pcess609

This monthly article series reports sector metrics in the S&P 500 index. It is also a top-down analysis of all ETFs based on the S&P 500.

Fast Facts on BBUS

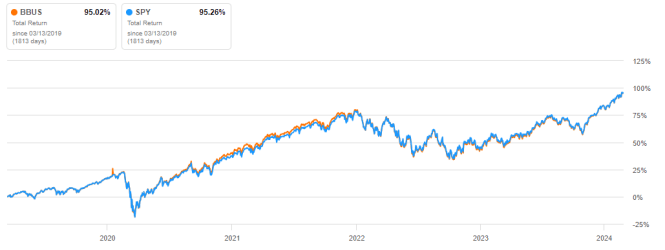

JPMorgan BetaBuilders U.S. Equity ETF (BATS:BBUS) was listed on 03/12/2019 and tracks the Morningstar® US Target Market Exposure Index. This large and mid-cap index is similar to the S&P 500. Since BBUS inception 5 years ago, BBUS and SPDR® S&P 500® ETF Trust (SPY) have followed the same path, as plotted on the next chart. The difference in total return is negligible.

BBUS vs SPY since inception (Seeking Alpha)

The top 10 holdings are identical and their weights are close, as reported below.

|

Ticker |

Name |

BBUS |

SPY |

|

MICROSOFT CORP |

6.85% |

7.10% |

|

|

APPLE INC |

6.00% |

6.22% |

|

|

NVIDIA CORP |

4.18% |

4.50% |

|

|

AMAZON.COM INC |

3.65% |

3.69% |

|

|

META PLATFORMS INC CLASS A |

2.43% |

2.52% |

|

|

ALPHABET INC CL A |

1.83% |

1.89% |

|

|

BERKSHIRE HATHAWAY INC CL B |

1.69% |

1.76% |

|

|

ALPHABET INC CL C |

1.55% |

1.60% |

|

|

ELI LILLY + CO |

1.45% |

1.42% |

|

|

BROADCOM INC |

1.28% |

1.33% |

The next table compares various characteristics of the two funds:

|

BBUS |

SPY |

|

|

Inception |

3/12/2019 |

1/22/1993 |

|

Expense Ratio |

0.02% |

0.09% |

|

AUM |

$2.98B |

$497.11B |

|

Avg Daily Volume |

$14.63M |

$39.22B |

|

Holdings |

573 |

503 |

|

Assets in Top 10 |

30.91% |

32.03% |

|

Turnover |

3.00% |

2.00% |

|

P/E ttm |

24.02 |

24.15 |

The cheap fee of the JPMorgan ETF is attractive for long-term investors. However, much higher trading volumes make SPY a better instrument for traders.

Shortcut

The next two paragraphs in italic describe the dashboard methodology. They are necessary for new readers to understand the metrics. If you are used to this series or if you are short of time, you can skip them and go to the charts.

Base Metrics

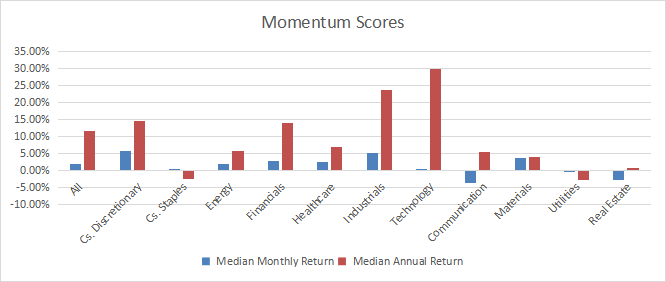

I calculate the median value of five fundamental ratios in every sector: Earnings Yield (“EY”), Sales Yield (“SY”), Free Cash Flow Yield (“FY”), Return on Equity (“ROE”), Gross Margin (“GM”). All are calculated on trailing 12 months. For all these ratios, higher is better and negative is bad. EY, SY and FY are medians of the inverse of Price/Earnings, Price/Sales and Price/Free Cash Flow. They are better for statistical studies than price-to-something ratios, which are unusable when the “something” is close to zero or negative (for example, companies with negative earnings). I also calculate two momentum metrics for each group: the median monthly return (RetM) and the median annual return (RetY).

I prefer medians rather than averages because a median splits a set in a good half and a bad half. Capital-weighted averages are skewed by extreme values and the largest companies. As a consequence, these metrics are designed for stock-picking rather than index investing.

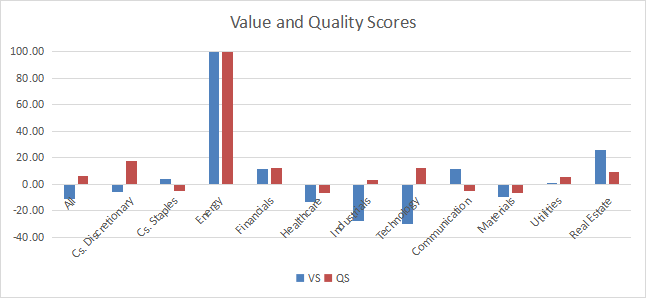

Value and Quality Scores

Historical baselines are calculated as the averages on a look-back period of 11 years for all metrics. They are noted respectively EYh, SYh, FYh, ROEh, GMh. For example, the value of EYh for technology in the table below is the 11-year average of the median Earnings Yield of S&P 500 tech companies.

The Value Score “VS” is the average difference in % between the three valuation ratios (EY, SY, FY) and their baselines (EYh, SYh, FYh). The same way, the Quality Score “QS” is the average difference between the two quality ratios (ROE, GM) and their baselines (ROEh, GMh).

VS may be interpreted as the percentage of undervaluation or overvaluation relative to the baseline (positive is good, negative is bad). This interpretation must be taken with caution: the baseline is an arbitrary reference, not a supposed fair value. The formula assumes that the three valuation metrics are of equal importance, except in energy and utilities where the Free Cash Flow Yield is ignored to avoid some inconsistencies. VS and QS are capped between -100 and +100 when the calculation goes beyond these values.

Current Data

The next table shows the metrics and scores as of the last daily closing. Columns stand for all the data defined above.

|

VS |

QS |

EY |

SY |

FY |

ROE |

GM |

EYh |

SYh |

FYh |

ROEh |

GMh |

RetM |

RetY |

|

|

All |

-11.20 |

6.44 |

0.0380 |

0.3611 |

0.0255 |

16.41 |

48.32 |

0.0432 |

0.4181 |

0.0277 |

15.14 |

46.27 |

1.98% |

11.50% |

|

Cs. Discretionary |

-5.91 |

17.40 |

0.0428 |

0.5378 |

0.0313 |

28.58 |

36.93 |

0.0451 |

0.6424 |

0.0302 |

21.51 |

36.24 |

5.67% |

14.49% |

|

Cs. Staples |

4.23 |

-4.81 |

0.0467 |

0.4955 |

0.0204 |

21.32 |

40.40 |

0.0420 |

0.4727 |

0.0211 |

23.48 |

40.57 |

0.47% |

-2.54% |

|

Energy |

100 |

100 |

0.0830 |

0.4968 |

0.0421 |

21.71 |

48.09 |

0.0242 |

0.5488 |

-0.0059 |

7.14 |

43.23 |

1.92% |

5.56% |

|

Financials |

11.30 |

11.95 |

0.0637 |

0.5435 |

0.0778 |

12.77 |

80.93 |

0.0687 |

0.4346 |

0.0670 |

11.09 |

74.42 |

2.68% |

13.93% |

|

Healthcare |

-13.32 |

-6.57 |

0.0297 |

0.2645 |

0.0262 |

13.93 |

62.87 |

0.0347 |

0.2769 |

0.0332 |

15.90 |

63.35 |

2.56% |

7.00% |

|

Industrials |

-27.62 |

2.98 |

0.0328 |

0.2793 |

0.0243 |

21.17 |

39.57 |

0.0440 |

0.5244 |

0.0272 |

21.28 |

37.16 |

5.09% |

23.72% |

|

Technology |

-29.84 |

12.17 |

0.0276 |

0.1640 |

0.0249 |

27.42 |

63.08 |

0.0373 |

0.2593 |

0.0340 |

22.06 |

63.07 |

0.48% |

30.05% |

|

Communication |

11.20 |

-5.23 |

0.0413 |

0.6879 |

0.0402 |

14.31 |

56.12 |

0.0461 |

0.5273 |

0.0354 |

16.50 |

54.57 |

-3.67% |

5.33% |

|

Materials |

-9.42 |

-6.52 |

0.0340 |

0.5975 |

0.0226 |

16.36 |

33.64 |

0.0439 |

0.6015 |

0.0238 |

17.42 |

36.15 |

3.74% |

3.95% |

|

Utilities |

0.89 |

5.77 |

0.0538 |

0.4630 |

-0.0995 |

9.96 |

42.75 |

0.0494 |

0.4985 |

-0.0557 |

9.59 |

39.71 |

-0.37% |

-2.92% |

|

Real Estate |

26.08 |

9.21 |

0.0326 |

0.1273 |

0.0092 |

8.08 |

64.90 |

0.0231 |

0.1146 |

0.0073 |

6.76 |

65.62 |

-2.77% |

0.58% |

Score Charts

The next chart plots the Value and Quality Scores by sector (higher is better).

Value and quality in the S&P 500 (Chart: author; data: Portfolio123)

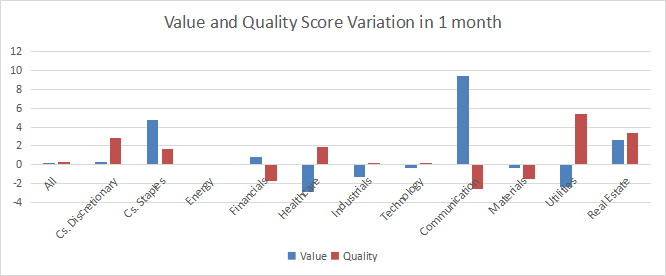

Score variation since last month:

Variations in value and quality (Chart: author; data: Portfolio123)

The next chart plots momentum scores based on median returns by sector.

Momentum in the S&P 500 (Chart: author; data: Portfolio123)

Interpretation

A hypothetical S&P 500 “median” company is overvalued by 11.2% relative to average valuation metrics since 2012. The quality score is slightly above the historical baseline. We can translate median yields in their inverse ratios:

Price/Earnings: 26.32 – Price/Sales: 2.77 – Price/Free Cash Flow: 39.22

Energy has been showing the highest value and quality scores among GICS sectors for 2 years. Real estate is undervalued by about 26% relative to 11-year averages, and also has a good quality score. Financials, communication, and consumer staples are undervalued by 4% to 11%. Utilities are just on the historical baseline in valuation and close above it in quality. Materials, healthcare and consumer discretionary are overvalued by 6% to 13% relative to their baseline. It may be justified by a good quality score for consumer discretionary. Technology and industrials are overvalued by almost 30%.

SPY has gained 30.2% in 12 months (total return), whereas the median return of the S&P 500 is 11.5% (reported in the table above) and the equal-weight return (measured on RSP) is 12.8% . It means the capital-weighted index has been massively skewed to the upside by mega-cap companies over the last 12 months.

We use the table above to calculate value and quality scores. It may also be used in a stock-picking process to check how companies stand among their peers. For example, the EY column tells that a large consumer staples company with an Earnings Yield above 0.0467 (or price/earnings below 21.41) is in the better half of the sector regarding this metric. A Dashboard List is sent every month to Quantitative Risk & Value subscribers with the most profitable companies standing in the better half among their peers regarding the three valuation metrics at the same time. The 9 stocks listed below are an excerpt of the list of 75 companies sent to subscribers for the March 2024 update.

|

Polaris Inc. |

|

|

Valero Energy Corp. |

|

|

Synchrony Financial |

|

|

Tenet Healthcare Corp. |

|

|

Lockheed Martin Corp. |

|

|

Apogee Enterprises, Inc. |

|

|

Bunge Global SA |

|

|

InterDigital, Inc. |

|

|

SJW Group |

It is a rotational model with a statistical bias toward excess returns on the long-term, not the result of an analysis of each stock.

Q2 2024 Earnings Call Transcript")