Savers often stack up a lot of pension pots during their working lives

Nearly three quarters of people who recently moved a pension did not check the fees charged by either their old or new schemes first, research reveals.

That is despite the staggering difference even a small percentage increase in charges can make.

A rise from 0.4 per cent to 0.75 per cent could take a £70,000-plus chunk out of a potential £870,000 pot – see below.

Savers often stack up a lot of retirement pots during their working lives.

It is sometimes, but not always, beneficial to merge them with your current workplace provider or move them to a private pension provider.

Fees are one of the top items to check before deciding, but many savers are unaware of how much they are paying or how small differences in costs can have an outsize impact on their eventual pot, according to People’s Partnership.

The pension provider, which surveyed 1,000 people who had moved an invested retirement pot without the help of a financial adviser over the past two years, found 11 per cent were unaware their pension had any charges.

Some 72 per cent who did this were unaware what the fees were on their previous or current pensions.

> What to check before moving a pension? Read our guide and find tips below

The People’s Partnership’s analysis shows you could end up with a pot tens of thousands of pounds smaller if you don’t pay attention to charges.

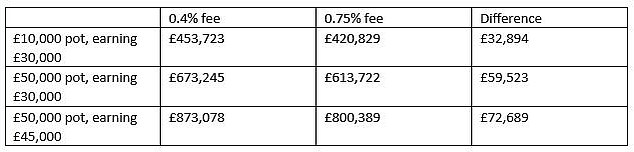

For example, a 30 year old earning £30,000 who moved a £10,000 pension pot from a provider charging 0.4 per cent to one charging 0.75 per cent could see £32,900 wiped off a potential £453,700 pot when they retired at 67.

They would be down £59,500 if they moved a £50,000 pot under the same circumstances. If they earned £45,000 and moved a £50,000 pension, the impact of charges would be £72,700.

This assumes total contributions are 8 per cent of salary, wage inflation is 3.5 per cent, investment returns are 5 per cent and inflation is 2.5 per cent.

PP also found that 50 per cent of those surveyed did not think it was easy to track down the fees they were being charged on their pensions.

It recommends searching your provider’s website first and if the information is not readily available ringing up to ask what you are being charged.

But PP adds that the pension industry needs to be more transparent and should help savers understand key information when transferring pots to prevent them making detrimental financial decisions.

Chief executive officer Patrick Heath-Lay says: ‘While there are many factors that can make a pension attractive, the two fundamental aspects are investment returns and charges.

‘Unfortunately, very few people know exactly what they are being charged for their pensions and they are being let down by an industry that doesn’t make this information easy to find or understand.

‘If people can’t make an informed decision about the value they are being offered by different providers, they risk losing thousands of pounds from their retirement pots.

‘Our research shows the real-world impact of small differences in percentages are incredibly hard to grasp.’

Why do savers decide to move pensions?

Source: People’s Partnership survey of 1,000 people who moved a pension in the past two years

Are YOU considering moving a pension?

The People’s Partnership offers the following tips.

– If you are thinking of consolidating your pension because you are changing jobs or want your pensions in one place, ask yourself what is most important to you when you retire and find a provider that will help you to meet your long-term goals.

– Lots of providers will enable you to consolidate your pensions, but there are big differences in the fees they charge and, in some cases, the investment returns they generate, which will impact how much you have saved at retirement age.

– There are three core areas of value when considering a pension provider: What is their most recent track record on investments? What sort of organisation are they in terms of the help they offer and how contactable they are? What they will charge you?

Six maths lessons everyone can learn to get richer

Money expert Becky O’Connor of PensionBee reveals the most useful – and profitable – real world sums.

Compound growth, which generates massive gains the longer you save and invest, is lesson number one… so what are the others?

<!- – ad: https://mads.dailymail.co.uk/v8/ua/money/moneypensions/article/other/mpu_factbox.html?id=mpu_factbox_1 – ->

– Charges are generally expressed as a percentage. Don’t think that the difference between seemingly small numbers is insignificant because the fact is you could have to work longer to get the value you are looking for to support you in retirement.

– There can be significant variation in fees between providers. You might also want to ask are there any penalties you may have to pay should you decide to move on in the future. There are other areas you can look at, any special conditions you could give up, such as what age you can access you savings with your new provider.

– Don’t fall for the first advert you see. Most people either talk to their existing provider about consolidating or respond to the first advert they see but it pays to do your homework.

– Ask your current pension providers, and any that you are considering switching to, to send you simple, easy-to-understand information about the fees they charge, with examples to bring this to life.

– There is independent help at MoneyHelper [a free, government backed money service].

What should you consider before moving your pensions? A 10-point checklist

Merging pensions is not always advisable because you can risk losing valuable benefits. Here’s what to check before making a decision.

1. Fees on old and new pension schemes

As explained above, you should check charges as they can make a serious dent in your future returns.

2. Where are your pensions invested

Past returns are not a guide to the future, but you should investigate where your money will be held. Read our guide to carrying out a healthcheck on investments.

3. A private provider versus your work scheme

Pension consolidation firms have sprung up to help people manage all or most of their pensions in one place, and this can be cheaper as well as more convenient.

However, your current workplace scheme might have negotiated lower fees and rolling up your older pensions there might be even handier if you want to cut down on admin.

STEVE WEBB ANSWERS YOUR PENSION QUESTIONS

4. Guaranteed annuity rates

If these are high it can be worth sticking with an old pension and using it to buy an annuity.

You have to get paid financial advice to move a pension worth £30,000 plus with a GAR attached.

5. Guaranteed fund returns

These are rare but it is worth checking the small print to see if you benefit.

6. Bigger lump sums

Some older company pensions allow you to take a tax-free lump sum of more than the typical 25 per cent.

7. Large exit penalties

Most default work pension funds are trackers with cheap charges these days. If you have a costly old pension with restrictive investment choices you could weigh the benefits of moving despite penalty fees.

Exit fees are capped at 1 per cent after you reach the age of 55.

8. Ongoing employer contributions

You will be getting free employer contributions into your current work scheme, and you don’t want to lose that cash coming into your pot.

9. Protected pension ages

It depends on the scheme rules so check them, but you might not want to lose the opportunity to access a pension at 50, especially if you have several others which will kick in later.

10. Final salary pensions

Outside the public sector, generous final salary pensions paying a guaranteed income until you die, plus valuable death benefits to surviving spouses, have virtually been wiped out.

They are the most generous and safest pensions available. You are required to get paid-for financial advice if your transfer value is £30,000-plus, which is a longstanding safeguard against making mistakes you can’t take back later.

> Should you combine your pension pots? Read our full guide

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

Q2 2024 Earnings Call Transcript")