Ethan Miller/Getty Images Entertainment

Introduction

Sphere Entertainment Co. (NYSE:SPHR) reports their fiscal Q2 numbers for the period ended Dec 31st, 2023 on Monday February 5th before the open. This is a key earnings report, because it’s the first quarterly report that encompasses an entire quarter of operations. Market/street expectations were originally very soft for the quarter, but have since been revised upwards dramatically as the venue has built up its audience and offerings. I’ve been covering Sphere since it opened, and you can review my previous works:

SPHR Fiscal Q2 Numbers

The company did not provide financial guidance for Q2 during their Q1 call, but did provide a plethora of information on Dec 5th when they did their debt offering. Here’s the key part:

Company Reports

The revenues and margins coming from the two major business lines (U2 and Sphere experience) were much higher than market expectations. The most important summary of this is that the company said they expect the Sphere Segment will report positive adjusted operating income. At the time, market expectations were that the company would lose $15-$30M dollars in the quarter.

This is crucial, because the Street has basically always had the view that Sphere would not be profitable early, and would require significant growth/margin expansion to become profitable in the future. If you’ve reviewed my previous works, that thesis has never made sense, and the market consensus is slowly coming on board with that. The story has gone from “can this money-losing Sphere manage to work really hard to turn a profit” into “can this money making Sphere flex its operating leverage and generate a massive profit?”

Mentally, I’m breaking the outcome of Q2 into these three buckets:

- Sphere Adjusted Operating Income (AOI) $0mm to $10mm is the general market/Wall Street consensus

- Sphere AOI of $10m to $20m is what I expect (small beat)

- Sphere AOI of $20m+ would be a very large beat

Note this is Sphere segment AOI, the other segment, MSGN, has a lot of volatility but does not account for a large % of the valuation of SPHR co, so as with most of my analysis, it is generally ignored. The Sphere segment results are what will primarily drive the stock.

Kevin’s Q2 Numbers

I think a material beat for Q2 (above $0 AOI) is possible for three primary reasons:

- Company issued guidance on Dec 5th (2/3 through the quarter) that they would be AOI positive. They still had 26 days of uncertainty left, and they were confident that they would end up positive. You either do this because you’re very confident of a healthy beat, or you do it because you’re being very aggressive with your guidance. The company has never been aggressive with guidance, it would be unusual to start now.

- Sphere Experience revenues during the Christmas/New Years period were extremely strong, something that the company probably didn’t expect or bake into their expectations. This was probably a $5mm+ windfall of pure gross profit.

- SG&A should run light as they’re able to move more of the Sphere Burbank costs into Direct COGS, and capitalize some of it (production of two new Sphere Experiences).

Analyst numbers

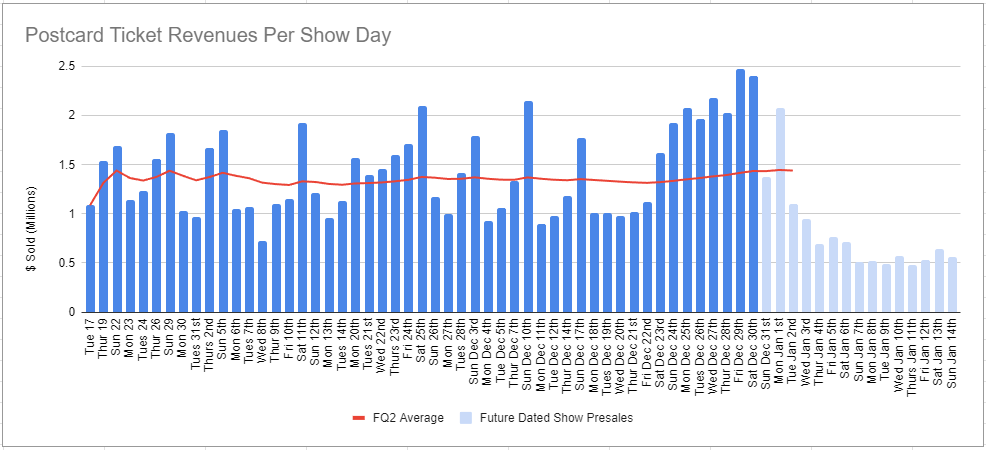

Note: You can see the Dec 23-Jan 1st period of very high ticket sales. They wouldn’t have expected this with any certainty when they gave guidance on Dec 5th.

Big Picture

As the numbers start to be realized and the Street calibrates on the “new normal,” we can finally move the conversation to the future of Sphere and its growth opportunities. While it’s not precisely in the context of the fiscal Q2 earnings, here are some big picture thoughts:

- Sphere’s profitability should improve dramatically over time. Their deal with U2 was very artist-friendly to entice U2 to take the risk of an unknown venture/venue. Now that Sphere is established, they can take a larger cut from future artists. There is only 1 Sphere, while there are many artists that are interested in performing. And other venues are not remotely close substitutes.

- Some analysts have pointed to a lack of “big blockbuster” names having signed residencies with Sphere to date. This is unrealistic, as the Sphere only “established itself” in October/November 2023. Blockbuster artists have busy schedules and aren’t available to book something in 3-6 months, never mind the fact that they want to get this right by not rushing it. The big artist residencies are coming soon.

- Apparently Cirque du Soleil ticket sales have softened since the launch of Sphere – which makes sense given they’re fighting for the same “night show” crowd and Sphere’s 20,000 seat theater soaks up a lot of demand. The problem for Cirque is that their shows have a high variable cost to operate (pay all of those very talented artists). As their numbers fall below a certain occupancy %, they need to cut shows, which creates more space for shows like Sphere Experience.

- In its first-year operating, Sphere will be featured as part of: F1, Grammy’s, the Superbowl, NHL Draft, MMA, with much more to come. They’re very quickly cementing themselves as a “culturally relevant” venue versus a “Las Vegas tourist trap.” The long-term future is very different if they succeed at the former vs the latter.

- The Phish and Dead & Co residencies feature multi-show runs that are unique, which pushes fans to purchase tickets for the Thursday, Friday, and Saturday show (versus 3 sequential shows with repeat content). This is quickly turning the Sphere into the primary purpose for people to come to Vegas instead of something to do while in Vegas. If this is successful, it becomes very relevant for the city of Las Vegas, and they will get additional resources/support due to their stature in the city.

- Sphere 1 has exceeded expectations and is quickly on its way to be a profitable powerhouse. That makes the probability of Sphere 2, 3, 4 etc. much higher, which makes the levered operating model even more valuable.

Big Picture, Bear Case

- The bear case is pretty straightforward: Sphere is a fad and while it’s busy right now, very quickly people will become “tired” of it. Occupancy rates will fall, revenues fall, margins flip to negative, and the facility loses money.

The main problem with this case is it assumes the following:

- On launch, Sphere’s operations are already optimized. In reality, over the next 3-12 months they’ll find operational efficiencies to save money, better ways to deploy marketing spend etc.

- U2 is the best act that they can get. There are so many acts that are so much bigger, and fans as well as artists have expressed huge interest in Sphere residencies.

- Postcard from Earth is the best in-house content they’ll produce. Credit goes to Aronofsky for taking the risk and making a film in a completely unfamiliar medium. Over time the Sphere team and directors will learn how to use the 16K immersive screens to improve story telling, plot, etc.

- Since Sphere 1 will fail, they will never build Sphere 2. The reported interest in expansion Spheres is quite robust, and the numbers coming from Sphere 1 justify additional builds. This is a “Go big or go home” business model and the going big is winning.

Summary

I’m looking forward to seeing the Sphere Entertainment Co. fiscal Q2 numbers on Monday Feb 5th. How the market reacts to the numbers (both on the event, and the days following) will be very interesting to observe. I think pretty soon, the market will be moving away from obsessing about the short-term numbers, and thinking more about the big picture growth story. That can/would lead to significant multiple expansion.

In the next 8 weeks I think we can see these catalysts:

- Market (quants, algos, etc.) adapting to a profitable Sphere. They still think residencies are loss-leaders with bad economics for Sphere.

- Tailwind from clickbait media (Headline: “Sphere goes from $100M loss to $10M profit”)

- Tailwind from U2 Performance at the Grammy’s

- Tailwind from Superbowl media appearances

- Tailwind from Analyst upgrades

- A large residency announcement for July/August 2024 (after Dead & Co finish). Most likely candidates: (Harry Styles, Beyonce, Miley Cyrus).

- Big sets of media reviews from Phish and Dead & Co. Everyone wants to know if U2’s visual success can be “repeated.” This seems like a forgone conclusion to me. This will also create more FOMO for other artists to sign.

In terms of valuation, I’m still holding firm on my $70 price target, and think there’s significant room for upside to this target if they build multiple Spheres, or expand their ad sales, or sell the naming rights, or build consistency into their live music business, or produce a blockbuster film.

Q2 2024 Earnings Call Transcript")