Ingenious Buddy

The iShares 20+ Year Treasury Bond BuyWrite Strategy ETF (BATS:TLTW) is a relatively new ETF with an inception date back in August, 2022. The investment objective of TLTW is to supply the following benefits for the investors:

- Enhanced income or yield: a higher yielding alternative for investors, who seek to carry an exposure towards traditional U.S. Treasury bonds by selling monthly covered call options.

- Diversification: because of the presence of covered call strategy, TLTW can serve as a diversification element providing a compelling hedge under a scenario of rising interest rates.

-

Easy access: a cost-effective and rather straightforward access to a systematic option strategy on the U.S. Treasury market (i.e., the avoidance of manual trades or expensive brokers).

All of this is offered for investors at relatively cheap price (i.e., 0.35% expense ratio) despite the embedded covered call strategy, which per definition is more complex and more difficult to manage than pure-play equity or fixed income ETFs.

Now, if we look at TLTW’s structure almost the entire AuM amount is allocated into iShares 20+ Year Treasury Bond ETF (NASDAQ:TLT). In other words, TLTW carries a base exposure towards long duration Treasury bonds, which, in turn, implies that TLTW is rather concentrated in the duration factor.

This means that without the presence of the embedded optionality, TLTW would reply to any changes in the interest rates in a more magnified fashion than Treasuries or corporate investment grade bonds with shorter maturities.

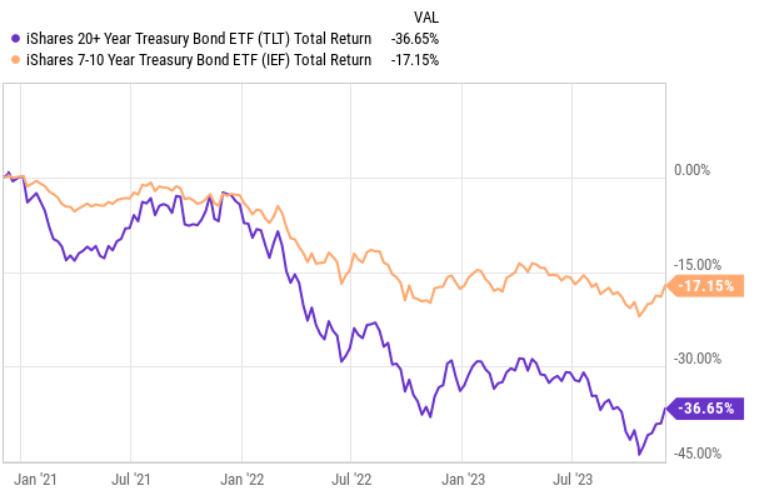

Ycharts

We can clearly capture the essence of a duration factor in the chart above, which illustrates how TLT has responded to the sudden tightening of monetary policy in early 2022 relative to an ETF carrying Treasuries that are bound by shorter maturity dates.

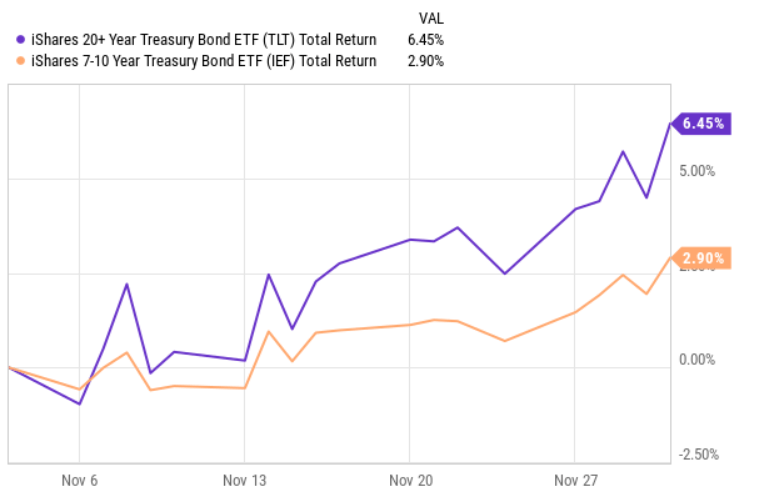

Ycharts

A similar logic or pattern applies, when the market starts to calibrate its expectations on experiencing rate cuts in the foreseeable future. In fact, this is what we have seen in the past couple of weeks. So it is only logical that TLT has bounced back in a more material fashion than most of the other fixed income ETFs with more limited duration factor.

Yet, in TLTW’s case there is a covered call strategy that is incorporated on top of the allocations into TLT. What this means is that TLTW sells call options which expire one month after their issuance and match to the number of TLT shares owned, thereby maximizing the coverage of base exposure to TLT.

By doing so, TLTW effectively ensures the following:

- Ceiling on the maximum monthly price gain or capital appreciation of TLTW that is limited to the strike of the sold call option.

- Additional monthly income on top of the underlying yield of TLT stemming from the pocketed premium of written call options.

- Slightly protected downside due to the collected premium in the case of advance rate increases, more hawkish expectations or credit-risk driven reject in the U.S. Treasuries.

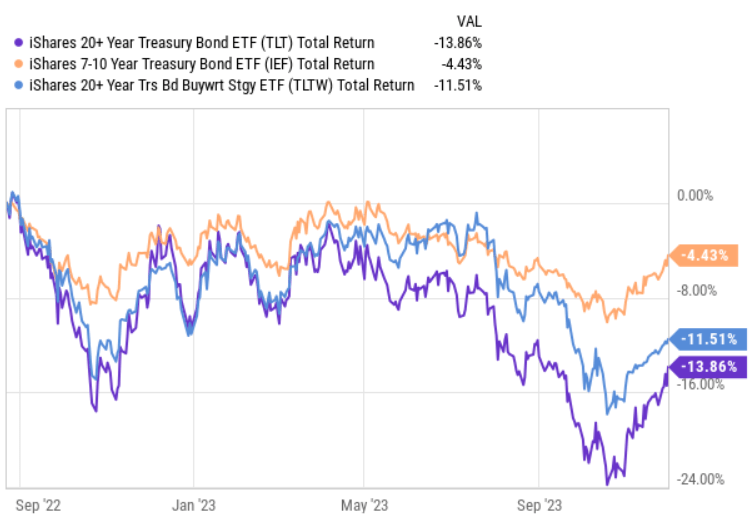

Ycharts

By looking at the chart above, it is quite evident how the aforementioned dynamics have played out for TLTW. Namely, in the period when the fixed income investors got increasingly punished, TLTW managed to outperform TLT, while over the past couple of weeks, when the market’s sentiment has become more dovish, TLTW has recovered in a bit more muted manner than TLT.

Thesis

All in all, TLTW provides an interesting exposure for investors to consider in their portfolios as at least an element of additional diversification. Plus, the notion of accessing optionality at so low costs seems also attractive.

However, in my opinion, this is not the right moment to go heavily long on TLTW; and the reason for this is rather simple.

We have to grasp that the added covered call strategy per definition works well when the market for bonds is trading sideways or if the interest rates are rising and the investors still wish to maintain some portion of their portfolios in fixed income securities.

In the situation of dropping rates, TLTW’s covered call strategy actually imposes a structural headwind for the Fund to attain the benefit of the underlying duration factor (i.e., capitalizing on the reject in interest rates). This is because whenever the TLT position appreciates beyond the strike level at which the calls have been written (plus the pocketed premium amount), all of the gains above that strike and premium money are lost.

With this in mind, the following two charts defend my stance on TLTW.

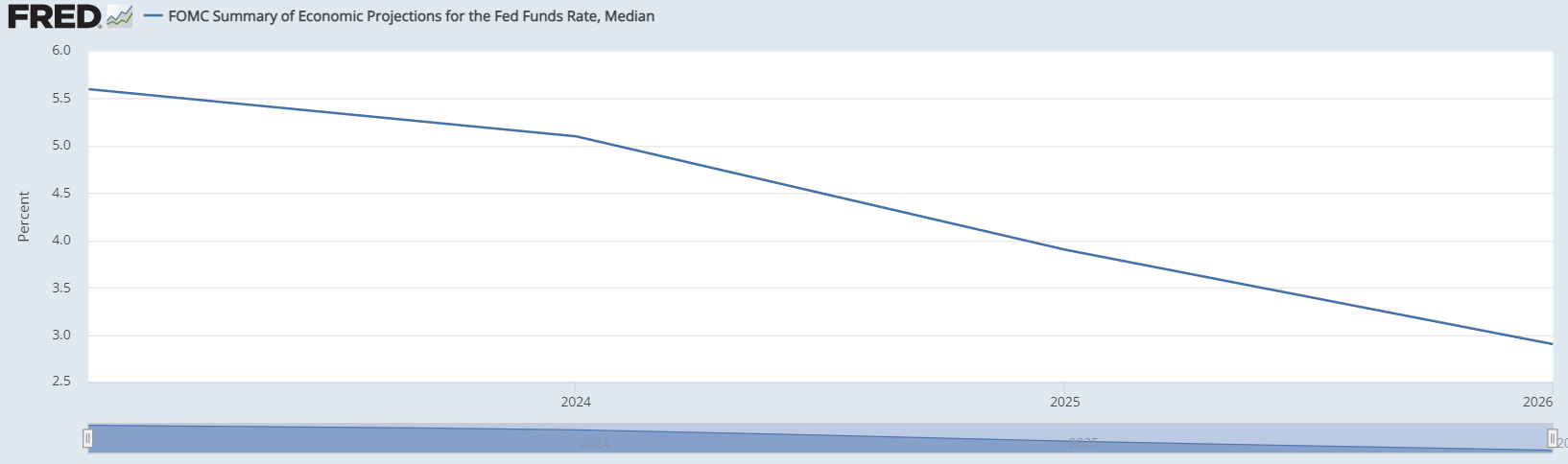

FOMC; St. Louis Fed

The Fed Funds Rate is clearly set to standardize over the foreseeable future. As we encounter lower interest rates, TLT would be inherently forced to advance higher. Here investors would be in a relatively worse situation by owning TLTW than TLT as the cap from covered calls would limit a full realization of the capital gains component.

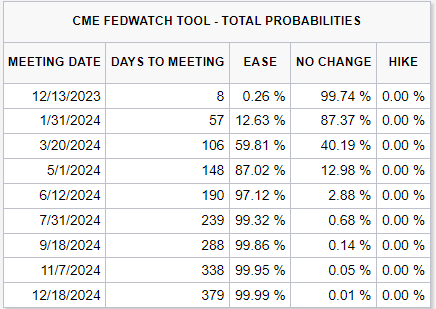

CME Group Inc

Finally, as we can see in the table above, the market seems to price in rather considerable probabilities of having lower interest rates some point in 2024.

The bottom line

In my humble opinion, considering the prevailing interest rate backdrop and the likely trajectory how the interest rates could evolve in 2024, there is no real motivation or basis of owning TLTW. By adding TLTW to portfolio, the likelihood is high that investors will underperform TLT or other long duration fixed income securities due to the inherent limit of the potential capital gains that could come from interest rate cuts.

It is also true that basing investment decision on how the market currently sees interest rates moving in the near future is a risky idea. However, in the context of my opinion on TLTW it does not really matter whether the rates go down early 2024 or late 2024 as the only thing that matters is that the overall trajectory of future interest rates seems to assume a structural downward trend that will inevitably limit the return potential.

Q2 2024 Earnings Call Transcript")