NosUA/iStock via Getty Images

Introduction

The Procter & Gamble Company (NYSE:PG) provides branded consumer packaged goods worldwide. It operates through five segments: Beauty; Grooming; Health Care; Fabric & Home Care; and Baby, Feminine & Family Care.

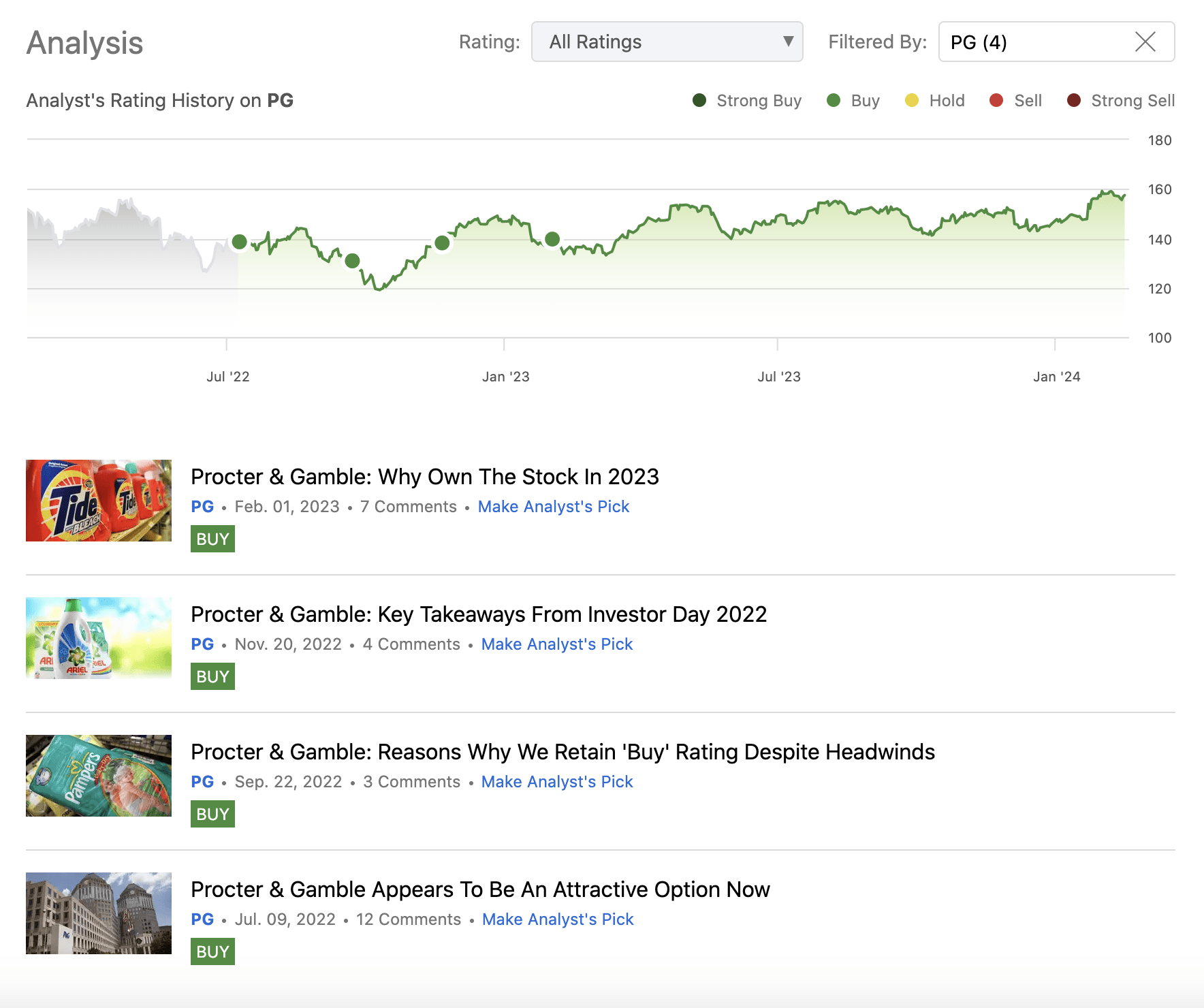

We have started covering PG in July 2022 and have written four articles on the company since then. During our entire coverage period, we have been bullish on the firm. The following screenshot shows our analysis history.

Analysis history (Author)

Slightly more than one year has passed since our last writing, so we thought it is really time to give an update and assess whether our previously established arguments for owning the stock are still valid or not.

A short recap, why we liked and why we have been bullish on the company previously:

- Attractive profitability and return on equity metrics.

- Attractive and sustainable dividend.

- Relative immunity to the negative impacts of the poor consumer confidence.

In today’s article, we will be focusing on how the profitability of the firm has changed over the past year, also including the metrics from the latest quarterly earnings report. We will also take a look at the valuation, at the liquidity ratios and last, but not least on the dividends and share buybacks.

Profitability

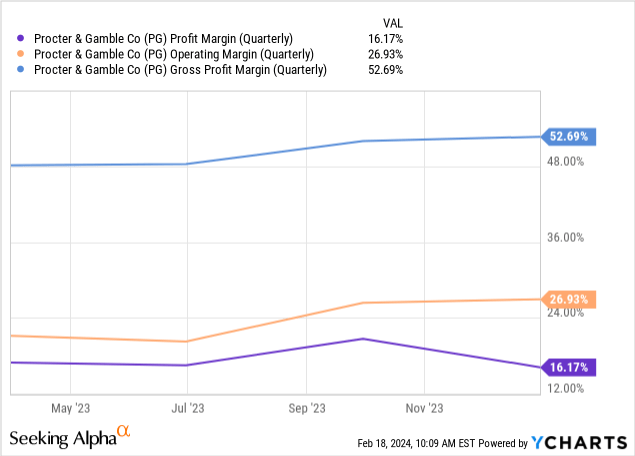

There are three profitability metrics that are often used to evaluate and compare the company’s performance with others. These are namely: gross profit margin, operating margin and net profit margin.

The following chart shows how these margins have developed over the twelve months on a quarterly basis.

Both the gross- and the operating margin have been expanding gradually over the past year, reaching eventually 53% and 27%,respectively. At the same time, the net profit margin has been somewhat volatile, but downwards trending in the past quarter.

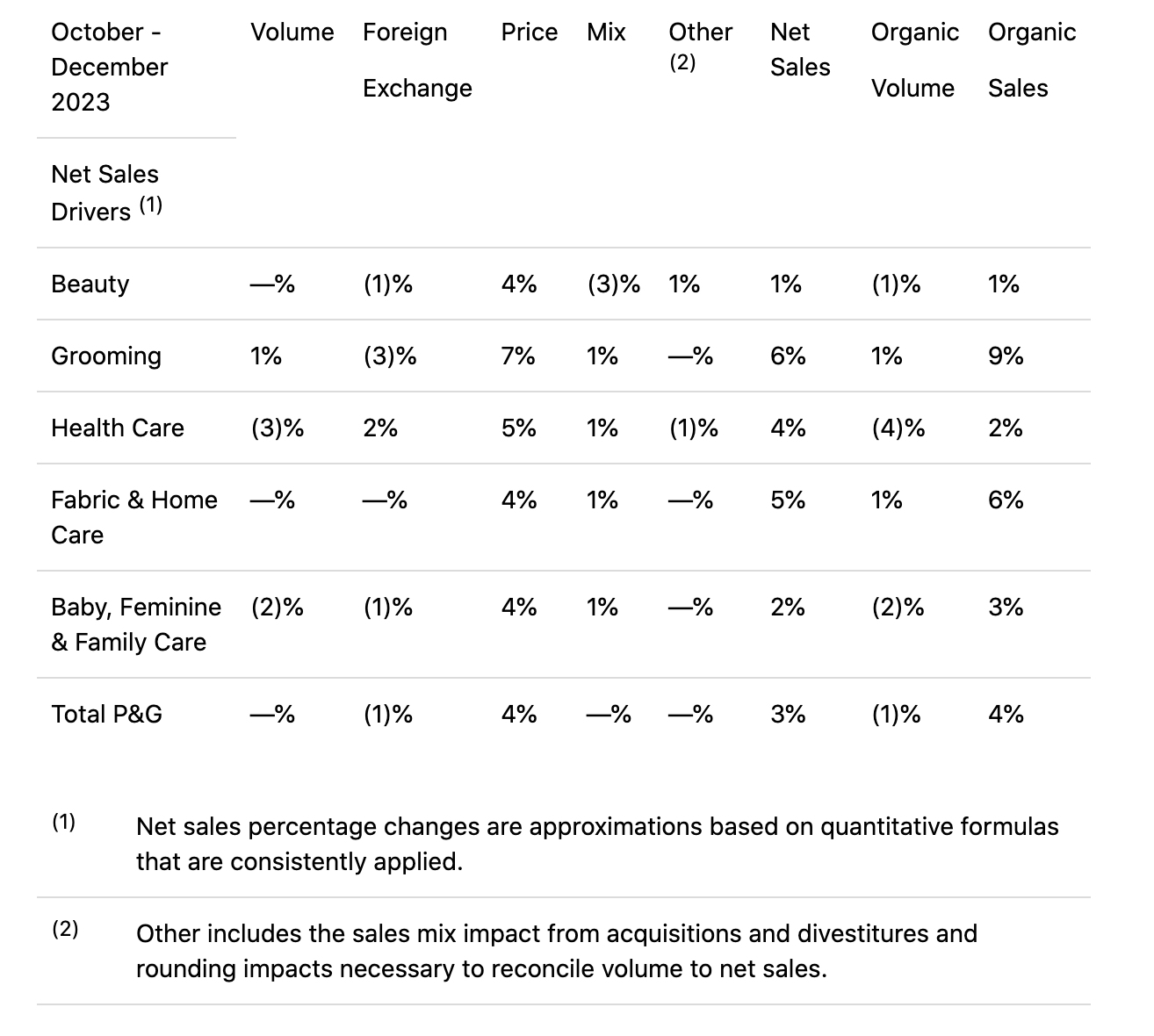

The gross margin expansion of 520 basis points year-over-year has been primarily driven by gross productivity savings, favorable commodity costs and increased pricing. Important to note that the organic sales growth for the quarter has been 4%, accompanied by a 1% volume decline. The operating margin expansion has been 400 basis points year-over-year, mainly as a result of gross productivity savings.

Note that alongside the margin expansion, the demand for PG’s products has remained robust. Organic sales have increased across all segments, primarily driven by the pricing, and occasionally offset by the volume. Looking forward we expect the demand to remain stable as the consumer confidence has shown signs of significant improvement in the past months. One significant risk that needs to be mentioned here is the strength of the economy and consumer in China, which can have a significant impact on the sales volume.

Results – October – December 2023 (PG)

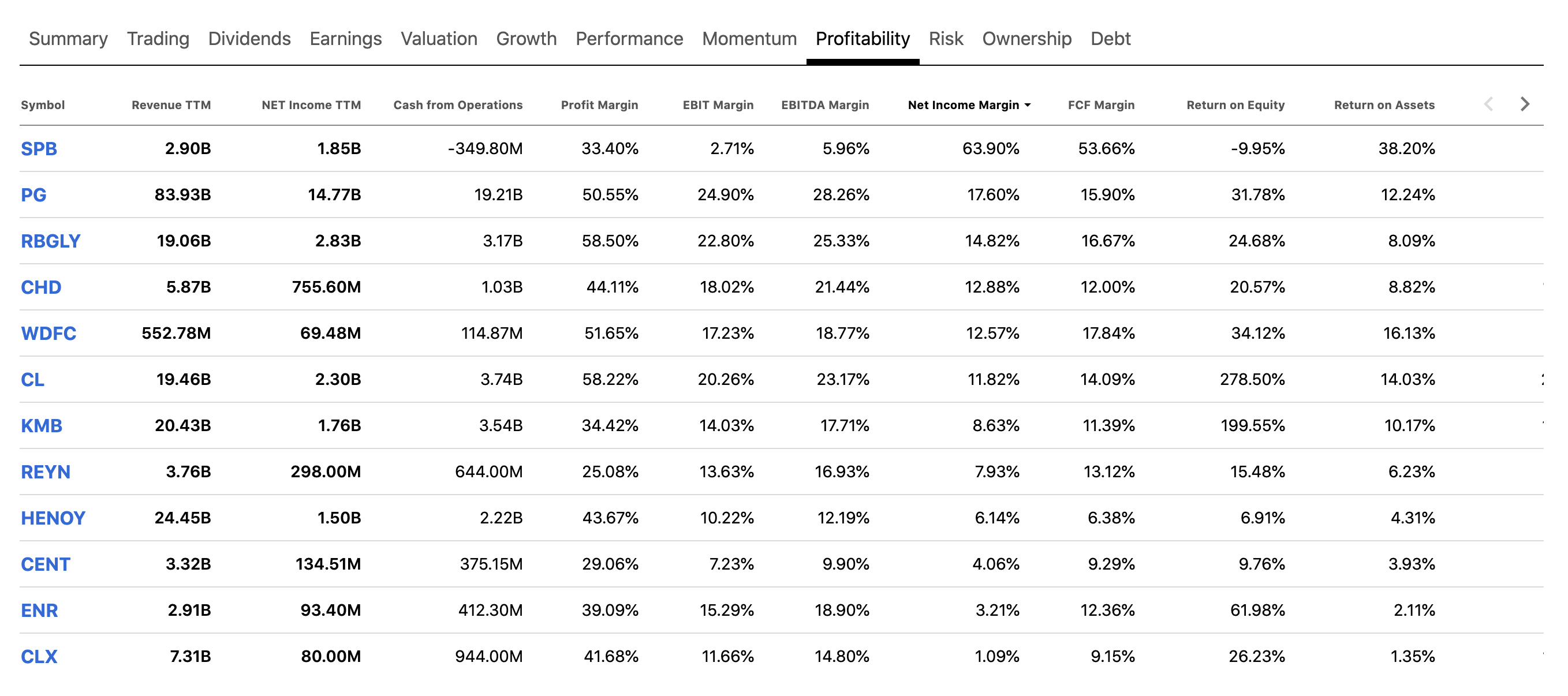

Now, back to profitability. To put PG’s margins into perspective, the following table compares a set of metrics across firms in the household products industry.

Comparison (Seeking Alpha)

We can clearly see that PG’s numbers appear to be close to the top of the list in terms of net income margin, EBITDA margin, EBIT margin and return on assets.

These metrics indicate that PG is an attractive, quality firm within the household products industry. Furthermore, the company expects tailwinds of approximately $800 million after tax due to favorable commodity costs in 2024, which are likely to further boost profitability. Looking forward, however, we are somewhat more cautious and expect the commodity prices to remain relatively volatile, due to the ongoing geopolitical tensions in Eastern Europe and in the Middle East, alongside with the atrocities on the Red Sea. Increased commodity prices could put downward pressure on the margins, which we believe is realistic near term risk for PG and its investors.

It is also important to mention that the firm is expecting also several headwinds during 2024, including unfavourable exchange rates and higher interest rates.

P&G continues to expect unfavorable foreign exchange rates will be a headwind of approximately $1 billion after tax. The Company now expects the net impact of interest expense and interest income to be a headwind of approximately $100 million after tax.

Before moving on, we would like to point out one more thing, and that is related to the net profit margin drop. The recently reported EPS figures have been hurt by the firm’s non-cash impairment of the Gillette intangible asset:

Diluted net earnings per share were $1.40, a decrease of 12% versus prior year primarily due to a non-cash impairment of the carrying value of the Gillette intangible asset. […] The impairment charge arose from a reduction in the estimated fair value of the Gillette indefinite-lived intangible asset due to a higher discount rate, weakening of several currencies relative to the U.S. dollar and the impact of the non-core restructuring program.

Higher non-core restructuring charges have also contributed to the decline.

In our opinion, these are one-time events, and we expect the net profit margin to normalise and continue its upward trend in the coming quarters.

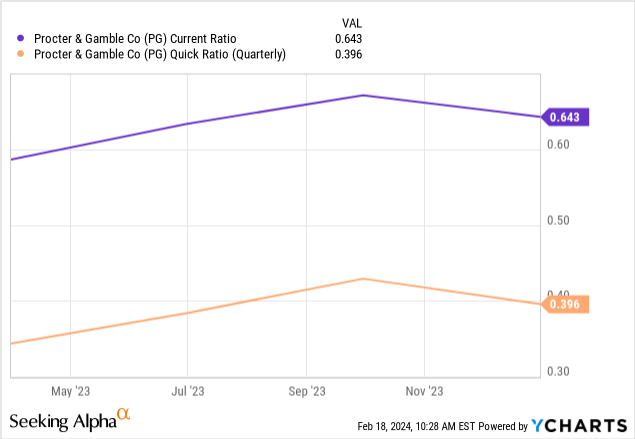

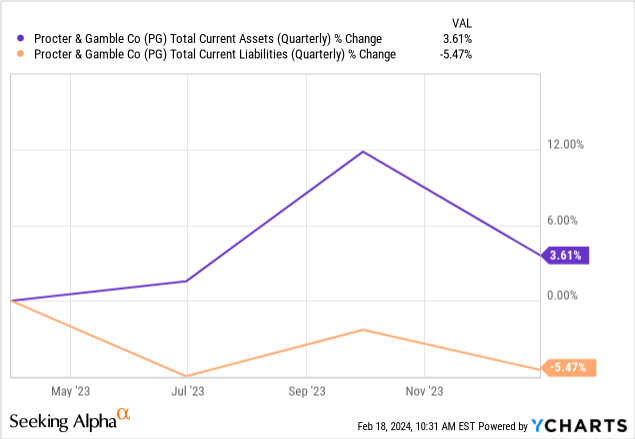

Liquidity ratios

In our previous article, we have pointed out that the firm’s liquidity ratios – current ratio and quick ratio – have been well below 1 and have been trending downwards.

This positive development over the past year has been a result of declining current liabilities and slightly increasing current assets on a year-over-year basis.

We are happy to see that over the past year, these ratios have also improved. While they are still far away from 1, which would indicate that the current assets are sufficient to cover the current liabilities, it is still a promising sign that they are exhibiting an upward trend.

Dividends and share buybacks

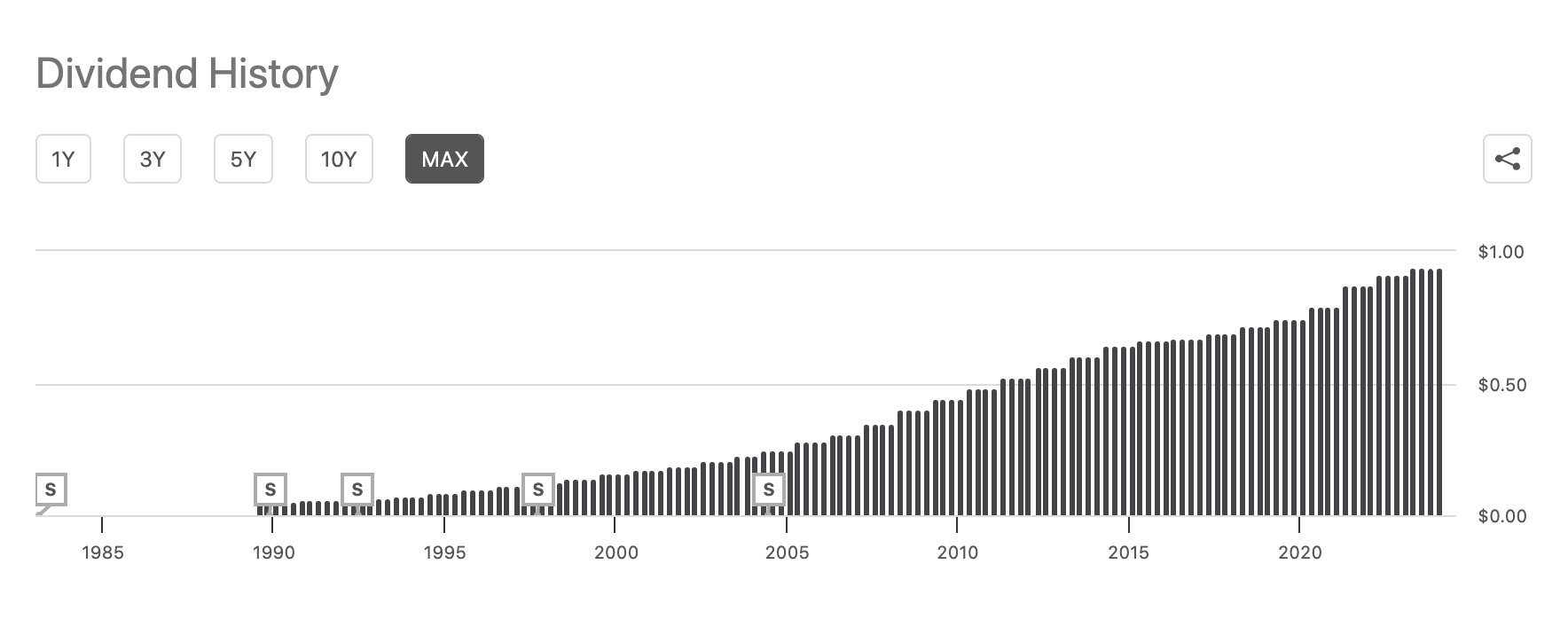

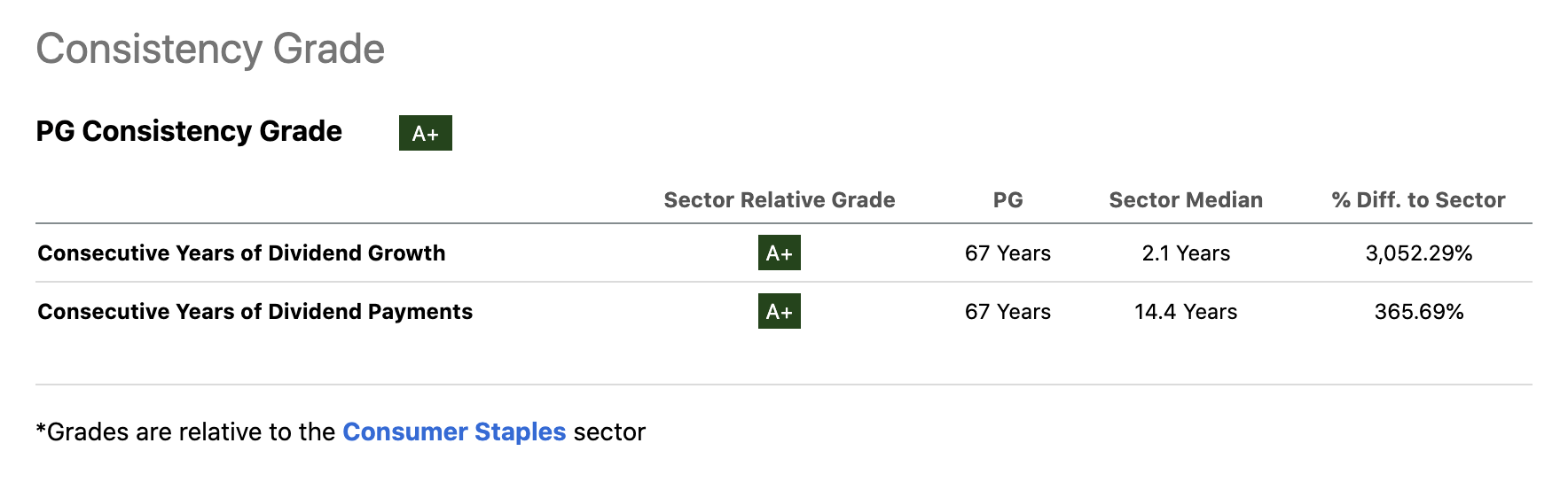

PG has been a favourite of many dividend and dividend growth investors. The company has been a reliable dividend payer for 67 years, and they have managed to increase the dividends in each of these years. As a result, the firm currently pays a quarterly dividend of $0.94 per share, equivalent to an annual dividend yield of 2.4%.

Dividend history (Seeking Alpha ) Dividend growth (Seeking Alpha)

While consistency in dividend payments is important, one needs to make sure that these payments are also sustainable, before blindly investing in a stock for its dividends.

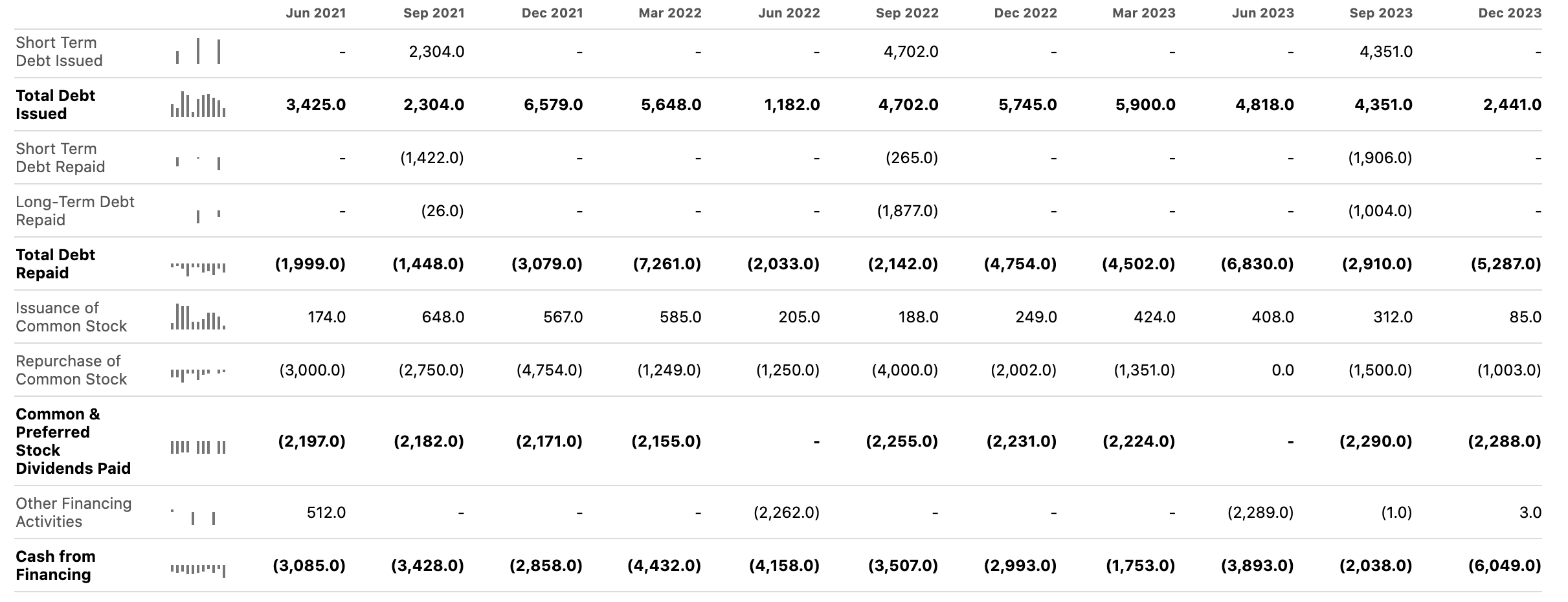

In the past quarter, PG has spent roughly $2.3 billion on paying dividends and roughly $1 billion on buying back shares. At the same time, PG has generated roughly $5.1 billion in cash flow from operations and spent about $0.8 billion on CAPEX, leaving more than sufficient amounts to cover both the dividends and the share buybacks.

Cash from financing (Seeking Alpha)

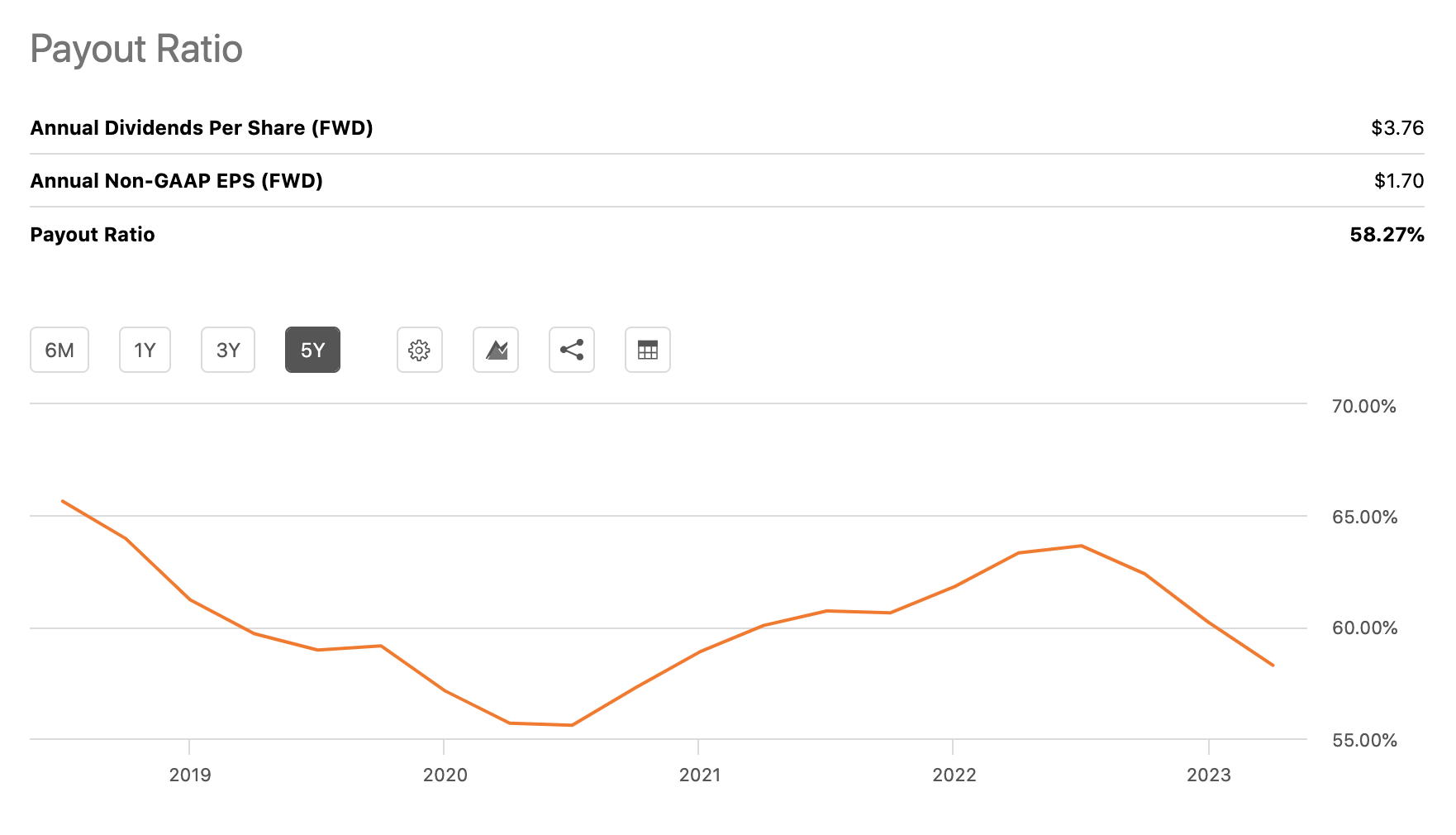

Furthermore, in the past quarters, the company’s payout ratio has also been trending downwards, which is also a strong indication that the returns to shareholders are likely to be safe and sustainable in the near term.

Payout ratio (Seeking Alpha)

The company has also reiterated its commitment to return value to its shareholders in the latest press release:

P&G continues to expect adjusted free cash flow productivity of 90% and expects to pay more than $9 billion in dividends and to repurchase $5 to $6 billion of common shares in fiscal 2024.

For these reasons, we believe that PG remains an attractive option for dividend and dividend growth investors.

Valuation

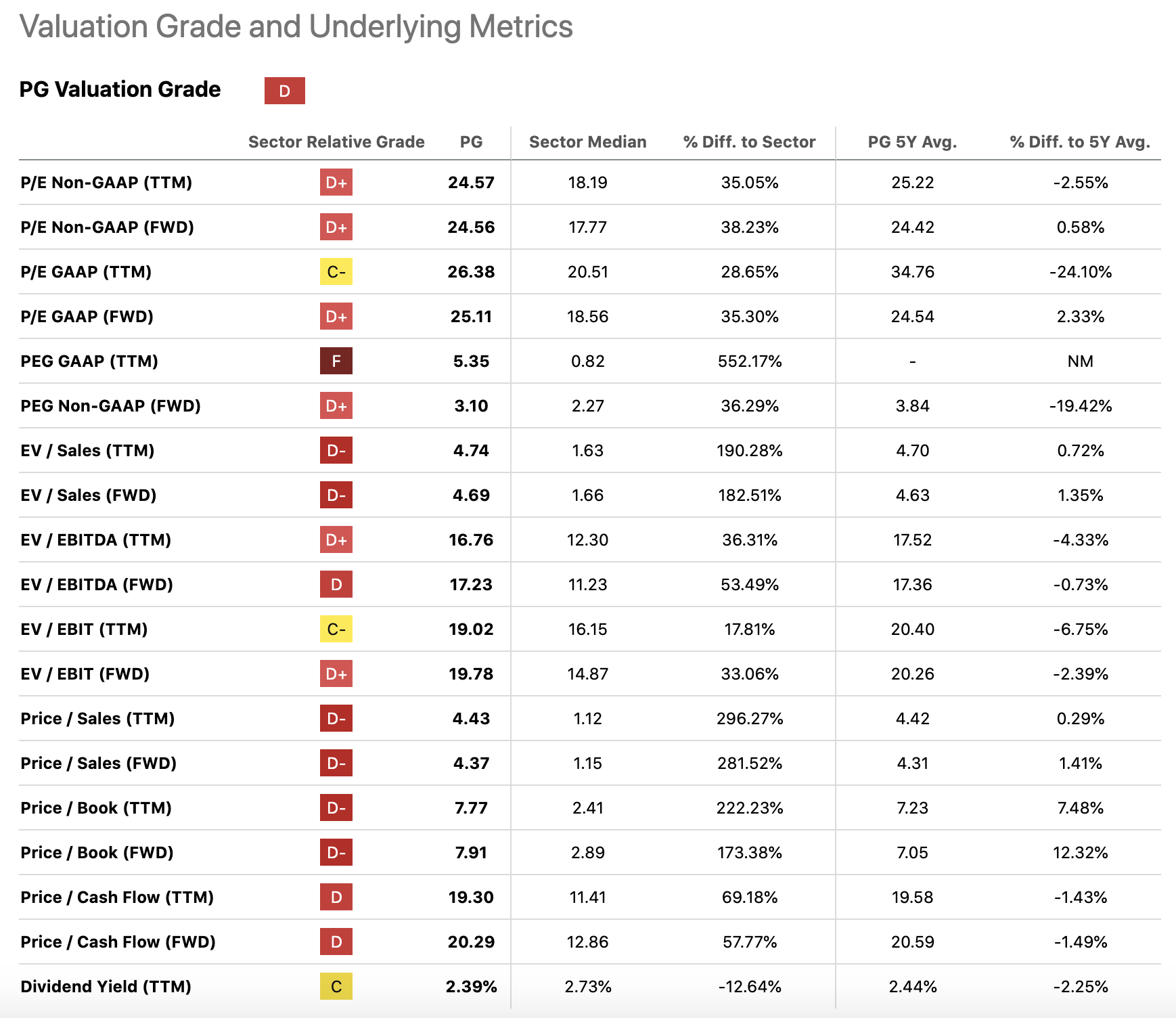

Last, but not least, we have to take a look at the company’s valuation. We will be looking at a set of traditional price multiples to assess, whether the current price could be an attractive entry point or not.

Valuation (Seeking Alpha)

According to the table above, PG seems to be trading at a significant premium compared to the consumer staples sector median. On the other hand, according to most metrics, it is trading at a slight discount or in-line with its 5YR historic averages.

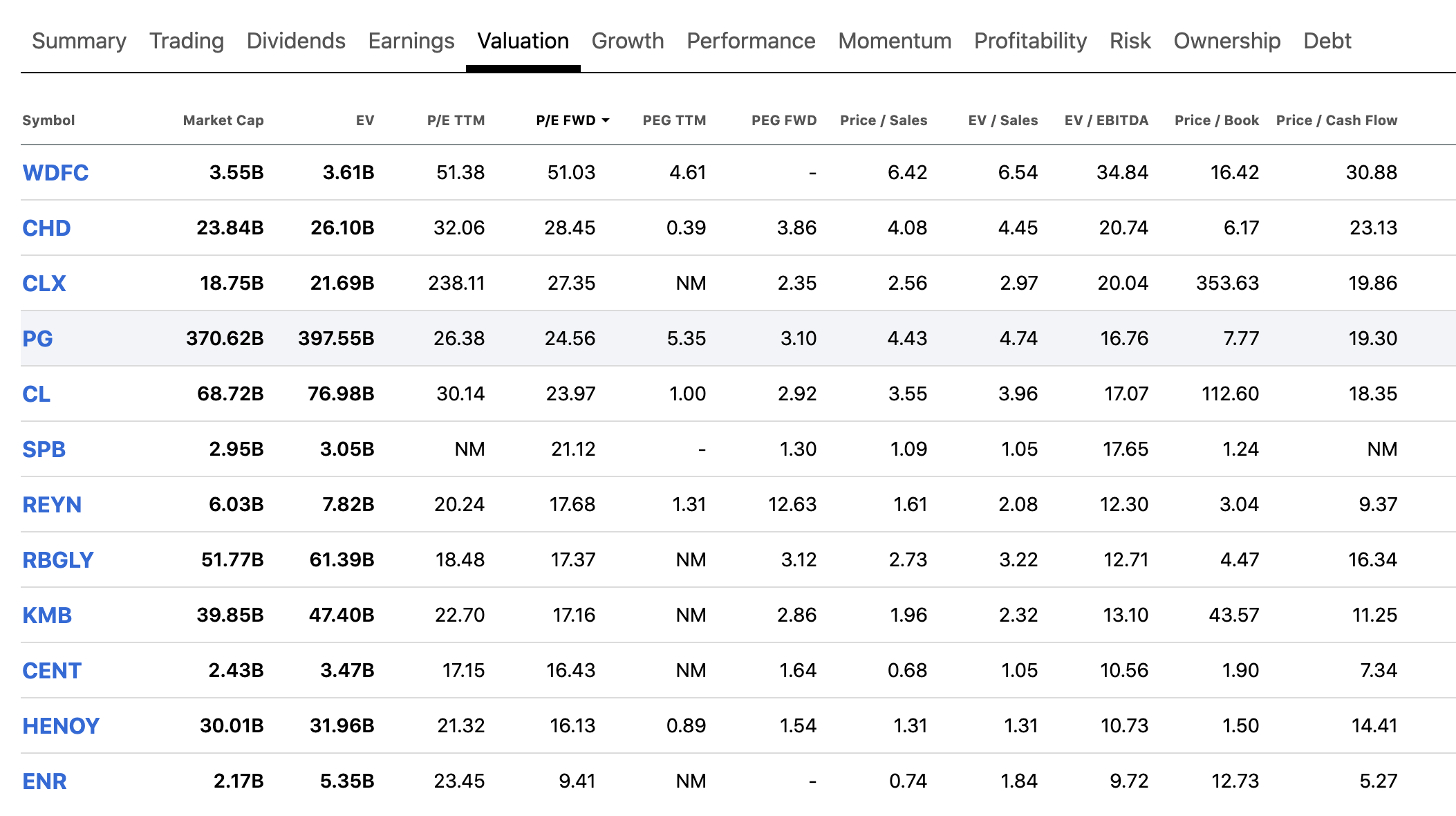

When we narrow down the peer group to the household products industry, PG also appears to be on the more expensive side of the list.

Comparison (Seeking Alpha)

We, however, believe that this valuation is justified. PG has achieved significant organic sales growth in the past quarter, it has improved its profitability, and it keeps paying an attractive and sustainable quarterly dividend. UBS has also named PG on its quality stock list, where they also acknowledge that these stocks tend to be slightly more expensive, but are also more likely to outperform.

For these reasons, we believe that the current price could be an attractive entry point.

Conclusions

PG remains attractive from a profitability point of view, with both gross- and operating margins expanding meaningfully year-over-year. While net profit margin has seen a decline in the previous quarter, we believe that the reasons are one-time events, and the margin should continue growing in the coming quarters.

The firm’s liquidity ratios have also improved year-over-year.

The company remains committed to paying a safe and sustainable quarterly dividend, while it also keeps repurchasing its shares, further improving shareholder returns.

For these reasons, we believe that PG’s stock is an attractive investment in 2024 at the current price levels.

Q2 2024 Earnings Call Transcript")