SOPA Images/LightRocket via Getty Images![]()

Investment action

Based on my current outlook and analysis of Thomson Reuters (NYSE:TRI) (TSX:TRI:CA), I recommend a buy rating. I expect TRI to grow EPS to low teens in FY25/26 post-the FY24 investment year and, coupled with a low single-digit dividend yield, bridges to a total return of 24% over the next 2 years. TRI has shown that it is able to drive acceleration in organic growth, and with the upcoming launches of AI-related products, I am optimistic about TRI sustaining growth at high single-digits, which should also drive operating leverage.

Basic Information

TRI is a leading information and solutions provider with five primary segments, split between the Big 3 (Legal Professionals, Tax Professionals, and Corporates), Global Print, and Reuters News. The Big 3 is the biggest revenue driver for TRI, contributing 80% of FY23 revenue. At a high level, TRI offers mission-critical databases, tools, and analytics to professionals (like lawyers, tax professionals, and the government). Please refer to the TRI website for more detailed information, as the technicalities are too long to list here. As of FY23, TRI generated a total revenue of $6.8 billion, EBITDA of $3 billion, and net income of $2.5 billion. TRI also has a strong balance sheet that exited 4Q23 with $3.28 billion in gross debt and $1.3 billion in cash.

Review

TRI grew its 4Q23 reported revenue by 2.8% to $1.815 billion, 50bps below the consensus of 3.3%, primarily due to the impact of divestitures. Adjusting for like-for-like comparison, organic revenue grew 7% y/y, mainly driven by the Big 3, which saw organic revenue growth of 8%. Breaking the growth split in the Big 3, legal revenue grew 7% organically, tax and accounting grew 10% organically, and corporate revenue grew 7% organically. EBITDA margins also expanded 300 basis points to 38.9%, way ahead of consensus expectations of 37.5%. As a result, TRI reported a strong beat in EPS, coming in at $0.98 vs. the consensus of $0.91.

Once again, TRI showed that its business is resilient against the macro environment, a factor that I believe many investors are appreciative of. In 4Q23, TRI managed to accelerate its organic revenue by 100bps to 7%, effectively putting an end to any doubts that organic growth is impacted (organic growth remained below 7% for the past five quarters since 3Q22) and also painting a very positive outlook for 1Q24 if momentum persists. Notably, the organic growth recovery was in part driven by the strong bounce back in Reuters News organic revenue growth, from 3% in 3Q23 to 9% in 4Q23. This has huge implications for organic growth expectations moving forward, as the segment’s average organic growth rate was in the low single digits previously. I believe the step-up in organic growth is structural, as it was driven by generative AI-related content licensing transactional revenue, which I expect to continue to be in demand as more businesses use AI to improve productivity.

On the point of generative AI, my take is that it will structurally improve the growth outlook for TRI as it continues to push forward with its investments, leveraging the capabilities of TR Labs. The results from these investments are bearing fruits, which I expect to show up in the financial statements soon (I take the high customer interest as an indicator of demand). The most recent product release is the Westlaw Precision AI-Assisted Research, which was introduced in late 2023. Looking ahead, TRI anticipates releasing additional generative AI products across segments in 2H24, as well as the Practical Law Course Finder, which is powered by generative AI, in early 2024. Going forward, I anticipate that more AI-related products will continue to support high-single-digit organic growth, especially since management has reiterated their goal of spending over $100 million/year on generated AI. Management’s forward-looking guidance is reflective of this AI tailwind and the strong organic growth potential. Specifically, they are guiding for FY24 organic growth of 6%, followed by an acceleration to 7.25% at the midpoint (6.5% to 8%) in FY25/26.

Customer interest in our AI-driven offerings and product roadmap remains extremely strong with several additional launches coming in the next few months. Corporates organic revenue growth was 7% in line with the growth last quarter.

The emergence of GPT-4 and advanced Generative AI technologies ushered in significant change for our product organization, which had to reprioritize on the fly, reimagine customer experiences, and then quickly deliver TR quality product innovations. 4Q23 call

Moving down the P&L, while management guided for margin to contract in FY24, it should not impact the stock narrative too much since management guided for EBITDA margins to expand by 75 bps in FY25 and more than 50 bps in FY26, indicating FY24 margin compression is simply a matter of reinvestment. More importantly, this margin guidance indicates that TRI continues to experience operating leverage.

A key part of the TRI equity story is its capital return policy. Over the past few years, TRI has consistently bought back shares, reducing share outstanding from ~500 million in FY19 to ~455 million in 4Q23, a roughly 10% decrease over 4 years, translating to ~2.5%/year. As of the end of January, TRI has repurchased $457 million worth of shares, and management has announced plans to complete its $1 billion repurchase plan in 2Q24. This translates to around 0.7% of buybacks. With $1.3 billion in cash, potential monetization of its stake in London Stock Exchange Group, and flexibility to flex the balance sheet by taking more leverage, I am confident that TRI can continue to buy back shares.

In 2023, we sold 56 million shares for nearly $5.5 billion of gross proceeds. Of the remaining 16 million shares we own, 2.6 million could be sold through exercise of the call options we sold in September, and we have 6.1 million additional shares that are eligible for sale in 2024. Our tax basis on the remaining 16 million shares is approximately $650 million. For your math, we would assume a 25% capital gains tax rate on gains above $650 million. Lastly, the value of foreign exchange hedges held against our LSEG stake were $26 million as of December 31. We currently have approximately 86% of our remaining LSEG position hedge. 4Q23 call

Valuation

Author’s work

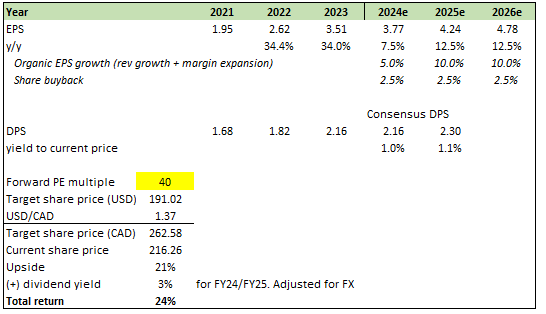

My model indicates a potential upside of 24% over the next 2 years, driven by 7.5% EPS growth in FY24 and 12.5% EPS growth for both FY25 and FY26, and a dividend yield of ~3%. Underlying my EPS growth assumption is organic growth of 5% in FY24 (6% organic revenue but modestly offset by margin contraction due to reinvestments) and 10% organic growth in FY25/26 as TRI grows at the top end of its guided range (8% topline) coupled with margin expansion. For my forecasted period, I expect TRI to continue buying back shares at its historical rate. I used consensus DPS for my model. One assumption that I differ greatly from the market is that I am assuming PE to see mean reversion, as the stock valuation tends to revert back to mean whenever it approaches the top end of the range (44x PE).

Risk and final thoughts

TRI is trading at a very high valuation on an absolute basis, which means there is plenty of room for valuation to re-rate downwards if organic growth were to disappoint and, for whatever reason, see major deterioration to low single-digits. In conclusion, I recommend a buy rating for TRI based on its impressive 4Q23 results, showcasing organic growth, strong margins, and share buybacks. The company’s resilience in a challenging macro environment and accelerated organic revenue growth, driven by generative AI-related products, position TRI for sustained high-single-digit growth. Despite FY24 margin contraction due to reinvestment, the expectation is the margin will expand in the following years, indicating operating leverage.

Q2 2024 Earnings Call Transcript")