Jasmin Merdan/Moment via Getty Images

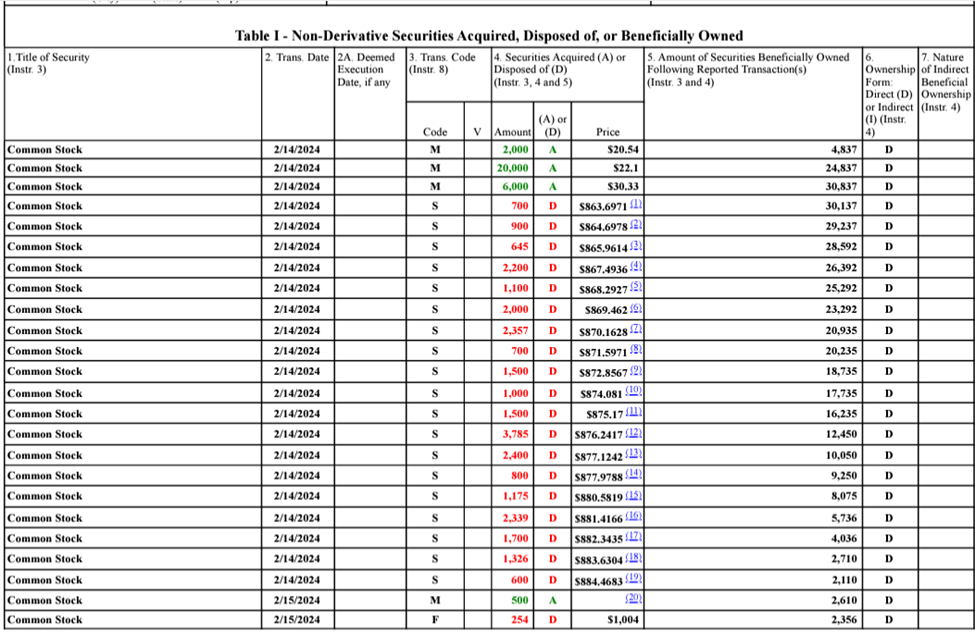

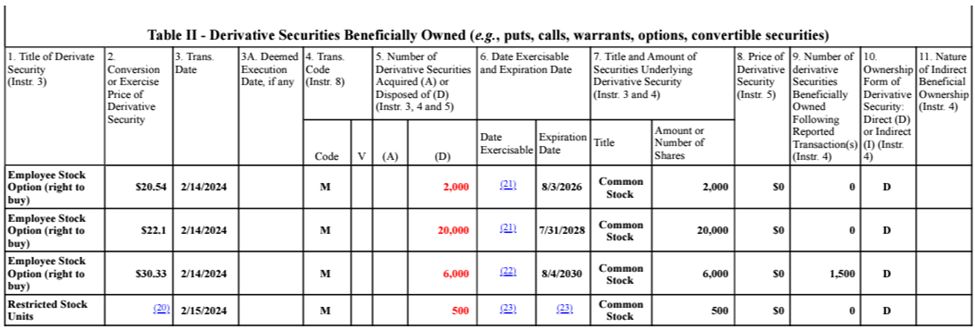

The first question that comes to mind after this huge run-up in share price is whether Super Micro Computer (NASDAQ:SMCI) still has gas in the tank to continue appreciating in value. Since January 2023, the stock has returned 2.23x before pulling back -20% on February 16, 2024. A -20% pull on share price should raise an alarm bell for any prudent investor; however, looking at the recently filed Form 4, it appears that Don Clegg, SVP of Sales sold a large block going into the end of the week. The real question to ask is whether this sell-off was the beginning of a new trend and whether this large block sold by an insider is a signal to the market for imminent events to come. Despite this pullback in the share price, I believe that SMCI has a significant upside potential given management’s ambitious growth strategy. I provide SMCI shares a BUY recommendation with a price target of $1,700/share based on 5x eFY25 sales.

Form 4 Form 4

Operations

Q2’24 was a major turning point for SMCI as the firm experienced significant growth at the top line of 103% on a y/y basis. This level of growth should not go unnoticed for the 30-year-old company, as the firm plays a central role in the transition to higher capacity computing in the renaissance of GenAI. Despite this hypergrowth state, management did raise some concerns in their q2’24 earnings call that appear to be relatively common for companies that are central to the corporate AI initiative. Palantir (PLTR) experienced similar challenges with high interest for their platform as more companies turn to AI technology to optimize operations and subsequently expand their sales team to cater to this heightened interest. In their own respect, SMCI is scaling their operations with new facilities in Silicon Valley and Malaysia to cater to this heightened level of interest in their hyperconverged infrastructure. As SMCI acts as an omnichannel for all the major chip manufacturers, including NVIDIA (NVDA), Advanced Micro Devices (AMD), and Intel (INTC), I believe their advanced compute systems will play a pivotal role in scaling GenAI at the data center level.

JPMorgan (JPM) analyst Samik Chatterjee sees substantial growth in the broader hardware market as AI takes form.

Despite a cautious view on the sector in aggregate for 2024 on account of the elevated valuation multiples heading into 2024, the leverage to AI for certain sections of the broader hardware coverage is likely to be a windfall moment with an opportunity for a re-rating on account of the incremental TAM opportunity around AI.

Though this article references competitors to SMCI, I believe that it gets the point across that SMCI will have the opportunity for continued growth within the growing TAM, as well as a valuation rerating as the hardware refresh goes through a cyclical upswing.

Looking to operations, SMCI has 4,000 racks/month in production capacity as of q2’24. As of this period, the firm has capacity of 1,500 racks/month with direct attached liquid cooling and expects to build capacity to reach 5,000 racks/month. I believe that this additional capacity will provide SMCI the ability to drive significant revenue growth, as this type of cooling is vital for the next generation of high-performance computing. As of q2’24, the firm’s facilities operated at 65% capacity across the US, Netherlands, and Taiwan facilities and are quickly filling in the gap. The firm is actively expanding capacity with their new Silicon Valley facility and Malaysia facility as well as increasing the capacity at their APAC facility (2-3x) that will provide a lower-cost, higher-volume solution to the firm’s scaling challenges. With this additional build-out, management anticipates some headwinds to margins as the firm adds headcount and capital equipment, which I believe may result in another quarter or two of negative free cash flow. I don’t believe the capital outflow should be concerning, as the firm is going through a revitalized growth phase and must invest in working capital and capital equipment to meet the market’s demand. With these new facilities, management believes that the firm will reach their $25b annual revenue target. Despite the near-term headwinds to margins, I believe that once the facilities are built out and operational, SCMI will experience economies of scale as they will be better positioned to meet market demand for their integrated solution.

Forecasting financials, I anticipate SMCI to continue to experience significant revenue growth into the duration of eFY24 and eFY25 as the firm scales production volumes on the back of the AI boom. I do anticipate some margin contraction through gross and operating income as the firm undergoes their period of high capital and operating investment to scale operations. I do anticipate margins to trend upward through eFY25 as the firm realizes this scale, but not to reach FY23 margins quite yet.

Corporate Reports

Despite my optimism in the company, there are some negative risks to take into consideration before building a position. There are heightened geopolitical risks between Taiwan and China that may impact SMCI’s production if tensions were to escalate. 14.7% of total sales derived from Asia in FY23, making this risk, though a longshot, a potential risk to take into consideration when making an investment decision. Another risk worth considering is whether their strength in sales will continue as the firm invests in these new facilities. If AI were to become more harshly regulated and infrastructure demand were to suddenly fall off, SMCI could be poorly positioned with excess capacity.

Lastly, Taiwan Semiconductor (TSM) is doubling their capacity for their advanced chip packaging process, CoWoS to support Nvidia’s growth. This can be a positive signal for demand for SMCI’s infrastructure.

Value & shareholder Value

Corporate Reports

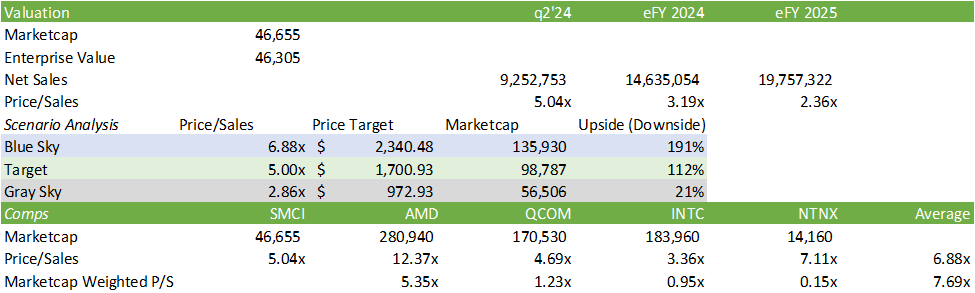

Ultimately, we need to figure out how to value SMCI. The old cohort of IT infrastructure companies doesn’t justify SMCI’s high trading multiple, which by comparison is very expensive.

Corporate Reports

Comparing SMCI to the AI tech names, such as AMD, QUALCOMM (QCOM), Nutanix (NTNX), and INTC, paints a more viable comparison as the firm’s recent swing to a higher valuation is more comparable to this cohort of companies. Considering these comps, I believe that the 6.88x sales will be too high of a valuation for SMCI as SMCI depends more heavily on hardware integration in their operations and will not experience as strong of margin expansion as this peer cohort as the firm scales operations. I believe that this 6.88x will be the absolute blue-sky valuation that will likely not occur. I believe the current valuation at 5x sales is more appropriate for SMCI, giving it an upside potential of 112% based on eFY25 revenue. I believe that this recent pullback was unjustified given the massive block sale from an insider and that SMCI shares still have some gas in the tank. I provide SMCI shares a BUY recommendation with a price target of $1,700/share based on their eFY25 revenue.

Corporate Reports

Technical Trading

On the tactical side, shares should recover and reach $1,345 in the next cycle using Elliot Wave Theory before pulling back to ~$1,125/share. From there, shares should reach my fundamental price target of $1,700/share in the last wave. For the active traders, I believe each pullback will provide a buying opportunity to build positions. Do note that tactical trading poses no proof that shares will reach their potential, and know the assumed risks when trading short-term positions.

TradingView

Q2 2024 Earnings Call Transcript")