As you may have learned recently, the “Magnificent Seven” is a group of powerhouse stocks including Nvidia, Apple, and Microsoft, most of which have benefited significantly from the enthusiasm surrounding their artificial intelligence (AI) efforts. But which would be the equivalent businesses if the same concept were applied to the healthcare sector rather than the technology sector?

As it turns out, there are only four stocks that have the right combination of ongoing growth and market-outperforming returns. All four of these magnificent healthcare companies have solid business models, upwardly trending share prices, and, unfortunately, somewhat frothy valuations.

But they also have very long growth runways and a history of good execution, so there’s a solid chance that their price tags will be justified by continued strong performance. Let’s meet the players.

Eli Lilly and Novo Nordisk

Eli Lilly (LLY -0.52%) and Novo Nordisk (NVO -1.46%) are two big pharma stocks that don’t need much introduction thanks to the increasingly absurd popularity of their smash-hit medicines for obesity and type 2 diabetes.

Eli Lilly makes the drug Mounjaro for diabetes as well as Zepbound, which is the same therapy but formulated for weight loss. It’s the largest healthcare company by market capitalization with a size of $729 billion.

Novo Nordisk is the second-largest healthcare competitor by market cap, clocking in at $549 billion. It’s responsible for the type 2 diabetes medicine Ozempic, as well as the obesity-oriented version of the same drug, Wegovy.

Both companies plan to continue the process of penetrating those same metabolic-disease markets, in addition to others, over the rest of the decade and beyond. Their pipelines are packed with mid-stage and late-stage programs that could become the perfect tools in a smattering of different medical niches, or which could expand the indications and addressable market of their already-approved medicines.

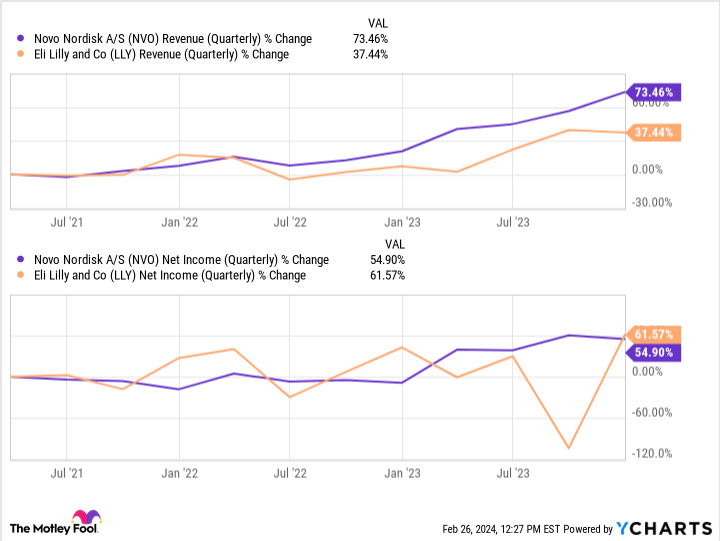

And neither company anticipates much of a problem with competition over market share, given that the markets they’re interested in are tremendously deep and expected to keep growing. Not convinced that their trajectories are in line with magnificence? Consider this chart below. As you can see, they’re ramping up sharply, and they’re worth buying if you don’t mind their valuations.

NVO Revenue (Quarterly) data by YCharts.

Vertex Pharmaceuticals

Vertex Pharmaceuticals (VRTX -1.46%) is a drug developer focusing on rare diseases like cystic fibrosis (CF). Recently, it commercialized a new gene therapy called Casgevy for both sickle cell disease (SCD) and beta thalassemia with the help of CRISPR Therapeutics. Its market cap is $111 billion. And in fittingly magnificent fashion, its shares are up by an impressive 45% in the last 12 months.

One of the key things that drives Vertex’s stock to greater and greater heights is that its cystic fibrosis medications, of which it’s always producing and testing more, are deeply entrenched in the market. In fact, of the 92,000 known patients with CF in the Western world, Vertex is currently treating all but 20,000 of those who are eligible.

On top of that, there’s no direct competitor for its gargantuan market share. And patients need to take its medicines for life to control their symptoms.

With a safe base of revenue from sales of its CF drugs, the company has leeway to invest in research and development (R&D) targeted at larger and more competitive markets, like for acute pain therapies. That means it can afford to take a lot of ambitious shots on goal without overextending. And that’s a big part of the reason its trailing-12-month net income rose by 68% over the last five years, reaching $3.6 billion. As more of its programs get approved for sale, that figure will only increase, as will its share price.

Intuitive Surgical

Last but not least is the robotic surgery company Intuitive Surgical (ISRG -0.26%), which boasts a market cap of $136.9 billion and a top line of $7.1 billion in 2023.

In its line of business, customers in hospitals first purchase its da Vinci brand robotic surgical units. Then they pay Intuitive for maintenance contracts, spare parts, new surgical toolheads, and training programs for surgeons, generating a long tail of recurring revenue over the years.

The more procedures customers perform with their da Vinci units, the more recurring revenue it rakes in, and the more the device becomes established as a workhorse in bariatric, urologic, and general surgery operating rooms.

And the competition is, for now, nowhere to be seen. So it’s no surprise that Intuitive’s profit margin, at 25%, is as wide as it is. Considering that the demand for surgery is not going to decline anytime soon, the surprising part is that the company isn’t already included in the existing set of Magnificent Seven stocks.

Alex Carchidi has positions in Apple and Microsoft. The Motley Fool has positions in and recommends Apple, CRISPR Therapeutics, Intuitive Surgical, Microsoft, Nvidia, and Vertex Pharmaceuticals. The Motley Fool recommends Novo Nordisk and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")