Liudmila Chernetska/iStock via Getty Images

Investment Rundown

The stock performance for Tennant Company (NYSE:TNC) has been on a strong move over the last 12 months outperforming the broader markets, being up 33%. TNC is included in the industrial sector and more specifically the industrial machinery & supplies components industry. The product portfolio remains well diversified for the business and margins are at the highest levels in the last few years even as the interest rates have rapidly risen in the US. I think this underscores some of the demand that TNC still experiences and its strong market position has helped it hedge against what for others has been a very turbulent year.

The company is valued quite low right now and I think that has to do with the growth outlook for the business. I don’t see anything that would put TNC in a spot where it can deliver strong double-digit growth YoY, it’s just not that kind of company. I would view TNC more as a resilient dividend payer that could make up a smaller portion of a portfolio and provide some stability when markets are volatile. Because of this, the slightly low valuation makes a lot of sense in my opinion, and I would need an even lower one to make a buy case here. I would say it’s fairly valued based on what I would think is around 4 – 5% CAGR for the revenues. These projections lead me to rate the company a hold for now, with the possibility of an upgrade should the price reach an area where I think there is an ample amount of value to be had.

Company Segments

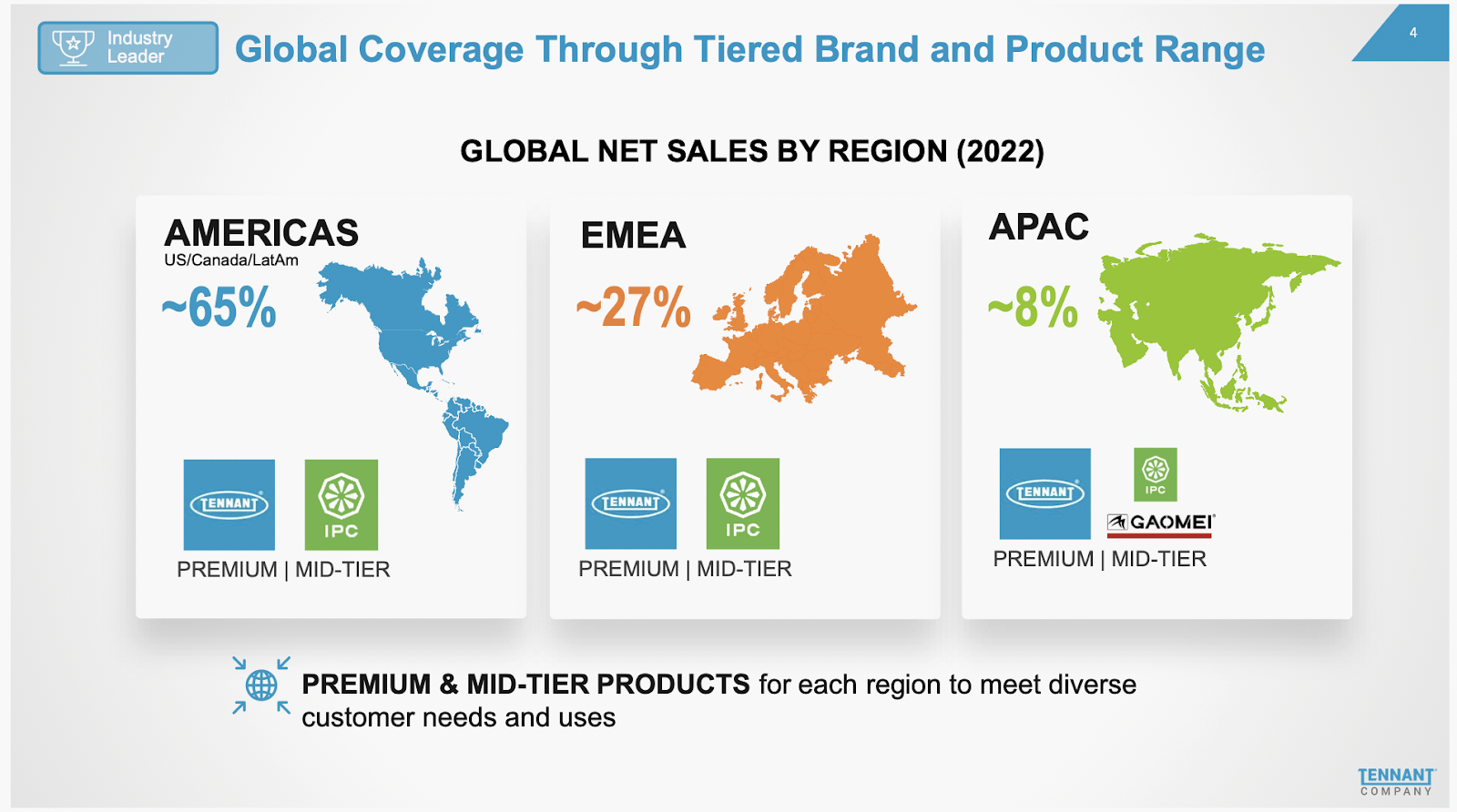

TNC operates in the floor cleaning equipment market, with a global presence spanning the Americas, Europe, the Middle East, Africa, and the Asia Pacific. The company’s diverse product range includes floor maintenance and cleaning equipment, innovative detergent-free and sustainable cleaning technologies, and a variety of aftermarket parts and consumables.

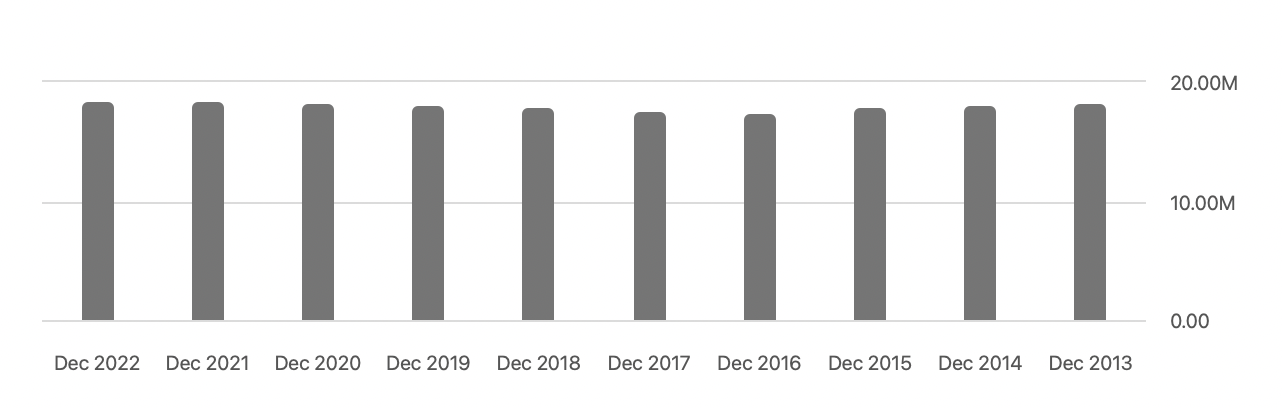

Company Sales (Investor Presentation)

TNC offers comprehensive equipment maintenance and repair services, along with asset management solutions. To further support its clientele, the company provides a range of business solutions, including flexible financing, rental, and leasing options, as well as advanced machine-to-machine asset management solutions. In terms of how this diversified approach has netted the company over the years the compounded 5.09% growth rate for the top line I think is very strong. The company had set out some girth targets with a 5-year plan, which they have managed to achieve a year early. Some of these targets included a 3% annual revenue growth rate EBITDA percentage of 15%. I think that these achievements have been a factor in the stock price performing so well over the past 12 months.

Earnings Highlights

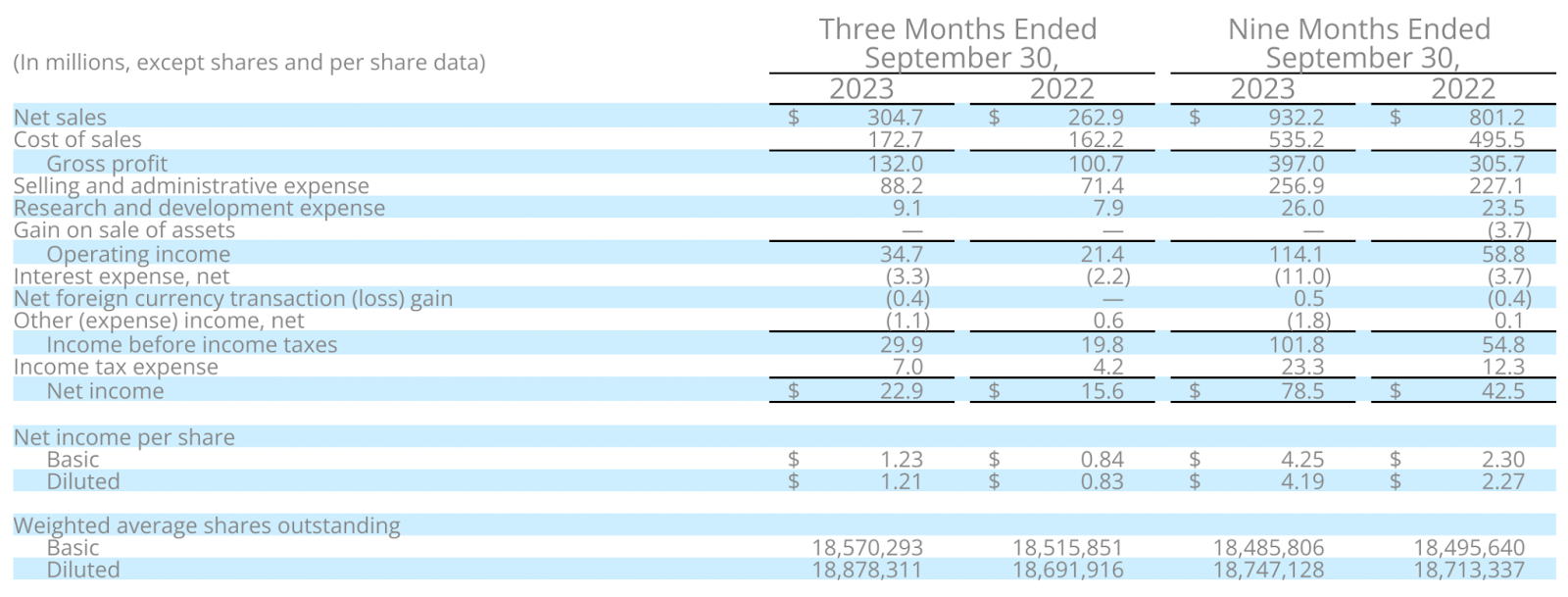

Income Statement (Earnings Report)

The most recent report by TNC was released on October 31 2023 and we seem to be a little over a month out from the next report which would provide the full-year results of 2023 by TNC. As far as the income statement goes, it’s visible that TNC managed to grow quite well YoY. The revenues reached over $300 million which is just a slight decline from the record levels seen in the previous quarter of $321 million. I do think the revenues will stabilize somewhat and more growth instead come from acquisitions. The last major acquisition by the company was some years ago though, when they purchased the stake Ambienta had in IPC Group valued at $353 million in total. This pushed up the debt levels by almost 10 fold but it has since declined by over $100 million.

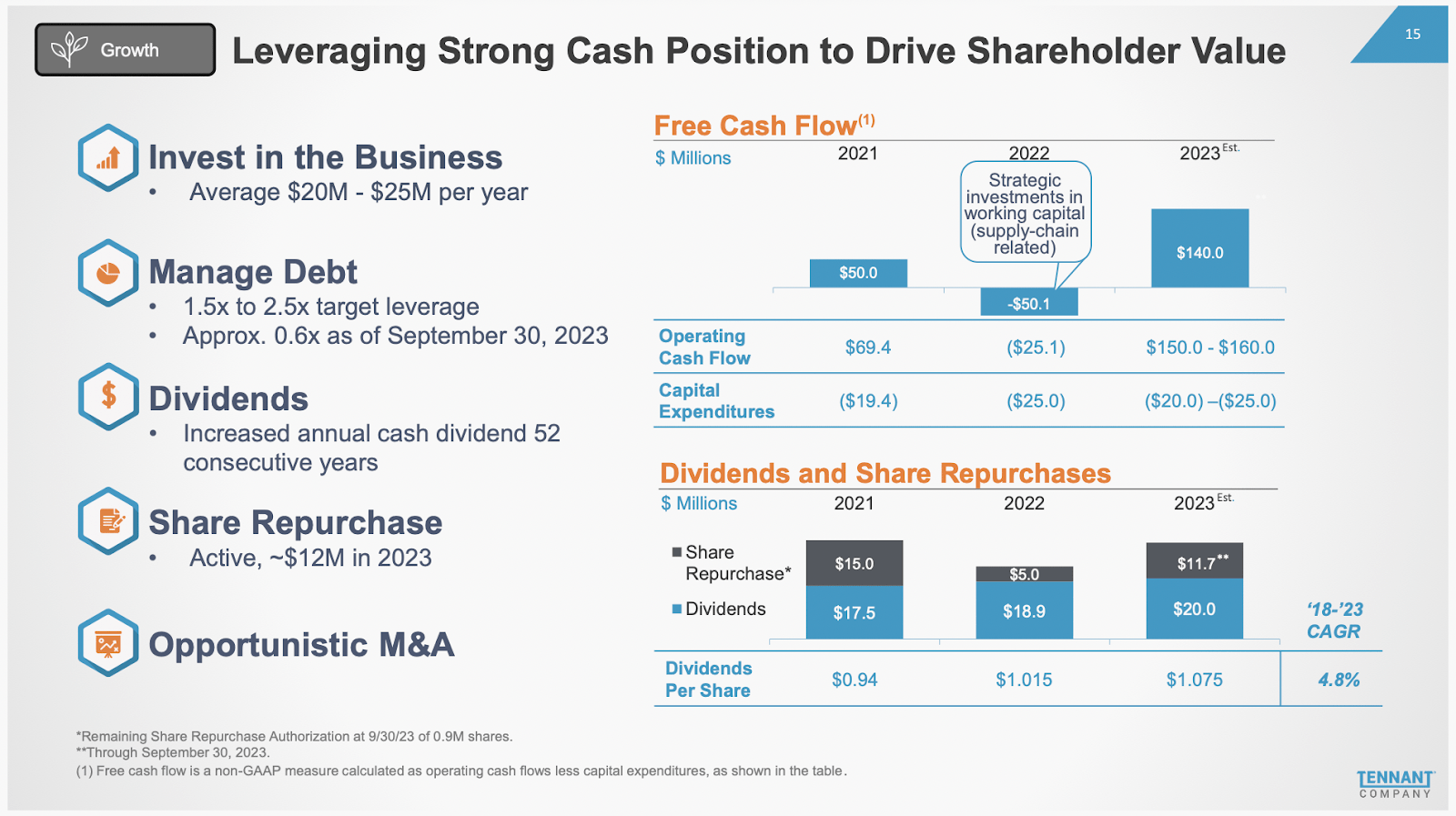

Cash Position (Investor Presentation)

The company makes it quite clear that it intends to have a lower level of leverage to properly manage market climates and challenges. The target debt leverage is 1.5 to 2.4 which right now is at 0.6. This means that the company is in a great position to make further acquisitions and still stay within this leverage range. As far as catalysts that I am looking for, this would certainly be one of them. The growth of the business organically is not that high I think. The global cleaning products for the household for example are estimated to grow around 6.5% in the next 7 years in total. That is not a very high growth market in my opinion, but I do think TNC could do a good job in reflecting that CAGR in their top line in the same time frame, given the market position they have acquired so far.

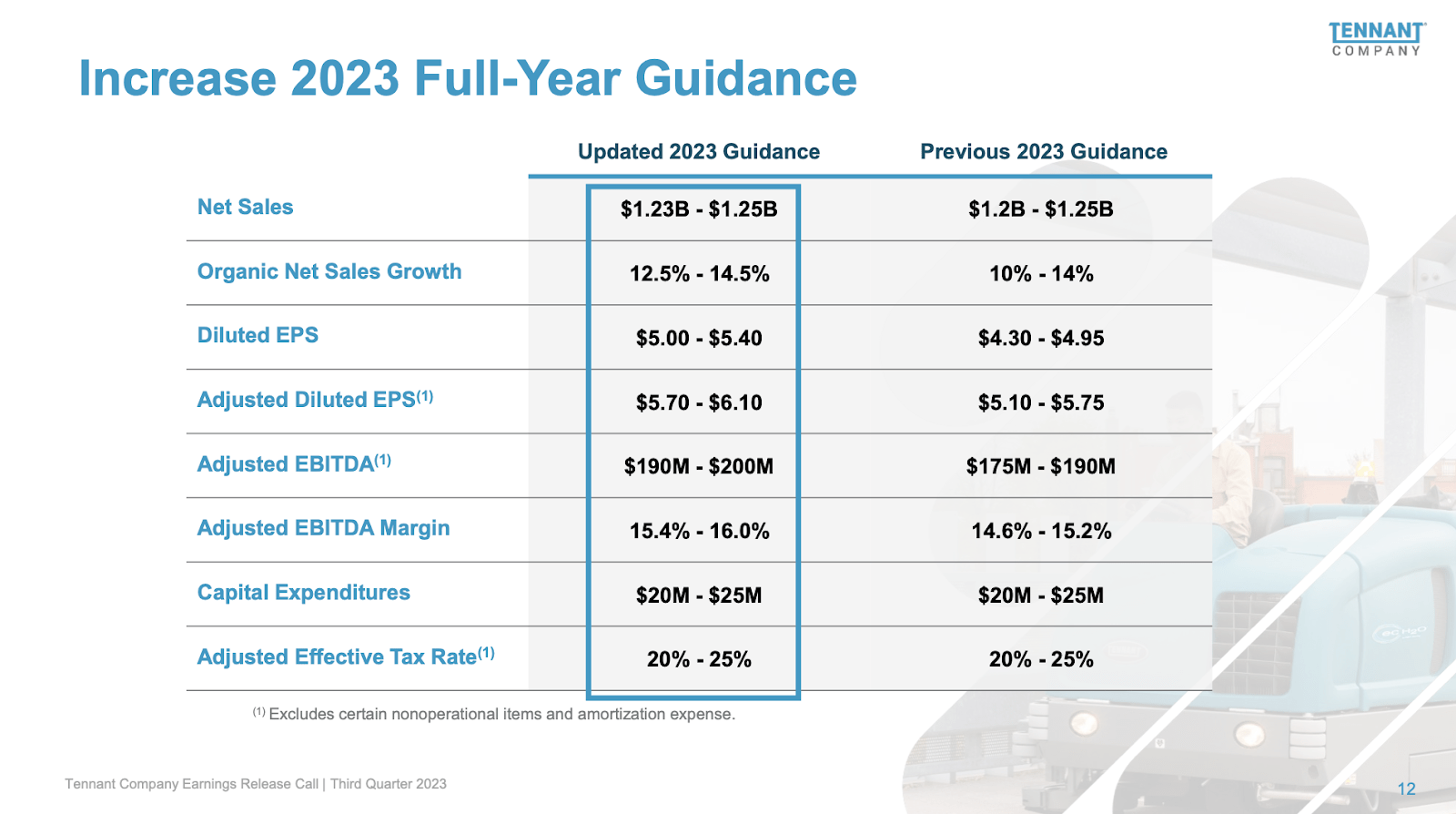

2023 Guidance (Investor Presentation)

The guidance for 2023 is for sales to reach between $1.23 – $1.25 billion, which is a very tight range but also underscores the relatively steady and reliable demand that TNC has. This would lead to a 12.5% – 14.5% YoY sales growth. If the margins remain strong it would result in $5.4 for the EPS and put TNC at an FWD multiple of 16.6. I have made it clear that I don’t think the current valuation is that appealing to buy at, I would prefer something in the range of 13 -14 instead, because of the poor growth outlook that still exists with TNC. It’s not operating in a market with a lot of disruption and catalysts that fuel growth, which I have to stress again isn’t something negative necessarily. I think that TNC will produce EPS growth of around 5 – 6% over the next 7 years, which would be smaller than the cleaning products market. That level of growth is not worth the current multiple and with m preferred one puts the company at a 12-month price target of $77 instead. This means a drop of 16% is necessary before I get in, but given the rapid rise in the stock price over the last 12 months, this isn’t so unlikely if the markets see a broader sell-off.

Risks

One of the notable risks associated with TNC is the potential for share dilution, a trend observed in the company’s recent history. While the current level of dilution isn’t alarmingly high, it remains an important point of consideration. Should the company maintain high rates of dilution, coupled with a potential decline in demand, there might be a need for further share dilution to manage and repay maturing debts.

Share Dilution (Seeking Alpha)

Another risk that is put on the company is elevated material costs. The company manufactures a variety of products and if the revenues can’t climb faster than the cost of revenues there will be pressure on the margins of the business. In the last 12 months, the improvements have gone in the right direction with revenues growing nearly 12% and the cost of revenues growing roughly 5% YoY instead. One of my worries is that the ongoing conflicts in the Red Sea are going to disrupt the shipments that TNC has. It’s a global company with 10% of sales in Asia. Deliveries to that region all go through the Red Sea. We have already seen the shipping rates increase quite rapidly in the past months because of this escalation, but should they stay persistent I am worried about the bottom line for TNC. It could result in the share price dropping and leaving us with a buying opportunity, which ultimately would be a positive perhaps.

Final Words

I have not covered TNC before but doing so now has led me to a company that I think can produce quite steady results over the long term. It operates in a very stable market where cleaning products and equipment are always going to be in demand. The company has seen margins rise quite rapidly over the past few years which might have given way to the stock price rising just as fast, but in my mind, there isn’t enough incentive here with the stock to make for a just yet. My 12-month target is $77, but I would still argue holding onto shares makes sense given the dividend and stability of the business. Short-term fluctuations in the stock price could open up a buying opportunity, but for the moment the stock will be a hold.

Q2 2024 Earnings Call Transcript")