Kameleon007

Overview

My recommendation for S&P Global Inc. (NYSE:SPGI) is a buy rating. The recent fall in share price represents an attractive opportunity to long the stock as the business outlook remains strong. SPGI core business ratings exited 4Q23 on a strong note, and I expect momentum to persist into FY24. Non-rating businesses also performed very well, showing the perks of having a diversified revenue base. Importantly, management continues to be shareholder-friendly, returning capital to shareholders via buybacks, which continues to support the EPS growth outlook.

Business

SPGI is a popular name for equity investors that does not need another big introduction. Keeping it short, SPGI mainly provides credit rating services (26.3% of FY23 revenue), market intelligence services (34.5% of FY23 revenue), which are popular for its CapitalIQ platform, and S&P Global Commodity Insights (15.4% of revenue), which provides benchmarks, news, insights, data analytics, and workflow solutions for investors and businesses dealing with commodities.

Recent results & updates

SPGI reported 4Q23 total revenue of $3.15 billion, which was a 7.3% y/y growth that beat consensus of 6.6%. By segment, ratings revenue grew 18.9% y/y, driven by healthy global debt issuance volumes in 4Q23. Market intelligence revenue grew 8.7% y/y, commodity insights grew 10.2%, indices grew 4.7% y/y, and mobility grew 9.3% y/y. EBIT margin also expanded nicely by 300bps to 44.1% but did not meet consensus expectations for 46.1%. By segment, EBIT margin expansion was driven by ratings, indicators, and market intelligence, but offset by a slight contraction in commodity insights and mobility. At the bottom line, SPGI performed in line with consensus by reporting EPS of $3.13 vs. consensus of $3.15.

I believe the SPGI stock price decline post-earnings release was overly done, and as such, I see this as an attractive opportunity to buy the stock. In my opinion, management FY24 guidance was the reason for this share price decline. Management guided FY24 revenue growth of 5.5 to 7.5% on a reported basis and 7 to 9% on an organic basis. EBIT margin is expected to expand by 100 basis points, and EPS is expected to come in the range of $13.75 to $14. This led to a series of consensus downgrades as guidance was below pre-results expectations (consensus expected 7.2% revenue growth and EPS of $14.45).

While it is true that SPGI seems to have a “disappoint” consensus, I don’t think the equity story of SPGI is heavily impaired because of this. If we consider the macroeconomic situation in FY23, where we had a high rate environment (huge increases at a high pace), SPGI core business ratings still generated 9.2% growth with a margin expansion of 60bps, indicating how resilient the business is as it rebounded back to its historical growth range (pre-FY22 average growth rate is ~9%) after a soft FY22 performance. If we look at 4Q23 performance, the ratings business continued to perform very strongly, growing revenue at 18.9%, indicating that the momentum is not slowing down, which I expect to continue into FY24. Notably, the revenue growth was driven by debt refinancing activity in high-yield and leveraged loans, which should continue into 2024 as management expects 2024 billed debt issuance growth of 3-7%. Given the expected timing of the Fed cutting rates, I believe the SPGI rating business will see a strong performance in 1H24 as issuers look to lock in these attractively high rates while they can.

In the fourth quarter, we continued to see issuers returning to the market with billed issuance growth driven primarily by strength in bank loans, structured finance and high yield.

What we’re actually hearing from the market is a little bit different. So for bank loans and high-yield, for example, we’re seeing and hearing couple of things. Number one, issuers have accepted the higher for longer. from: 4Q2023 earnings call

Ratings business aside, other parts of SPGI business continue to perform very strongly in 4Q23, reflecting benefits from diversified and recurrent revenue streams, and management remains steadfast on reinvesting in growth. The good thing about this diversification is that it makes SPGI, as a whole, more resilient to market cycles as it becomes less dependent on its rating business, which is highly exposed to how the economy is performing. In good times, businesses’ appetite for loans goes up, which also brings up the demand for more rating services. In bad times, the flipside happens. So far, management’s track record in achieving this diversification has been great. Using an example that management cited, its vitality index, measuring revenue contributions from new products, exceeded 11% in 2023, ahead of its 10% target. I expect management to continue diversifying the revenue base, which should have a positive impact on the stock valuation.

Looking further ahead, I also expect SPGI to incorporate more AI capabilities. During the call, management discussed the company’s ongoing efforts to advance generative AI projects by utilizing both internal Kensho AI capabilities and external partnerships. SPGI has begun releasing related products to a select group of customers, including ChatIQ (in December 2023), and has integrated generative AI capabilities into the S&P Global Marketplace to facilitate efficient queries of the company’s extensive data set. Rolling out to a pilot set of customers makes sense, as SPGI would be able to reiterate the product to better fit the needs of its customers. While we do not know the financial impacts of these products, I believe they are going to have a positive impact as they should improve customers’ productivity, making them willing to pay more. I also expect the announcements regarding AI-related products in the coming future to add a layer of positive sentiment to the stock.

Regarding capital allocation, management actions continue to be in favor of shareholders. In FY23, SPGI returned $4.4 billion to shareholders and is going to authorize a new $2.4 billion share repurchase plan, with the initial $500 million ASR (accelerated share repurchase program) happening in the very near term. As such, I believe share repurchase is going to continue to be a core policy for SPGI moving forward. Historically, SPGI repurchased its share at a low-to-mid-single-digit percentage a year, which I think is a good baseline for the future.

In 2023, we returned $4.4 billion to shareholders through dividends and buybacks, representing more than 100% of our adjusted free cash flow.

As you saw in the press release earlier this morning, our Board has authorized a repurchase of shares totaling up to $2.4 billion, which we expect to execute throughout the year.

We executed a $500 million accelerated share repurchase program or ASR in the first quarter and we plan to launch a new $1 billion ASR in the coming weeks, leveraging the proceeds of the Engineering Solutions divestiture and cash on hand. 4Q2023 earnings call

Valuation and risk

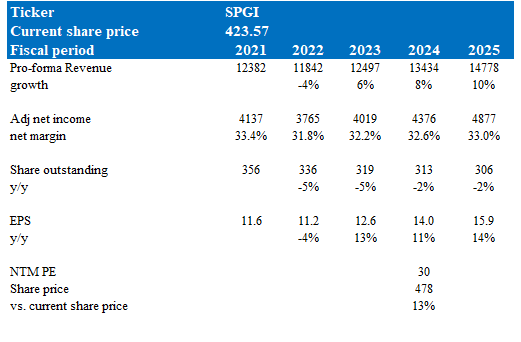

Author’s valuation model

According to my model, SPGI is valued at $478, representing a 13% upside. This target price is based on my growth forecast of accelerating growth over the next 2 years, reaching 10% in FY25, after achieving management-guided 7.5% growth in FY24. With the strong growth momentum exiting 4Q23 and the upcoming launches of AI products, I expect growth to be higher than FY24; as such, I expect FY25 growth of 10%. I derived my FY24 adjusted net income of $4.376 billion by working backward using management-guided EPS (I assumed $14) and a 2% share buyback. As for FY25, I assumed modest adj net margin expansion (similar to the rate between FY23 and FY24) to 33%, and with the same 2% share buyback assumption, I got to FY25 EPS of $15.90. Over the past 5 years, SPGI has traded within a valuation range of 25x to 29.5x. As I expect SPGI to see accelerating topline growth and margin expansion, I believe the stock should continue to trade at the high end of its valuation bend in the near term.

Investment risks to consider are that the strength in rating revenue might not be extrapolatable given that a bulk of issuance growth this year is coming from speculative grade refinancing, which tends to involve infrequent issuers. In addition, the market intelligence segment might be impacted by lower capital market activity as a result of a weak economic outlook (i.e., less preference for investments, leading to less need for SPGI’s market intelligence product).

Summary

I give SPGI a buy rating as I see the recent share price drop as an attractive entry point. The core business, particularly ratings, exhibited strong performance in 4Q23, and the diversified revenue streams contribute to resilience against market cycles. While the FY24 guidance led to a temporary share price decline, the company’s historical track record and robust business fundamentals suggest a positive outlook. Management also remains committed to being shareholder-friendly by continuing their share repurchases policy.

Q2 2024 Earnings Call Transcript")