I’d bet my last dollar that millions of retirees would gladly advocate for how beneficial Social Security has been for them. For decades, Social Security has provided a financial safety net for people in their golden years and has been one of the U.S.’s most vital social programs.

There’s a lot to be grateful for with Social Security, but you’ll still find many people who’d tell you they wish it were more straightforward. Social Security has many moving parts, and trying to keep up with it all can be a headache. Instead, you should focus on the more important details and let the rest take care of itself.

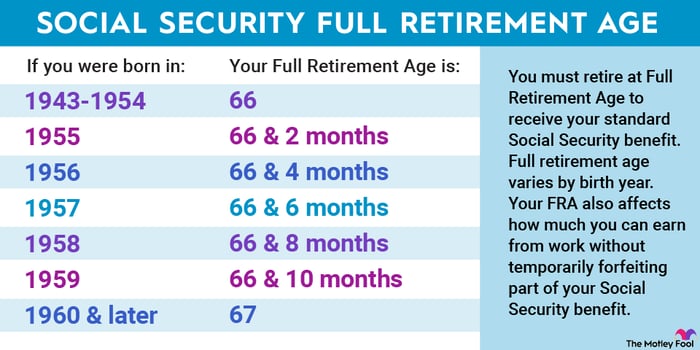

One of those details is your full retirement age, which is one of the most important numbers to know in Social Security.

Image source: Getty Images.

Your Social Security benefit starts with your full retirement age

Your full retirement age (FRA) is when you’re eligible to receive your primary insurance amount (PIA). Your PIA is your base monthly benefit, and it’s what Social Security uses to calculate your benefit if you decide to claim before or after your FRA.

Your FRA is based on your birth year:

Image source: Getty Images.

Claiming benefits early reduces them based on how far away you are from your FRA. If you’re within 36 months of your FRA, Social Security reduces benefits by five-ninths of 1% monthly. Any month more than 36 further reduces benefits by five-twelfths of 1%.

If your FRA is 67 and you claim benefits at 62, they’re reduced by 30%; if you claim benefits at 64, they’re reduced by 20%.

Claiming benefits after your FRA increases them by two-thirds of 1% each month, or 8% annually. If your FRA is 67 and you delay benefits until 70 (the age monthly increases stop), they’ll be increased by 24%.

Your full retirement age affects rules about working while receiving benefits

Aside from how your benefits are affected by when you claim relative to your FRA, other aspects of Social Security revolve around it, including rules surrounding working while receiving benefits.

Claiming benefits doesn’t mean you must stop working or earning money; plenty of people do both. However, it does mean you may have to monitor how much you make if you claim benefits before your FRA. Social Security uses a retirement earnings test (RET) for people who claim benefits early and continue to earn money.

In 2024, the earnings threshold for someone who won’t reach their FRA this year is $22,320. Social Security will reduce your annual benefit by $1 for every $2 you earn over that limit. The limit is $59,520 if you’ll hit your FRA in 2024, and earning over that will reduce benefits by $1 for every $3 earned.

If you’re at or past your FRA, you can work and earn as much as you please without worrying about having your benefits reduced.

Use your full retirement age to help you decide when to claim benefits

One of the more important retirement decisions people make is when to claim Social Security benefits. It’s also a decision that revolves around your FRA.

First, you should determine what financial role Social Security will play in your retirement. From there, you should consider reductions or increases to see when claiming benefits makes sense for you.

If you’re financially strained, maybe waiting until your FRA or after it isn’t an option. If you can survive off other retirement income sources like a 401(k) or IRA, maybe you can afford to delay Social Security past your FRA to get an increased monthly benefit.

Whatever the case, use your FRA and PIA to help guide your decision.

Q2 2024 Earnings Call Transcript")