nd3000/iStock via Getty Images

Investment Thesis

In continuing our coverage of Spectrum Brands Holdings (NYSE:SPB), we rated the stock a Buy on the back of its focused approach underpinned by strength in its Global Pet Care (GPC) business and stability in the Home and Garden business, along with relative valuation comfort. The company reported a strong start to FY24, beating the consensus expectation across the top line and bottom line, further demonstrating its continued momentum. We reiterate the stock a Buy on the back of visible signs of business turnaround and bottom line improvements along with an inexpensive valuation.

Strong Start to the Year

SPB reported a strong start to FY24 with a solid beat across parameters amidst signs of stabilization within its troubled segments. It reported an organic sales decline of 4.6% with the Home & Personal Care (HPC) and Home & Garden segments faring better than feared while the GPC business performing in line with expectations. Additionally, segment profitability came in much better than anticipated, particularly within HPC and Home & Garden segments. Gross margins shot up by over 6 percentage points primarily as a result of input cost inflation as well as lower cost inventory, pricing actions and exit from low-margin SKUs in certain segments. This helped them post an Adj. EBITDA more than doubled to $84 mn compared to $40 mn in the corresponding quarter last year (excluding investment income Adj. EBITDA still jumped by 50% YoY to $61 mn). This in turn enabled them to post a consensus beat on the EPS front by a sizeable margin, posting at $0.78 compared to $0.39 expected.

Balance sheet position remained strong with the company ending in a net cash position, again with $1.4 bn in debt as well as $1.4 bn in cash. The company reiterated its full-year guidance and continues to expect a low single digit decline in sales while EBITDA is expected to grow by high single digits driven by lower cost inventory partially offset by brand investments. The worsening outlook on freight expenses with ocean freight contracts expected to be renewed between May-September is likely to have a potential impact in H2 2024 (~$10 mn headwind) but the full impact of it is going to be flowing through in 2025. This is largely as a result of its 50%+ exposure in GPC and ~90% in HPC to its Asian suppliers. We expect the guidance to be achievable as the worst seems likely to be over for the HPC segment along with strength in the Global Pet Care business. Looking ahead, given the relative balance sheet strength which has now been fixed along with achievable guidance, we believe SPB is an attractive proposition.

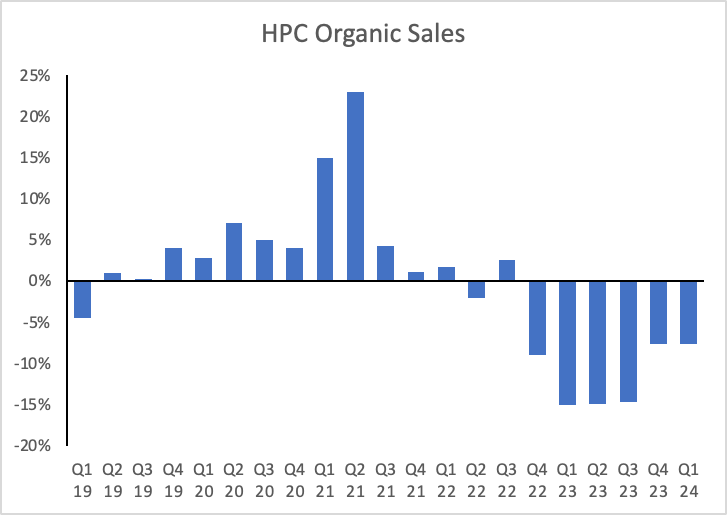

HPC Turnaround to Bolster Strategic Process

SPB reported an organic sales decline of 7.6% driven by the continued decline in within the small kitchen appliances in the North American region, while international markets remained a silver lining which reported positive momentum within personal care as well as small kitchen appliances. This marks the second straight quarter of MSD organic sales decline, significantly better than the mid-teens decline it experienced over the past several quarters.

Company filings, Author

Adjusted EBITDA margins improved by 420 bps YoY, primarily driven by low-cost inventory and cost optimizations along with lower promotional spends. This was also helped by the phasing off investments from Q1, which is now expected to be reallocated to H2 when consumer demand is expected to be on a high, particularly during the holiday season. However, the situation is not expected to be starkly better going forward as we believe the company to report mid-single digit decline as a result of low consumer demand and pricing pressure within small kitchen appliances, which is still in the phase of inventory normalization post COVID. However, we believe that the company is likely to benefit from the replacement cycle within the next couple of years for the consumers who purchased during 2020-2021, which could mark a strong recovery for the segment. This could potentially help them to accelerate the strategic review process of the division, which had been echoed by the company’s management.

Given the improved performance of this business and our healthier outlook for it now, we are starting to accelerate the process to separate HPC via a sale, merger or a spin in hopes to have a transaction announced later this year.

– David Maura, Executive Chairman and CEO

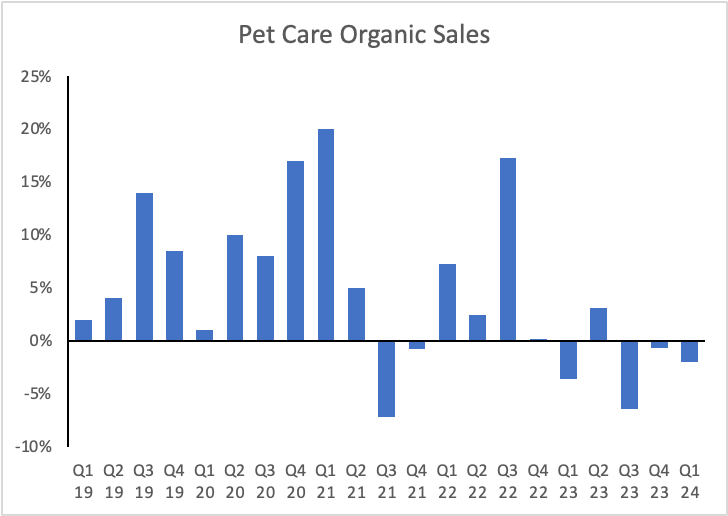

GPC continues to be stable

GPC segment has continued to show signs of stabilization with organic sales down 2% YoY driven by the continued outperformance of its companion animals category offset by a decline in aquatic sales along with exit from select categories and SKUs. Companion animals in North America grew low single digits while aquatic sales continue to be pressured, down double digits, as the aquatic marketplace continues to remain challenged as a result of consumers trading down to value channels. However, while its decision to exit a few categories and low-profit SKUs has been a topline headwind, the company has been able to bump its bottom line in a meaningful way.

Company filings, Author

EBITDA margins shot up by 560 bps YoY to 19% primarily driven by lower cost inventory and exit from low-margin products partially offset by brand investments. This provides further strength and an improved outlook on the bottom line front in the near future and demonstrates building blocks to 20%+ margins soon.

Valuation

We continue to value SPB on a SOTP basis given the different business models. We compare its Home & Personal care business with Hamilton Beach Brands (HBB), Newell Brands (NWL), SharkNinja (SN), De’Longhi S.p.A. (OTCPK:DELHF) and Helen of Troy (HELE). Despite some relative stability, We continue to apply a 30% discount and ascribe an EV/Fwd EBITDA of 7.0x for its HPC business, as it still does not seem to be out of the woods.

| EV/Fwd EBITDA | |

| Hamilton Beach Brands | – |

| Newell Brands | 8.9x |

| SharkNinja | 11.0x |

| De’Longhi America | 9.8x |

| Helen of Troy | 11.0x |

| Average | 10.1x |

We continue to compare its Home and Garden business with The Scotts Miracle-Gro Company (SMG), Central Garden & Pet (CENT) and Henkel (OTCPK:HENKY) and ascribe an EV/Fwd EBITDA of 10.4x in line with the peer average.

| EV/Fwd EBITDA | |

| Scotts Miracle-Gro | 11.7x |

| Central Garden and Pet | 10.6x |

| Henkel | 8.8x |

| Average | 10.4x |

We compare its Global Pet Care business with other players in the pet care and wellness market including Chewy (CHWY), Freshpet (FRPT) J. M. Smucker (SJM), Central Garden & Pet (CENT) and Petco (WOOF). We ascribe a target multiple of 9.7x in line with its peer average and discontinue applying any premium as the valuation differential seems to narrow due to slight underperformance relative to its peers in recent quarters.

| EV/Fwd EBITDA | |

| Chewy | 20.8x |

| Freshpet | NM |

| J. M. Smucker | 9.4x |

| Central Garden & Pet | 10.6x |

| Petco | 9.0x |

| Average | 12.5x |

SOTP Value

| ($mn) | Valuation Basis | Enterprise Value |

| HPC | 7.0x Fwd EBITDA | $392 mn |

| Home & Garden | 10.4x Fwd EBITDA | $797 mn |

| Pet Care | 9.7x Fwd EBITDA | $1,979 mn |

| Total EV | ||

| (+) Net Cash | $85 mn | |

| Equity Value | $3,253 | |

| Implied Price | $107 |

Risks to Rating

Risks to rating include

1) Prolonged headwinds within its Home and Personal care business as a result of management’s inability to sell or spin-off the business can lead to continued overhang and divert management’s focus on growth engines.

2) Inventory rationalization can continue to pressure near term growth across its business, particularly within its Global Pet Care and Home & Garden business.

3) Gross margins have improved in recent quarters primarily as a result of low-cost inventory, which could become a headwind in the near future if it is unable to pass on the costs to its consumers.

Conclusion

We believe the company has shown signs of stabilization in its operational performance after years of challenging quarters. The strong EBITDA beat was much better than feared, which sent shares jumping about 8% on the day. We believe that stabilization in HPC and Home & Garden business along with bottom line improvements in GPC could render a strong comeback from current levels which are still inexpensive in our view. Reiterate Buy and upping the target price to $107 on an SOTP basis.

Q2 2024 Earnings Call Transcript")