alvarez/E+ via Getty Images

Aberdeen has already made some big moves since taking over the management of four of the previously managed Tekla healthcare and biotechnology CEFs on October 27th, 2023.

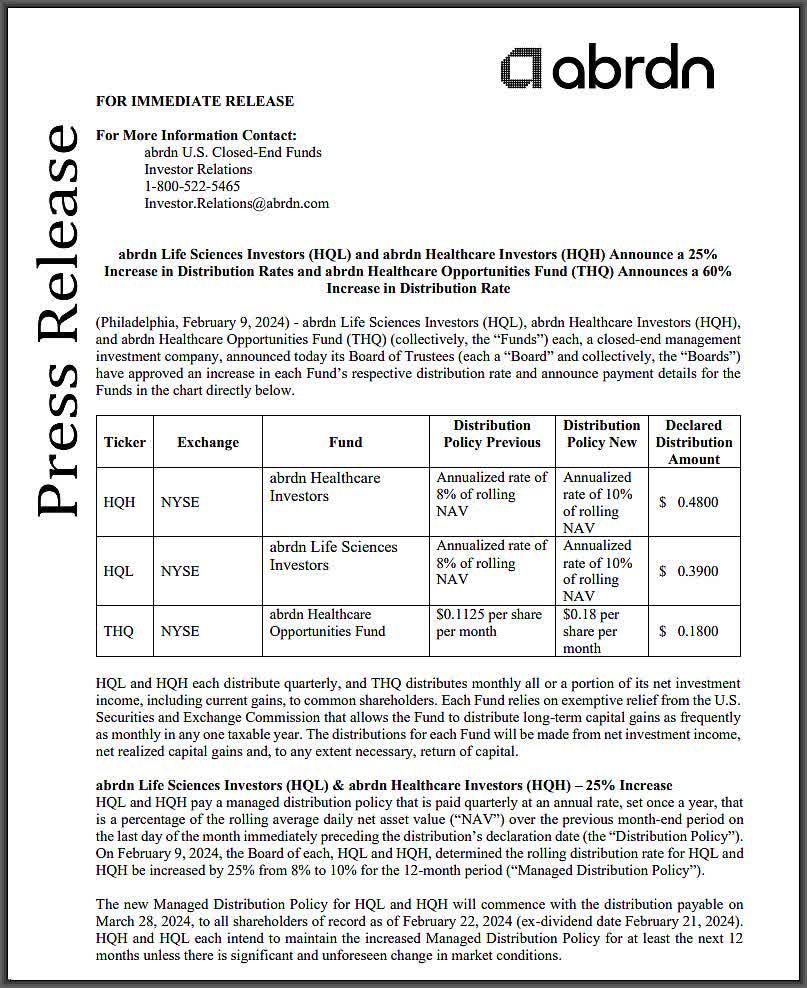

Perhaps the biggest change came just the other day on February 9th when distribution declarations for February were announced and Aberdeen increased the distributions for the abrdn Healthcare Investors (HQH) fund, $17.41 closing market price, and the abrdn Life Sciences Investors (HQL) fund, $14.10 closing market price, by 25% and increased the distribution for the abrdn Healthcare Opportunities Fund (NYSE:THQ), $19.44 closing market price, by a whopping 60%.

Usually, if a fund increases its distribution by that much, you would see an immediate jump in market price and indeed, THQ did open up over $20/share the next business day on Monday, February 12th, and got as high as $20.19 that day.

But by the end of last week, THQ closed at $19.44, only +3.2% better than where THQ closed before the distribution increase was declared. This got me thinking, why would shareholders sell after such a blockbuster announcement?

After all, THQ’s monthly distribution has been the same $0.1125/share ever since it came public in July of 2014. That is, it didn’t change during COVID-19 in 2020, it didn’t change during the Federal Reserve’s rate hiking campaign in 2022, nor during any taper tantrums, tariff wars or any other bear market period since 2014.

So increasing the monthly distribution 60% from $0.1125/share to $0.18/share, starting with this Wednesday’s, February 21st ex-dividend date, should have been HUGE news. That 60% distribution increase also increased THQ’s current market yield over 500 bps from +6.9% all the way up to +11.1%.

But instead, THQ’s market price discount valuation only improved from -14.7% to -12.7% since the announcement. Now, you could argue that these changes just put THQ’s yield and discount in the same ballpark as HQH and HQL, but HQH and HQL are also more biotechnology stock focused, which doesn’t seem to get as high a valuation over the more conservative pharmaceutical and traditional healthcare stock-based funds.

And besides, THQ’s sister fund, the abrdn World Healthcare Fund (THW), $12.66 closing market price, trades at a +2.3% premium valuation even though its portfolio reflects a global selection of healthcare stocks with only 64% exposure in the U.S.

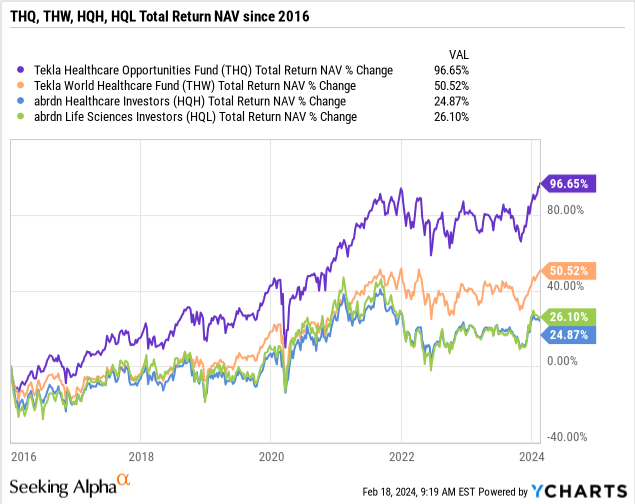

So, does something seem off that we wouldn’t see a bigger positive reaction from THQ now that its market yield has jumped to 11.1%? What makes it even more perplexing is that THQ’s NAV performance is far, far ahead of the others over just about ANY time frame you use.

Here is the NAV total return percentages of all 4 Aberdeen healthcare CEFs since 2016, the 1st year that all 4 funds were trading after THW came public in June of 2015:

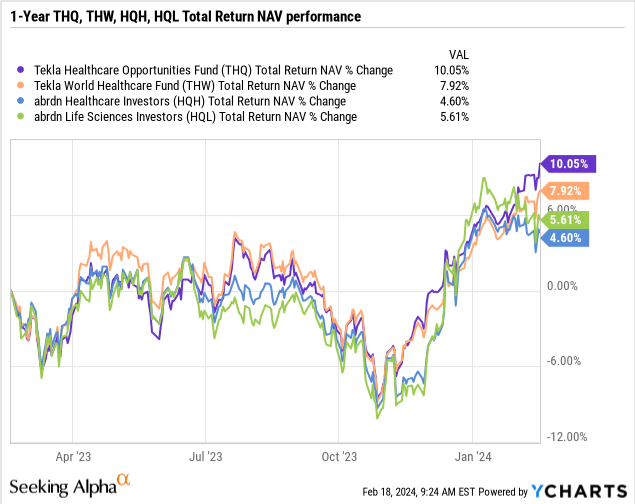

And if you look at a 1-year NAV total return comparison, once again, THQ is far ahead of the others:

Certainly, the fact that THQ is more pharmaceutical and healthcare equipment/services stock weighted than biotechnology and is more U.S. healthcare stock focused than global like THW, has helped THQ to a much better NAV performance over the years.

But shouldn’t that mean that THQ should be trading at a better valuation than the others, especially after this distribution increase? Before I get into that, however, let’s do a quick overview of THQ.

THQ is a 20.4% leveraged equity (77.7%) and fixed-income (15.7%) CEF that also uses a slight option-write strategy on individual stock positions. So, leverage helps the appreciation and income potential of the fund while an option-write strategy provides some defensiveness while also providing some income in case of a flat to down market environment.

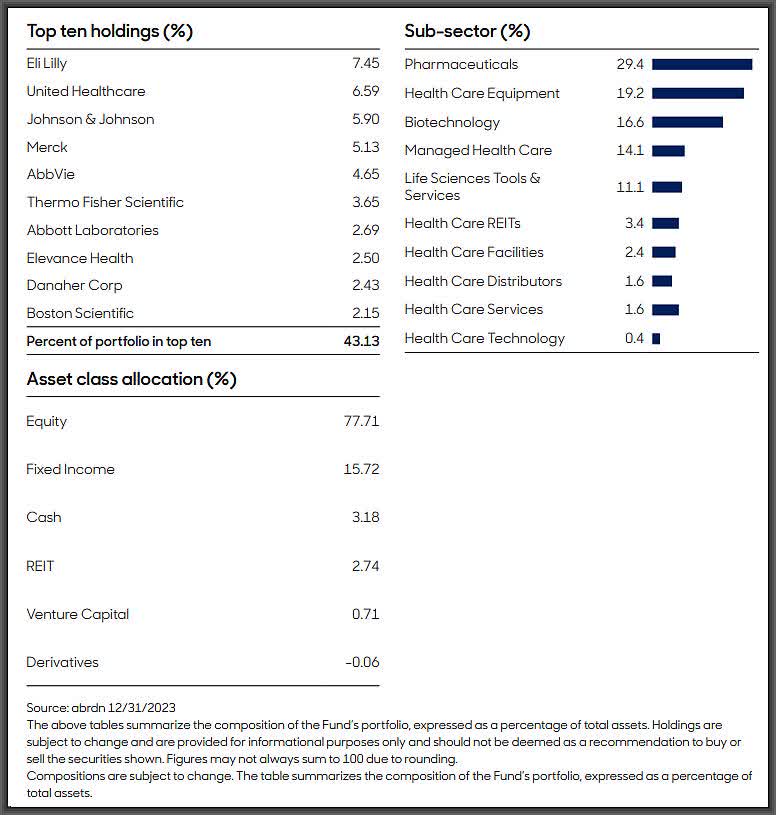

Here are the highlights of THQ’s Fact Sheet as of 12/31/2023 (hit link to see the entire Fact Sheet):

Aberdeen

Why THQ Should Be Trading At A Better Valuation Than Its Real Comparable, BME

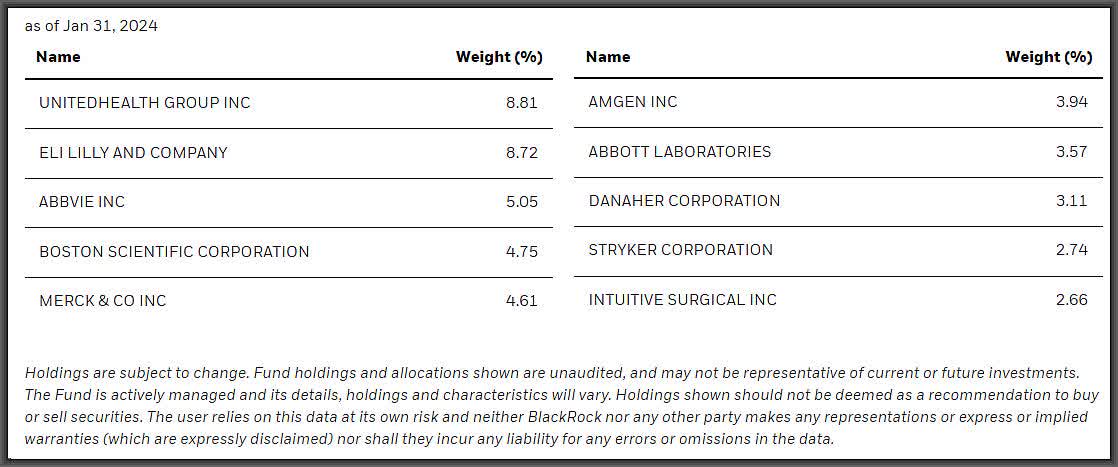

If you want to know THQ’s closest comparable from a holdings standpoint, it would be the BlackRock Health Sciences Trust (BME), $42.28 closing market price.

BME is a CEF that trades at a -4.3% discount and offers only a +6.1% current market yield. But more importantly, BME and THQ have very similar portfolios because they both are essentially healthcare index funds with 90%+ exposure to U.S. healthcare stocks (THW, for example, is only 64% U.S. stocks).

And you can see above for THQ and below for BME, both funds have 8 of the same top 10 holdings:

BlackRock

But there are some notable differences that should impact NAV performance. First, BME does not use a leveraged strategy and instead, employs a much higher percentage of option writing (33.8%) against its individual stock holdings.

THQ, on the other hand, uses a more aggressive leveraged strategy but also has a higher exposure to fixed-income securities, mostly non-convertible notes. And as I said above, THQ uses a limited amount of option writing.

What does this all mean? Well, this should give an advantage to THQ’s NAV performance over BME’s in a bull market for healthcare, pharmaceutical and biotechnology stocks, though THQ’s fixed-income exposure will have some interest rate sensitivity too.

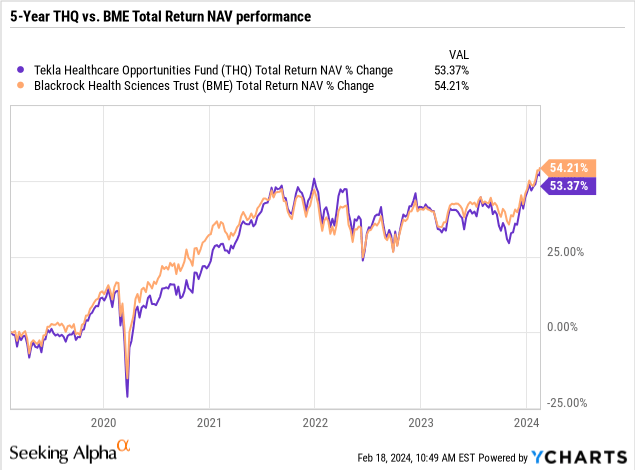

And if you look at the two funds total return NAV performances over the last 5-years, they are virtually the same, which probably reflects the fact that healthcare stocks have had an up and down history over the last 5-years, up during COVID-19 and flat to down over the last couple years:

Note: Total return NAV performance is the true portfolio performance comparison whereas in CEFs, MKT price performance can be subject to shareholder whims and emotions in the demand & supply of shares

And as of last Friday, February 16th, here is where the 2-funds stand YTD:

Capital Income Managment, LLC

And going back over the years, here is how the two funds have performed at total return NAV and total return MKT price each year going back to 2015 (THQ went public in 2014):

Capital Income Management, LLC

Note: Notice how much better THQ performs in a strong up year for healthcare stocks like in 2021.

Does THQ Now Deserve The Same Valuation As BME Or Even THW?

With BME trading at a -4.3% discount and a +6.1% current market yield while THW is at a +2.3% premium and an +11.1% current market yield, where should THQ trade now that it’s increased its distribution by 60%?

Well, certainly not the -12.7% discount since that is dramatically wider than BME’s discount while offering almost twice the market yield of BME now.

Thus, I would argue that THQ, which is essentially a more aggressive version of BME anyway with its leveraged appreciation and income strategy, should trade at least at a similar valuation as BME and probably closer to THW’s valuation.

But even if THQ traded at -4.3% discount, that would put THQ’s market price at roughly $21.25, assuming THQ’s current $22.26 NAV stays the same. And if that happens, then that would be a +9.3% gain in THQ’s market price from its closing $19.44 market price (not including distributions along the way).

Doesn’t that seem more fair? Heck, even at a $21.25 market price, THQ’s market yield would still be +10.2%, still much higher than BME’s current +6.1% market yield.

So, why did shareholders sell off THQ last week after opening over $20 on Monday?

Frankly, I think it has to do with: a) Shareholders being conditioned for a relatively flat healthcare stock performances over the last couple years; and b) resistance levels for THQ around the $19.50 to $20.00 range.

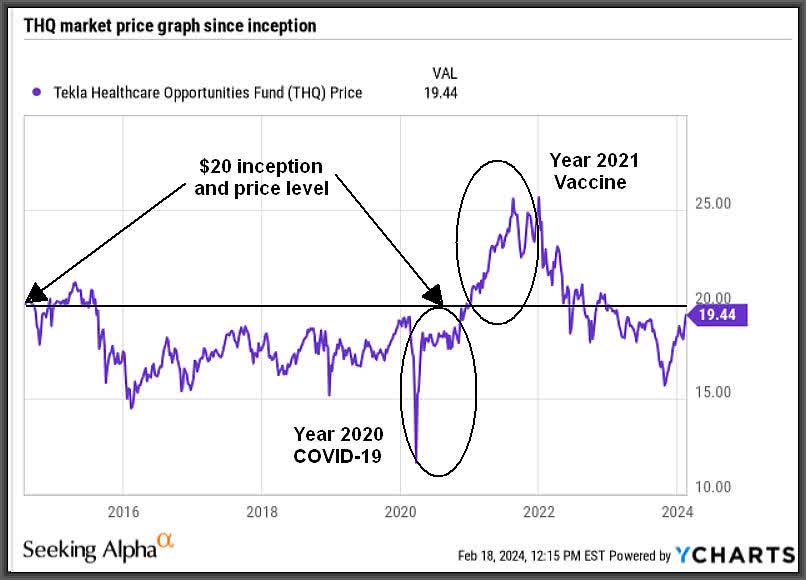

If you graph THQ’s market price (not NAV this time) since inception in 2014, THQ has traded significantly above $20/share only once, and that was in 2021 when healthcare and biotechnology stocks took off after vaccines for COVID-19 became available. In fact, healthcare stocks actually started moving up in 2020 but THQ’s market price still didn’t eclipse the $20/share level until 2021 came around:

Y-Charts

$20 also happens to be THQ’s inception price, though who knows how many original shareholders are left from 2014. And even though this does not take into account THQ’s monthly distributions of $0.1125/share over the years, can you see how $19.50 to $20.00 would have been a tough price level to break?

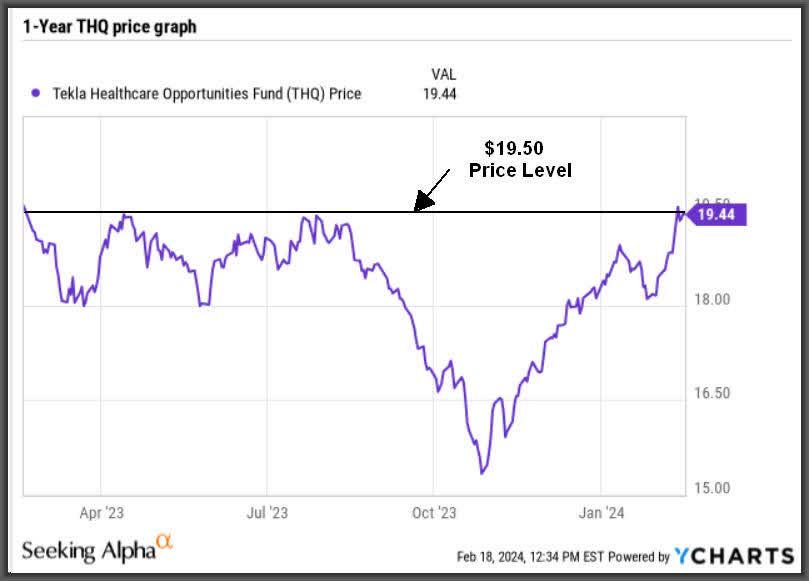

And if you look at a 1-year market price graph, you can definitely see where the $19.50/share price level was tough to break through, let alone $20.00/share:

Y-Charts

Which is why I believe shareholders of THQ are not seeing the forest through the proverbial $19.50 to $20.00 trees. In fact, I believe it’s only a matter of time before THQ breaks-out above $20/share and moves even higher after this news.

I mean, would you sell now? I sure wouldn’t, and I have been telling my subscribers since December, even before the distribution increase, that THQ was attractive if the healthcare sector saw a resurgence this year after two underperformance years.

And, so far, that is exactly what is happening, even if we are still in the early stages of a recovery.

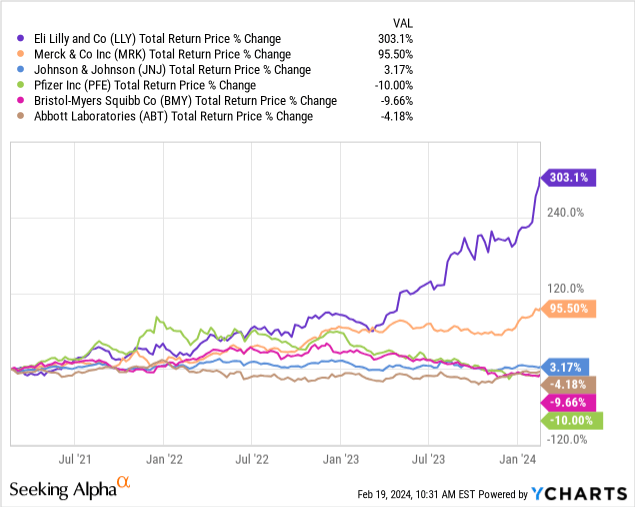

Consider Eli Lilly (LLY), $782.06 closing market price, +3.2%, which is THQ’s top position and a top 10 position for THW and HQH as well, though in lower weightings. Eli Lilly is up +34.4% just YTD and is up +140% over the past year. There’s even talk that LLY may be the next $1 trillion market cap member among all stocks.

And though LLY is clearly the superstar among the U.S.-based pharmaceutical giants, don’t you think this is going to put a lot of pressure on these other pharmaceutical companies to perform better since they can’t really blame the healthcare industry or the regulatory environment if LLY is doing this well.

Here is a 3-year total return price performance of LLY, Merck (MRK), Johnson & Johnson (JNJ), Pfizer (PFE), Bristol-Myers (BMY), and Abbott Labs (ABT):

And though biotechnology stocks have also gotten off to a slow start this year, we don’t need another COVID-19 scare to see this sector perform better. Already, new drugs directed at weight-loss are being developed after it was realized that Novo Nordisk’s (NVO) drug Ozempic, which was developed to help manage type 2 diabetes, proved to be an effective appetite suppressant as well.

Think obesity and diabetes isn’t a huge market? NVO is another company that is showing technology stock like performances, up +77.4% over the past year.

These companies are showing that healthcare is back in favor and that should also help attract big money to who might be next in line for a break-through drug or in the case of biotechnology stocks, who might be bought out.

This is a big reason why I endorsed THQ late last year and even made the abrdn Healthcare Investors fund, $17.41 closing market price, one of my Top Picks for 2024.

HQH is the former Hambrecht & Quist biotechnology fund that debuted back in 1987 and made its name by being an early investor in Genentech before it took off. Note: Genentech was taken over by Roche in 2009.

I remember this period well, since I was a financial advisor with Smith Barney and then Morgan Stanley in San Francisco from 1994 until 2004, during a time in which Hambrecht & Quist and Genentech were big names in the SF Bay Area. In any event, that’s where HQH, and later HQL, got their ticker symbols from (Hambrecht & Quist).

With Aberdeen now taking over the helm of the former Tekla healthcare funds, I think it’s important to appreciate the long history of these funds, especially HQH and HQL. In the Press Release from October 27th, Aberdeen makes a point to say:

The Funds will continue to be managed in accordance with their existing investment objectives and strategies, by the same team of Boston-based investment professionals pursuing the same investment philosophy and employing the same investment process that has served the Funds well through the years.

To me, that’s good stewardship, and I find it interesting that Aberdeen took over management of THQ, THW, HQH and HQL at the EXACT bottom of the markets on October 27th of last year. That certainly gives me more confidence that they saw the funds as an undervalued opportunity than if they took over the funds at a high-water mark.

So, Aberdeen is doing what they can to bring back confidence to current shareholders by increasing HQH’s and HQL’s distributions by +25% and THQ’s distribution by +60%. And if that doesn’t also bring in new investors, I don’t know what will.

Note: The 25% distribution increase for HQH and HQL is actually an increase of their NAV distribution policy from 8% to 10% annualized. So whereas THQ’s +60% increase is set at $0.18/share for the foreseeable future, HGH’s and HQL’s can vary quarter to quarter based on a rolling NAV value

ALL of the funds go ex-dividend at their higher distributions (except THW) next Wednesday, February 21st.

Here is the Press Release from February 9th:

Aberdeen

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")