Ethan Miller/Getty Images Entertainment

Almost a year has passed since broadcast company TEGNA Inc. (NYSE:TGNA) terminated its $8.6 billion deal with hedge fund group, Standard General over regulatory bottlenecks. While the stock has dropped 6.04% (YoY), the company has announced a robust capital allocation strategy to boost performance in 2024. This includes a $800 million share repurchase program and a 20% increase in dividends. As of February 2024, TEGNA stated that it had already repurchased 22% of its shares.

Thesis

TEGNA has renewed most of its contractual obligations in 2024 focusing on aspects such as professional sports, news, weather, and related advertisements. In partnership with Comscore, TEGNA will gain expanded coverage through qualitative content generation based on data progression. Further, apart from owning about 64 television stations in more than 50 markets, TEGNA’s Premion- a leader in digital advertising acquired Octillion Media to advance its organic growth through a premium connected TV (CTV) experience. The stock is also poised to gain due to the upcoming US elections and related political advertisements in the year.

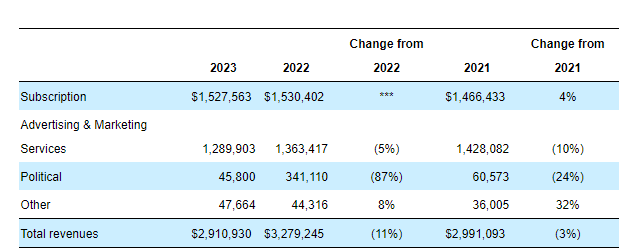

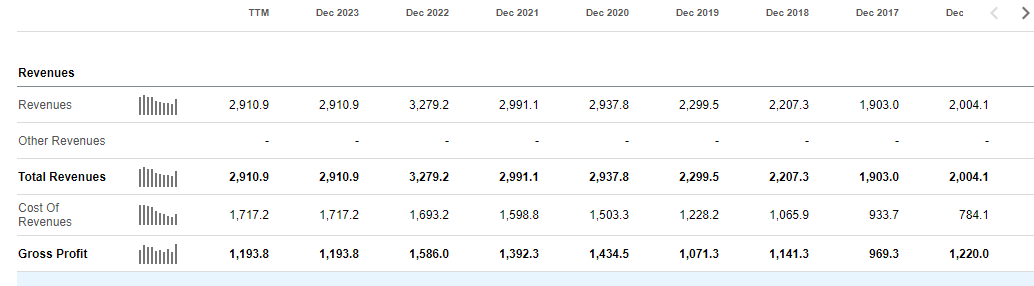

FY 2023 was not a stellar year for TEGNA after its revenues declined 11% (YoY) to $2.91 billion from a high of $3.3 billion in FY 2022. The decline was partly attributed to low returns from both advertising and marketing services (AMS) at -5% (YoY) and the political segments at 87% (YoY).

TEGNA 2023 10-K

TEGNA’s core business to date remains linear television, where it has the largest audience. In this space, TEGNA faces the pressure of finding the right content that is suitable for consumers. Over the years it has also had to ramp up its digital viewership including media websites, over-the-top (OTT) applications, and even mobile devices. As of 2023, TEGNA explained that its digital outlets targeted an audience of about 80 million monthly visitors.

In this regard, the company announced its partnership with media analytics firm Comscore, which will allow it to measure its platform audience. I believe this multi-year agreement will consider audience behavior across all platforms both TV and mobile. TEGNA, widely known for its coverage of local community reports will use the in-house analytics from Comscore in the delivery of content. Such data is essential in understanding a practical monetization framework or a subscription model that best suits the viewers. In essence, it involves matching content expected for release by TEGNA with consumers. I also think this deal with Comscore could not have come at a better time, especially with the ever-changing demographics and habits of consumers.

So basically, TEGNA is looking to revolutionize 3 main segments: content generation through personalization of local demographics, enhancing customer engagement- probably at the household level and improving its sales/ marketing.

Over the past 10 years, TEGNA has acquired at least 40 TV stations. In 2019, it bought 11 TV stations from Nexstar Media Group (NXST) for $740 million (in cash) strengthening its portfolio by becoming a pure-play broadcaster. Over the last three years, it has acquired 15 TV stations, at least two radio stations and the Locked On Podcast network- a sports podcast. There has been a positive impact of these new acquisitions on TEGNA’s revenue which has grown 26.59% since the year ending December 2019.

Seeking Alpha

Expanded contractual obligations into 2024

At the beginning of 2024, TEGNA announced the renewal of a multi-year deal with NBC covering 20 markets in the US. The deal covers more than 21 million households which it stated was about 17% of all US TV households. While making the announcement, TEGNA’s CEO, Dave Lougee stated,

As the largest NBC affiliate group among independent station groups, we are proud of our longstanding partnership that enables us to serve local communities. This new multi-year agreement allows our stations to continue providing consumers and advertisers with premium network content such as TODAY, Sunday Night Football, and this summer’s Paris Olympic Games alongside our award-winning local news, weather, and sports.”

NBC is a subsidiary network of Comcast (CMCSA) and is known for its brands of film and TV stations. Unlike TEGNA which is largely local/ domestic, NBC is a distribution network for both domestic and global networks. NBC also owns video streaming networks such as Peacock which since its launch in 2020 has shifted viewing from broadcasts or cables to the Internet and amassed over 30 million (active) subscribers.

TEGNA also announced the renewal of its “multi-year distribution agreement with DirecTV” to cover all its stations and markets. This agreement ratified in January 2024 returned all TEGNA’s stations/ programming to customers of “DirecTV, DirecTV Stream, and U-verse.” This agreement reached at in Q1 2024 ended a 6-week long blackout on fans of sports (especially NFL), late-night TV shows, and other local news programs in major states across the US. There was an impasse as to what DirecTV customers were to pay. In its Q4 2023 transcript, TEGNA admitted that a part of its reduced revenue was attributed to the blackout by DirecTV. I expect revenues into 2025 to increase as TEGNA continues to reap from its renewed relationships.

The Premion Factor

TEGNA owns Premion an advertising company in the US that offers premium Connected TV experience and over-the-top advertising. Over the years, Premion has continued to increase TEGNA’s market share in the digital advertising space. Advertising and marketing accounted for the second-highest revenue source for TEGNA in FY 2023 after subscription and I believe Premion played a role in gaining this revenue share. At the beginning of February 2024, Premion announced that it had acquired Octillion Media, a demand-side platform (DSP) that would help grow local advertisements.

The potential growth in Premion’s revenue from this deal may come from new clients in the advertising verticals that Premion does not control. For example, Octillion serves in the quick-serve restaurant (QSR) business, automotive, and mattress brand retailing, segments in which Premion may not be prominently involved. I believe it is about bringing in net new advertisements that will in the end grow income.

In 2017, Premion ” announced its partnership with blockchain-based ad-tech solutions provider, MadHive.” At the time, MadHive was to help it scale the OTT advertisement space and improve its ad tech supply. MadHive is an external demand-side platform and bringing in Octillion will enable Premion to have its own DSP with a particular set of tools, innovative inventory, and even a customer base. I am also looking at Premion charging a fee per every ad tech used in an advert campaign (with Octillion in its wing).

Another angle to consider is the aspect of innovation and technological development which is the bedrock of advertisements. Premion will become attractive to other advertisers with Octillion, thereby increasing product diversification. This is an already-established entity with a particular set of measurement tools that will add color to TEGNA. Overall, Premion needs to do everything possible to increase its recognition among other media companies in the connected TV sphere since as we have seen, the DSP space has high competition.

Risk

Low cash

TEGNA’s cash balance as of Q4 2023 stood at $361.04 million against a debt level of $3.16 billion. However, the media advertisement space is highly leveraged since Comcast has $6.22 billion in cash against a total debt balance of $103.68 billion. Additionally, TEGNA’s free cash flow as of FY 2023 stands at $559.2 million since its cash generated from operations in 2023 stood at $587.2 million against a cash usage of $28.0 million in CapEx.

Competition from video streaming services

As a leader in linear television, TEGNA continues to face stiff competition from streaming networks such as Netflix, YouTube, and others such as Amazon Prime. Despite being founded in 2005 (while TEGNA was founded in 1906) YouTube’s revenue in the FY 2023 stood at $31.5 billion. Netflix’s revenue for FY 2023 stood at $33.7 billion while Amazon’s Prime was $40.2 billion. These streaming services have overtaken TEGNA due to the rapidly changing consumption space.

My view is that TEGNA should sell some of its assets whose total value stands at $7 billion and increase its stake in DirecTV. I believe most consumers may desire lower subscription fees and will take up the opportunity offered by TEGNA. We must also remember that Q4 2023 dealt a blow to TEGNA due to its standoff with DirecTV that led to a blackout.

Needs a high technological roll out

We have to appreciate that TEGNA controls at least 39% of all US TV households (as of 2023). It acquired 15 TV stations in the past 3 years alone and a total of 64 stations. While this is an incredible feat, it needs to expand its innovative technological rollout. It has to ramp up its digital space and improve content generation to increase its appeal to consumers. Additionally, with 2024 being an election year for the US, TEGNA will need to increase its political expenditure, especially in advertisements, and in-house gathering of voter registration data. However, this strategy will help market TEGNA’s stations from a political perspective. TEGNA’s revenue as of December 2020 grew 27.76% (YoY) to $2.94 billion against $2.3 billion realized in 2019.

Valuation

TEGNA’s forward P/E ratio stands at X4.58 against the industry average of 13.76, a difference of -66.70%. Additionally, TGNA’s forward EV/ EBITDA is 5.44 against the industry average of 7.87. It leaves off a difference of -30.90%. These metrics show TEGNA is undervalued and we may see an increase into 2025.

Bottom Line

TEGNA has renewed most of its contractual obligations into 2024 to grow its subscriber base and improve its advertisement networks. On the creation of shareholder value, TEGNA has increased its capital allocation towards the growth of its dividend and share repurchases. It has already purchased 22% as of February 2024 with more expected by H2 2024. TEGNA’s Premion is taking over the digital advertisement space with the acquisition of Octillion Media which seeks to grow the company’s DSP market share. TEGNA expects to increase its monetization metrics and subscriptions while matching content development with changing consumption habits. For these reasons, I propose a buy rating for the stock.

Q2 2024 Earnings Call Transcript")