RiverNorthPhotography

Investment Thesis

T. Rowe Price (NASDAQ:TROW) is a fundamentally solid asset manager with a long track record of outperforming relative benchmarks which has led to consistent growth in assets under management. Despite short-term challenges driven by rising interest rates which as led to net outflows over the past few years, I believe interest rate cuts will be on the horizon in 2024 which should help TROW turnover these short-term challenges. TROW has a shareholder-friendly management team and maintains a healthy balance that can help the company weather any macro-economic environment. Based on a DCF valuation, I see TROW as a hold as I estimate that the stock will deliver 10% annual returns over the next five years.

Company Overview

T. Rowe Price is one of the world’s largest investment managers which offers access to their own mutual funds and advisory services. The business makes money through management fees which are based on the amount of assets under management from both institutional and retail clients. The TROW business model has proven to be sustainable as the company has been around for 80 years but does face competition from competitors such as Blackrock (BLK) and Vanguard who offer low-cost index funds as well as Fidelity who is also an asset manager.

Assets Under Management To Turn-Around

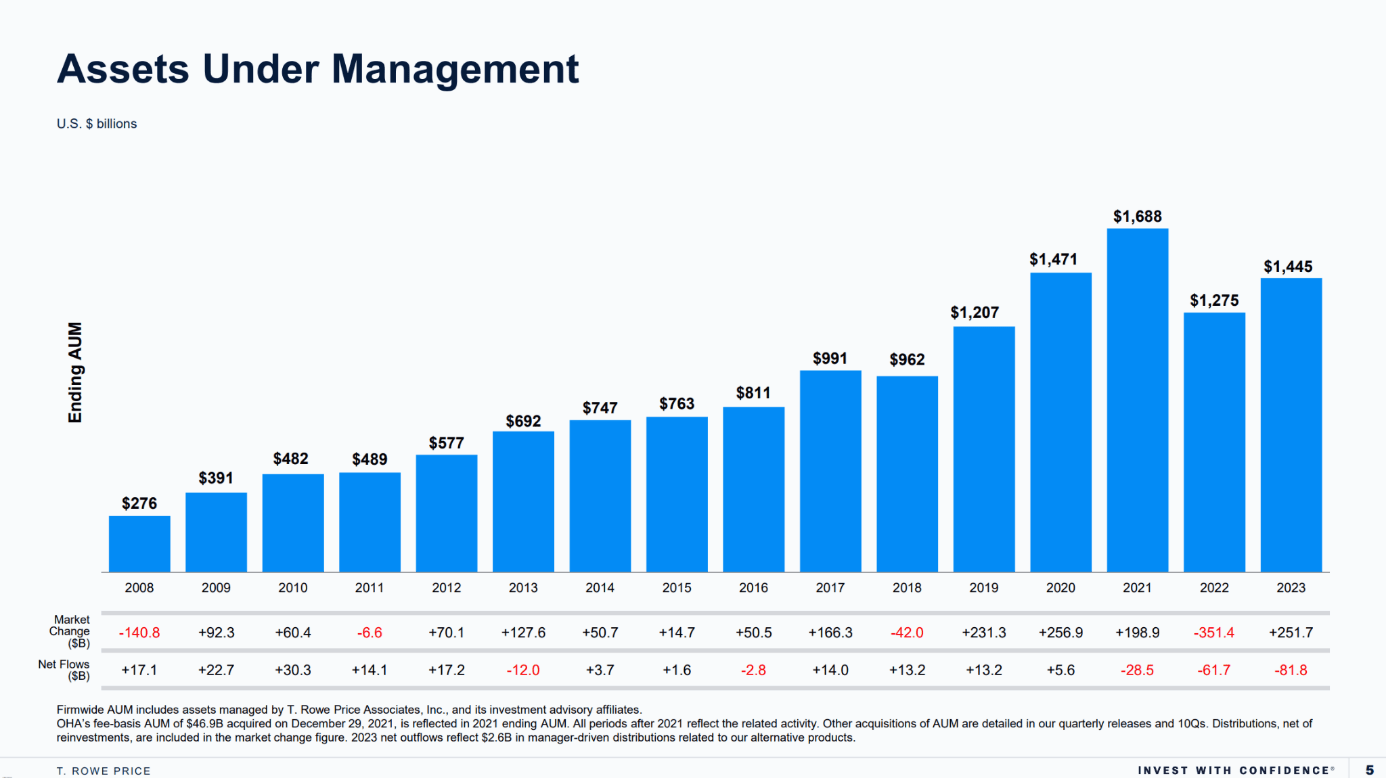

As we can see in the graph below is TROW’s assets under management from 2008 to 2023. We can see through this period that assets under management have been in a consistent uptrend going from $276 billion in 2008 to $1,445 billion in 2023. We can see that assets under management peaked for TROW in 2021 where assets under management reached $1,688 billion before dropping sharply in 2022. I believe this sharp drop was the result of two key reasons. The first reason is that the market had a rough year in 2022 where the S&P 500 returned -18.11%. As a result, this fall in the market caused assets under management to also fall. The second reason for the sharp drop was the changes in monetary policy that led to higher interest rates. As interest rates have risen, this has slowed demand and the amount of liquidity available for investors to place into funds such as TROW.

TROW Q4 2023 Earnings Presentation

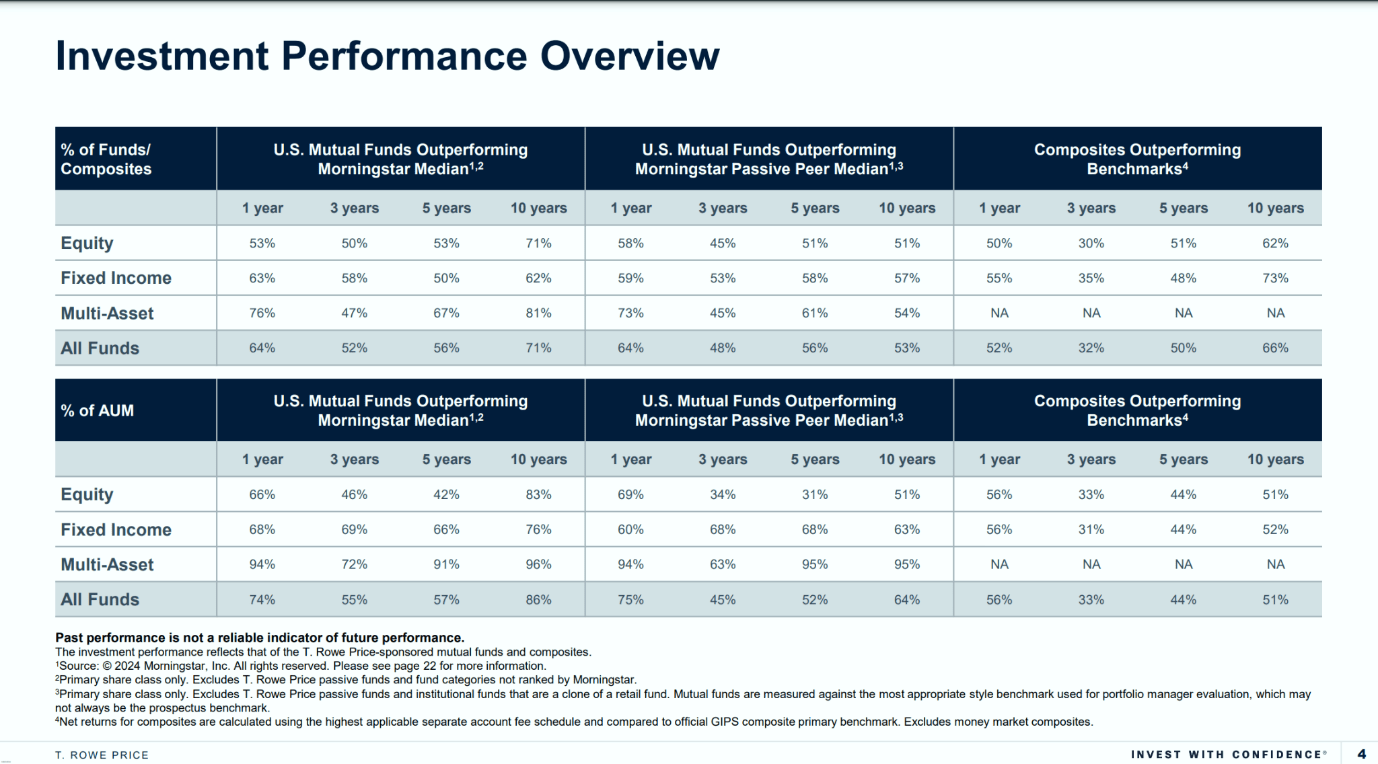

As we can see in the image below, a notable portion of TROW’s funds have consistently outperformed relative benchmarks over various time periods including equity funds, fixed income funds and multi-asset funds. I believe that as long as TROW’s funds continue to outperform their relative benchmarks, investors whether that be institutional or retail will want to be a participant in the outperformance. This should eventually bring net flow back into TROW.

TROW Q4 2023 Earnings Presentation

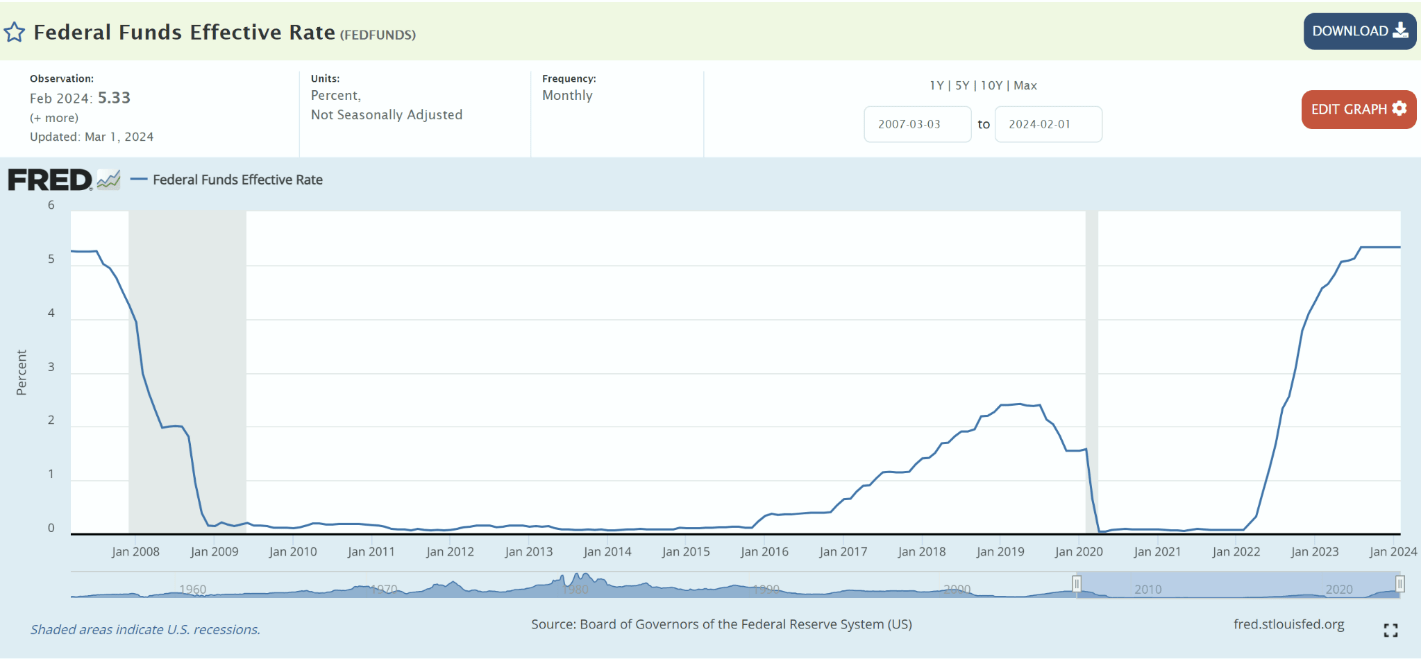

Furthermore, another reason I think net flows will turn around is because I think it is likely that the Federal Reverse will begin interest rate cuts later in 2024. The interest rate cuts will then likely draw investors back into TROW funds as available liquidity increases hence being a positive tailwind to assets under management.

Federal Reserve Bank of St. Louis

In my opinion, based on TROW’s long-term outperformance of relative benchmarks and likely interest cuts later this year, I see net flows improving and I expect TROW’s assets under management to continue its turnaround.

Shareholder Friendly Management Team

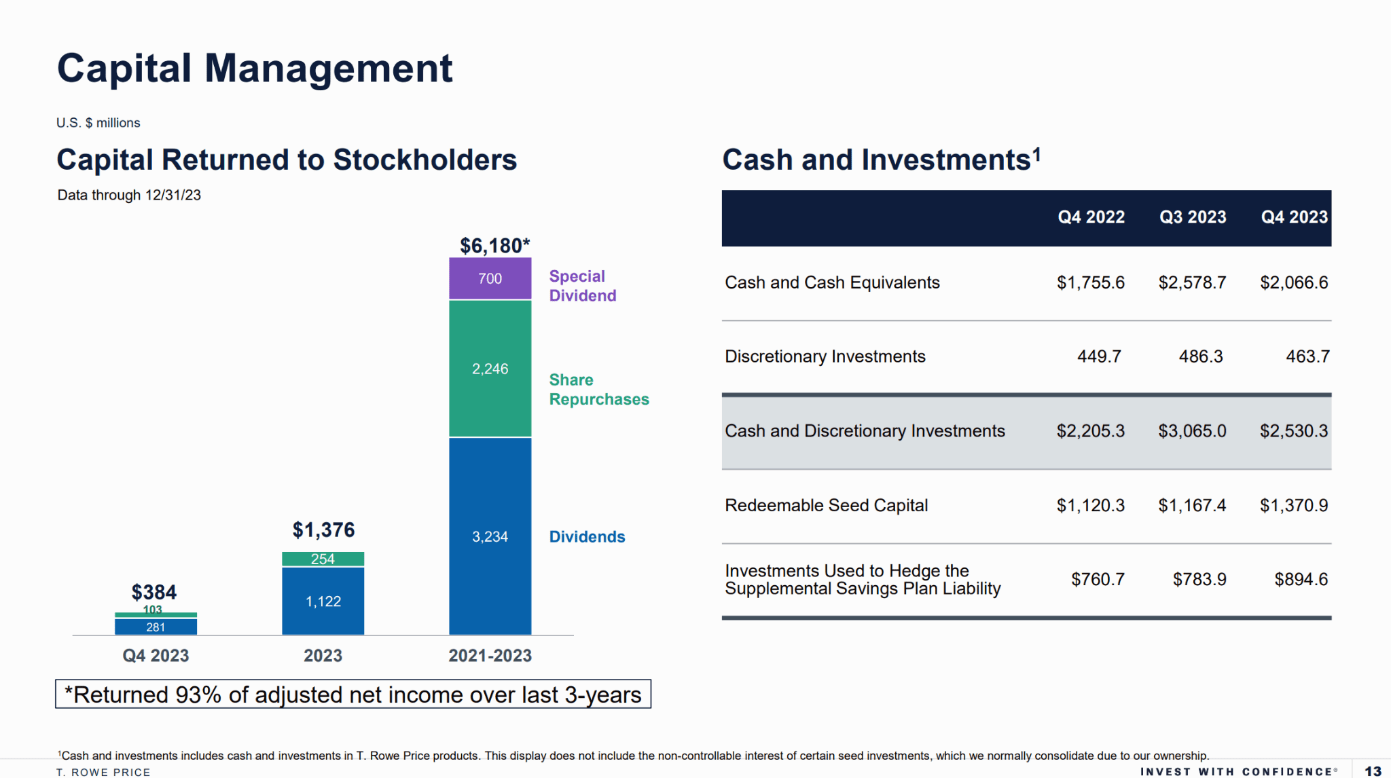

A true positive of TROW is their shareholder friendly management team where they have delivered 93% of adjusted net income over the last three years back to shareholders via a combination of dividends, share repurchases and a one-time special dividend as we can see in the image below.

TROW Annual Meeting of Shareholders 2023

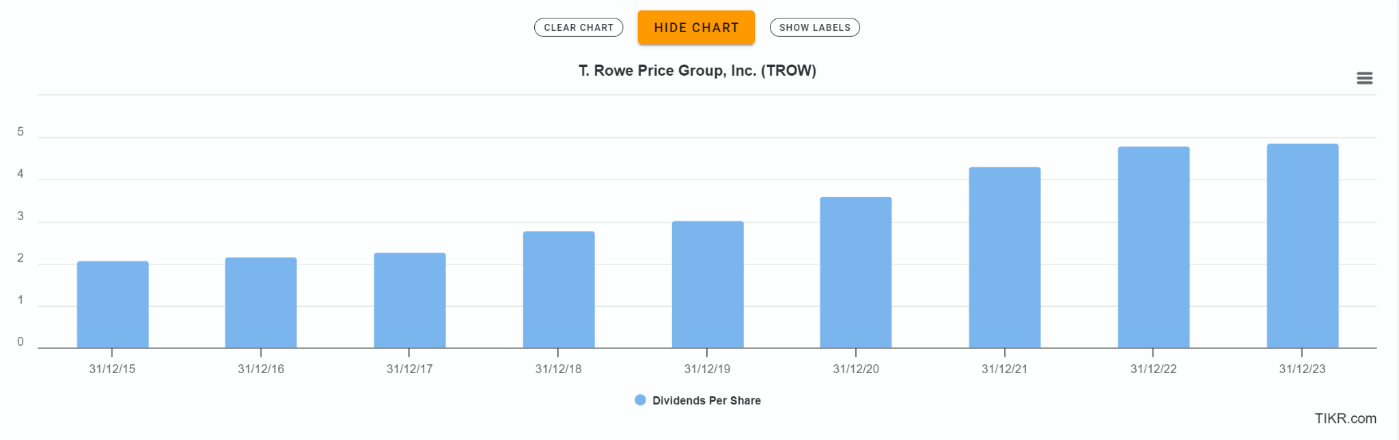

This commitment to returning capital to shareholders shows that the company is committed to returning the profits made within the business back to shareholders. The graph below shows TROW’s dividend per share from 2015 to 2023. We can see that the dividend payouts have gradually increased year after year beginning at $2.08 per share in 2015 and reaching $4.88 per share in 2023. In years of increased profitability, the company also likes to pay special dividends where they paid an additional $3 per share dividend in 2021.

Tikr Terminal

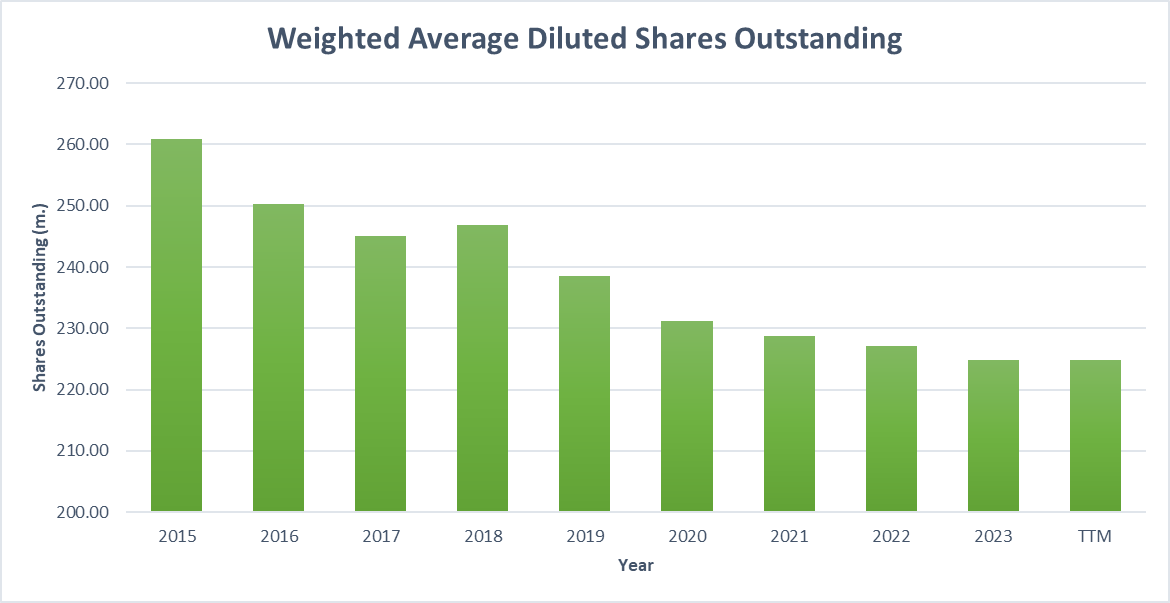

The image below highlights TROW’s share count through the past nine calendar years. We can see that diluted shares outstanding have dropped from just above 260 million shares down to about 225 million shares in the last twelve months. Hence, resulting in a 13.5% total decrease in the number of shares outstanding.

Created by Author

Overall, it is clear that the management team is prioritizing shareholders and is committed to delivering the majority of net income back to the owners of the business.

Financial Analysis

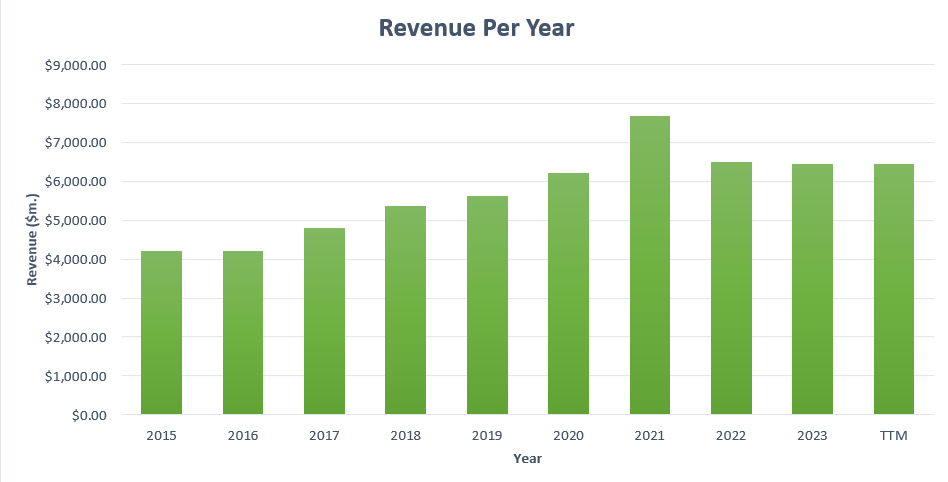

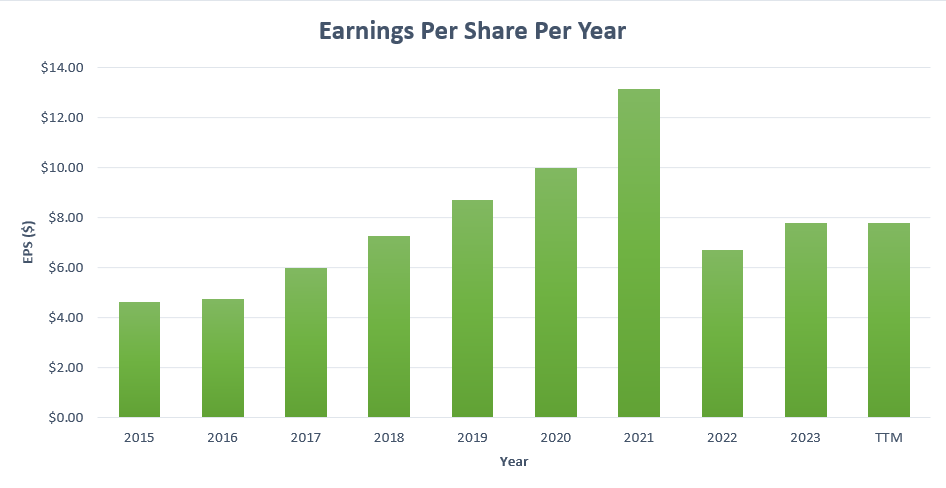

TROW’s revenue increased slowly going from $5,372.60 million in 2018 to $6,460.50 million in the last 12 months, with a CAGR of about 4%. The EPS over the last five years was pretty much flat, moving from $7.27 in 2018 to $7.76 in the last 12 months.

Created by Author

It should be noted that EPS peaked in 2021 reaching $13.12 per share, this was due to the historically low interest rates at the time and the demand being extreme for funds that focus on growth such as that of TROW. Since interest rates have risen, the demand from retail investors has decreased resulting in a loss of assets under management, hence affecting EPS. I believe EPS will turn around in 2024 and return to growth with interest rate drops likely becoming a tailwind for TROW looking out to the back end of 2024.

Created by Author

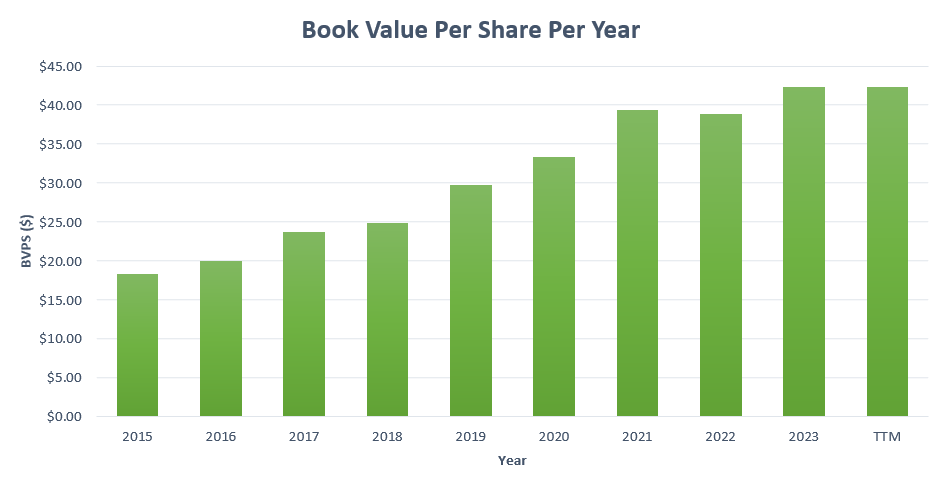

The Book Value Per Share (BVPS) has also grown, going from $24.80 per share in 2018 to $42.28 per share currently. The CAGR for this metric is around 11%, indicating that the company has increased its intrinsic value over the years.

Created by Author

As for liquidity, the latest quarter shows cash and cash equivalents of $2,066.60 million. The company’s total long-term debt is $89.00 million, which is easily manageable. The current ratio is 1.79, I was this as healthy for TROW’s short-term financial health. Overall, the balance sheet is very strong, and debt is no issue for TROW.

Looking forward, I think financial performance will improve compared to the previous two years as I forecast TROW returning to earnings growth driven by likely upcoming interest rate decreases which should drive more liquidity back into TROW’s funds, hence increasing revenues associated with management fees.

Valuation

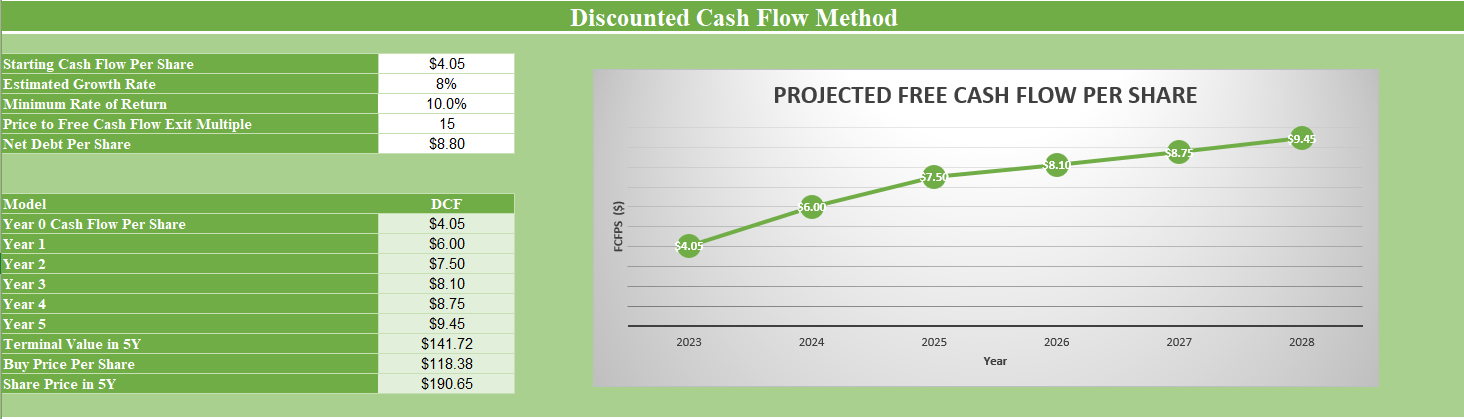

As of Q4, 2023, TROW’s current free cash flow per share is $4.05. Given that I believe TROW’s assets under management will return to growth, I anticipate an annual growth rate of 8% for TROW’s free cash flow per share over the next five years. The 8% growth rate for free cash flow per share I believe will be driven by a combination of two main factors. The first factor is that I expect continued outperformance of their funds which will attract additional net flows that will boost TROW’s assets under management. The second factor is that I expect share buybacks to continue which will decrease the share count through the next five years, hence acting as a tailwind for free cash flow per share. Taking this growth into account, the projected free cash flow per share for TROW by Q4 2028 would be $9.45.

Using an exit multiple of 15, which is based on TROW’s average price-to-free-cash-flow ratio over the past decade, the estimated price target for the stock in five years would be $190.65. Therefore, if you invest in TROW at its current share price of $118.33, the expected CAGR would be 10% over the next five years, based on these calculations. As a result, based on this valuation I see TROW as a hold as at the current share price there is no margin of safety.

Created by Author

Conclusion

I see TROW as a solid asset manager. They have faced short-term challenges with net outflows of capital seen over the past few years which has put pressure on assets under management. However, TROW’s funds have a strong long-term history of beating relative benchmarks which should help draw investors back into their funds particularly when we likely see interest rate cuts later in 2024. I believe once interest rates turn back around this will be a positive tailwind for TROW’s assets under management. TROW also has a capable management team that has a strong focus on delivering capital back to shareholders via dividends and share buybacks. Based on current valuations, I see TROW as a hold given that I estimate an annual return of 10% over the next five years.

Q2 2024 Earnings Call Transcript")