asbe

SMCI and the AI Tidal Wave

Super Micro Computer (NASDAQ:SMCI) is currently the best-performing stock in the S&P 500, soaring 255% year-to-date and almost tripling the next best performer, NVIDIA (NVDA). As covered in my last article on Nvidia, both companies have seen a surge in revenues on the back of accelerating demand for artificial intelligence. Developments in generative AI applications, specifically Open AI’s Chat GPT, helped spur market affinity for businesses of the like.

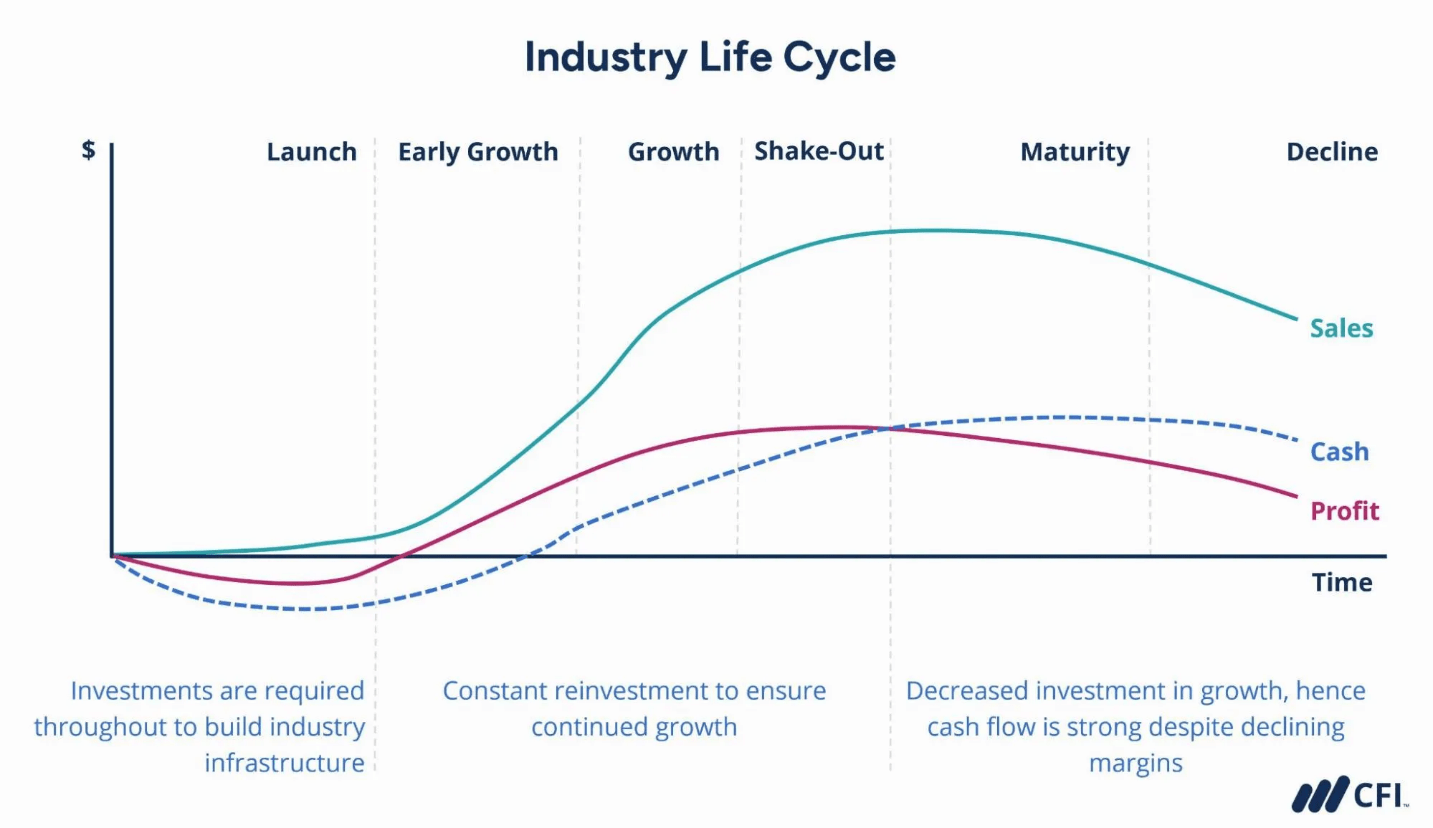

The industry life cycle curve is a helpful way to visualize the modern emergence of AI. Let’s start by looking at the chart:

Corporate Finance Institute

Machine learning and AI have been in development since the 1950s, making periodic strides as the decades passed. We could classify this as the Launch/Early Growth stage. But only in the last two decades has there been a boom in more direct use cases, thanks to massive amounts of data via the internet and the discovery of high-efficiency computing processors like the GPU – carrying us further into the Early Growth stage. Then in late 2022, Chat GPT signaled the start of the Growth stage, characterized by deepening investment, rapid adoption, and category-defining leaders like NVDA generating tons of revenue and expanding margins. Given the disruptive potential of AI, basically a technology of technologies, I expect the growth stage to outlast most technologies of the past – with some firms benefiting more than others.

In this article, we’ll examine the bull and bear cases for Super Micro Computer and see if it has the potential to be a long-term winner in the AI industry. Then, we’ll dive into the company’s current valuation and assess the stock’s attractiveness as shares soar into the $1,000’s. But first, let’s see where SMCI fits in the AI value chain.

During a Gold Rush, Buy Shovels

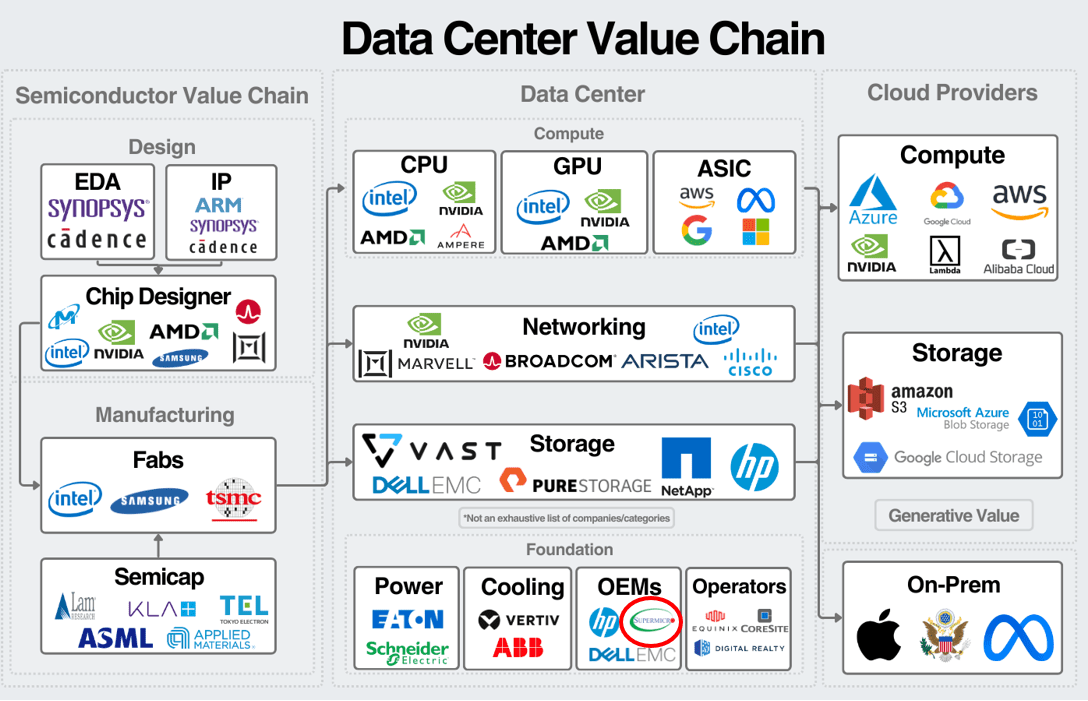

Super Micro Computer (or Super Micro) designs and manufactures high-performance servers and storage systems for data centers across various industries. Server and storage infrastructure is required to handle the intensive computational workloads in technologies like cloud and edge computing, 5G, cybersecurity, and artificial intelligence. Storage units enable data availability and accessibility so hyperscalers like Google, for example, can store and access the trillions of data points captured across its suite of products. Servers house the memory, processors, and cooling systems and are thus the vehicle by which large language models are trained and inferenced. Eric Flaningam has an excellent breakdown of the data center value chain (SMCI circled at the bottom):

Eric Flaningam

Essentially, the investment case for IT infrastructure companies is ‘in a gold rush, buy shovels’. But will this strategy play out with Super Micro?

The Bull Case

Industry Tailwinds

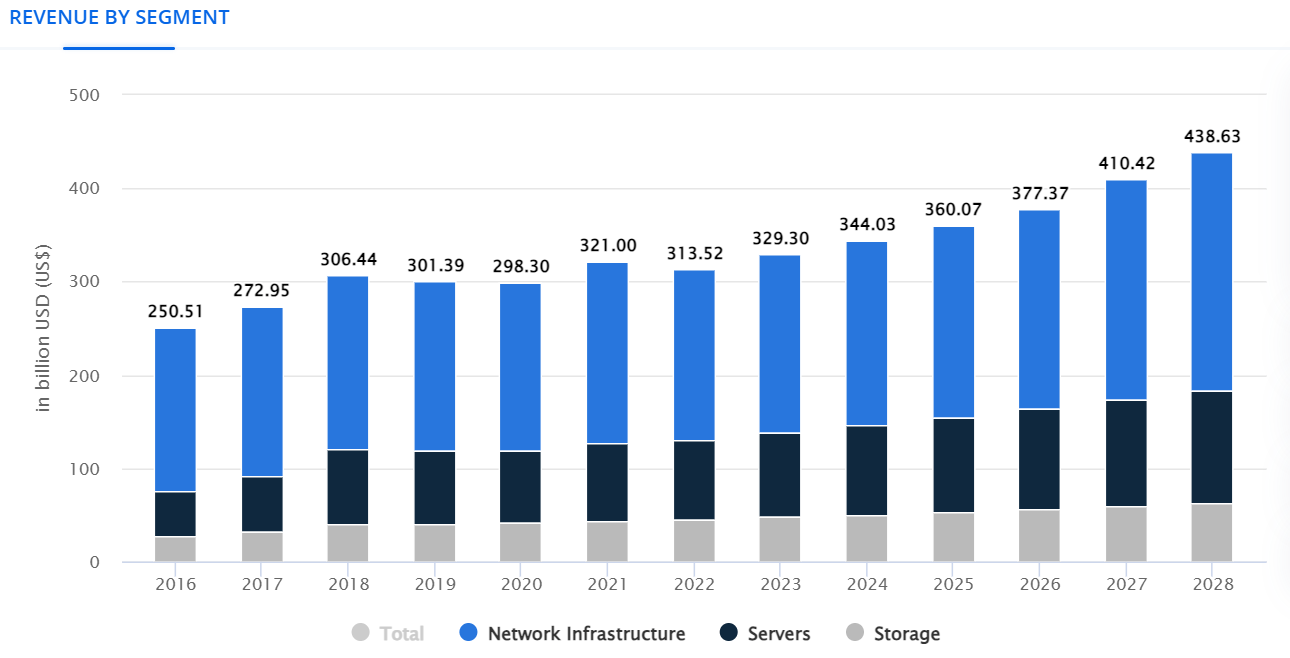

As covered in my last article, the potential of AI to reshape how businesses and economies function is compelling, which has helped propagate the market’s excitement. The primary vertical for a hardware company like Super Micro is data centers, which is where the magic happens for AI and high-performance computing (‘HPC’). Overall, Statista expects the global data center market to reach near half a trillion dollars by 2028. Networking is expected to continue comprising the largest share, but servers and storage should still benefit handsomely.

Statista

This blog post by network systems company FS outlines the primary drivers behind demand for advanced data center servers, including:

- Increased computational demands for deep learning models

- Greater storage requirements for massive data sets

- Scalability challenges as workloads grow

- Specialized hardware for new processing technology

- Energy consumption cost and environmental issues

Requirements for data center infrastructure will likely grow in tandem with AI and HPC adoption. This list also helps us identify the key differentiators within Super Micro’s competitive space and leads us to the next piece of the company’s bullish case.

Product & Strategy

Super Micro products are designed to address the current industry challenges listed above as the company seeks to capture two-fold differentiation: technological and time-to-market advantages.

SMCI is heavily focused on product development as 50% of its workforce are engineers, including its founder and CEO. SMCI invests on average 4-6% of revenues on R&D, whereas main competitors Dell (DELL) and Hewlett Packard (HPE) are closer to 2-5%. Albeit Dell and HP’s absolute R&D spend is in the billions while Super Micro’s is about half a billion. Even so, Super Micro is more of a pure play on advanced data center technology, with an emphasis on AI and HPC data center operations. And the company tailors its products as such. It focuses development on high performance, scalability, energy efficiency, and adaptability with new technologies to keep up with innovations in the processing space. All of which address key factors just listed. Here is a quote from the company’s CFO at a recent tech conference describing the company’s approach:

This differentiates us from both the ODMs as well as other Tier 1 server manufacturers who try to offer a select number SKUs to address all of – a broader part of the market. Whereas we go in and we design something unique for a customer that not only gives them the very best const performance metric, but it also gives them the lowest total cost of ownership.

Along with this is the company’s most meaningful advantage in my view: a concentration on being first to market. Innovation is rapid in AI and HPC, often awarding the nimblest companies. SMCI aims to implement new technologies quickly, iterating along the way and allowing customers to keep up with customer demands for AI. Its rack scale and liquid cooling solutions then enable the scalability and energy efficiency many companies require. Partnerships are also a big help in this area. The company is strategically headquartered in Silicon Valley near many of the world’s largest tech firms, allowing SMCI to quickly implement new technologies from partners like Nvidia, AMD, and Intel.

It’s easier to claim competitive advantages than it is to show them, but Super Micro appears to be walking the talk.

Growth & Market Capture

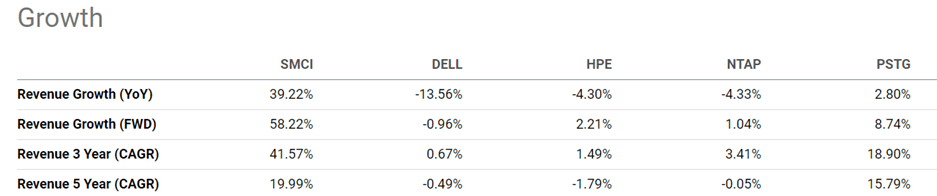

Super Micro’s incredible growth is at least some evidence of differentiation in its competitive field. Revenue has been doubling and even tripling the company’s historical growth and vastly outpacing competitors who have printed near zero growth.

Seeking Alpha

The trend doesn’t appear to be slowing as management has guided for over 100% topline growth in fiscal 2024. SMCI has also been able to command a premium price, or at least keep up with inflation, with leadership pointing out average selling prices (‘ASP’) were a big driver of growth the last two years, yet with volume demand remaining a tailwind going forward.

Our growth will be quicker in terms of unit number. So that volume growth will be quicker than ASP, because the last two years, our ASPs have been growing a lot. So, in next day, but I guess unit number, volume will grow faster.

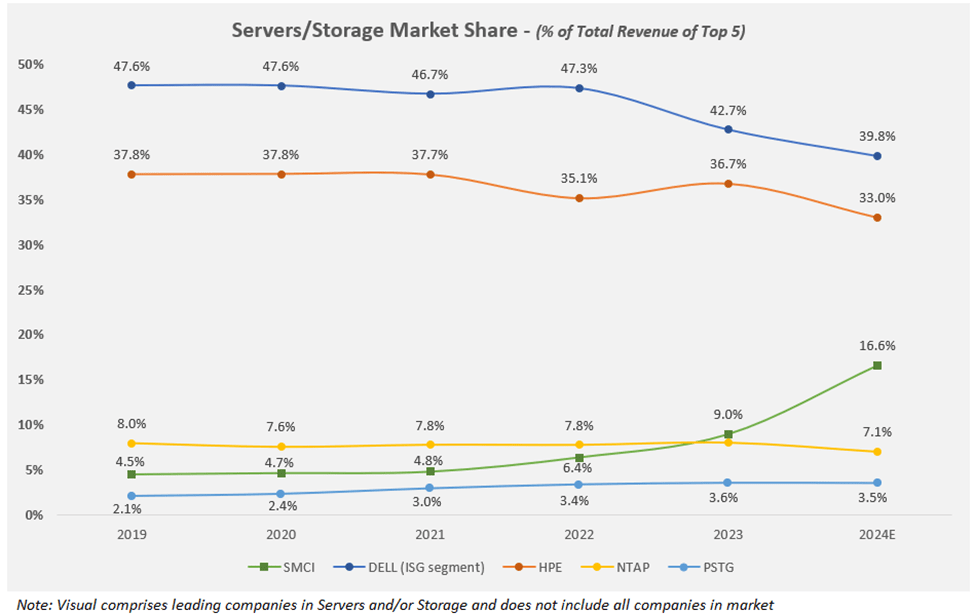

This comparatively strong growth has enabled the company to capture meaningful market share:

Author

The Bear Case

Market Positioning

While I do believe Super Micro is in an attractive industry with heavy tailwinds and that it has some competitive strength in servers and storage; I view the space as less advantageous than others.

Server and storage designers and/or manufacturers may exhibit some technical advantages but are ultimately reliant upon innovations within processors up the value chain, a weaker position economically. Chip producers have sizable leverage both technically and on supply and pricing as a result. Evidence of this is shown in Super Micro’s cost of sales and gross margin. According to the company’s 10k:

Prices of certain materials and core components utilized in the manufacture of our server and storage solutions, such as GPUs, serverboards, chassis, CPUs, memory, hard drives and SSDs, represent a significant portion of our cost of sales.

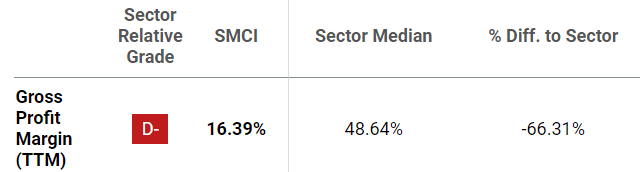

Despite expanding gross margins from 15% in 2021 to 18% in 2023, margins shrunk back to 15.4% through the first half of 2024. Management also set a target for gross margin between 14% and 17% in 2021 and has not changed that range. Even considering the low gross margin nature of the company’s industry, this range is meaningfully below the sector median and close competitors:

Seeking Alpha

Currently, Super Micro is heavily investing in production and capacity to keep up with demand with the goal of achieving economies of scale, and thus margin leverage:

…as we ramp revenues up, we are going to get leverage on the gross margin because, as Charles mentioned earlier, we are going to get higher efficiency and factory throughput as we — which will lower costs as we put more through the factories. So we will get some benefit there. We will also get benefit as we transition more manufacturing over to Malaysia and Taiwan. And I think that — so that’s why right now we are, although, very competitive situation.

While the company has done well expanding market share and capturing bigger customers, allowing for more room to grow, Super Micro relies heavily (90%+ of revenues) on unit sales instead of a recurring source of revenues like software or networking, making scalability much tougher.

SMCI 2023 10K

And the longer this process takes without showing fruit, the greater the opportunity there is for competitors to step in. If you’re Nvidia or AMD, you don’t have much of an incentive to only sell chips or components to Super Micro, outside of a partnership agreement. If chipmakers have supply, they will sell far and wide to meet demand. And if they don’t because of supply chain issues, Super Micro also suffers. The company also has significant supplier and customer concentration risks, which have increased into 2024.

SMCI 2023 10K SMCI 2023 10K

These two interesting suppliers, Ablecom and Compuware, represent over 60% of purchases each and are located in a geopolitically volatile Taiwan, along with a big portion of SMCI’s operations. The customer concentration is less of a risk, one even rumored to be Meta (META), but should these customers switch suppliers, SMCI would be in trouble. Some hyperscalers even prefer to build their own internal data center infrastructure, limiting some of SMCI’s potential market.

In sum, the nature of Super Micro’s positioning in the data center value chain carries much less long-term leverage on both the supplier and buyer side, has lower margins, and is exposed to greater cyclicality. All in addition to several internal risks.

Management & Capital Allocation

Let’s start with the positives. Super Micro is founder-led with insiders owning almost 15% of shares outstanding. ‘Owner-operator’ companies tend to have more aligned interests with shareholders and long-term value creation. SMCI’s stock price appreciation is not the only indicator that CEO Liang has captained the company well. Leadership has kept operating costs under control while still investing heavily in R&D and Capex to gain a competitive edge and has recently churned out impressive returns on capital through mostly organic growth.

Morningstar

Even though recent growth has created value through high returns on capital, the road ahead looks hazy. Super Micro has generated some expansion in operating margin, but it has stabilized recently (unlike Nvidia), possibly due to a lack of leverage mentioned previously. Additionally, operating and free cash flow are hit or miss, meaning the company is having difficulty turning operating income into cash. I suspect this is due to rapid growth putting pressure on working capital and supply/inventories. As a result, management is forced to borrow debt or raise equity to help fund operations. Raising debt or equity isn’t necessarily a bad thing, but I prefer companies that avoid shareholder dilution and avoid the risks associated with debt, using internally generated cash instead.

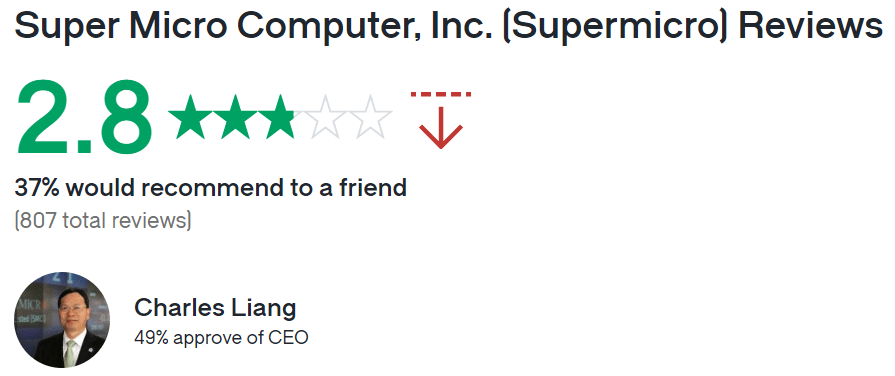

Super Micro is also poorly rated on Glassdoor, with CEO Liang only garnering 49% approval.

Glassdoor

Additionally, the company is not without its questionable internal activities the past five years:

- Faced allegations of Chinese tampering of its servers with spy chips by Bloomberg Businessweek, which the company has denied.

- SEC regulator identified widespread accounting violations resulting in a $17.5M settlement.

- Two biggest suppliers, Ablecom and Compuware. CEO of Ablecom is Charles’ brother Steve and Charles’ wife has a 10.5% stake in Compuware.

- CEO Liang borrowed $12.9M from his brother’s wife to repay margin loans which has expanded to $16M as of June 2023.

Valuation

Now that we have an idea of the main arguments in the bull and bear camps, let’s investigate the stock’s valuation.

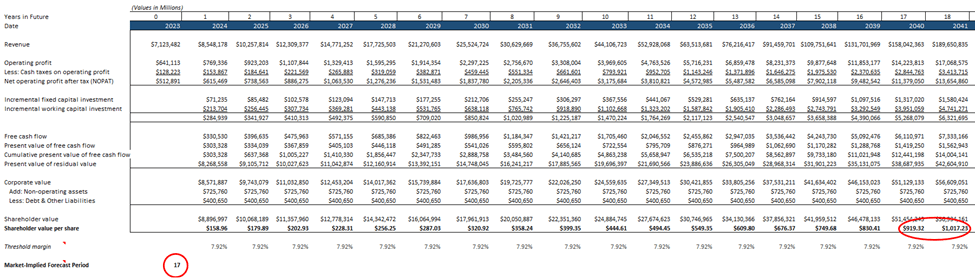

For this article, I wanted to try out the valuation approach outlined in Expectations Investing by Colombia professors Michael Mauboussin and Al Rappaport. It entails utilizing a long-term reverse DCF to assess the fundamental expectations already baked into the stock price, then using scenarios and probabilistic thinking to determine an expected fair value. This approach enables me to take a mostly objective view of price, prior to making my own assumptions and forecasts, and judge the reasonableness of the market’s expectations.

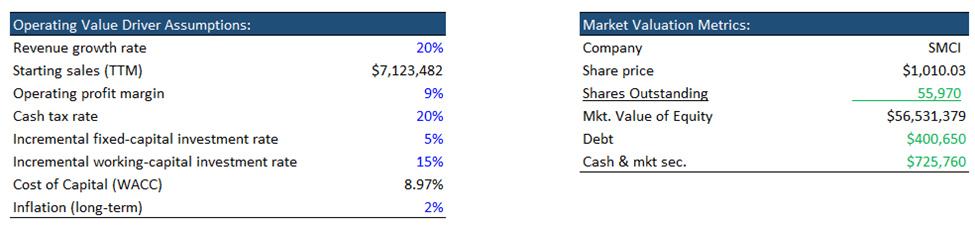

First, we find the consensus view of the drivers of value (cash flow): long-term revenue growth, operating margin, taxes, cost of capital, and reinvestment. For revenue, I grabbed average analyst estimates from Seeking Alpha, excluding an outlier full year 2024. Consensus estimates of operating profit are around 8-10%, so I stuck with 9%. I kept working and reinvestment rates were slightly higher than 5-year averages as Super Micro keeps up with growth. And lastly, I calculated cash taxes and WACC to be 20% and 9%, respectively.

Author

Next, I used a reverse DCF model to calculate the market’s implied forecast period (‘MIFP’), or the number of years the market expects the company to generate returns above the cost of capital. It essentially shows how long the company would need to generate the above value drivers to justify the current stock price and gain returns equal to or above the cost of capital. It does this by showing how long it would take for shareholder value (PV of cash flows per year) to reach the current stock price. The higher the MIFP, the higher the market’s current expectations. At the current price, SMCI’s forecast period is 17. Meaning the market expects Super Micro to grow revenues at 20% annually through 2040, which would total just shy of $160B. Those are quite high expectations.

Author

Next, I introduced bull and bear scenarios by adjusting revenue growth and operating margins up and down 3% each and comparing the increase or decrease in shareholder value in year 17. SMCI shows some downward asymmetry.

Author

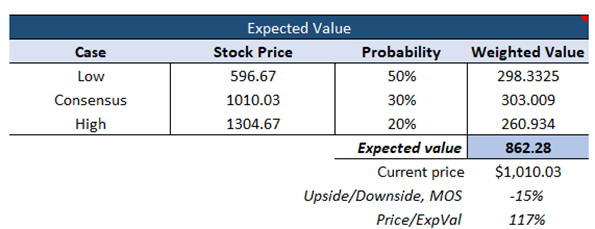

Finally, I assigned my own probabilities to each scenario and calculated a weighted average ‘expected value.’ Here is a breakdown of my rationale for each case:

- Low (underperform consensus): I view this scenario as most likely with a 50% probability. As we saw, the server industry is a smaller, slower-growing, and less advantageous piece of the data center value chain.

- Consensus: While I think it’s more likely SMCI will achieve consensus operating margin targets, I do not believe the company will generate 20% annual revenue growth for 17 years based on factors already discussed.

- High (outperform consensus): I view this as highly unlikely but assigned a 20% probability to hedge against the potential of SMCI to generate new sources of revenue.

The result was an expected value of $862.28. SMCI is overvalued by at least 15% based on my assumptions.

Author

Conclusion

I don’t put all my eggs in the valuation basket, but even if SMCI is fairly valued, I see other areas of the data center and AI industries as much more attractive than Servers and Storage – especially considering the internal issues and risks apparent with Super Micro. And it’s at least unlikely that the stock is undervalued, given the tremendous expectations baked into the price. Ultimately, the future is quite uncertain for Super Micro with a quickly changing and dynamic industry. Both bulls and bears have solid arguments, but because of its premium price, tough competitive environment, and quality below my standards, I would not consider buying shares.

Q2 2024 Earnings Call Transcript")