PM Images

Shares of Sprinklr, Inc. (NYSE:CXM) plunged today despite the company beating EPS and revenue expectations in fiscal Q3 2024 and raising the full-year guidance revenue and EPS guidance. This was because the beat-and-raise came along with a warning of tougher macro conditions that are impacting customer spending and deal sizes in fiscal Q4, and with the company acknowledging it is making slower progress on some of its other go-to-market initiatives. These factors have made management guide for 10% revenue growth in fiscal 2025 versus the 16% consensus at the time of the earnings report.

While I agree that this kind of reset in expectations deserves a negative reaction, a 30%+ plunge seems admire an overreaction and management maintained the fiscal 2027 guidance for subscription revenues exceeding $1 billion, or a 15% CAGR from fiscal 2024. Sprinklr was one of my active Trading Ideas in our Investing Group, and I took a small loss as I sold half of my position ahead of the earnings report and the other half today at the open. Trading Ideas are focused on short and medium-term momentum, and this plunge ruined the momentum, and I also want to limit losses on trading positions to a maximum of 8-10%.

And while recovery may take some time, I continue to see Sprinklr as well positioned to create value in the medium- and long-term and believe this week’s guidance for next year resets expectations and sets the stage for the company to beat-and-raise throughout fiscal 2025 (calendar 2024).

Sprinklr’s fiscal 2025 outlook overshadows a beat-and-raise quarter

Fiscal Q3 2024 results and the boost in full-year guidance made the earnings report look admire the traditional Sprinklr quarter. The company sets the stage at the start of the year by guiding conservatively and then beating the revenue and EPS guidance and raising the full-year guidance range each quarter.

Total revenues grew 18.5% Y/Y to $186.3 million, beating the analyst consensus by $5.9 million. As is usual, the beat was driven by strong subscription revenue growth which grew 22% Y/Y to $170.3 million. Non-GAAP EPS was $0.12 and it handily beat the $0.07 consensus.

As a result of the strong year-to-date performance, management increased the full-year total revenue guidance range from $719-721 million to $725.5-727.5 million, and subscription revenue guidance range was increased from $658-660 million to $664-666 million. Similarly, the full-year non-GAAP operating income guidance range was increased from $65-67 million to $80-82 million, and the non-GAAP EPS guidance range from $0.30-0.31 to $0.36-0.37.

All was well after this earnings report and there was little change in after-hours trading until the earnings call started. There, management threw cold water on investors and Street analysts by saying it is seeing a more difficult end of the year macro environment. They acknowledged that they have made slower progress on some of the other go-to-market initiatives focused on the core product suites. These factors are expected to have an impact on near-term growth and have resulted in the company setting the preliminary guidance for fiscal 2025 to 10% growth over the previous year versus the analyst consensus of 16%.

These comments had a devastating impact on the stock and it lost a third of its value in a day. Management reiterated the guidance for reaching $1 billion in subscription revenue in fiscal 2027, which translates into approximately 15% CAGR in the next three years and suggests growth will speed up after the next few quarters which are expected to be more challenging as the company adjusts and executes its growth strategy.

Importantly, there are no changes to the market opportunity or competitive landscape. If this is a matter of execution, it can be resolved, and based on the company’s execution to date, I believe that this short-term pain should result in long-term gains.

And regarding customer behavior, this is a phenomenon seen across the global economy. Customers remain very cost-conscious in the near-term and this has resulted in incremental pressure on renewals as customer make downward adjustments to spending levels with Sprinklr. This is unlikely to change in the next few quarters and remains a headwind for growth rates, but should the situation better in the back half of calendar 2024, we could see growth reacceleration, driven not only by improved macro conditions but also by the company resolving the go-to-market execution issues it is currently facing.

I also think that management has made a tough but reasonable decision to reset expectations sooner rather than later and to set the stage for their traditional beat-and-raise guidance policy which would not be possible in March when the company usually provides the guidance for the next fiscal year. The 10% growth is also the preliminary guidance, and it will be updated in March when the company reports fiscal Q4 2024 results.

Conclusion

Shares of Sprinklr could remain in the penalty box in the following months due to the reduced growth expectations for next year, but I believe that the market has overreacted and that this plunge sets the stage for a successful 2024 because there are no real changes in the Sprinklr platform value proposition, and potentially even more successful 2025 as the company addressing the execution issues and macro conditions potentially improving could guide to growth reacceleration.

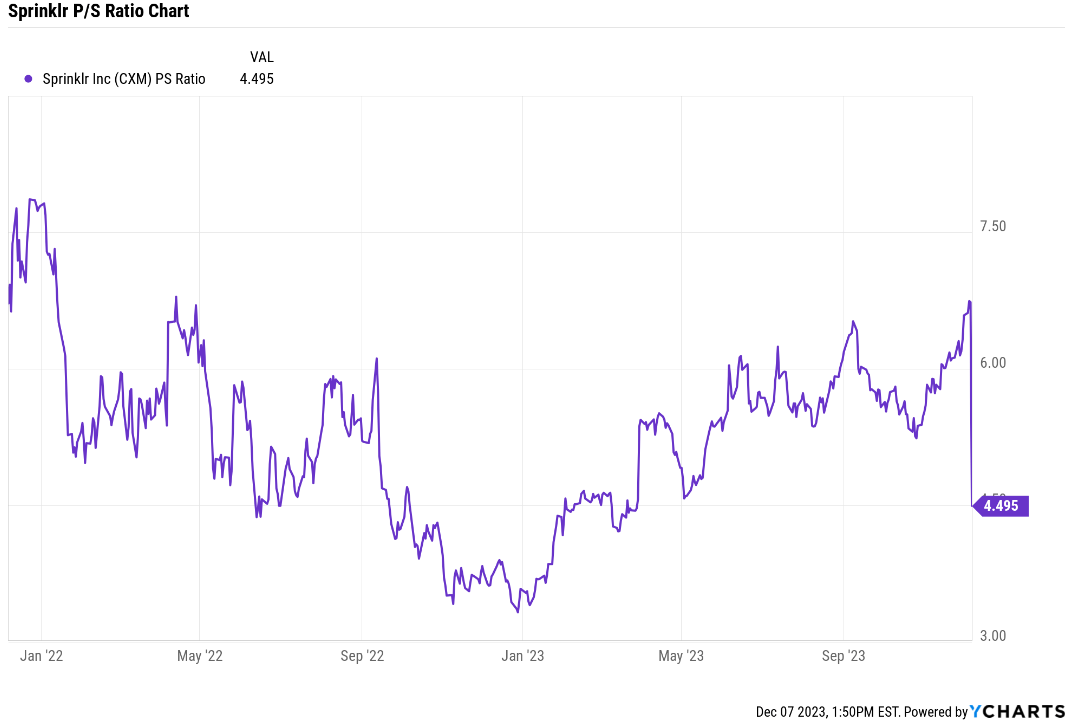

The stock was successfully re-rating higher as I suggested in my initial article in May, reaching a P/S ratio of 6.5 (or EV/revenue ratio of nearly 6). Should the story evolve the way I am suggesting today – expectations reset followed by beat-and-raise throughout fiscal 2025, we could see the stock back to recent highs and long-term, Sprinklr reaching a market cap of $6-7 billion in three years, assuming the company does reach more than $1 billion in subscription revenue in fiscal 2027, which translates to the stock reaching low to mid-20s.

Ycharts

The key risks during this period are worse-than-guided execution and macro conditions taking a turn for the worse and advance impacting growth rates and Sprinklr, Inc.’s valuation.

Q2 2024 Earnings Call Transcript")