imaginima

Investment Thesis

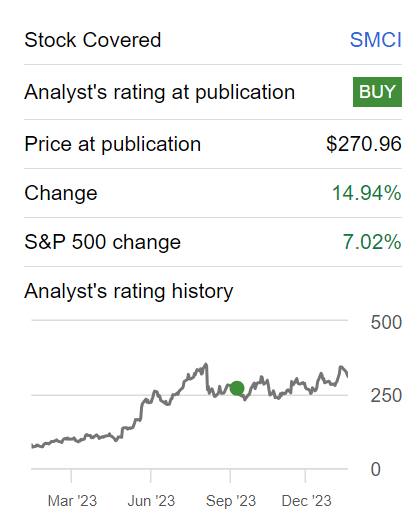

Super Micro Computer (NASDAQ:SMCI) delivered new fiscal Q2 2024 guidance that took investors by surprise. The business is guiding for such a strong fiscal Q2 2024 that investors are in awe.

More specifically, SMCI with a net cash position of approximately $400 million, is expecting its revenues in fiscal Q2 2024 to grow by more than 100% y/y to approximately $3.7 billion.

According to my estimates, this leaves this hyper-growth business priced at 14x non-GAAP EPS. Even as we consider some notable risk factors facing this business, I still believe this stock offers investors a compelling risk-reward.

Rapid Recap

Back in September, in a bullish analysis, I wrote,

I find Super Micro Computer to be a compelling investment opportunity due to its specialization in high-performance and energy-efficient computer systems, catering to AI markets.

[…] Despite this positive outlook, there are challenges to consider, including the potential commoditization of their hardware and competition on pricing.

Additionally, while profitability has room for improvement, the company remains confident in its ability to generate strong cash flows. With AI’s continued growth and Super Micro’s innovation capabilities, I see strong prospects ahead for this investment.

Author’s work on SMCI

Since I penned those words, the share price has moved slightly higher, but I don’t believe investors were expecting SMCI to deliver such a strong return. Therefore, I remain bullish on this stock.

Why Super Micro Computer? Why Now?

Super Micro Computer specializes in designing high-performance and energy-efficient computer systems for diverse markets such as data centers, cloud computing, and AI. Their product range includes servers, storage systems, and blade servers. The company stands out for its rapid development and testing of new computing platforms using common building blocks. Collaboration with leading hardware and software suppliers helps integrate cutting-edge technologies into their products.

A distinctive feature is their commitment to resource-saving architecture, aiming to reduce data center operating costs. This architecture supports independent refresh of CPU and memory resources, lowering refresh cycle costs and minimizing electronic waste. Super Micro Computer also offers space and power-efficient products by enabling the sharing of computing resources in data centers.

The majority of their business revolves around server and storage systems, with a notable success in providing complete rack-scale solutions to major AI innovators, including Nvidia. This strategic focus positions them well in the growing AI market, with potential for expansion to additional clients beyond Nvidia.

Given this background, let’s discuss SMCI’s new guidance.

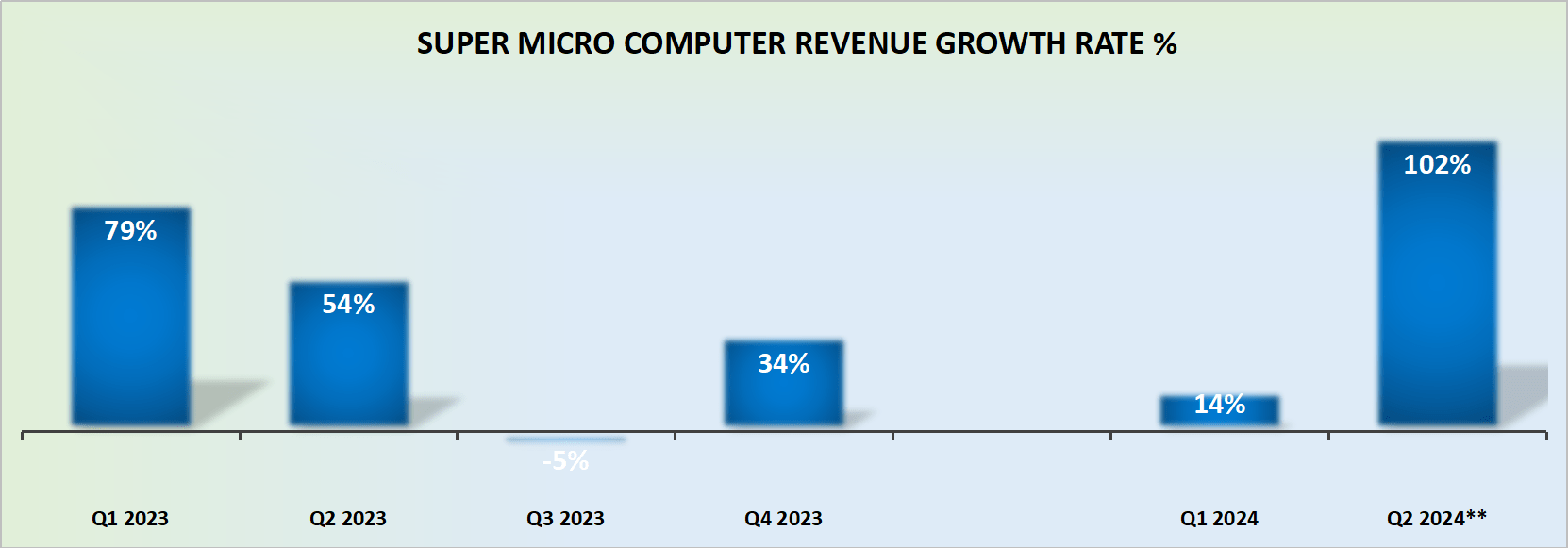

Revenue Growth Rates Astound

SMCI revenue growth rates

There was always the expectation that Super Micro Computer was going to deliver a strong fiscal Q2 2024 result since the company had previously guided at the high end for more than 60% CAGR.

But I don’t believe many investors would have expected the company to earnestly deliver more than 100% CAGR at the high end of its revenues. Particularly when we consider that fiscal Q2 2023 was a pretty tough quarter to beat, in and of itself.

What’s more, fiscal Q3 2024 and fiscal Q4 2024 are both up against dramatically easier comparables. Consequently, given the company’s newly found growth, it appears likely that fiscal H2 2024 should deliver around more than 80% CAGR.

Here’s the math – for fiscal Q2 2024 the high end of its guidance points to $3.7 billion. This is an increase of 72% sequentially from fiscal Q1 2024. Therefore, in order to provide me with a margin of safety, I expect that fiscal Q3 2024 grows by 10% sequentially each quarter.

Even though 10% sequentially on the back of this fiscal Q2 2024 guidance seems to me so conservative that it borders on being erroneous, for the sake of our discussion, let’s just use this estimate.

This means that SMCI is now on a path towards $17 billion in revenues in the coming 12 months.

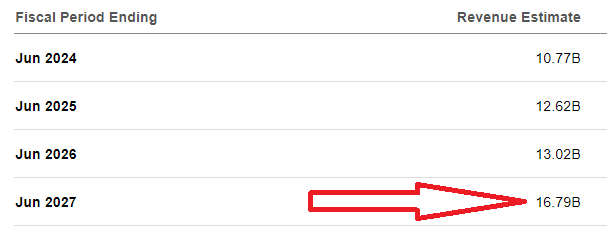

What’s more, consider what analysts had expected from SMCI.

SA Premium

The Street wasn’t expecting SMCI to deliver $17 billion of revenues until 2027. Put another way, SMCI has pulled forward 3 years worth of revenues.

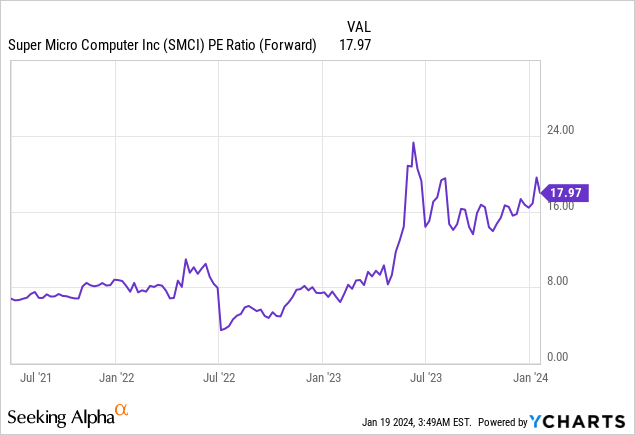

SMCI Stock Valuation — 14x Forward EPS

Previously, on the back of fiscal Q1 2024, SMCI was expecting to see around 4.90 of EPS at the high end. This would have meant that SMCI was growing at 43% y/y.

That was clearly an attractive growth rate, which investors were previously paying about 17x forward EPS.

And now, at the high end, SMCI is guiding for $5.55 of EPS. Consequently, on a forward run-rate, it appears likely that SMCI could deliver $25 of EPS over the next twelve months.

This means that SMCI is priced at about 14x forward EPS. Even if we consider the fact that SMCI’s recently ignited growth rates are not going to be sustainable, because this sort of growth never lasts long, having to pay 14x forward EPS for a business that I estimate to grow by +80% over the next 12 months seems like a very compelling investment.

Risk Factors

This is not a stock that has traded at particularly high P/E ratios in the past. This means that irrespective of this stock’s growth rates, this stock isn’t likely to re-rate significantly higher.

SMCI predominantly collaborates with NVIDIA (NVDA), AMD (AMD), and Intel (INTC). This means, that as its customer base continues to scale higher, there’s going to be increased customer concentration with these customers. More specifically, as of last quarter, fiscal Q1 2023, one customer accounted for 25% of the net sales for that quarter.

This means that SMCI is highly contingent on that customer for its growth rates, and it is very much at this customer’s mercy when it comes to renegotiating contracts.

Alongside this key risk factor, there’s the corollary to it, which is, how long can investors expect SMCI to grow at these breakneck rates? Naturally, I have no ability to predict that, and it’s a risk that readers need to be aware of.

The Bottom Line

In summary, I am impressed with Super Micro Computer’s new fiscal Q2 2024 guidance, which have defied expectations and sparked investor awe.

With a substantial net cash position of approximately $400 million, the company anticipates a remarkable over 100% year-over-year revenue surge to reach around $3.7 billion in fiscal Q2, 2024.

While I acknowledge certain risk factors, such as customer concentration and the sustainability of this accelerated growth, the robust financial position and the stock’s valuation at 14x forward EPS make SMCI an enticing investment. Considering the expected +80% growth over the next 12 months, this unexpected acceleration in revenue trajectory positions SMCI as a compelling and exciting prospect in the market.

Q2 2024 Earnings Call Transcript")