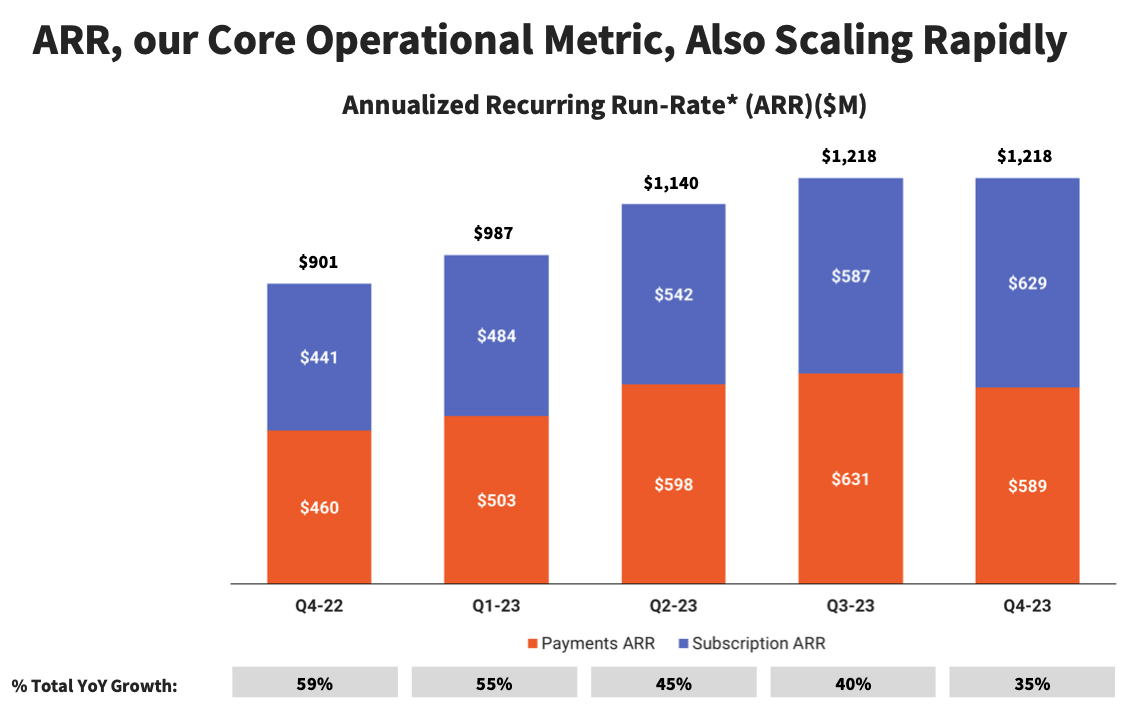

The company, meanwhile, continues to grow ARR on a y/y basis, which is the lifeblood of its recurring revenue model. ARR grew to $1.22 bilious, up 35% y/y. You may notice that ARR is sequentially flat to Q3, but this is normal seasonality for Toast, which saw similar trends play out last year in Q4’22. The company typically starts adding ARR again in Q1.

Toast ARR trends (Toast Q4 earnings deck)

The company continued to grow its install base, adding 6,500 net-new locations in the quarter to end with 106k installed locations, up 34% y/y and marking the first quarter that Toast expanded beyond 100k locations. The company continues to cite substantial go-to-market expertise and execution in the local SMB space. Per CEO Aman Narang’s remarks on the Q4 earnings call:

Our ability to sustain over 30% location growth at this scale is a testament to our competitive differentiation. Our all-in-one platform, our localized go-to-market approach, and the consistent execution by our sales and customer success teams.

The momentum in our SMB segment has allowed us to double the number of flywheel markets over the past year, with 30% of our markets now in flywheel defined by over 20% SMB market share.

Our rep productivity in flywheel markets is over 10% higher than other markets, leading to faster share gains. Even in our most penetrated markets where we have over 30% market share, we are still gaining share at a healthy clip. These markets are a benchmark for how we expect other markets to evolve over time and gives us confidence in sustaining healthy location growth.

The foundation of our success starts with high-value full-serve restaurants, which our go-to-market team is prioritizing. In addition, we’re gaining traction across the broader TAM as we expand our product offerings to serve different restaurant types.

And as our addressable market grows and we see gradual adjustments in our mix across SMB, mid-market, enterprise, and international restaurants. We expect ARPU to continue to increase and GPV permission to remain above industry averages. Our team continues to ensure we maintain a healthy unit economics as we scale locations across these categories.”

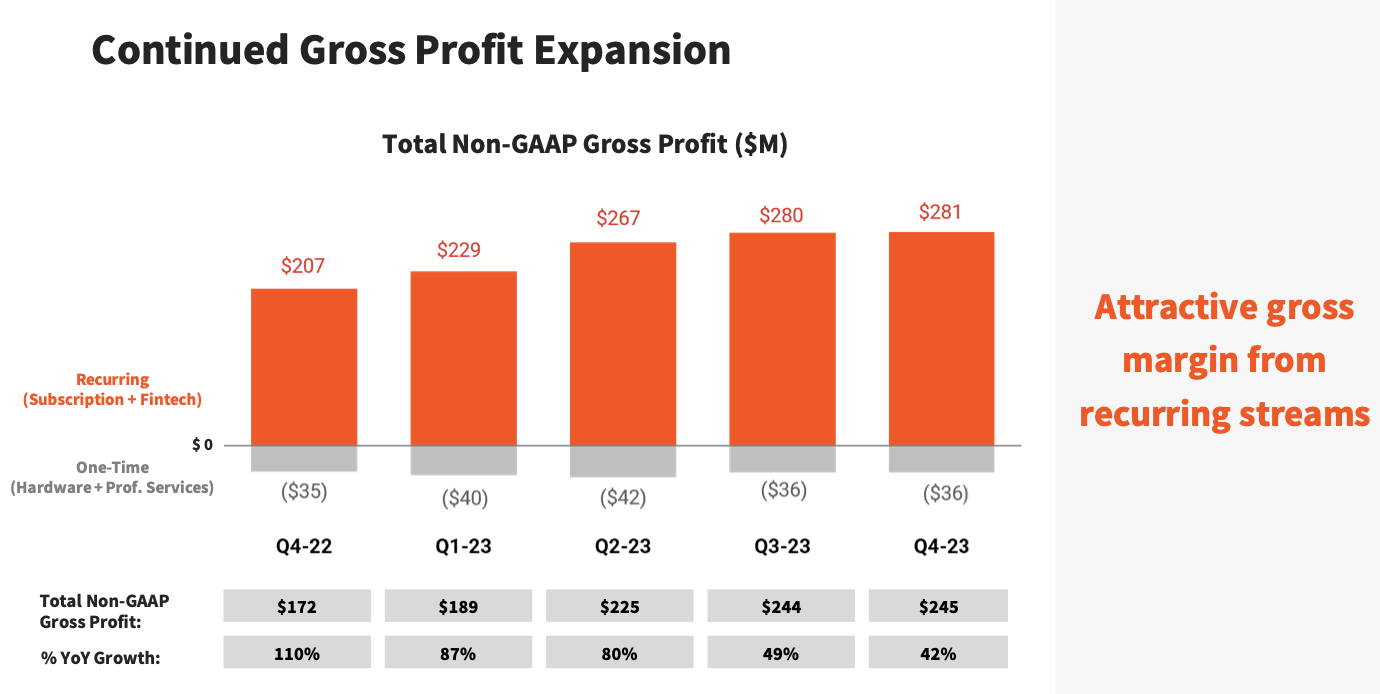

From a profitability perspective, the company continues to expand nicely. Pro forma gross margin dollars grew 42% y/y at a faster clip than revenue, driven by lower shipping costs on hardware units.

Toast margin expansion (Toast Q4 earnings deck)

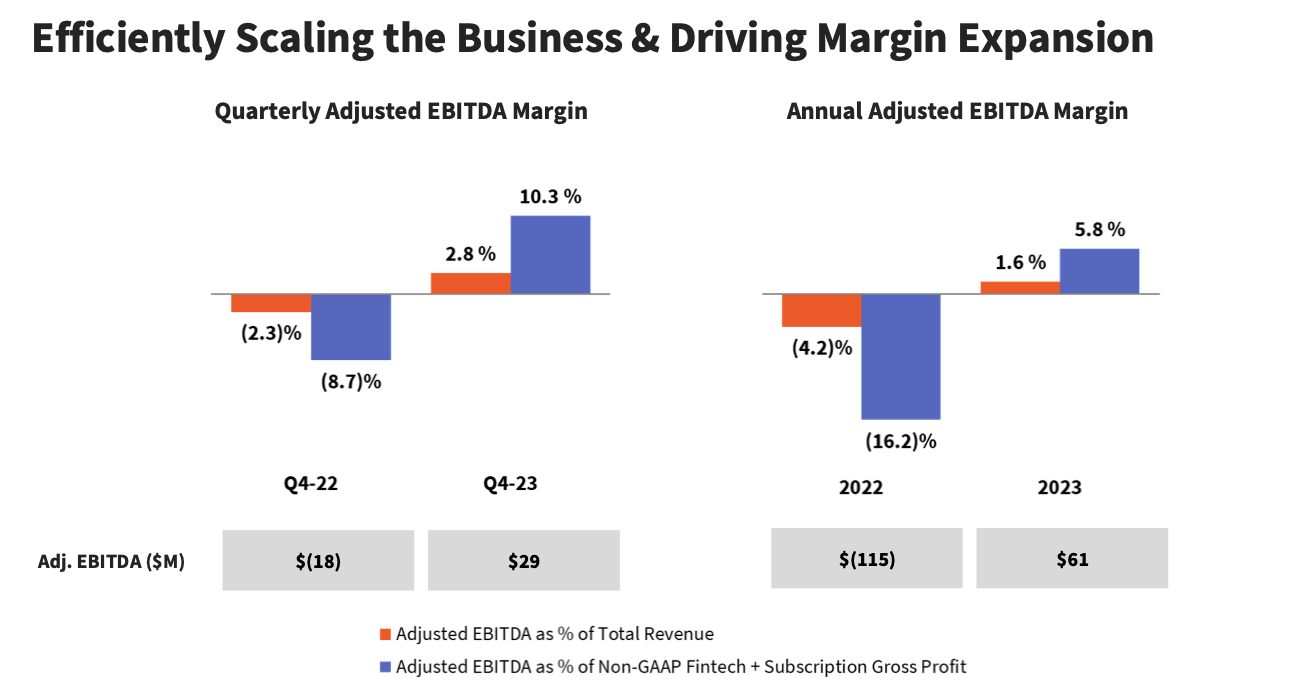

Adjusted EBITDA margins, meanwhile, surged to 10.3% in the quarter, 850bps better than the year-ago quarter.

Toast adjusted EBITDA (Toast Q4 earnings deck)

Note that Toast has guided to full-year adjusted EBITDA of $200-$220 million in FY24, substantially better than just $61 million in FY23. That target reflects opex savings from the company’s recent workforce reduction decisions, but if revenue, ARR, and gross profit dollars continue to grow at a ~30% y/y pace (Q1 guidance calls for gross profit dollars to grow only in the mid-20s), we could see substantial upside ahead.

Key takeaways

In my view, Toast is just starting to show its chops as a profitable, recurring-revenue business. It is building on a foundation of strong go-to-market execution and has plenty of TAM to address. Stay long here and continue to enjoy the recent rebound.

Q2 2024 Earnings Call Transcript")