Annabelle Chih/Getty Images News

The incumbent Democratic Progressive Party (DPP) won a third consecutive term in Taiwan over the weekend. However, the DPP received its lowest winning percentage since 2000 and has been pushed into a minority government, having lost its majority in the Legislative Yuan. The new President of Taiwan, Lai Ching-te, rose from the more aggressive pro-independence wing of the DPP but moderated his stance on relations with China through the campaign. We believe the outcome of the elections reduces the risk of escalation in tensions between China and Taiwan this year, with the next key watchpoint for investors the naming of the Legislative Speaker in February.

Relationship with China a key focus in the elections

For those that are less familiar with Taiwanese politics, a bit of background. Relations with China tend to be a big issue when it comes to Taiwanese elections. The DPP is in favor of independence from China. Historically, the opposition Kuomintang Party (KMT) has been in favor of closer relationships with China. This year, the Taiwan People’s Party (TPP) also ran on a policy platform that was more closely aligned with the KMT than the DPP.

In the lead-up to the election, both parties made some moves toward the center. For example, Lai Ching-te dampened down his stance from resist China to protect Taiwan to seek peace to protect Taiwan. Similarly, the KMT was less averse to military purchases than it had previously been, noting that increasing the defence capability was a viable strategy.

A closer look at the results

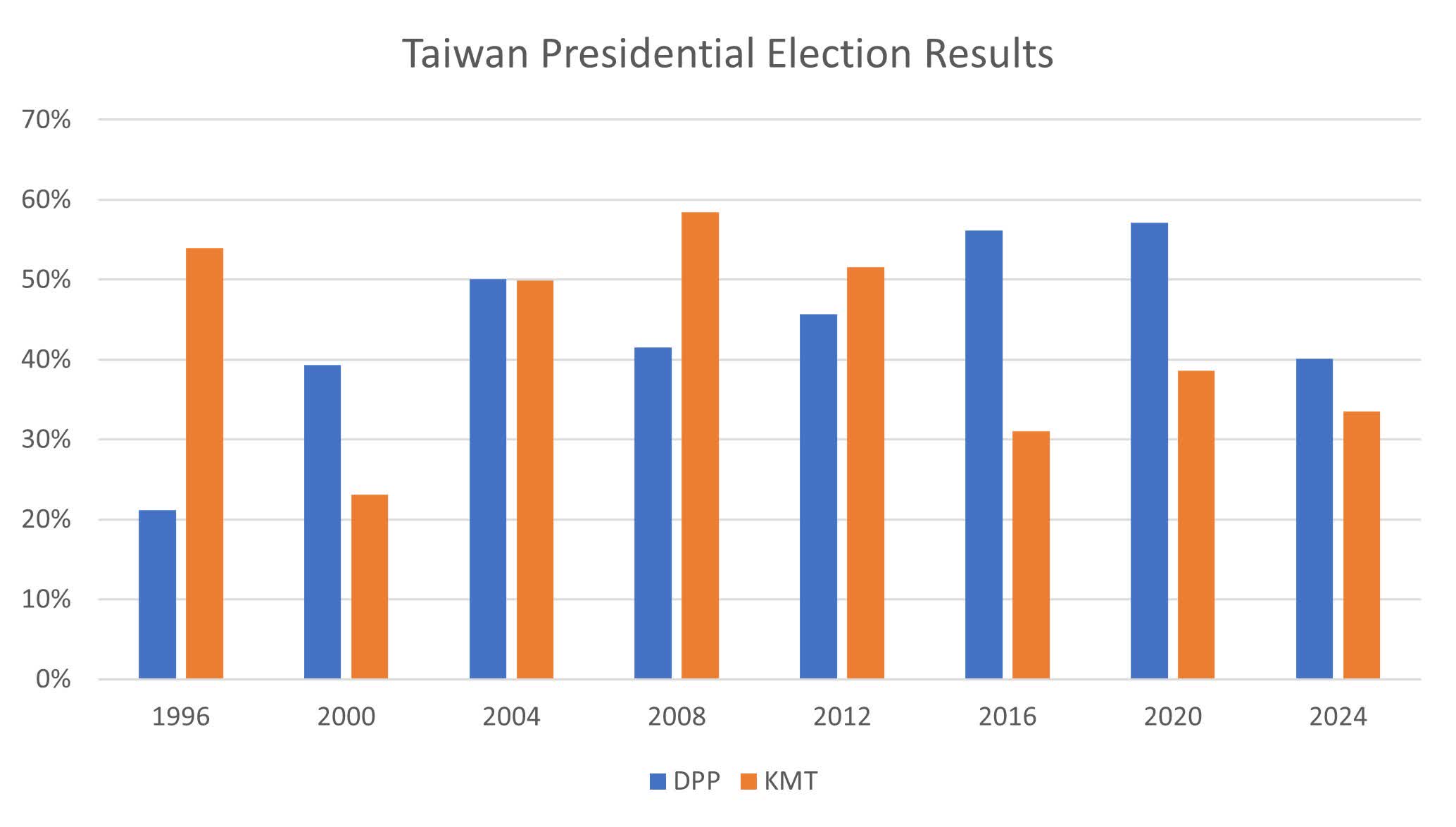

The chart below shows that the DPP’s vote share was the lowest since 2000, which as mentioned above is also the lowest winning percentage over that period. In the Legislative Yuan, the DPP has lost its majority – indeed, the KMT has one more seat than the DPP. This means it is going to be difficult for the DPP to pass new legislation without working closely with the TPP and the two independent parties. Effectively, this creates a scenario where a lot of compromises will have to be made between the parties for any new spending bill or government initiative. This should reduce the potential for dramatic shifts in policy, which tends to be good news for markets.

Source: Central Election Commission

China reacts to the results

It’s important to consider China’s reaction to this election. Coming into the elections, China had labeled Lai Ching-te as a “dangerous separatist” and indicated it would be displeased with his victory. Since the result, however, it appears that tensions between the two countries have lowered given the split parliament, with China noting that “the DPP can by no means represent mainstream opinions on the island.” We will be closely monitoring the commentary from Beijing, but for now, this appears encouraging.

The outlook for Taiwan-China tensions this year

Along with the results of the elections, there are a couple of other reasons to think that tensions are unlikely to escalate this year. First, the relationship between China and the U.S. is improving at the margin, and an increase in tensions with Taiwan would be a setback to this relationship – something China likely wants to avoid. Second, China is quite focused on the domestic economic growth situation after a lackluster 2023, and we expect this matter will command most of its attention.

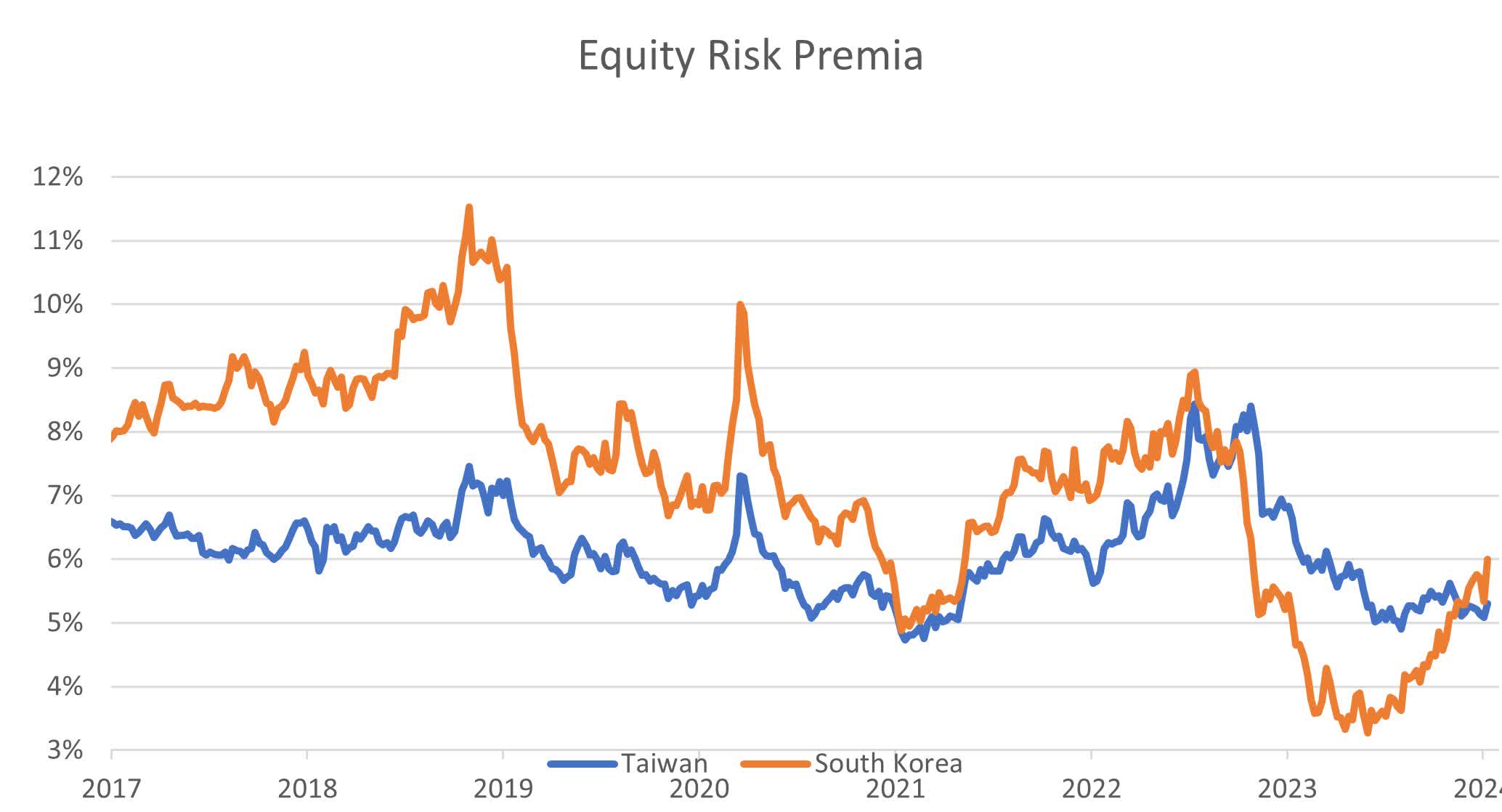

This all indicates to us that tensions on the Taiwanese Strait are unlikely to intensify in the months ahead – which should prove to be good news for Asian markets. We have seen our proxy for the equity risk premia (i.e., the additional return above government bonds demanded by the market) in Taiwan tighten over the last couple of months, indicating a reduction in perceived risk.

Source: LSEG Datastream, 15 January 2024. Equity risk premia calculated as the earnings yield less the 10 year government bond yield

Key watchpoints for investors

We believe the next big watchpoints for Taiwan will be the naming of the Legislative Speaker in February – given the divided Legislative Yuan – followed by the formal taking of office by President-elect Lai in May.

At first glance, the potential for China-Taiwan tensions to not escalate further would appear to remove one of the concerns that investors have had from a geopolitical perspective. However, given the backdrop of still-elevated global recession risks, we do not believe the Taiwanese election results are a green light for equity markets to take off. Additionally, there are a number of other geopolitical risks still present in the global economy, including the upcoming U.S. elections and any potential shift in U.S. policy toward China.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

CORP-12396

Q2 2024 Earnings Call Transcript")