chinaface

Investment thesis

Suncor Energy (NYSE:SU) is an absolute oil and gas superstar, given the company’s strong profitability, which allows it to produce substantial free cash flows. The management’s capital allocation approach is exceptional as the company successfully balances between reinvesting in the business, keeping a clean balance sheet, and keeping shareholders happy with solid dividend payouts and stock buybacks. The company is willing to capitalize on tailwinds for energy commodities markets, which I describe in my analysis. Moreover, my valuation exercise suggests that the stock is massively undervalued. All in all, I assign Suncor a “Strong Buy” rating.

Company information

Suncor is an integrated energy company headquartered in Calgary, Canada. The operations include oil sands development, production, and upgrading; offshore oil and gas; petroleum refining in Canada and the U.S.; and the national Petro‑Canada retail distribution network.

The company’s fiscal year ends on December 31. Suncor operates via the following segments: Oil Sands, Exploration & Production [E&P], Refining & Marketing [R&M], and Corporate. For the first nine months of 2023, Oil Sands accounted for 58% of the total SU’s pre-tax earnings, and R&M’s share was 39%.

Financials

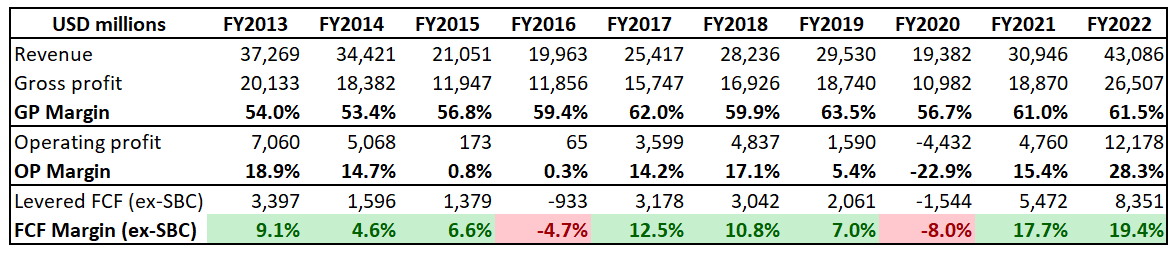

The company has demonstrated stellar financial performance over the last decade. Revenue was substantially volatile given the nature of Suncor’s business, where the top line of oil and gas companies heavily depends on the cyclicality of commodity prices. But even during years of low oil prices, the company delivered decent profitability and free cash flow [FCF] with the only negative outlier in the COVID-19 panic year, 2020. The staggering almost 20% FCF margin in 2022 suggests the company is strong in absorbing periods of sky-high oil prices.

Author’s calculations

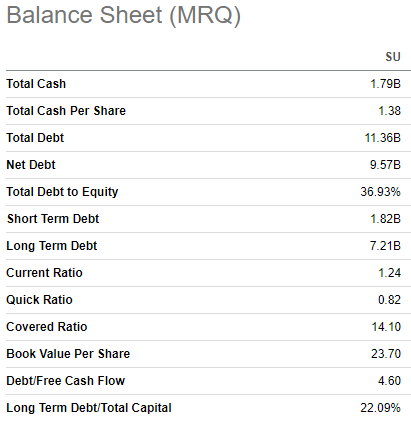

Suncor’s wide FCF metrics allow the company to successfully balance between sustaining a healthy balance sheet, expanding operations in a capital-intensive business, and keeping shareholders happy with consistent dividend payouts and stock buybacks. Liquidity metrics are firm and the leverage ratio is very prudent. A sound and balanced capital allocation approach is a good quality sign for me as an investor because it demonstrates that the company’s profits are deployed efficiently and strategically to improve shareholder value. That said, I believe that the currently offered by the stock’s 5.1% dividend yield is safe and has solid growth prospects, given a very moderate 37% payout ratio. The latest 5% dividend enhance was announced a month ago.

Seeking Alpha

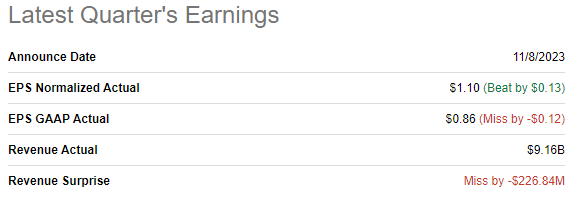

The latest quarterly earnings were released on November 8, when the company missed consensus revenue and EPS estimates. On the other hand, there was a positive surprise in terms of the non-GAAP EPS. Revenue decreased by 16.4% on a YoY basis due to the decreased crude oil prices.

Seeking Alpha

Despite revenue decrease, the company delivered a solid quarter from the profitability perspective. The operating margin was notably above 20%, which allowed to produce $1.9 billion in FCF, which helped to advocate solidify the company’s financial position.

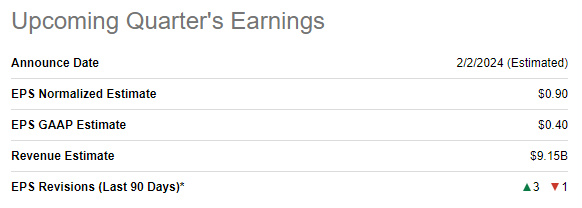

The upcoming quarter’s earnings release is scheduled for February 2, 2024. Quarterly revenue is expected by consensus at $9.15 billion, which indicates a 12% YoY reject due to decreased crude oil prices. The adjusted EPS is expected to follow the bottom line and shrink from $1.36 to $0.90.

Seeking Alpha

The revenue reject in 2023 should not mislead investors due to the inherent cyclicality of oil and gas companies’ revenues. Moreover, it is crucial to recall that last year was an outlier for crude oil prices after massive panic in almost all commodities markets after Russia’s invasion of Ukraine, which led to the economic isolation of one of the largest global crude oil exporters.

This year, crude oil prices demonstrated softness compared to the 2022 price spike. Still, it is important to recollect that the largest oil consumer, the United States, saw the tightest monetary policy over multiple decades. It was weighted on the economic activity level, resulting in weaker oil demand. Still, despite the harsh environment, oil prices were high in 2023. This week’s Fed’s announcement that three rate cuts are on the table in 2024 is good news for commodities markets. Lower Federal funds rates mean reduced borrowing costs for businesses and individuals, likely stimulating economic activity and investment, ultimately fostering increased demand for energy commodities in the market.

Apart from the positive shifts in the U.S. monetary policy, I see a couple more solid tailwinds for the oil and gas industry. Joseph Biden’s administration aggressively utilized the U.S. Strategic Petroleum Reserve [SPR] in 2022 to stem inflation and recently started to refill it. As inventory levels in SPR are at multidecade lows, I think the tailwind is solid and is likely to last longer. It is also important to keep in mind that the global geopolitical situation is very uncertain with two big ongoing military conflicts. Several oil-rich countries are involved in these conflicts, both directly and indirectly. Yes, it seems that oil sanctions against Russia do not work, but apart from geopolitical uncertainties in the Middle East, we have recently seen escalating territorial disputes between oil-rich Venezuela and Guyana.

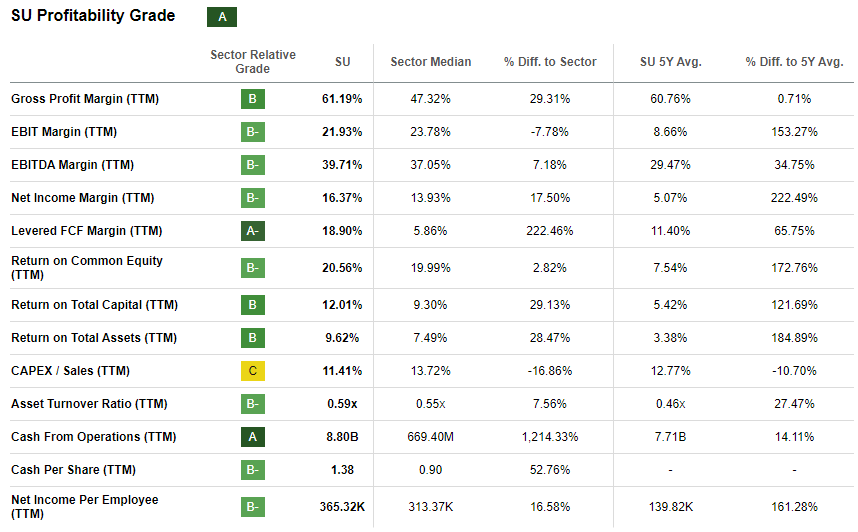

That said, industry tailwinds seem to be strong enough to preserve Suncor’s top line over the next years. But for value investors top line and FCF are the factors that matter the most. Suncor historically has demonstrated exceptional profitability, being best-in-class across multiple key metrics.

Seeking Alpha

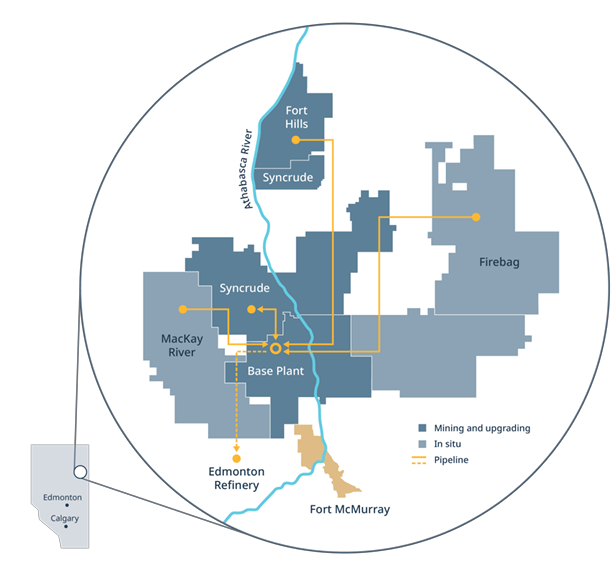

Suncor’s stellar profitability is achieved with a diversified base of high-quality assets which complement each other. Oil sands reserves have solid longevity with an estimated 26 years and the geographical location of key fields also helps to boost efficiency. Sites are in close proximity and connected by pipeline which allows to improve supply chain and bring down costs. The company’s wide profitability metrics allow it to invest heavily in capex to advocate boost infrastructure and create more opportunities to drive more efficiency.

Suncor’s latest earnings presentation

Valuation

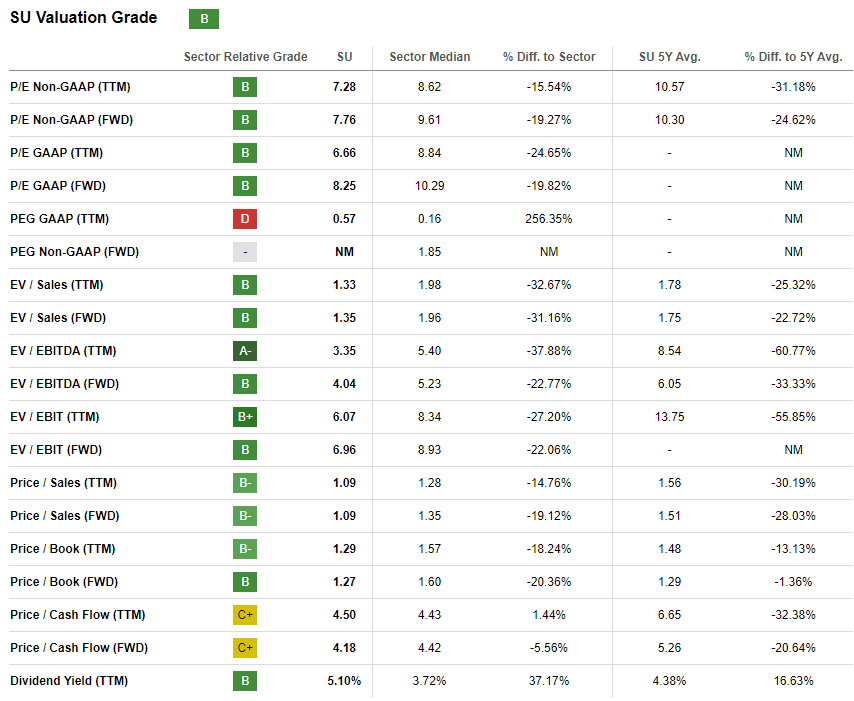

The stock price increased by 3.5% year-to-date, significantly lagging behind the broader U.S. market. However, SU demonstrated better 2023 performance than the American energy sector (XLE). Seeking Alpha Quant assigns Suncor’s stock an attractive “B” valuation grade because ratios are currently significantly below the sector median and the company’s historical averages. That said, the stock looks very attractively valued from the perspective of valuation ratios.

Seeking Alpha

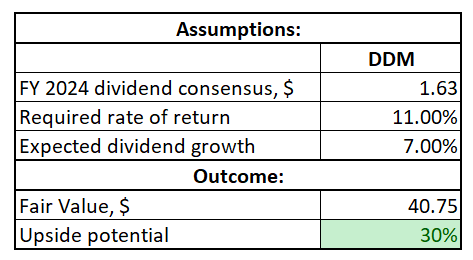

SU has consistently paid dividends over the last three decades. Therefore, the dividend discount model [DDM] simulation looks admire a reliable valuation method. I use an 11% WACC as a required rate of return. I include $1.63 as the current dividend, which is the consensus assess for FY 2024. Suncor has a strong dividend growth record. To be conservative I use a 7% last five years CAGR.

Author’s calculations

According to my DDM calculations, the stock’s fair price is slightly below $41. This indicates a 30% upside potential from the current levels. To sum up, Suncor’s stock is very attractively valued.

Risks to consider

The fact that the U.S. avoided recession in 2023 does not mean that it can do so infinitely. In case of a recession in the world’s largest economy, the commodities market will highly likely be adversely affected, which will impair Suncor’s earnings. On the other hand, OPEC and OPEC+ demonstrated multiple times this year that the organization is prepared to cut oil production to address negative shifts in the global oil demand. OPEC’s flexibility to adjust supply looks admire a solid protection against sharp oil price drops unless a new black swan, admire the pandemic, appears.

Investing in oil and gas companies might not be a good fit for long-term investors, given the secular shift to clean energy. While it is impossible to visualize our world without using oil and gas, the industry is very mature and the U.S. Energy Sector SPDR Fund ETF (XLE) demonstrated no stock price appreciation over the last ten years. Investing in companies admire Suncor better fits dividend investors and the ones who are seeking an opportunity to record capital gains on the industry’s cyclicality.

Bottom line

To deduce, SU is a “Strong Buy”. The company has been historically strong in absorbing high oil prices and my analysis suggests that the recent softness in oil prices is temporary and multiple industry tailwinds are behind Suncor’s back. The stock currently offers an attractive 5.1% dividend yield and a massive 30% upside potential, according to my valuation analysis.

Q2 2024 Earnings Call Transcript")