lcva2

We have previously presented two notes on Teleperformance SE (OTCPK:TLPFF), highlighting an attractive risk-reward profile underpinned by solid fundamentals. The stock is flat since our initiation as the company has navigated a challenging economic backdrop, and guidance has been revised downwards, disappointing investors. In this note we will discuss Q3 results, the agreement with UNI Global Union, and the departure of Majorel’s CEO; update our valuation and investment recommendation; and analyze risks.

Q3 results

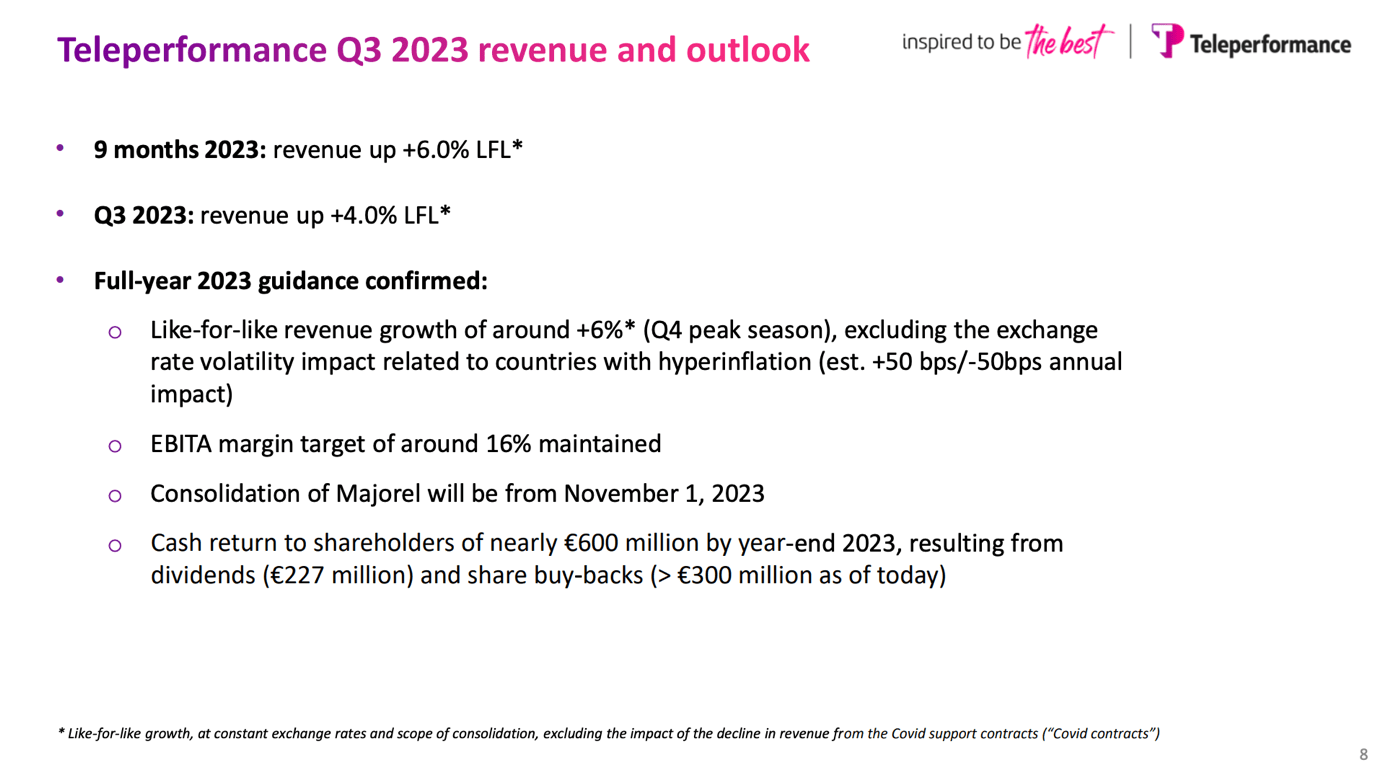

Teleperformance reported Q3 results below consensus expectations, with like-for-like sales growth coming in at 3.1%. Like its competitors, Teleperformance is facing a significant slowdown in call center services, particularly in Latin America and North America. Meanwhile, specialized services grew by over 16% like-for-like as passenger traffic recovery benefited LLS and TLS. The group is guiding for 6% like-for-like growth in FY2023. Moreover, the firm announced it is holding a Capital Markets Day in Q2 2024. While the results point to several weaknesses, we believe the negative news has already been priced in.

Teleperformance Q3 Results Presentation

UNI Global Agreement

In December, UNI Global Union held a call to provide updates on the deal signed with Teleperformance in 2022. The conference call was open to investors and analysts. UNI confirmed Teleperformance’s progress, particularly in Columbia, where the firm had previously faced issues with unions and the government. TEP is the only company in the sector that has signed a deal with UNI, demonstrating leadership in terms of worker issues. We view this positively as it indicates Teleperformance’s commitment to mitigating similar dispute risks in the future.

Industry outlook

The sector has faced several challenges. The impressive organic growth and strong pricing power driven by digital clients during the Covid period is now over. Demand is softer as clients are implementing cost-cutting measures and increasing automation. Teleperformance’s competitors, including Concentrix, TaskUs, and Telus have reduced their guidances and refrained from providing 2024 targets due to uncertainty while emphasizing the tougher environment. While the environment is certainly difficult, we believe that the current weakness is merely cyclical and not indicative of deteriorating fundamental long-term trends. Moreover, this is already priced into Teleperformance’s share price.

Majorel update

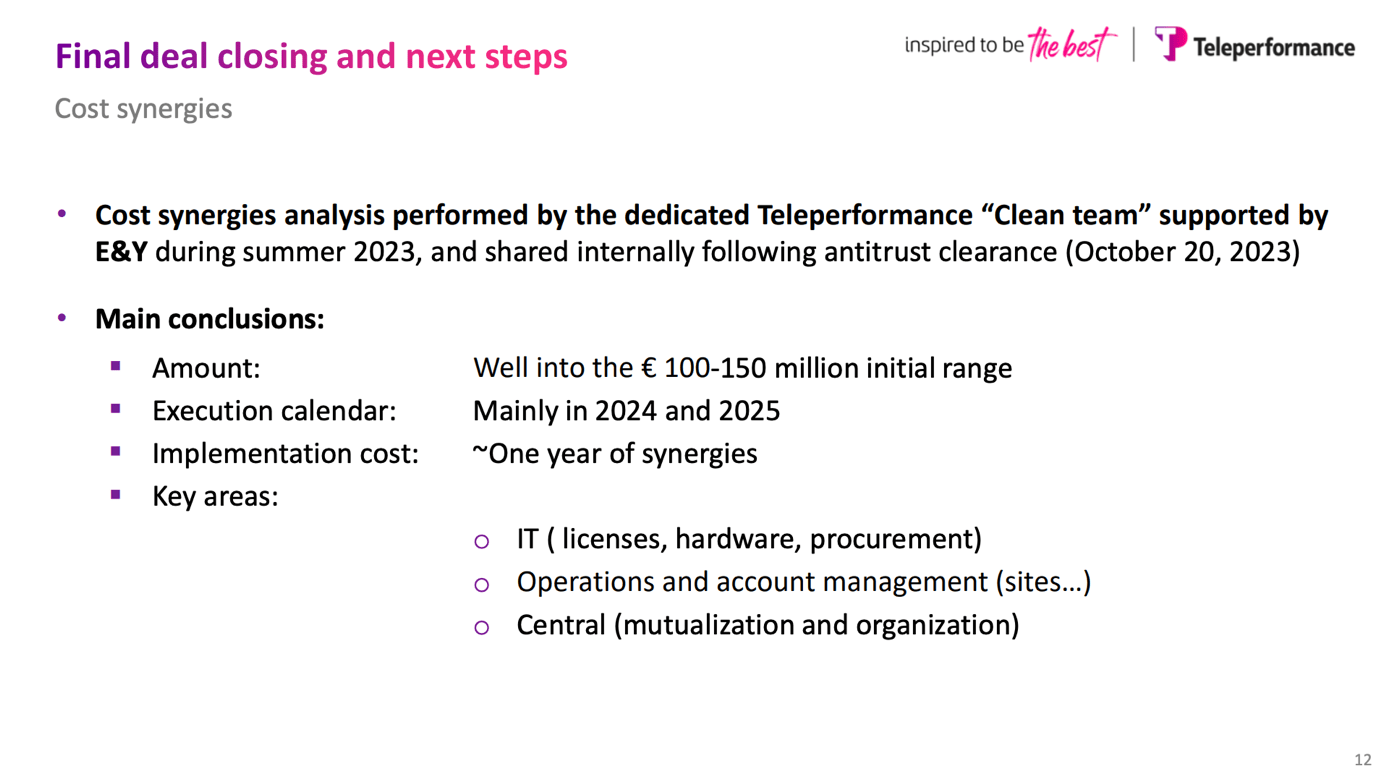

The acquisition of Majorel is surely transformative. It is the most important acquisition TEP has made over the last few years. We have analyzed it in our previous notes and highlighted our constructive view. However, big transformative acquisitions come with integration risks. The unexpected departure of Mr. Mackenbrock, Majorel’s ex-CEO, and later head of EMEA and APAC regions, raises additional questions among investors. It is important to note that EMEA is the region where most of Majorel’s business activities lie and where most synergies should be extracted. On the other hand, we would also like to note that the CEO of Saham Group, the former anchor shareholder of Majorel, now owning more than 3.5% of TEP’s shares, will be joining the board of directors in March.

The CEO of Teleperformance went on to reassure investors and expressed his confidence in achieving the higher end of its stated objective. The successful integration of Majorel should have a significant EBITDA margin impact of >1% of revenue or approximately €100-150 million of synergies over the medium term. We were surprised by the departure but remain reassured by TEP’s management. We would like to point out Teleperformance’s successful M&A track record. The successful integration of Majorel and achievement of synergy targets is a major catalyst for Teleperformance going forward.

Teleperformance Q3 Results Presentation

Updated valuation and investment recommendation

We value Teleperformance using PE ratios and FCF yields. We estimate €11.2 billion of revenue, €2.4 billion of EBITDA, and €950 million of net profit in FY2025. Moreover, we forecast €1.2 billion of Free Cash Flow in FY2025. Our estimates are in line with analyst consensus forecasts. This implies a valuation of merely 9x forward EPS. We would like to underline that the stock trades at nearly half of its median historical multiple. Despite recent woes, we remain convinced that the current valuation does not reflect Teleperformance’s true value.

TEP’s return on capital remains well above its cost of capital, cash generation remains high, and EPS growth remains well above GDP growth and CAC40 earnings growth. We reiterate our 13x forward EPS valuation, arriving at a target price of €191 per share, implying an upside of 38%. We would like to note that we do not apply a quality valuation premium similar to the wider quality business services peer group, and we still value Teleperformance at a 30% discount to its median PE over the last 10 years.

Combined with a low single-digit dividend yield, we forecast more than 20% IRR over two years. We believe that the successful integration of Majorel, an improved business momentum in 2024, and more clarification over AI disintermediation risks will be the main catalysts for Teleperformance’s rerating.

Risks

Downside risks include but are not limited to a worse-than-expected economic environment, a more challenging industry outlook, disruption from generative AI, higher-than-expected competition, wage inflation leading to margin compression, unionization of workers, stricter labor laws, negative news flow around business practices, misallocation of capital including value destructive M&A, failure to integrate Majorel and obtain synergies, legal risk, succession risk as CEO and founder eventually steps down, etc.

Conclusion

We believe the worst is over and Teleperformance should rerate. We find the risk reward attractive at the current valuation, and we maintain our Buy rating on Teleperformance.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")