Ralf Hahn

There’s nothing wrong with the trends in S&P 500 earnings data, at least what’s tracked weekly at Refinitiv, since the numbers continue to firm.

Unfortunately, the S&P 500 couldn’t close above its July 23, ’23 high of 4,607.07, closing this week at 4,604.37.

S&P 500 data:

- The forward 4-quarter assess fell $0.15 this week to $236.26 from $236.41.

- The P/E ratio ended the week at 19.5x.

- The S&P 500 ended the week at 5.13%, still at the lower end of the preferred range, meaning the S&P 500 still looks rich or fully valued.

- This coming week, we get quarterly earnings from Oracle (ORCL) Monday night, December 11th, Adobe (ADBE) reports Wednesday, December 13th after the close, and then Costco (COST) and Lennar (LEN), on Thursday, December 14th, after the close.

Rate of change

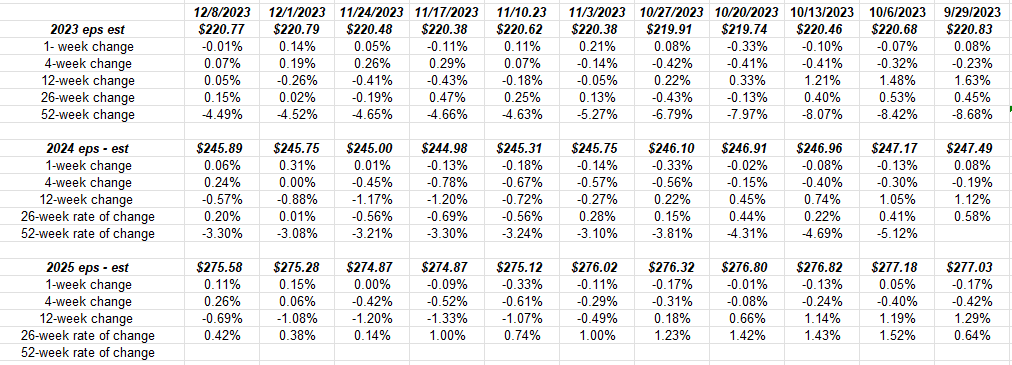

This Excel table shows the full year 2023, 2024 and 2025 S&P 500 EPS estimates. The expected growth rates are +2%, +11% and +12% respectively for 2023 – 2025.

Even with pressure on Q4 ’23 bottom-up EPS, calendar 2024 has yet to change very much, and companies are starting to leak out their calendar ’24 guidance.

Let’s put it another way: If there is a problem in 2024, I don’t think it will be earnings-related, but still bond market-related or interest rate-driven.

Maybe the whole earnings-related discussions are pointless, since the tech sector EPS growth in 2023 is just 7%, and yet the sector is up 49.97% YTD as of 12/1/23.

In 2019, with Jay Powell cutting the fed funds rate, the S&P 500 rose roughly 30% on zero S&P 500 EPS growth (talk about P/E expansion).

Looking at expected S&P 500 EPS sector growth rates for 2024, the tech sector’s EPS growth is expected to rise from 7% in ’23 to +15.8% as of 12/8/23.

Summary/conclusion: Oracle’s conference call will be interesting after the bell on Monday, December 14th. This blog will have an earnings preview on ORCL over the weekend.

Margins have been under pressure thanks to the Cerner acquisition. Guidance tanked the stock after the August ’23 quarter reported in September.

With worries about Walmart (WMT) and “deflation”, Costco’s quarter on Thursday night will get some interest. Costco is a juggernaut. They execute regardless of the macro. What a brand, but it’s always fully-valued.

Recent jobless claims and this morning’s November jobs report shows the US economy still slowly decelerating, but not enough to send S&P 500 EPS off a cliff (at least not yet).

With Oracle, Adobe, Lennar and Costco this week, and then Nike (NKE), FedEx (FDX), Accenture (ACN) and Micron (MU) in coming weeks, readers will get a nice cross-section of the US economy that is driving this market.

Don’t neglect the November CPI and PPI due Tuesday and Wednesday next week. The drop in crude oil has been very helpful for the overall indices. Gasoline, at least in Illinois last week, is $3.16 a gallon (at Costco), the lowest since Christmas week of 2022, when it was $3.00 to $3.05.

Technically speaking, the S&P 500 needs to trade above that July ’23 high of 4,606.07 and then run towards the all-time high at 4,795-4,800 to maintain the bull’s case. The S&P 500 price targets for 2024 seem awfully bearish today.

Take all this with substantial skepticism, and a considerable grain of salt. None of this is advice or recommendation. Past performance is no assure of future results, and investing can involve the loss of principal.

Capital markets can change quickly for both the good and the bad. evaluate your own comfort with your portfolio volatility and adjust accordingly.

Thanks for reading.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Q2 2024 Earnings Call Transcript")