Bilanol/iStock via Getty Images

Introduction

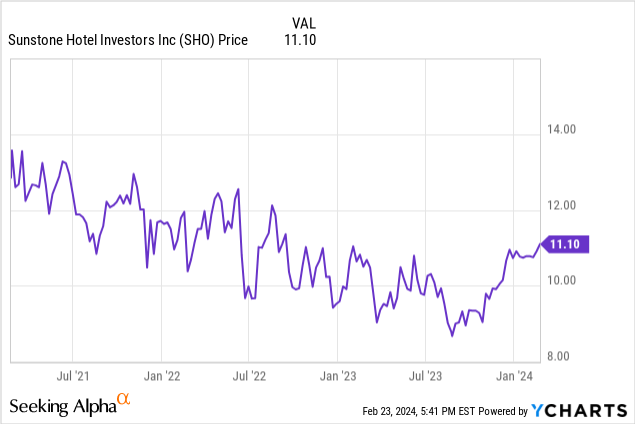

I have owned the preferred shares of Sunstone Hotel Investors (NYSE:SHO) for several years now as I think the (cumulative) preferred dividends offer an excellent stream of quarterly dividends that I don’t have to worry about thanks to the robust balance sheet of the REIT.

The recently published 2023 results confirm the preferred dividend is very well covered

As the net income is pretty irrelevant for a REIT, I will focus on Sunstone’s FFO and AFFO performance as that’s a more reliable metric to determine how attractive the stock is currently priced.

Sunstone Investor Relations

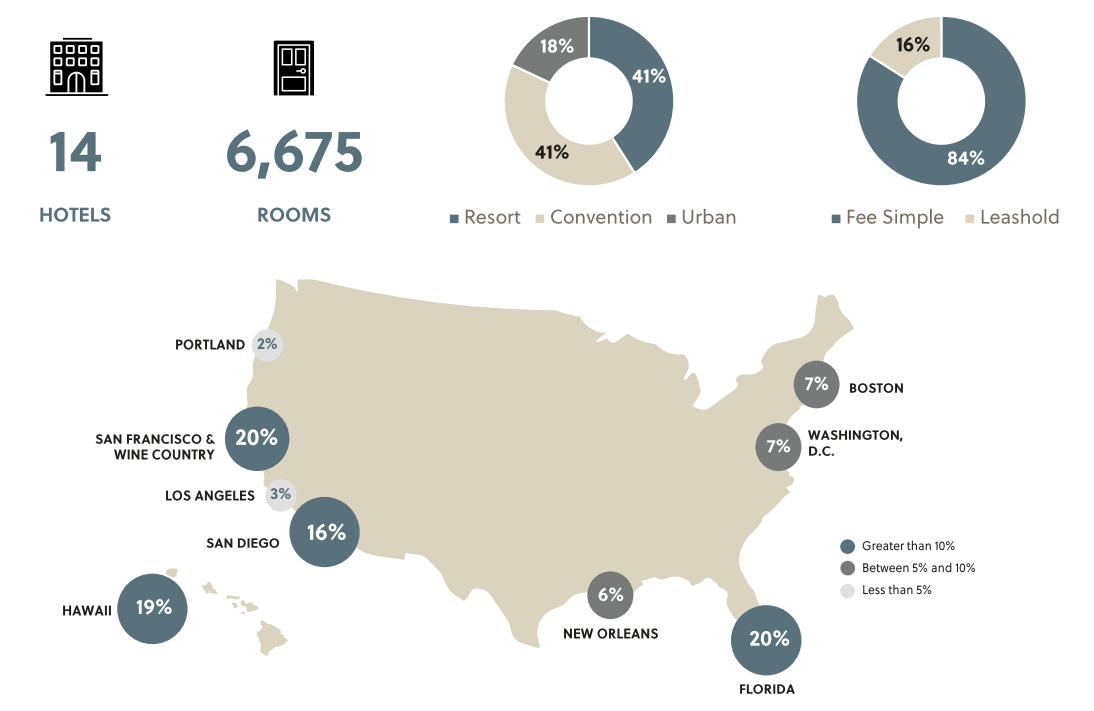

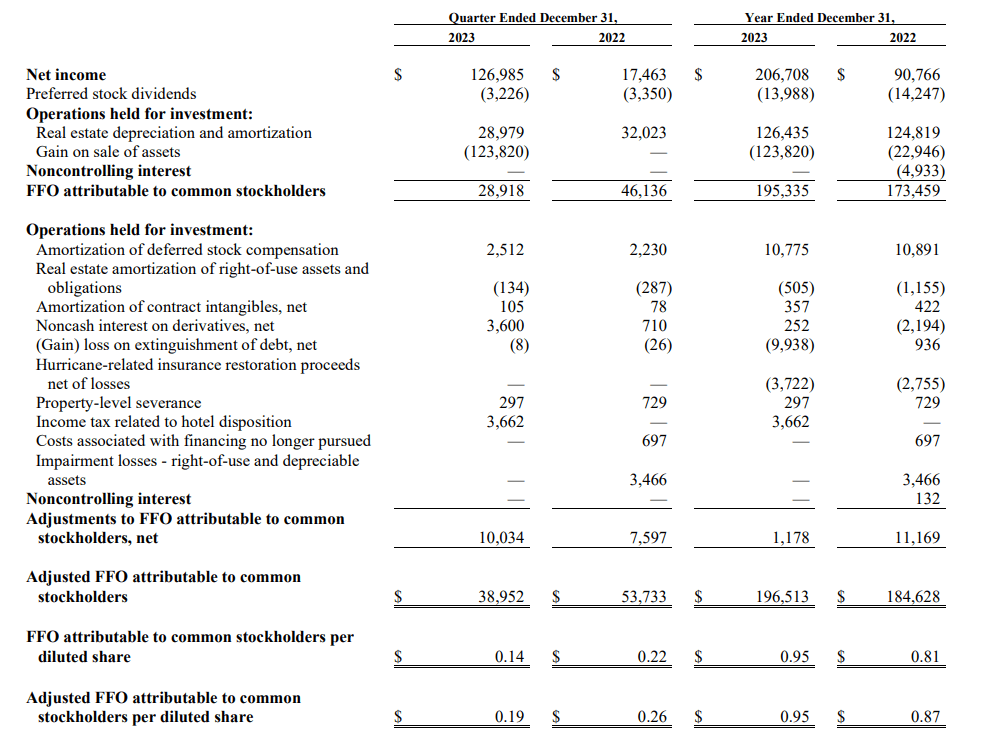

As you can see below, Sunstone recorded an FFO of just under $29M in the final quarter of 2023 which was substantially lower than the Q4 2022 result as the FFO in Q4 2022 was more than 50% higher. This wasn’t really a surprise as the interest expenses increased by approximately $5M on a year-over-year basis. Additionally, the Confidante Miami Beach hotel was closed for renovation during the fourth quarter. This reno will require the hotel to remain closed for about a year to complete all the work. Sunstone anticipates an 8%-9% net operating income yield once the renovation is completed.

Sunstone Investor Relations

As the image above shows, the FFO/Share in Q4 was approximately $0.14 while the AFFO was a little bit higher at $0.19 per share. The higher AFFO was caused by the non-cash interest on derivatives and the taxes payable on the (profitable) sale of a hotel during the quarter.

This brought full-year AFFO at $0.95 per share, an increase from the $0.87 generated in FY 2022. And an important element is that the $196.5M in full-year AFFO actually includes the $14M in preferred dividend payments. On a pre-dividend basis, the adjusted AFFO was $210M which means the payout ratio to cover the preferred dividends was just 7%. And that indeed indicates the preferred dividends should be safe.

As explained in my previous article, there are currently two series of preferred shares listed.

The H-series are trading with (SHO.PH) as the ticker symbol and offer a 6.125% preferred dividend for a total of $1.53125 per year, while the I-Series are trading with (SHO.PI) as the ticker symbol offering a 5.7% preferred dividend for a payment of $1.425 per year. Both issues are cumulative and can be called by Sunstone from May 2026 (SHO.PH) and July 2026 (SHO.PI) on.

As both preferred shares rank equal, it all comes down to buying the one that has the highest yield (as I think the risk for the preferreds to be called is negligible). That’s also why looking at the current yield makes more sense than the yield to call as I think a call is pretty unlikely.

At the time of writing this article, the H-shares are trading at $21.89 while the I-shares trade at $20.53 for a yield of, respectively, 7% and 6.94%. This indicates that, at the current share prices it makes more sense to buy the H-shares as the yield is slightly higher and the preferred shares with a higher preferred dividend are more likely to be called than lower-yielding securities.

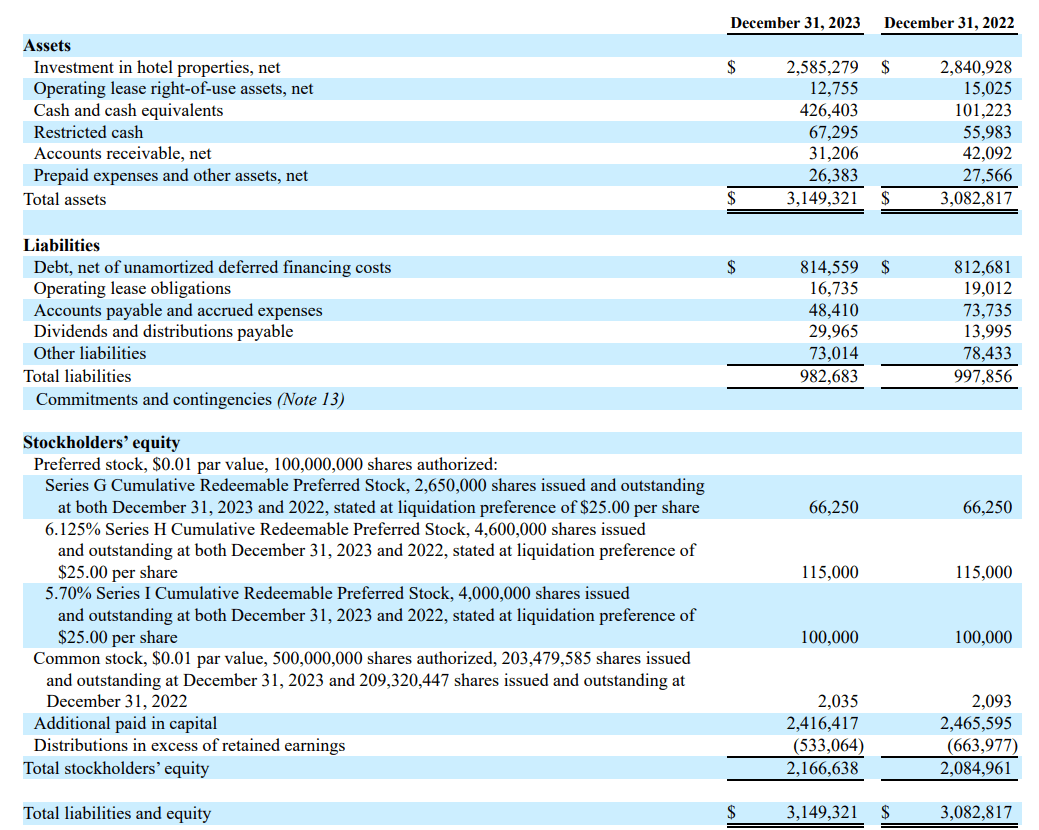

I already confirmed the preferred dividends are well covered, but I also wanted to highlight the strong asset coverage ratio. As you can see below, there’s approximately $281M in preferred equity which means the common equity accounts for just under $1.9B of the total equity.

Sunstone Investor Relations

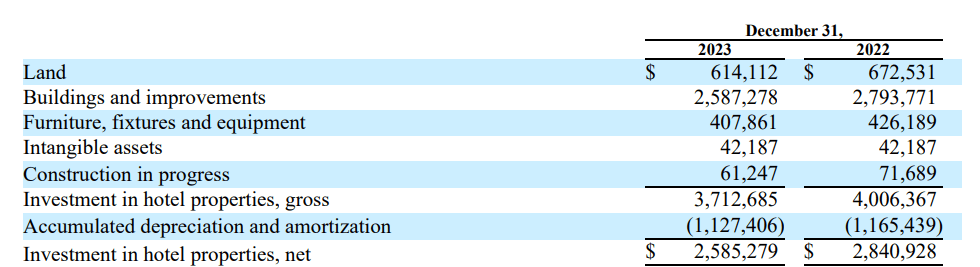

Also keep in mind the total equity “cushion” is based on the $2.59B book value of the real estate assets. As you can see below, this already includes in excess of $1.1B in accumulated depreciation, so the fair value of the real estate assets is likely quite a bit higher than the book value.

Sunstone Investor Relations

And that’s not just daydreaming. The Boston Park Plaza was sold in Q4 2023 for $370M, representing a gain of almost $124M compared to the book value of the asset.

2024 will be weaker due to renovations, but there’s little risk for the preferred securities

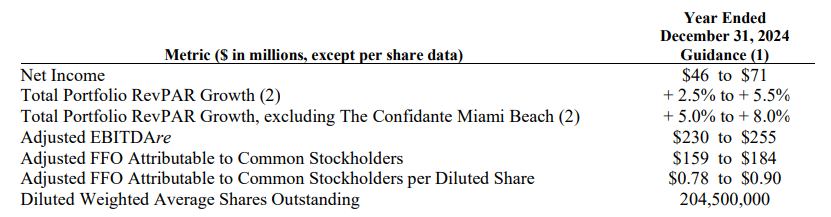

The REIT has also already provided an outlook for 2024. It expects to report a Revenue Per Available Room growth of 2.5%-5.5% and 5%-8% excluding the Confidante Miami Beach. More important to us is the anticipated AFFO of $159-$184M, which represents $0.78-0.90 per share.

Sunstone Investor Relations

That’s encouraging as it means the preferred dividends will continue to enjoy an excellent coverage ratio. The Confidante will reopen in the final quarter of 2024 so we should see an uptick in 2025. Meanwhile, the new Westing Washington DC opened in Q4 2023 and will start to provide a meaningful contribution to the result in 2024.

Investment thesis

I still like the preferred shares issued by Sunstone Hotel Investors very much. The preferred dividends are well covered while the strong balance sheet means there’s plenty of equity in the capital structure ranked junior to the preferred shares. That cushion gets even better if you compare the book value of the assets with the original investment in the hotel properties.

I have a long position in both series of the preferred shares, and I have no intention to sell them anytime soon. A cumulative preferred dividend yield of 7% is pretty attractive.

Q2 2024 Earnings Call Transcript")