krblokhin

My Thesis

Usually, I’m comfortable investing in companies with an extensive moat, ones that can deliver great results no matter what stands in their way. However, sometimes, I like to invest in profitable companies that may not have the widest moat but offer an appealing price. I believe that Sprouts Farmers Market (NASDAQ:SFM) has a management team that knows what to do, and based on its returns this year, it seems like many investors share that belief. Even after a 33% return year-to-date, I believe the current price compensates for the lack of the wide moat I typically seek. This article differs from my previous ones because it focuses more on value play than quality at a reasonable price.

The Business

Sprouts Farmers Market is a retailer that caters to health-conscious customers. It operates stores in a unique format that resembles a farmer’s market. The company sells healthy and organic products, without featuring major CPG brands in their catalog.

Sprouts has its private label, which offers better profit margins, and it accounts for 20.5% of total sales. We’ve seen from brands like Kirkland (COST) and Amazon’s private label (AMZN) that retailers often embrace this strategy because it enhances profitability. Since Sprout’s suppliers are not large CPG brands, SFM can negotiate for better prices from these smaller suppliers, thus achieving greater profitability.

Another operational move highlighted by SFM’s CEO in their recent conference call is their strategy to establish locations close to their distribution centers, thereby improving the freshness of their food.

Sprouts operates in a highly competitive market, with a strong emphasis on serving two primary markets: health enthusiasts and innovation seekers. These two markets are estimated to be worth around $200 billion, and their growth potential is expected to increase as more people become conscious about their health.

Another crucial aspect of SFM’s business is its e-commerce division. E-commerce sales are outpacing physical sales in terms of growth, and this is even more significant when considering the following facts:

Our research shows an online delivery customer is a valuable omni-channel customer, as nearly 80% of our online customers also shop in store. And as a bricks and mortar customer starts using e-commerce, their spending increases more than 30%.

In the past, SFM had a strategy of distributing coupons to boost in-store foot traffic. However, the problem was that the customers who came in response were of low quality, as they would only return if more discounts were offered. The new strategy, introduced by Jack Sinclair, aims to target high-quality customers, specifically the ‘health enthusiasts’.

Another operational initiative advocated by the current management is to reduce the size of new stores, making them less expensive to build, decreasing non-selling space, and cutting occupancy and operating costs.

Regarding its marketing efforts, the company is focusing on the younger generation, collaborating with 270 health influencers in 2022.

Although it may not have a wide moat, I appreciate this business due to its recurring revenue and sales which are less susceptible to economic downturns. It’s worth noting that current sales even surpass the average of the past five years, with Q3 sales showing an 8% growth.

Growth

SFM has two strategies for increasing its top-line growth. The first involves expanding its share count. Currently, SFM primarily operates in the Southwest and Southeast United States. The company aims to increase its store count by 10% annually, and as of October, it had 401 stores. Management expects to add 30 new stores in FY23.

The second option is to enhance same-store sales growth, which historically has grown slightly above inflation, at about 3% in comparable growth. In the last quarter, comp sales grew by 3.9%, which is a positive sign. However, considering that the Health & Wellness Food Market is projected to grow by more than 9% by 2030, there’s room for improvement.

If SFM can achieve its store count goal and maintain a similar pace of same-store sales growth as in the past, we could expect double-digit top-line growth, a milestone they haven’t reached in recent years but might achieve with the current high-quality customer strategy.

Regarding FCF growth, while they have plans to reduce costs, such as store size reductions, I don’t base my valuation on margin expansion. Therefore, FCF should grow alongside long-term revenue growth.

One key factor that makes SFM’s stock relatively inexpensive is its share buybacks, reducing the share count by about 5% annually. This enhances FCF per share growth, which is a driver of stock appreciation. A similar approach has worked well for companies like AutoZone (AZO), which reduced their share count over the past decades, resulting in outstanding returns, even in a slow-moving market.

By combining the growth of store count, comp sales, and share reduction, we can anticipate a 17% FCF per share growth, in an optimistic scenario. However, I will employ a more conservative approach in my valuation.

Profitability

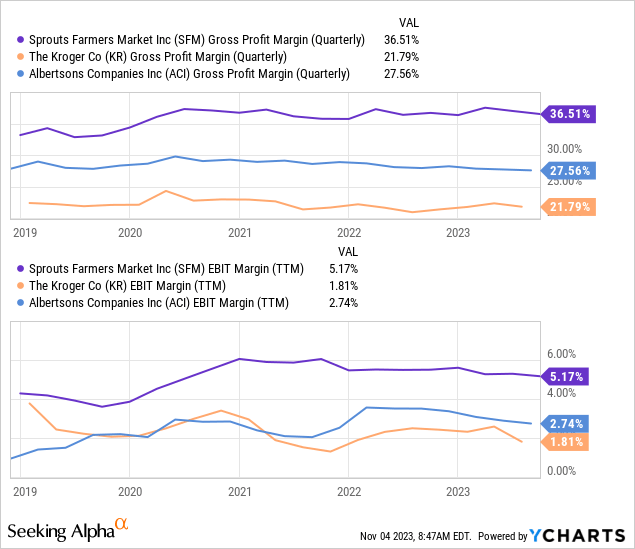

I like to examine two important and related factors that contribute to the business’s resilience and demonstrate its robustness. The first factor is high and stable margins. When a business maintains high margins, the management can focus on future growth opportunities without worrying that it will significantly impact current profits. Furthermore, during rough economic times, it can avoid cutting dividends, buybacks, or capital expenditures for growth investments.

As you can see from the chart, SFM maintains stable margins, which is excellent in my opinion. It also enjoys higher margins compared to other grocery retailers in America. While other main competitors like Whole Foods and Trader Joe’s are not public, SFM’s margins appear to be on the higher end of the spectrum among grocery retailers, similar to Whole Foods’ margins ten years ago.

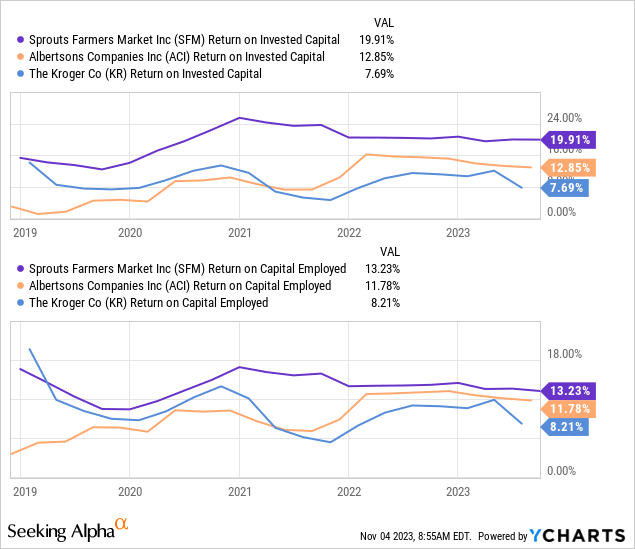

High margins, in my opinion, play a significant role in driving the main value creation ratios, alongside top-line growth, and one of these ratios is return on capital. SFM demonstrates high ROCs relative to its industry, and what’s even more important, they are stable. Recent research by Morgan Stanley has shown that a high and growing spread between ROIC and WACC serves as an indicator of stock outperformance. I am hopeful that recent operational initiatives, along with comp sales growth, will enhance SFM’s efficiency and consequently improve these ratios, ultimately creating more value.

Cannibal

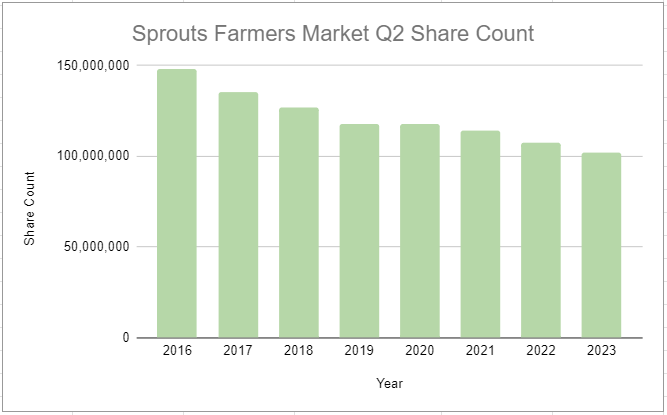

SFM is doing a great job deploying its cash. Share repurchases are a great way to enhance FCF per share growth, especially when the stock is believed to be undervalued. Annually, SFM has reduced its share count by 5%, which is even more aggressive than other notable buyback leaders like Apple, Lowe’s, and AutoZone.

Since 2016, Sprouts has consistently reduced its share count at a 5.2% annual rate, bringing the number of outstanding shares down from 148 million to 102 million.

Share count (chitchat money)

These buybacks are a significant factor supporting my belief that SFM is undervalued.

Solvency

SFM boasts a robust balance sheet with negative net debt, capable of covering its interest nearly 30 times. It maintains a current ratio of more than 1 and an Altman Z-Score above 3.

Furthermore, SFM’s free cash flow is more than sufficient to repay its debt twice over.

Valuation

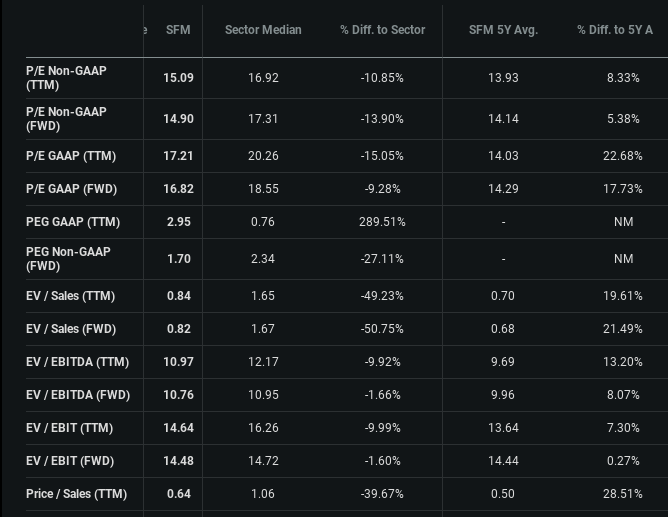

Compared to its historical multiples, SFM’s strong performance over the past year has pushed its valuation a bit higher, with most multiples surpassing their historical averages. I prefer to invest in companies when they are trading below their historical averages, as it indicates potential for multiple expansion. However, an improvement in the business’s operations can lead to even higher multiples than in the past.

multiples (Seeking alpha)

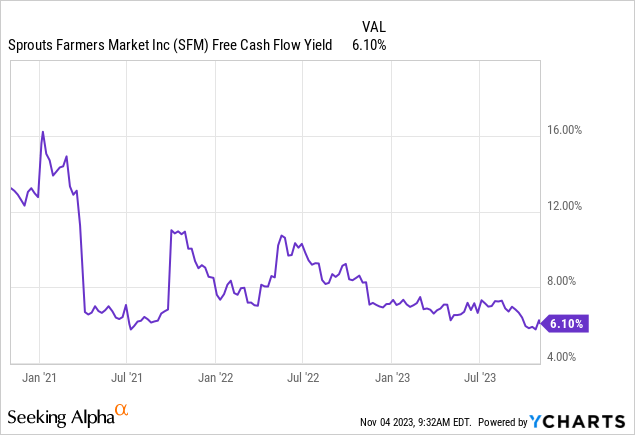

One of the most favorable ratios is the Free Cash Flow yield, and SFM boasts a high FCF yield, indicating that you are receiving a substantial amount of FCF for your investment, or that the stock is undervalued. A ratio higher than 5 is considered favorable, and SFM’s FCF yield is even greater than 6.

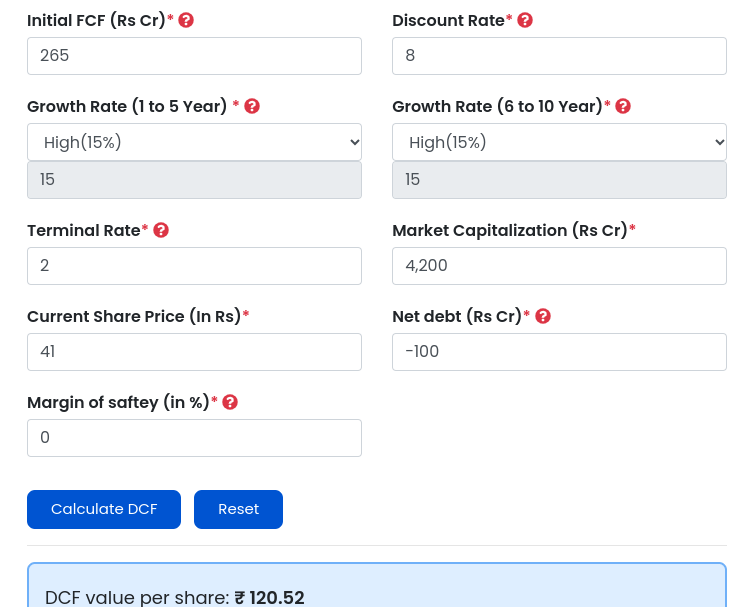

For the DCF (Discounted Cash Flow) model, I will use the following calculations for two scenarios: a bullish case and a bearish case.

In the bullish case, assuming 3% comp growth, 9% store count growth (a bit under management’s goal), and a 3% annual reduction in share count, the FCF per share growth will be 15%. The WACC is 8%, and the terminal growth is 2%. In this fairly optimistic scenario, where everything goes according to plan, the stock appears to be significantly undervalued with an intrinsic value of $120, making it almost 200% undervalued. However, I acknowledge that this prediction may not be entirely realistic. Now, let’s consider the more bearish case.

DCF (finology)

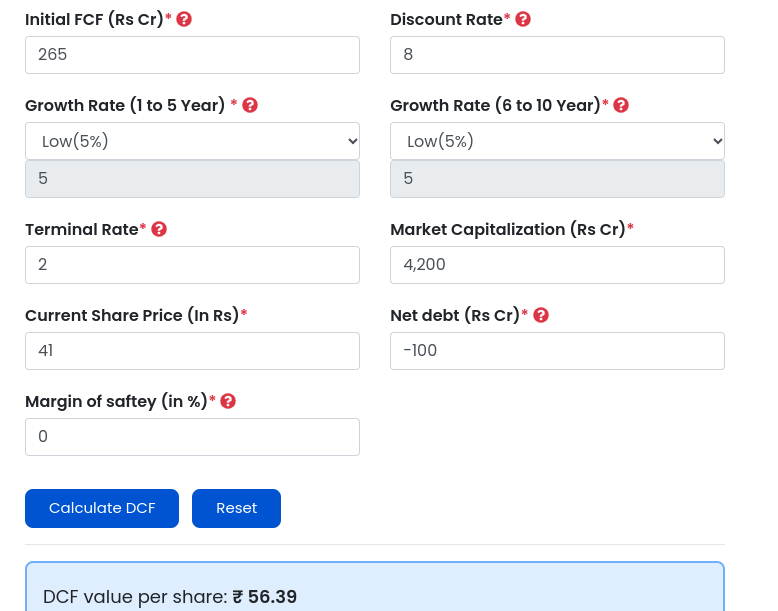

In the bearish case, assuming that everything goes wrong, with unsuccessful comp growth, delayed store openings, and limited FCF for buybacks, I project a 5% FCF per share growth. All other inputs remain the same. Even in this more pessimistic scenario, the stock still appears to be undervalued by 36%.

In my opinion, this risk-reward balance is favorable, especially given the predictability of this business. I anticipate that it will continue its recent trend of outperformance.

DCF (finology)

Risks

While it is generally a predictable business, there are still some inherent risks to consider:

1. Inflation or a recession could affect the buying behavior of health-conscious individuals, causing them to reduce their purchases of pricier health food in favor of cheaper consumer packaged goods (CPG).

2. The store model might not perform as well in the northern states compared to the southern ones, potentially leading to margin contraction.

3. If comparable sales don’t improve, it could undermine the company’s future growth prospects.

Apart from these considerations, I don’t see any major risks for this relatively straightforward business.

Conclusion

While Sprout may not be the ideal wide moat business I typically seek in my investments, its simple formula of comp sales growth, store count growth, and buybacks is quite appealing to me. Additionally, it boasts high and stable ROCs in comparison to its competitors. What truly caught my attention is the stock’s perceived undervaluation, where even the bearish case seems bullish. Consequently, I’ve decided to rate it as a STRONG BUY.

Currently, I don’t hold the stock, but I’m considering starting to buy it soon. I’d love to hear your thoughts on this one.

Q2 2024 Earnings Call Transcript")