Cindy Ord

Back in March, I placed a “Buy” rating on The TJX Companies (NYSE:TJX) saying that while it was not cheap, the company was in an ideal environment and that it should be a nice beneficiary of industry de-stocking issues. In September, meanwhile, I raised my price target from $100 to $120, noting the company was firing on all cylinders. The stock is up about 25% since my initial write-up. Let’s catch up on the name.

Company Profile

As a refresher, TJX is an off-price retailer in both the apparel and home furnishing spaces. In the former, it operates the T.J. Maxx, Marshalls, and Sierra concepts in the U.S. and Winners and T.K. Maxx internationally. In the home furnishing space, it owns HomeGoods and HomeSense.

It refers to its largest segment as Marmaxx, which consists of its T.J. Maxx and Marshalls brands. Its HomeGoods segment, meanwhile, consists of its HomeGoods and HomeSense brands.

Q3 Results

For its fiscal Q3 reported last month, TJX saw revenue climb 9% to $13.27 billion. That surpassed the analyst consensus of $13.04 billion. Overall comparable store sales rose 6%.

The Marmaxx segment was once again strong, with sales up 9% to $8.1 billion in the U.S. Same-store sales climbed 7%. The segment’s profit margin was 14%, up 50 basis points, helped by lower freight costs. The same-store gains were once again driven by increased traffic and showed strength across regions and customer income levels.

HomeGoods, meanwhile, continued its recovery, with revenue rising 13% to $2.21 billion. The segment’s comparable-store sales jumped 9%. Segment profit margin was 10.3%, up 140 basis points, helped by lower freight costs and expense leverage. Comps were strong across geographies and demographics.

TJX International sales, meanwhile, grew 10%, or 3% in constant currencies, to $1.63 billion, on a 1% increase in same-store sales. TJX Canada saw revenue rise 2%, or 5% on a constant currency basis, to $1.32 billion, as comparable store sales rose 3%.

Overall gross margins came in at 31.1%, up 200 basis points.

EPS of $1.03, meanwhile, beat analyst expectations by 4 cents. The company had a -3 cent charge from closing its HomeGoods online business in the quarter, as well as a 3 benefit from the timing of certain expenses.

Inventory at quarter end was $8.8 billion, flat versus a year ago. On a per store basis, inventories were also flattish.

The company ended the quarter with 4,934 stores compared to 4,793 a year ago.

Looking ahead, TJX guided for fiscal Q4 EPS to be between $1.07 to $1.10, which was below the $1.13 consensus at the time. This guidance includes a 10-cent benefit from Q4 having an extra week but excludes a -3 cent reversal on the timing of expenses it saw in Q3. It is looking for same-store sales to increase between 3-4%. It expects Q4 gross margins to improve 210-230 basis points to between 28.2-28.4%, helped by lower freight costs.

For the full year, the company is projecting EPS to be between $3.71-3.74, up from a prior outlook of $3.66-$3.72. That compared to a consensus of $3.73 at the time. This does not include the 3-charge for closing its e-commerce business. It is looking for comparable sales to rise between 4-5%, up from a previous forecast of 3-4%.

On its Q3 earnings call, CEO Ernie Herrman said:

“I’d like to highlight the key opportunities we see to keep driving sales and traffic in the fourth quarter. First, as always, offering outstanding value is our top priority for the holiday selling season, especially in an environment, where consumers’ wallets are stretched. The marketplace continues to be loaded with quality merchandise and we are set up extremely well to offer a wide range of good, better and best brands to consumers. Second, we believe we are strongly positioned to be a top destination for gifts this holiday season. Our buyers have done a terrific job selecting the best merchandise available from our global vendor base to surprise and excite our customers. We are confident that shoppers will find an eclectic assortment of gifts to choose from for everyone on their list. In addition, we will remain focused on being a gifting destination throughout the year. Next, we will be following fresh product to our stores and online multiple times a week throughout the holiday season, which we believe differentiates us from many other major retailers. With our ever-changing mix of merchandise, shoppers can see something new every time they visit. Further, we feel great about our plans to transition our stores post-holiday and offer consumers the categories and trends they want to start the year. Lastly, we feel great about our holiday marketing campaigns across all of our brands, which launched earlier this month.”

TJX turned in another strong quarter as it continues to benefit from a strong merchandise position following earlier de-stocking issues in the apparel industry and a shopper preference for value given increased prices due to inflation and an uncertain macro. Meanwhile, it has seen a nice recovery in its home furnishings business as well, despite the struggles with full-priced sellers in the industry. Lower freight costs are also leading to some solid gross margin gains.

There likely was some confusion with TJX’s guidance, as the company gave an adjusted number for Q4 that only took out the extra week, which isn’t generally how that would be calculated. Meanwhile, it left in charges for the full year for the closure of its HomesGood online store. It also didn’t adjust for the timing of the expense shift, which benefited Q3 but will negatively impact Q4. Overall, the TJX story remains on track and I think the company was being conservative ahead of the holiday season.

Valuation

TJX stock currently trades at 15.4x the FY 2024 (ending January) consensus EBITDA of $7.2 billion. Based on FY26 analyst estimates of $7.8 billion, it trades at 14.3x.

On an EBITDAR basis, it trades at 12x FY25 estimates and about 11.3x FY26 estimates.

It trades at a forward PE of 21.5x the FY25 consensus of $4.12 and 19.8x the FY26 consensus of $4.58.

The company is projected to grow revenue by 4.6% in FY25 to $56.45 billion.

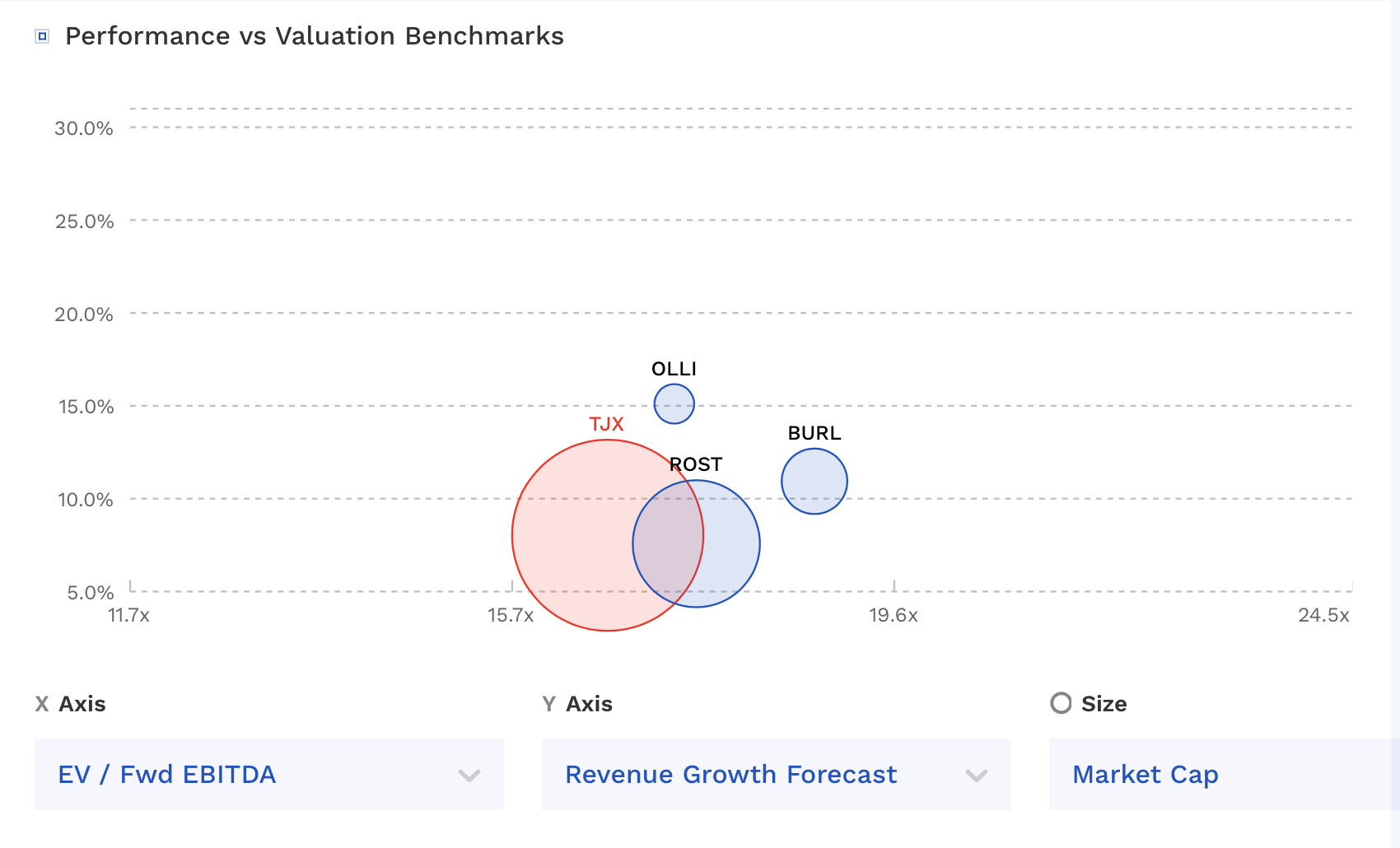

TJX trades at a discount to competitors Burlington Stores (BURL) and Ross Stores (ROST).

TJX Valuation Vs Peers (FinBox)

Given the momentum in the business and where its peers trade, I’d place a fair value for TJX of between 13-15x EBITDAR, which is a stock price of between $105-122.

Conclusion

TJX remains a solid growth story in retail, as it benefits from both increased store traffic, improving gross margins, and store expansion. It’s operating in a great environment for off-price retailers, which should continue into 2024 given a consumer that wants to spend, but who also is being more value-conscious.

While the stock isn’t cheap, I still think it should have some momentum left. That said, given its valuation, there is a risk that if growth starts to slow, the stock could re-rate lower. At this time I continue to rate it a “Buy” with a $120 target, but I’d continue to watch that same-store growth remains on track.

Q2 2024 Earnings Call Transcript")