yocamon

Dear readers/followers,

Subaru, (OTCPK:FUJHY), or native ticker 7270 in Japan which is the one that I invest in, is an impressive automotive business with an upside that is one of the four Japanese companies I currently invest in. I have been invested in Subaru for about a year at this point, and despite a recent decline, I’m in the green on this position on an overall basis.

Subaru has reported 1Q24 results, and these are results that we’re going to take a closer look at today – however, one of the main reasons for my update today is the ongoing trends in overall global automotive, which gives me some worry for the established brands.

What am I talking about?

Let me show you by talking about Subaru and where I believe the company is going. My last article on the company can be found here, and my stance at the time was a positive one due to undervaluation. My return since my first investment in Subaru is still like this.

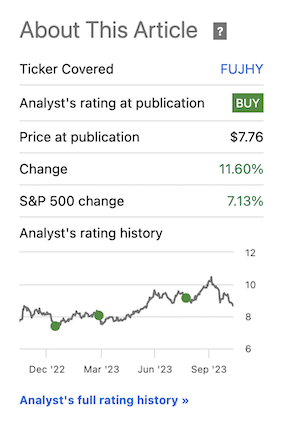

Seeking Alpha Subaru (Seeking Alpha)

So, you can see the advantages of valuation-oriented investing are still holding strong even in a market such as this. Some of my other investments in Japan include Canon (CAJ), as well as others.

Let’s look at the current Subaru results.

Subaru – The valuation is up, but Subaru is well-prepared to handle the upcoming challenges

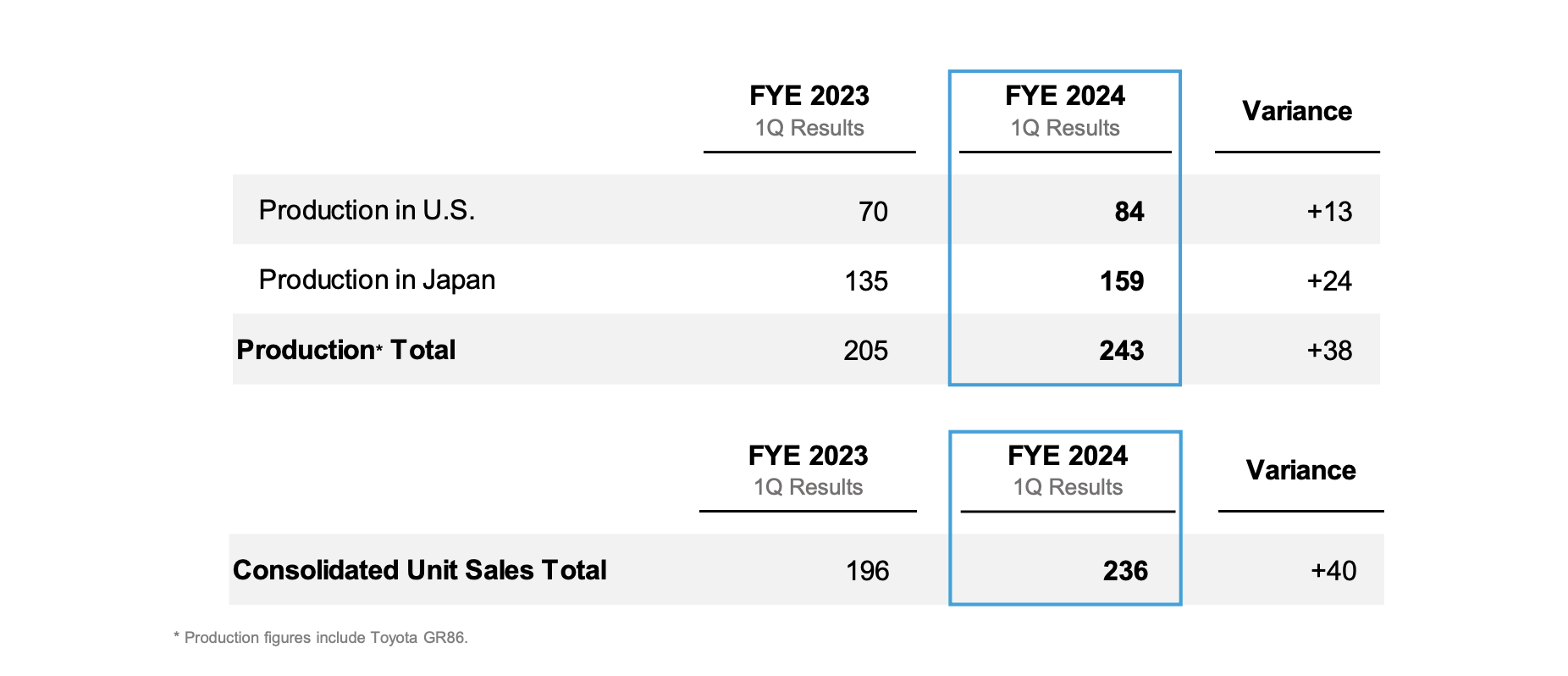

The latest results we have were presented in early August this year and for the 2024 Fiscal given the company’s structure. And the results were very good here. We’re talking about an 18% top-line production improvement and a 128% YoY increase in operating profit. This was due to both good volume growth, and good FX from a weak Yen which is currently offsetting increases in input costs and SG&A, and other factors.

The company forecasts a significant, 16% YoY production with a unit count of just over 1M, and an operating profit increase of double digits – around 12% – for the same reasons as mentioned here. Profit risks and uncertainties here are, among others, ongoing fluctuations in the Yen and what this may bring, as well as continued uncertainty in the semiconductor space, to which Subaru still has significant exposure and dependence. Many of the trends are familiar to me because the ongoing weakness of the SEK as a currency is having similar effects on some companies here in my home market.

Sales are strong, and the overall trends look promising.

Subaru IR (Subaru IR)

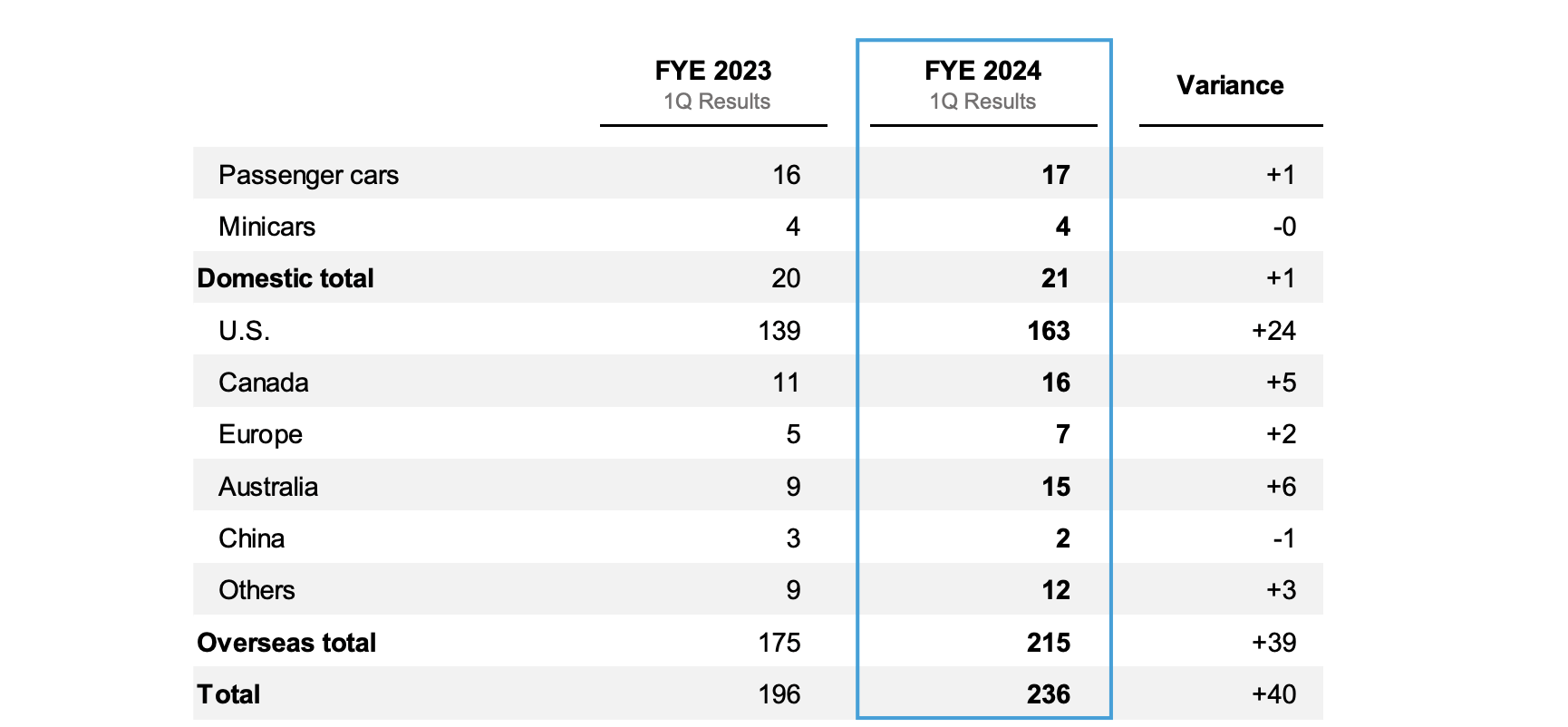

As I said in one of my earlier articles on the company, Europe and some other markets such as China remain minuscule or very small for Subaru – that is still the case for the latest results. Europe has simply been an “underfocused” market where Subaru has left space to other companies, such as KIA which has taken much of the market share from other Asian brands, while domestic or regional brands like VW (OTCPK:VWAGY) and their sister brands have much of the market share in specific price points.

Remember, Subaru was less than 37 cars from selling less than 1,000 cars in a month in all of Europe back in July of 2022, selling 1,035, and it indeed even dropped to 777 cars sold back in April of 2020, during COVID-19. The 2020 sales numbers showed a 40.24% sales drop, and the company’s market share is now down to between 0.15% to 0.17%. Even with slight improvements, as we’re seeing this quarter, this shows us how comparatively unimportant these markets are for the company. In the USA, by comparison, Subaru has 22 times the European market share, around 4%, and it continues to sell 3-5x the cars in one month in the US than it sells in Europe during an entire year.

Subaru’s US focus, aside from Japan, makes sense.

Subaru IR (Subaru IR)

At the same time, we want to be careful of just how much positivity we bake into the current results and look forward. The reason is just how much these latest results were impacted by FX. Calculating the Yen, we’re seeing a significant FX impact that more or less comes to the close level of the cost impacts, inclusive of SG&A and R&D. So if the Yen normalizes, then there is likely to be a drag on operating profit.

At a 300B Yen EBIT, and 210B attributable to owners, the company saw a significant increase – but mostly due to exchange effects. Still, the signs I see in Subaru that give me conviction for the future aren’t just the ones here, but flexibility in terms of its electrification plans, in that the company expects to go at this slower than its peers. The company’s EV targets for 2030E come to around 50% of total sales at a production of 1.2M in 6 years. Unlike some EU manufacturers which have already stopped manufacturing diesel engines, Subaru maintains its plan to produce ICE well beyond 2028 both in its facilities in Japan and also in the US. It’s also not starting up BEV until 2025E if we look at in-house in Japan, and 2027E in the US – also, a next-gen HEV production is coming online.

I have made no secret of my dubiousness for the EV push in automotive. I do not own an electric car. I went out of my way to buy the last nonelectrical Benz luxury car that I could. I have no plans to buy an EV, probably not until that car completely breaks down and they remove the pumps for diesel, which is way off. This is not due to hostility towards EVs, but rather a lack of conviction in the business model (and a personal dislike for the way the products feel and look and cost).

It looks like, as of late, I am getting some tailwind in my stance from global trends. There is an overall slowdown in EVs. Last night Ford (F) reported numbers, that fell 12% due to a stated slowdown and losing $37,000 per sold EV. Do you know what company is not losing money per sold vehicle?

Subaru, among others.

Much of the current business model for EVs seems predicated on a continued low interest rate which was around when this started. I’ve always been suspicious of any business model not time-tested through multiple economic environments, and so too this one. The warning from Ford was far from the only one. General Motors (GM) and Honda (HMC) scrapped a famous JV/partnership that was supposed to reduce costs for EVs less than 2 years after initiating it, causing warnings from battery manufacturers. Yes, Electric vehicle sales are still growing strongly, but that demand is not keeping up with the expectations of carmakers and other companies that have invested billions of dollars in the EV space.

Companies have been pushing billions into this space for years, and due to the combined whammy of inflation and unemployment as well as a potential recession, I am of the firm stance that customers are not lining up to sink their hard-earned money into a chargeable vehicle. Rather, I believe used vehicles will be repaired, and driven longer, and flexible ICE vehicles will be favored in the near term.

With a stated shift from GM to “meeting demand” rather than hitting specific volume targets, I believe the writing is on the wall here. And to anyone saying that “this is just one trend”, I can tell you the signals are popping up everywhere.

The signals in Sweden are very clear, dropping more than 10-12% in less than a year. The reason for this is very clear. The reason for the increased sales volume in EVs over the past few years has been the low-interest rates and cheap leasing costs. With increased rates and as many countries are moving alongside Sweden, which has completely eliminated EV incentives on the purchase side, the appeal is gone, and people simply don’t have the money for an expensive car.

Even if you choose the cheapest EV, you can get a 2-3 year used car of quality for 30-40% of the price. The estimate for the % of EVs of all sold cars during 2023 has been reduced by 5% back in June. I believe this is likely to continue to be revised downward.

There was in fact, a famous article here in Sweden by a large dealer, who between the 8th of November 2022 and the end of the year, did not sell a single electric vehicle. The 8th of November was when the incentive was removed.

I tell you this to build the thesis for where I see automotive going in a higher-interest world, and Subaru’s position in that world. I believe the last few years of EV push and sales were mostly a product of cheap money and good leasing incentives coupled with EV incentives that are slowly being unwound. I do not believe that this will be the standard going forward.

Because of this, I believe companies that have not abandoned ICE in a baby-with-the-bathwater sort of logic, are going to see increased interest for their products going forward.

There are few manufacturers that are clear about their plans to maintain ICE for some time. Subaru is one of them. BMW (OTCPK:BMWYY) is another, with BMW actually researching new ICE motors for release in 2027. My own, “in-house” brand Mercedes, has sadly decided not to go this road at this time.

For me, anecdotally, that probably means that my next car in 5-10 years, is going to be one of the brands that still maintains this technology – unless something wondrous happens with EV pricing and products.

So – that’s my overall, high-level view on the automotive industry. I realize that many of you may view me as a relic (despite being younger than 40 years old) with this stance, but this is what I view as likely, and why I like what I see in Subaru.

I’m not against EVs – just make them profitable and a logical choice.

Let’s look at Subaru’s valuation.

Valuation for Subaru – Attractive, even here

Subaru isn’t currently at the cheapest or most attractive levels that it’s ever been. In fact, I would say that compared to many alternatives on the market today, especially when we consider its hit/miss ratio in terms of historical statistics, there are better investments out there.

But I do believe Subaru offers one of the more compelling theses in automotive on the long-term here, given that it typically trades at a 13-14x P/E, and is currently below 8.2x, despite dropping down quite a bit.

The company yields 2.9% here, which isn’t world-beating (or even beating risk-free rates) but coupled with a 2024-2025E upside based on forecasts, this Japanese giant could certainly outperform.

In my last article, I actually raised my PT to ¥2,700, and this is the target I stick to in this article as well. Even with the challenges we can see in the current interest rate environment, I believe the path is paved, thanks to mid-term growth, to outperformance here. You can estimate the company at the lower range of its historical premium, of 10-12x P/E, at a 10.5x P/E to a native implied PT of ¥3,800, and you’d still get 21% RoR per year until 2026E (fiscal). In fact, you could stick to today’s target range of 8-9x P/E, and your returns would still be double digits inclusive of dividends.

This forms a very appealing basis for an upside – and it’s what I consider to be the reason for potentially buying more here.

Like most Japanese companies, Subaru has almost no debt. We’re talking sub-10% LT debt/cap. This adds further safety to many of the heavier-indebted European and US peers.

For comparison, the current S&P Global targets for Subaru come to a range between ¥2,300 to ¥4,100 with an average of ¥3,000. So my target is conservative. 8 analysts out of 15 are at a “BUY” for the native here. If you want to “BUY” the native rather than the ADR, which is the path that I would take, I would go for a broker that allows native Japanese trading.

Automotive, in its current state, is a tricky venture – but I believe the company offers enough of an upside and safety for us to really be able to go deeper here.

For that reason, I give Subaru a “BUY” and consider it worth going for here.

My thesis is as follows.

Thesis

- Subaru is a USA-exposed automotive company with a small aerospace arm. It has fundamentally appealing products, perhaps suffering a bit from being behind some of its competitors, and having almost no market share in Europe. But overall, great products.

- The company has seen years of negative returns, reflecting a drop in earnings. However, this is expected to reverse in 2023 and forward.

- I stick to my raised PT for the company. Subaru now has a native ¥2,700 PT, and an upside to today’s share price.

- Subaru is a “BUY” here, but no longer a cheap one.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company fulfills all of my investment criteria here except it being cheap. This still makes it a “BUY”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")