BlackJack3D

Semiconductors did well in 2024 with the iShares Semiconductor ETF (NASDAQ:SOXX) gaining 33% since I last covered it in July last year. At that time, I had a neutral position mostly because of demand softness, high inventories especially for memory, and Chinese authorities imposing export restrictions on a key ingredient used to make chips.

Moreover, at that time, NVIDIA (NASDAQ:NVDA), the king of AI constituted only about 9% of the ETF’s weight which meant it was not positioned to benefit from accelerator GPUs in the same way as the VanEck Semiconductor ETF (NASDAQ:SMH) which devoted a much higher percentage of its assets to the semiconductor giant.

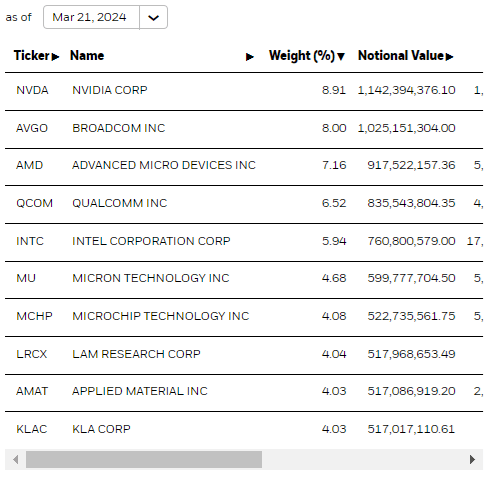

Currently, the NYSE Semiconductor Index tracking SOXX still holds about 9% of Nvidia as illustrated below, but, as AI proliferates across the industry and benefits other names, this thesis aims to show that this lower exposure now represents strength while navigating an environment characterized by more risks.

SOXX Holdings (www.ishares.com)

To start with, given that global chip sales declined by 8.2% last year according to the SIA (Semiconductor Industry Association), it signifies that much of the 33% upside was driven by AI enthusiasm, making it imperative to assess in depth which holdings are capable of monetizing artificial intelligence.

Nvidia Triggering Proliferation of AI in SOXX’s Other Holdings

First, looking at the king of AI, it is witnessing upbeat demand for its H100 GPU chips as these find their way into the data centers of CSPs (cloud service providers) and large enterprises with spending power. The company has also launched the H200 Tensor Core GPU which packs more processing power to accelerate the speed at which AI models are trained.

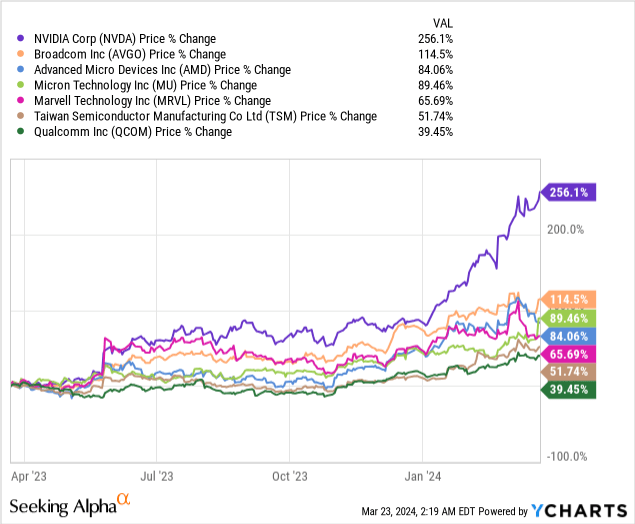

In the same vein, its excellent revenue figures and sales guidance tend to paint a bright landscape for AI, or one characterized by both sustained demand for this innovative technology and its proliferation across the industry. This in turn helps those already in Nvidia’s supply chain like Taiwan Semiconductor Manufacturing Company (TSM) providing the contract manufacturing services. Then, comes providers of complementary products like Micron (NASDAQ:MU) as well as competitors like Advanced Micro Devices (NASDAQ:AMD), and, noteworthily, their share prices, while appreciating, have not benefited to the same degree as Nvidia as shown below. This should change as the AI magical wand touches their products too.

First, looking at the competition, despite Nvidia commanding the lion’s share, the server AI GPU market is expected to grow at a CAGR of nearly 32% from 2023 to 2028, meaning other suppliers like AMD can profit from additional sales. Thus, the company could ship between 300,000 to 400,000 units of its Instinct MI300 this year.

Second, complementarity is where a component from one company is paired with one from another to deliver the final product. Here, Micron, with its HBM3e chips, which are high bandwidth memory will form part of H200s. The reason for Nvidia choosing Micron is that its HBM3e could consume about 30% less power than competitors and contribute to reducing data center operating costs. As a result, Micron’s order book is full for 2024 and most of 2025.

Pursuing further, depending on how companies deploy their AI infrastructures, for example buying discrete GPUs before integrating them within their particular data center environments, there are also opportunities for others like Broadcom (NASDAQ:AVGO) whose revenue for the fiscal year 2023 grew by 8% YoY driven by AI. In this case, certain hyperscalers do not buy Nvidia’s DGX H100 supercomputer which amounts to a packaged solution and already includes the proprietary InfiniBand for interconnecting the compute part to the storage (data pool). Thus, by providing high-bandwidth interconnects together with customized solutions, Broadcom’s management expects AI-related revenues to more than quadruple on a YoY basis to $10 billion in fiscal 2024.

Looking across the industry, there is also Marvell (MRVL) which could benefit from an AI revenue stream, but for others, the good news is the recovery in the chip market this year.

The industry is Back to Growth but Look out for Monetary Policy and Geopolitical Risks

In this respect, the market for personal computers and smartphones which suffered from low demand for most of 2023 could see a stabilization, with the high inventories starting to bottom out.

Continuing on a positive note, the SIA expects the industry to return to growth this year with a target of 13.1%, driven mostly by a recovery in memory sales. However, AI-related growth appears not to be priced in. For this purpose, a report by Gartner which takes into consideration the demand for semis in high-performance GPU-based servers for training AI models forecasts an even higher growth rate of 16.8% for the semiconductor industry. This figure also represents a reasonable upside for SOXX since its holdings provide exposure to American companies that design, manufacture, and distribute chips. In other words, by holding companies that operate across the semis value chain, the ETF provides an industry view.

Applying this percentage to SOXX’s current share price of $224.45, I obtain a target of $262.15 (224.45 x 1.168) which accounts both for industry-level recovery in 2024 as well as AI proliferation opportunities I have identified earlier.

Thinking aloud 16.8% is much lower than the 59% upside enjoyed in 2023, but there are risks.

First, it is premature to expect a complete rebound in semis, because of persistent weakness in the industrial, auto, and wireless segments which should impact the revenues of companies specializing in analog, mixed-signal devices, and related areas. Thus, companies like Analog (NASDAQ:ADI) and STMicroelectronics N.V. (STM) which both form part of SOXX holdings, expect toplines for their upcoming quarters to be lower than the consensus by analysts.

Second, in addition to AI, other forces that drove the market in 2023 were the possibility of a soft landing (or no recession) and, that somehow the Federal Reserve would be able to tame inflation and cut interest rates. Thus, according to a survey of market participant sentiment by Deutsche Bank (DB), from the 76% who were expecting a soft landing in December, this number increased to 84% after the latest Fed meeting earlier this month. Moreover, according to JPMorgan (JPM), there could be up to three cuts this year despite a stronger economy together with lower unemployment expectations while inflation remains sticky at above 3%.

SOXX Seems Better than SMH For 2024 as Volatility Risks Are Likely to Rise

Moreover, brokerages and market participants expect a rate cut in June. For this matter, market participants were already pricing rate cuts in March which did not happen. Now, in case the Fed does not achieve its aim to bring down inflation at 2% and maintains rates higher for longer, there could be volatility in June, which, by the way, will be just five months before the November elections which is the third source of risk.

In this connection, if the stance against China hardens and threats about imposing a 60% tariff on Chinese goods start to make headlines during political debates, this could be another source of volatility for semis, especially if there is tit-for-tat rhetoric from authorities in that country. The reason why there could be an escalation in geopolitical tensions is they have already urged their main electric vehicle manufacturers to prioritize domestic chips and any hardening of their stance like restricting imports from Western sources could spell trouble for the likes of Nvidia, NXP Semiconductors (NXPI), and Texas Instruments (TXN) among others.

Therefore, in addition to uncertainty about monetary policy, there are also geopolitical-related risks to contend with.

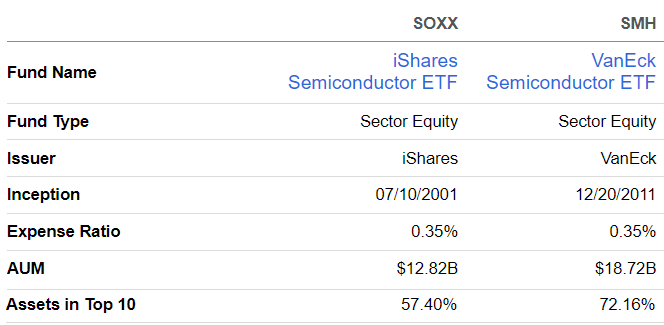

In these circumstances, for those wishing to position themselves on semis, it is better to opt for SOXX compared to alternatives like SMH. The reason is the iShares ETF bears fewer concentration risks as the percentage of assets dedicated to its top ten holdings is less by 14.76% (72.16 – 57.40) as tabled below.

Comparison with a peer (seekingalpha.com)

Using the same reasoning, over one-fifth of SMH’s weight is constituted by Nvidia, and, as AI proliferates across other names in the chip industry mentioned earlier, the semiconductor giant is likely to garner relatively less attention. It may even see outflows, especially after all the enthusiasm of 2023 and easy money flowing into the stock and propelling it higher by 256% as shown in the above chart. Therefore, by choosing SOXX, one could not only benefit from the recovery of the chip industry but also obtain a broader exposure to the AI story, or in a less concentrated way.

Finally, as seen with softness in industrial demand, this remains a cyclical industry, but, one where an additional dosage of chips will likely be required for PCs to make them more AI-driven. Therefore, from data centers to devices, the increased proliferation of innovative technology in more industrial and consumer goods has the potential to make AI become a secular trend in turn benefiting the semis industry.

Q2 2024 Earnings Call Transcript")