MF3d

MIM

The Mercator International Opportunity Fund Year End Report, 2023

In 2023, as in 2022, equity markets looked like a big tug-of-war between company fundamentals and guesses about the future direction of interest rates. Ultimately, the major factor influencing stock prices last year was the pace of North American and European central banks’ rate hikes. Because US investors were uncertain about bond markets and an ever-anticipated recession, they sought refuge in index ETFs and the leading large tech companies known as the Magnificent Seven.

MIM

International markets, in contrast, were neglected. Although a yearend rally took global stocks up across the board, foreign indices still trailed US equities. They now trade at an historic discount.

MIM

Following a November 1 low, the Mercator Fund rose 19.93% on the month, propelled by strong quarterly numbers from our portfolio companies and the apparent end of Fed rate hikes. Another 6.80% rise in December brought Mercator’s full year 2023 performance to +11.12%.

Forecasting vs. Investing

The Mercator Fund selects overseas companies in which to invest based on bottom-up fundamental research. We believe that over time we can create value by owning companies with the best long-term prospects, regardless of economic environment. Markets go up and they go down, but, ultimately, a stock price is the reflection of a company’s capacity to generate profits.

Rising interest rates or economic slowdowns may have an outsized influence on investors’ decision making over the short term. Negative geopolitical events, short of wars, are annoying contretemps. It is company managements’ task to sail through them. Values of businesses do not passively float along on short-term economic or political cycles like a flotilla of boats rising and falling together. Instead, hard times actually make strong businesses stronger and more valuable as weaker competitors flounder.

Despite this, volatility in markets often relates to external factors, not companies’ long-term prospects. It is as if investors try to predict the weather instead of looking at the journey. For example, consumer stocks or cyclical companies are often indiscriminately sold in anticipation of a slowdown in the economy. Growth stocks are sold across the board when interest rates rise. The reverse is true as well. We saw this in November when the anticipation that rate hikes were ending ignited a sharp bounce in growth stocks.

In today’s markets, these moves are magnified by ETFs and momentum investing. Short-term trends take on a life on their own. No matter how cheap or fundamentally strong, a stock which is perceived to be in the wrong sector for the cycle has to be sold. Redemptions in sector ETFs then lead to more indiscriminate selling. ETFs have the obligation to sell the baby with the bathwater.

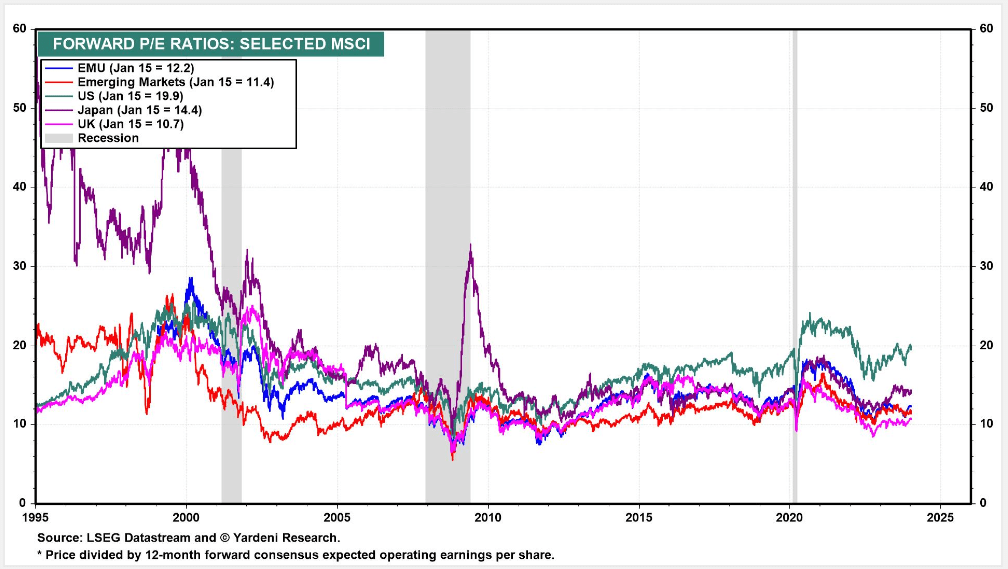

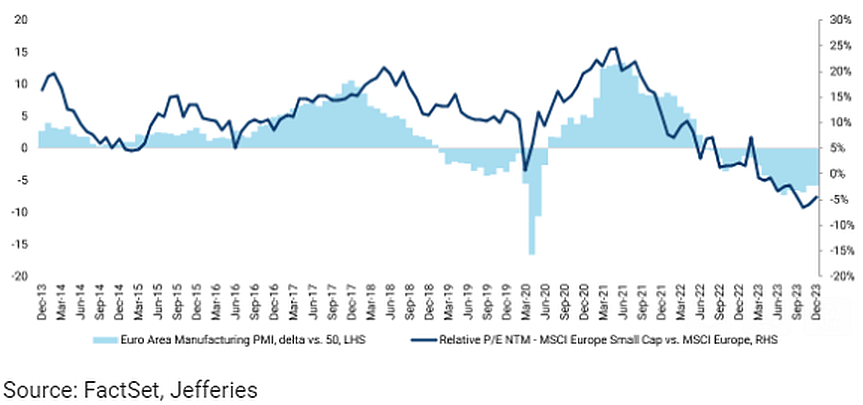

That has been the story of the last two years. As a result, many successful growth companies are now trading at very attractive prices. Realization of these stocks’ upside potential is likely to be dramatic as we saw last November. Volatility works both ways. The chart below shows why we believe the 4Q’s move could be just the beginning. There is still a long way to go before relative valuations get back in line with historic norms.

MIM

It would of course be very nice if we could perfectly time our buying and selling in anticipation of sentiment shifts, but as everyone knows, market timing is a mug’s game. Instead, the Mercator International Opportunity Fund (MOPPX) (MOOPX) tries to select long-term overseas winners and patiently let returns compound over time.

Quarterly Reality Checks

Every three months, quarterly results come out and markets are reminded of the business fundamentals underlying stock valuations. In July, the fund had a nice bounce in the wake of strong earnings reports for the second quarter of the year. The rally quickly fizzled when investors once again turned their focus on macro-economic factors disfavoring growth stocks.

The rollout of the third quarter earnings reports in November was even better for our portfolio holdings. As mentioned above, the combination of companies’ good performance with a more favorable monetary environment led to the year-end bounce in performance.

The Coming Political Tsunami In Europe

The energy crisis everyone was expecting in Europe at the outbreak of the Ukraine war did not materialize. The Old Continent managed to muddle through. Inflation is under control and interest rates seem to have peaked.

In the year ahead, we expect two major events in Europe, one monetary and the other political. Both will greatly affect stock valuations.

On the monetary side, we believe the European Central Bank will lead off the coming cycle of interest rate cuts around the world. The Bank of England will likely follow with some delay, as will the Scandinavian central banks. At this stage, that seems the most probable scenario.

In politics, Europe is on tsunami watch. The traditional parties, from the Dutch Liberals to the German Social Democrats or President Macron’s Renaissance Party, are all feeling pressure from new or rejuvenated conservative parties. Regional elections in Germany and national elections in Italy and the Netherlands have all seen a rejection of politics as usual in favor of parties that were formerly considered unacceptable.

Polls suggest that the May elections for European Parliament will see this movement accelerate. A tidal wave could drown most of the existing political establishment in favor of a new generation. French president Macron understands this. That’s why he appointed a new 34-year-old Prime Minister to try to break this wave.

The rising conservative movements in European countries share a common desire for a more pragmatic approach to today’s challenges. They don’t so much oppose existing policy goals as they try to manage them better. European citizens overwhelmingly believe in global warming but are fed up with the draconian regulations in place to combat it. The outgoing Dutch government’s plan to cut nitrogen emissions by shutting down big farms and reducing livestock herds by 50% is a case in point. How are these farmers supposed to make a living? What are Dutch people supposed to eat?

Most Europeans similarly do not reject the Europe Union, but they are tired of the endless stream of suffocating regulations coming from Brussels. Even immigration has become a hot topic mostly because it is perceived to be out of control. Many immigration policies are no longer just compassionate. They have become unaffordable. For example, reading the political tea leaves, President Macron asked his former Prime Minister to water down a long-existing law that gave every person on French soil, legally or not, full health benefits.

The new Continental conservatives are also taking a more pragmatic approach to business and social issues. Europeans are still very attached to their social programs, but seem to think that things went a bit too far. The mood is for a little less equality and a bit more meritocracy. This should translate into fewer constraints on businesses, including lower fiscal pressure, which could turn out to be very good for growth and profitability.

Japan: A Tourist Investor Destination No More

The Bank of Japan (BOJ) first pioneered Quantitative Easing policies in 2001, years before the Federal Reserve Bank started pumping up our financial system. Japan’s QE was an attempt to revive its economy following the collapse of the 1980’s asset bubble and the first of what would be Japan’s three lost decades.

The BOJ resorted to QE only after repeated attempts to kickstart the Japanese economy through fiscal stimuli produced nothing but the largest public debt ever seen in a functioning modern economy. This deficit had to be financed somehow. The BOJ obliged and QE was born.

Successive administrations and the BOJ were greatly helped by the large private Japanese banks. Many years ago I wrote about how Japanese banks were enabling government deficits by investing most of their deposits in JGBs (Japanese Government Bonds). The return on these bonds was laughably minimal, even negative at times, but so were the risks. Anyway, the government probably did not give banks a choice but to redirect money normally destined for the private sector. In Japan, the perceived common good tends to prevail.

Economists will long debate the effects of the BOJ’s method of financing Japan’s huge public deficits. It possibly helped avoid a more severe depression. However, it did not manage to get Japan out of its economic slump for the simple reason, one suspects, that public debt crowded out the private sector. Japan Inc went into hibernation.

Two additional lost decades later, the BOJ had very little to show for its efforts. But something has changed in recent years. Global inflationary forces finally seem to have stopped Japan’s deflationary spiral. This, together with a number of other factors which we discuss below, makes us feel optimistic about the long-term prospects for a sustainable Japanese comeback.

Japan Is Back

The Japanese post-war economic miracle was built on an export-driven economy fueled by an undervalued currency. The weak yen helped make Japan’s export machine the envy of the world. Even today, exports are a large part of Japan’s economic engine. They account for nearly 22% of the total GDP vs. roughly 10% in the US, whose economy is much more dependent on domestic consumption**.

Recently the Japanese turned again to the currency playbook that worked so well for them decades ago. Over the last three years the yen has depreciated sharply. In 2020, a yen holder could buy a dollar for 103 yen; today it costs 145 yen. This orderly depreciation made Japanese goods more competitive, and it boosted companies’ overseas revenues and profit margins.

The post-war economic boom was also built on a steady rise in the value-added of the goods exported. Japan in the 1980s dominated many technology industries, from PCs to consumer electronics and high-end cars to semiconductors. By the end of that decade, for example, half of all semiconductors in the world were made in Japan. Today, less than 9% are made there. Motivated by geopolitical tensions and the need to build a modern defense industry, there is a government-driven initiative underway to regain a dominant position in the semiconductor industry.

Along with the weak yen and the ambition to become a technology leader again, another factor currently making Japan more attractive to foreign investors is the ongoing push to improve corporate governance. Authorities of he Japanese bourse have started to publish a list of those firms attempting to strengthen their corporate value, implicitly shaming those who are not. In a country where public opinion is important, the motivational power of such pressure should not be underestimated.

All this is creating a renewed interest in Japanese equities and Warren Buffett is leading the charge. The Japanese stock market is no longer a value trap attracting “tourist investors”. In fact, the Nikkei index is at last about to break through its all-time high of 1989!

Hervé van Caloen, CIO

* Japan Private Consumption: % of GDP

** Domestic consumption accounts for 55% of Japan’s GDP, vs 68% in the US.

*** https://www.macrotrends.net/2550/dollar-yen-exchange-rate-historical-chart

The MSCI EAFE Index is designed to represent the performance of large and mid-cap securities across 21 developed markets, including countries in Europe, Australasia and the Far East, excluding the U.S. and Canada. The Index is available for a number of regions, market segments/sizes and covers approximately 85% of the free float-adjusted market capitalization in each of the 21 countries.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Fund. This and other important information about the Fund is contained in the prospectus, which can be obtained by calling 800-869-1679 or at www.mercatormutualfunds.com. The prospectus should be read carefully before investing.

The Fund is distributed by Arbor Court Capital, LLC, member FINRA/SIPC. Arbor Court Capital is not affiliated with Mercator Investment Management, LLC.

Q2 2024 Earnings Call Transcript")