Editor’s note: Seeking Alpha is proud to welcome Market Snippet as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Ken Ishii/Getty Images News

Recommendation

We recommend a Long Position for Square Enix (OTCPK:SQNNY). This recommendation is directed toward a client seeking exposure to the Japanese RPG Gaming space, characterized by high barriers to competition in the Japanese RPG space, forthcoming cost efficiencies, and a strong presence in the Japanese market with expanding global potential.

Square Enix has been significantly undervalued following the perceived underperformance of its latest release, FF16, which resulted in a 25% decline in share price. It’s important to note that while some consider it a “failure” due to its inability to recoup costs from underperforming IP releases, FF16, by itself, is a success. Selling 3 million copies in just 6 days, it garnered critical acclaim and secured a place as one of the top 17 PS5 games of 2023 according to Metacritic.

The perceived failure is rooted in Square Enix’s history of diversifying its game genres, relying on subsidiaries to develop new IPs through their Western studios such as Crystal Dynamics and Eidos Montreal. This diversification strategy led to a decline in both game quality and financial losses. However, in a pivotal move in May 2022, Square Enix divested from these underperforming Western studios, selling these assets to the Embracer Group. This strategic decision has realigned the company’s focus on core operations that generate the most value. With a renewed emphasis on their flagship IPs and forthcoming cost efficiencies from the full adoption of the Unreal Engine, we anticipate a significant improvement in their bottom line.

Square Enix’s dominant presence in the Japanese market, global expansion potential, and strategic realignment towards its core strengths make it an appealing long-term investment opportunity. While FF16’s immediate financial returns may not have met expectations, the overall trajectory of the company remains promising, and it’s bound to regain momentum.

Investment Thesis

Strong and Diversified Triple-A IP Portfolio, leading to barriers to competition

We believe Square Enix boasts a formidable portfolio of well-established and unique IPs, including Final Fantasy, Kingdom Hearts, Dragon Quest, NieR, and more, spanning multiple platforms. Their prowess in the mobile gaming arena is evident through titles like Kingdom Hearts Union X, which boasts 1 million downloads, and FF7 Ever Crisis, with 500k downloads and plans for monetization and content updates. These IPs have consistently achieved remarkable success, with recent releases from these franchises selling an average of 3 to 5 million copies within 2 weeks. Examples include the recent mainline installment of Kingdom Hearts, which sold 5 million copies in 2 weeks, and Final Fantasy 16, which sold 3 million copies in just 6 days. Square Enix’s IPs are finely tuned to cater to the demanding Japanese RPG market, an arena where excelling outside of Nintendo (OTCPK:NTDOY) IPs can be arduous. The diversity of their IP portfolio acts as a safety net – if one underperforms, others can compensate, reducing the overall risk associated with game development. This robust and diversified IP portfolio positions Square Enix as a formidable player in the gaming industry, with dominance in the Japanese RPG segment.

Comparing Square Enix to its competitor, Sega (OTCPK:SGAMY), we find that Sega’s Japanese RPG IPs, such as Persona and Yakuza, may appear to compete with some of Square Enix’s IPs, like Final Fantasy and Kingdom Hearts. However, Square Enix’s IPs, particularly Final Fantasy and Kingdom Hearts, possess a rich history with a dedicated fanbase. These franchises have consistently delivered critically acclaimed and commercially successful titles over the years, creating recognition and trust that act as a competitive advantage. In contrast, Sega’s Persona and Yakuza IPs, while gaining popularity recently, do not have the same level of recognition. This makes Sega’s titles, for now, more akin to cult classics or niche products, making it challenging for Sega to compete on a similar scale. Notably, Yakuza does not perform as strongly as Square Enix’s titles. Another competitor is Capcom (OTCPK:CCOEY), which indeed has strong IPs, but their catalogue has a more Western appeal, featuring titles like Resident Evil, Monster Hunter, and Devil May Cry. Consequently, they do not directly compete for sales, as their target audiences differ. Capcom derives 38% of its sales from Japan, whereas Square Enix draws 66% from the Japanese market. Furthermore, Capcom lacks expertise in mobile gaming and offers a narrower range of game genres compared to Square Enix.

Square Enix has effectively reduced competition and established high barriers in the Japanese RPG space through its diversified triple-A portfolio. Square Enix has consistently raised the development timeline and costs for triple-A games in the Japanese RPG space to achieve the creative vision the auteurs desire, thereby elevating the segment to new heights. These increased budgets are essential for developing games with cutting-edge graphics, extensive content, and complex gameplay systems. Consequently, both new and existing studios face considerable challenges when competing, as they often struggle to meet the new standards set by Square Enix. For instance, Square Enix’s FF16 exemplifies new peaks in graphical fidelity and cinematic scale within the genre.

Forthcoming bottom-line improvement from the Divestment of Western Studios and full adoption of the Unreal Engine

In the past, Square Enix faced challenges due to overextending itself with the diversification of its game genres, by having subsidiaries that develop new IPs via their Western studios. This diversification led to a decline in both game quality and financial losses. However, the company took a significant step in May 2022 by divesting from these western studios, selling them along with associated IPs to the Embracer Group for $300 million. This strategic decision redirected the company’s focus toward core operations that generate the most value. With a renewed focus on their flagship IPs, we anticipate a significant improvement in their bottom line once these flagship titles are released. The company’s renewed focus seems to align with what their unannounced plans are, as revealed through an NVIDIA database leak in September 2021, which contains the names of projects the company is currently working on. It appears they are focusing on remakes of their flagship IPs, similar to Capcom’s current strategy. Capcom introduced remakes to their pipeline, resulting in a much lower COGS as a proportion of revenue in Fiscal Year 2021, and a consequent 60% increase in net income for that fiscal year. This is due to shared resources between new releases and remakes of the same flagship IPs, expediting development for both. Furthermore, remakes require less development time, as the blueprint is already established.

We can further expect an improved bottom line from Square Enix’s adoption of the Unreal Engine, signifying a transformative change in terms of efficiency and cost reduction. This decision was driven by past experiences, including the notorious 10-year development of Final Fantasy XV and the broken launch of Final Fantasy XIV. Square Enix has since resolved these issues by embracing the Unreal Engine. This adoption is evident in Square Enix’s flagship franchises like Kingdom Hearts 3, FF7 Remake, and DQ11. The Unreal Engine has 3 key benefits: Firstly it’s an open engine, enabling developers to use already made assets off one another, reducing the time to create every asset from the ground up, and fostering a cost-effective approach. Secondly, the Unreal Engine enables Square Enix to attract and integrate developers proficient in its engine. This influx of top-tier developers enhances the overall skill set of Square Enix’s teams, but also since this is an engine that anyone can access, it reduces training costs, compared to Square Enix training new hires on proprietary engines. Thirdly, the engine distinguishes itself by its stability and support infrastructure, a marked improvement over Square Enix’s previous engines. This stability not only minimizes the likelihood of delays but also ensures prompt issue resolution.

Square Enix needs to introduce this engine to its main Final Fantasy franchise, as they currently have not done so, resulting in FF16’s having high development costs. This is evident in the Q4 2023 financial results, where Square Enix’s operating profit fell by 80%. In Q1 2024, the company maintained a similar level of operating profit, which concerned investors, leading to a sell-off of Square Enix’s shares and a share price decline of up to 25%. Square Enix attributed this decline to the high costs associated with the development of FF16, which did not adopt the Unreal Engine. However, we believe they will switch to the Unreal Engine from now on, reducing the likelihood of such issues occurring in the future.

Given the importance of development costs and their impact on operating profit, this change is crucial for investors and can significantly affect share prices. In light of these developments, we believe that operating profit will improve over time, leading to an improved bottom line due to the refocus on flagship IPs and the full adoption of the Unreal Engine. We anticipate consistently higher net income by the end of FY2024.

Potential Geographical Diversification into the Western Hemisphere

We believe Square Enix currently boasts a dominant position in the Japanese gaming market, with a significant potential for organic growth by expanding its global presence. Notably, Square Enix derives only 34% of its sales from the global market, excluding Japan. This underutilization of the global market can be attributed to Square Enix’s historical approach of focusing primarily on the Japanese market. Their previous strategy involved releasing games first in Japan and then internationally, often with a significant time gap. This approach has resulted in missed opportunities, as the initial hype diminishes, and potential players might have already watched the game online.

To address this issue and significantly boost its market share in the Western gaming landscape, Square Enix should enhance their exposure to the Xbox platform. Historically, Square Enix missed out on potential sales by not establishing a strong presence on Xbox, despite the substantial Xbox user base, currently comprising around 25 million Xbox Series X/S users, with only 2% of these users hailing from Japan. This marks an excellent opportunity for geographical diversification. Mena Kato, a former VP of Sony Business Development, but now a Director of Japan Partnerships at Xbox also argues that Japanese studios need Xbox for expansion.

An encouraging development for Square Enix is the recent commitment from the CEOs of Square Enix and Xbox to ‘partner more closely.’ This suggests that future Square Enix games will be more consistently available on Xbox, a shift from past practices. Notably, games like FF7 Remake and FF16 did not initially arrive on Xbox, representing missed opportunities for increased revenues due to limited exposure in the Western market.

The recent acquisition activity by Xbox, most notably the acquisition of Activision Blizzard, signals a strong commitment to becoming a formidable competitor to PlayStation. This increased competition between PlayStation and Xbox is expected to drive both platforms to be more aggressive in expanding their user bases. While PS5 boasts a current user base of 47 million, Xbox’s acquisition of Activision-Blizzard is set to substantially boost their user numbers. As these two giants vie for dominance, Square Enix stands to benefit significantly from the accelerated growth in the non-portable gaming landscape.

In conclusion, we predict that Square Enix will significantly enhance its presence and sales in the West by consistently releasing its games on the Xbox platform. Recent discussions between Xbox and Square Enix indicate this intention, and we anticipate a considerable increase in Square Enix’s revenues due to these factors.

Q2 2024 Commentary – Nov 7th 2023

Comparing Q2 2024 to Q2 2023, we observe that the Gross Profit remains relatively consistent, maintaining historical levels seen before the release of FF16. However, there is a notable 7.1% decline in revenues. This decline may be attributed to consumer caution in purchasing digital entertainment products amid macroeconomic uncertainties.

|

Q2 2024 |

Q1 2024 |

Q4 2023 |

Q3 2023 |

Q2 2023 |

Q1 2023 |

|

|

Revenue |

597,807 |

623,735 |

662,360 |

653,931 |

640,375 |

577,458 |

|

COGS |

263,119 |

357,806 |

383,091 |

312,962 |

306,080 |

233,194 |

|

Gross Profit |

334,688 |

265,930 |

279,269 |

340,970 |

334,295 |

344,265 |

Important to note: Western Studio’s divestiture occurred in Q2 2023, during which the studios were sold to Embracer Group. Q1 2024 marked the release of FF16, resulting in four quarters of high COGS attributable to its substantial development costs.

I anticipate consistently lower COGS in the upcoming quarters, particularly with the expected release of FF7 Rebirth in Q4 2024. Thus far, there hasn’t been a buildup of higher COGS, possibly owing to the directors behind the series having extensive experience in triple-A development. This contrasts with the director of FF16, who had primarily worked on MMOs. Additionally, the use of the Unreal Engine in FF7 Rebirth has likely contributed to smoother development, eliminating proprietary engine issues and potential delays.

|

% |

Q2 2024 |

Q1 2024 |

Q4 2023 |

Q3 2023 |

Q2 2023 |

Q1 2023 |

|

ROA |

8.86 |

1.96 |

1.89 |

9.54 |

7.51 |

9.57 |

|

ROE |

13.1 |

8.04 |

3.64 |

8.89 |

28.34 |

25.69 |

|

Gross Profit Margin |

55.99 |

42.64 |

42.16 |

52.14 |

52.20 |

59.62 |

|

EBITDA Margin |

18.49 |

5.64 |

5.42 |

18.62 |

15.11 |

21.81 |

|

EBIT Margin |

16.49 |

3.62 |

3.44 |

16.56 |

13.12 |

19.28 |

|

NI Margin |

11.96 |

7.35 |

3.27 |

7.51 |

23.86 |

24.51 |

Huge declines in ratios like the above did result in a 25% share price fall, with costs attributed to the development of their recent flagship title FF16.

The above table shows that for Q2 2024 margins are rebounding to normalized historical levels.

Valuation

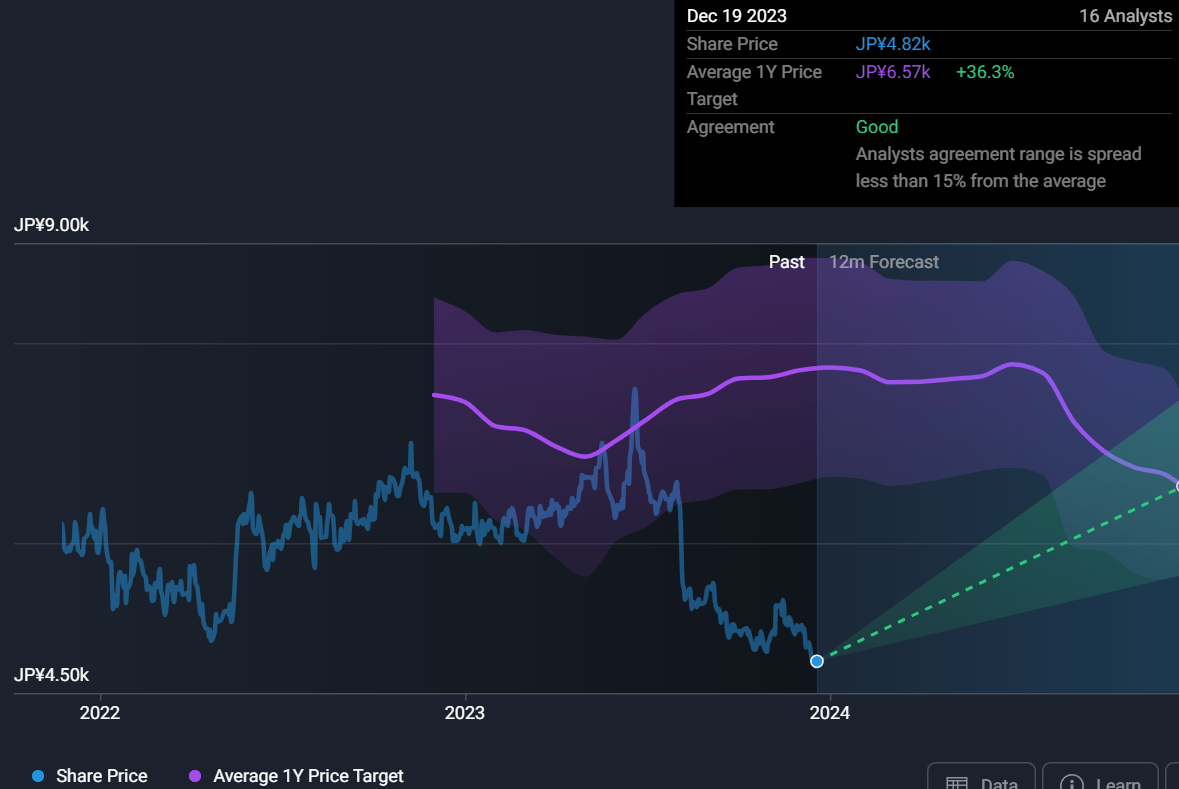

Analyst Consensus and Price Forecast

Analyst Forecast (Simply Wallstreet)

In our thesis, we concentrate on SQNNY, but the above forecast is for 9684.T; as SQNNY has no analysts and is on the OTC Market.

|

Intrinsic Valuation (SQNNY) Price Target: $22.18 Current Price: $16.68 The Upside: 33% Derived from 3-Statement model DCF |

Analyst Forecast (9684.T) Consensus Target: 6570 JPY High End: 8500 JPY Low End: 5400 JPY |

Income Statement Assumptions

Due to fierce competition and piracy, we expect the publications segment revenue to fall over time, so we price a 5% fall per year until 2028 as opposed to stagnation or a growing segment then if there is still a high implied upside in DCF, then there is more conviction.

As management gauges demand and supply later, we assume growth in merch lags growth in the digital entertainment segment, as also shown in the data.

Past COGS ranges from 49% to 52% of sales, and we assume 49%. Though thesis point 2 is based on future cost efficiencies, so we could go lower, we make a conservative assumption so that if there is still a high implied upside in DCF, then there is more conviction.

The Digital Entertainment segment projected revenues include specific products that we believe will be released each year, as well as revenue estimates based on past sales data and our judgement.

Income Statement Digital Entertainment Assumptions

For each fiscal year, we project sales in the Digital Entertainment segment by taking last year’s sales, reducing them by 20%, and then adding the anticipated sales of both expected and unexpected new products. We assume a 20% decrease in sales, as in the previous fiscal year (FY2023), there was a 27% decline attributed to a drought in flagship products. However, we do not anticipate a similar level of flagship scarcity in the subsequent years, so we have chosen a more conservative estimate of a 20% decline.

We assume that FF16 will sell an additional 2 million units, reaching a total of 5 million by the end of FY2024. This is comparable to the number of sales FF7 Remake achieved on PS4 alone. Additionally, we include an assumption of 4 million sales for FF7 Rebirth by the end of FY2024, which concludes in March 2024

For FY2025, we assume that FF16 will be released on PC with 2 million units sold, and FF7 Rebirth on PC will also achieve 2 million units sold. This assumption is based on FF7 Remake selling 2 million units when released on PC. The FF14 MMO DLC, Dawn Trail, is expected to be released; however, as it approaches the end of its MMO lifecycle, we anticipate that only 50% of the 1.3 million completionist player base will purchase the DLC. Despite 2.5 million preorders for the most recent expansion, we aim to remain conservative and not expect an increase in the player base. Additionally, we anticipate a drought in new Triple-A releases, which is likely to lower revenues, similar to the situation in FY2023.

For FY2026, we assume the releases of DQ12 and KH4. DQ11 sold 3.4 million units in Japan across all platforms in a little over a year, with an additional 0.6 million units sold globally after 2 months. Over a span of 2 years, it accumulated a total of 6 million units sold. Based on this, we expect DQ12 to achieve 4 million units in the first week. Global sales are likely to see an improvement, as it will have a simultaneous release with Japan, unlike DQ11. Additionally, the IP’s popularity has grown due to various re-releases. KH3, having a 10-year wait for fans, sold 5 million units in its first week. However, we anticipate that KH4 may sell fewer units due to nostalgic fans moving away from the KH franchise and the mixed online reception of KH3. As a result, we assume KH4 will achieve 3 million units in the first week. It’s worth noting that first-week sales are crucial, as the majority of game sales come from preorders, with some exceptions.

For FY2027, we assume the releases of FF7 Part 3 and FF9 Remake. While both have not been officially announced, FF9 Remake was legitimately leaked via an NVIDIA Database leak. Additionally, FF7 Remake was stated by its director to be released in three parts, and if Part 2 proves to be successful, we anticipate a sequel within 3-4 years. We expect FF9 Remake to sell 3 million units for the year, and FF7 Part 3 Remake to sell 4 million units for that year.

For FY2028, in the absence of an updated roadmap, there appears to be a flagship drought, a phenomenon that frequently occurs at Square Enix. However, with their new vision, we are confident that they will generate more releases. For now, we assume FY2028 sales to mirror those of FY2027 but with a 20% decrease.

DCF assumptions

Since there is no debt in Square Enix, we also assume no debt in the future, so WACC = Cost of Equity.

CAPM: 7.4%=4.22%+0.55(10%-4.22%)

Though ROE * RR is 6.56%, we assume in perpetuity growth is 3%.

By relying on our assumptions, we can calculate Free Cash Flow to Firm (FCFF) from 2024 to 2028. Subsequently, we derive a terminal value and discount all these cash flows to the present using the Weighted Average Cost of Capital (WACC). With the calculated Enterprise Value, we then compare it to the current Enterprise Value of the firm to ascertain the degree of undervaluation. Finally, we compare the stock’s current price with the degree of undervaluation to determine its intrinsic value.

Multiples compared with competitors

|

Square Enix |

Sega |

Capcom |

|

|

Trailing P/E |

21.9 |

7.3 |

21.2 |

|

Forward P/E* |

22.3 |

9.0 |

21.6 |

|

P/S |

1.6 |

0.9 |

6.3 |

|

D/E |

NA |

42.8% |

4.2% |

|

ROE |

8.4% |

18.1% |

27.8% |

|

ROA |

5.5% |

9.0% |

18.4% |

*Forward P/E for Sega and Capcom provided by Yahoo Finance, while Square Enix Forward P/E found using our model.

Though Square Enix currently underperforms in metrics such as Return on Equity (ROE) and Return on Assets (ROA), these metrics are poised for substantial improvement by FY2026 and beyond. This optimism is anchored in the points I’ve outlined in thesis points 2 and 3, where the company is embarking on a path of transformation.

Risks

Square Enix’s success and strong track record with their Diversified Triple-A IP Portfolio is owed much to the exceptional talents within the company, as those IPs can only maintain their value and relevance due to key creatives. Therefore, a risk in the thesis is that the departure of any key individuals could result in a significant intellectual capital outflow, which would harm the longevity of Square Enix and the strength of their IPs. This is an issue Konami, a competitor in the HD gaming space faced when Hideo Kojima departed. However, Square Enix stands out as it has a depth of talent and diversification in its creative team, such as Tetsuya Nomura, Naoki Yoshida, Yoko Taro, and others. This diversity and depth of talent means that even if a key figure were to leave, there are capable individuals within the company who can step in and continue producing high-quality content.

Another risk is that though Square Enix has been adopting the unreal engine more, they haven’t used the engine in its main Final Fantasy franchise, resulting in FF16’s having high development costs. This is evident in the Q4 2023 financial results, where Square Enix’s operating profit fell by 80%. In Q1 2024, the company maintained a similar level of operating profit, which concerned investors, leading to a sell-off of Square Enix’s shares and a share price decline of up to 25%. Square Enix attributed this decline to the high costs associated with the development of FF16, which did not adopt the Unreal Engine. Square Enix has been trending towards using the Unreal Engine more with franchises such as Kingdom Hearts, Dragon Quest and FF7 remake, but we could see high development costs if the mainline Final Fantasy Franchise continues to use proprietary engines. And so the issue of their ballooning cost would persist.

Another risk to the thesis regarding potential Square Enix exposure to the Xbox platform is that Sony could continue offering exclusive temporary deals that could limit the reach of Square Enix games on Xbox. However, the current trends in the industry suggest a growing partnership between Square Enix and Xbox, making this a promising avenue for the company’s expansion into the global gaming market.

With SQNNY trading on the OTC Market with poor trading volumes and high illiquidity, there’s a risk of lagging market appeal, potentially hindering its ability to rally compared to 9684.T. If a price catalyst triggers a surge in SQNNY value, persistent illiquidity might force investors to sell at a discount. Moreover, entering a position at a higher price due to illiquidity could diminish potential returns. In contrast, competitors like CCOEY and SGAMY appear to avoid such illiquidity issues. As market sentiment on Square Enix improves and catalysts materialize, we anticipate a stock price rally and a reduction in illiquidity concerns

Catalysts

While Q2 FY2024 earnings were released on November 7th, the primary catalyst for the market to address its undervaluation is expected to be earnings announcements in FY2026, which begins April 2025 as by then they would be full steam on Flagship IPs with new releases from FF7 Rebirth, Dragon Quest and Kingdom Hearts, with turnarounds faster than prior years, multiple PC releases of existing games like FF16 and FF7 Rebirth and a clearer remake roadmap we believe would make Square Enix really profitable.

Another catalyst could be that since the industry is facing mass consolidation from the Activision-Xbox deal, we could see announcements of Square Enix getting acquired, which would in turn rally the stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")