SoundHound AI (SOUN) develops advanced AI solutions, enabling voice-based interactions. Their products range from automotive voice assistants to customer service solutions, making it easier for users to engage with devices and businesses using their voices.

The business has an alluring narrative, but there are pesky details that keep me bearish on this stock. For one, the business’ backlog growth rates are rapidly decelerating. Secondly, the terms of the debt on its balance sheet leave this business with no room to maneuver.

While their technological advancements are commendable, the company’s current revenue growth rates and profitability metrics suggest a considerable overvaluation, making it advisable for investors to avoid this stock.

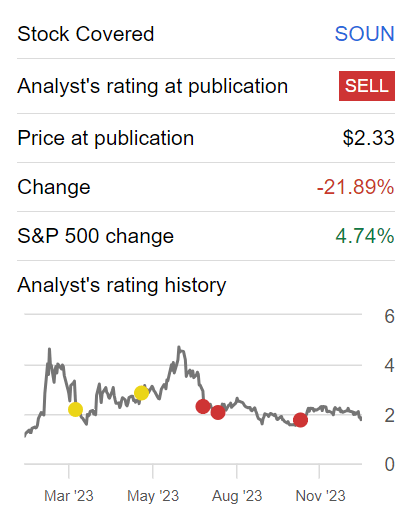

Author’s work on SOUN

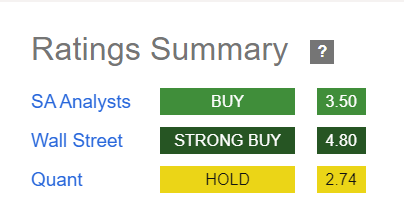

Since I turned bearish on this stock, it has underperformed the S&P 500 (SPY) as you can see above. Moreover, with the passage of time, I’ve only grown increasingly bearish on this stock. Even though the stock remains very highly rated, as you can see below.

SOUN AI ratings

Why SoundHound AI? Why Now?

SoundHound AI is a technology company that creates AI solutions. They make products that use AI to understand and respond to human voices. They’ve achieved success in various areas, such as automotive technology, where they provide features, like voice assistants. They’ve also expanded to TVs and other devices, making it easier for people to interact with technology using their voice.

SoundHound AI’s near-term prospects appear promising as they continue to witness momentum in their third quarter, marked by a robust 52% sequential increase in revenue to a record $13.3 million (more details on its financials to come).

With a diverse product portfolio spanning automotive, TVs, IoT devices, and AI-driven customer service solutions, SoundHound is positioned as a leading innovator in the AI space. The expansion of their Pillar 1 category, including partnerships with major automotive brands like Hyundai and Stellantis, underscores the growing acceptance of their technology.

Furthermore, the deployment of generative AI capabilities in automotive and the introduction of SoundHound Vehicle Intelligence enhance their offerings, signaling potential growth in revenue and customer base. The company’s strategic focus on large language models, such as the Polaris initiative, and a commitment to delivering unique multimodal generative AI foundation models showcase their dedication to staying at the forefront of conversational AI technology.

However, SoundHound AI faces several near-term challenges. Despite positive revenue growth, achieving sustained profitability remains a key hurdle.

Also, the competitive landscape in the AI sector is intense. Besides, the company must carefully manage operating expenses, especially as they accelerate investments in disruptive technologies like Polaris. Furthermore, the success of their solutions in various industries, including the highly competitive restaurant space, requires meticulous execution and continued market acceptance. Altogether, it may be challenging for forecast what’s vision and rhetoric and what’s realistic.

Given this context, let’s now discuss its financials.

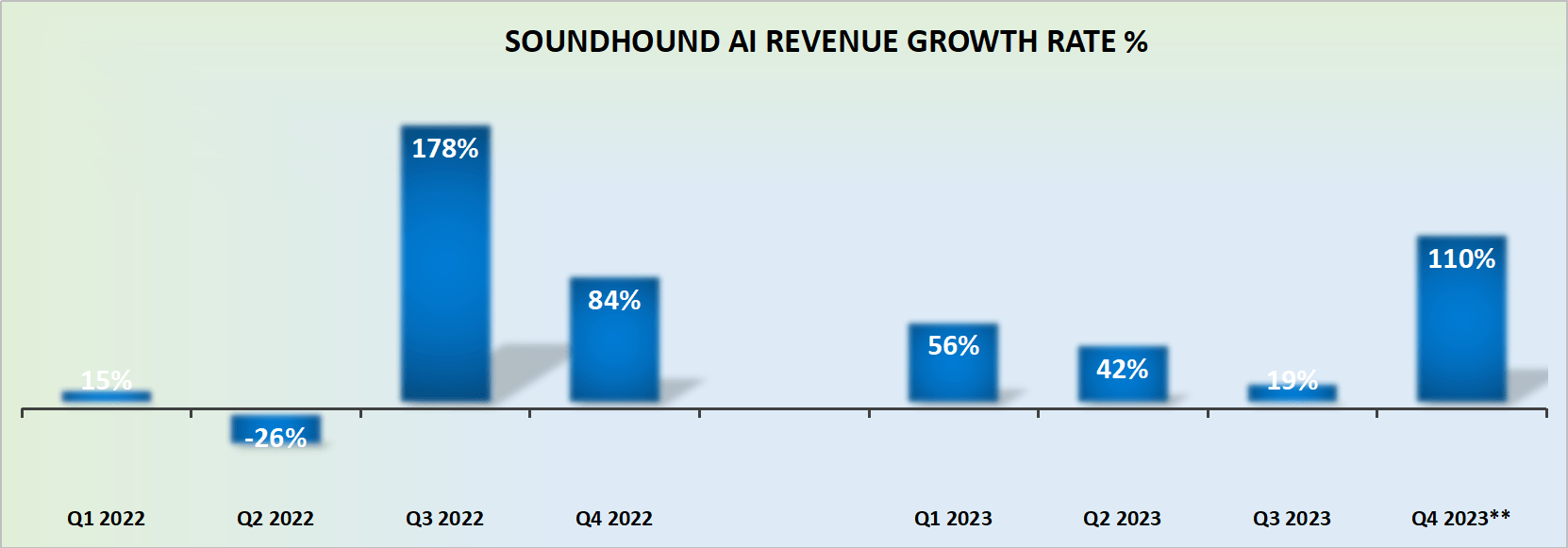

Revenue Growth Rates Are Patchy

SOUN revenue growth rates

There’s a lot to like from SoundHound’s Q4 guidance. After all, the guidance points to revenues coming in at 110% y/y at the high end. This is guidance is terrific as it points to strong growth rates ahead.

The problem though is that this guidance points to $50 million of revenues in total for 2023. And why is that such a big deal?

Firstly, because $50 million is nearly precisely what SoundHound guided for at the start of last year. This means that despite all the clamor about strong demand for their services, management wasn’t able to upwards revise their revenue outlook throughout this year.

Secondly, management has left themselves some room to slightly miss this figure of $50 million in revenues for 2023, by the way it guided for a range for Q4 revenues. Meaning that, at the midpoint of its guidance, the business may only be growing by 90% y/y in Q4.

Furthermore, since we have already started 2024, we must now form a view on what 2024 is likely to look like for SoundHound AI. I believe that in 2024 we are unlikely to see more than 20% CAGR. What makes me say so?

Consider this trend that follows for SoundHound AI’s cumulative backlog figures:

Q3 2022: 239%

Q4 2022: 59%

Q1 2023: 46%

Q2 2023: 20%

Q3 2023: 13%

What you see above is a clear sign that SoundHound AI is working its way through its previously attained backlog of orders and the company hasn’t quite found a way to reaccelerate the demand for its product.

Any growth investors seeking to reward this company with a high premium on its stock will be put off from getting involved with the stock until it’s clear that the backlog is once more growing at 20% CAGR or better.

SOUN’s Financial Position

SoundHound holds just under $100 million of unrestricted cash on its balance sheet. Against this sum, SoundHound AI’s debt liabilities are approximately $100 million (this figure includes the amortized discount).

Further compounding matters, even though SoundHound AI proclaims that the business will be EBITDA profitable starting Q4 2023, we have to keep in mind the following detail.

SoundHound AI’s interest payments on the $100 million of debt carry an interest rate of 14%. What this means in practice, is that there are approximately $12 to $15 million of interest payments due in the next months, depending on certain factors.

Consequently, put another way, the business is on a path toward about $60 million in revenues in the next twelve months, but this is combined with interest payments that will reach approximately 20% of its underlying revenues.

Given that SoundHound is only barely profitable when we take on board the health of its balance sheet, this makes stock unnecessarily risky.

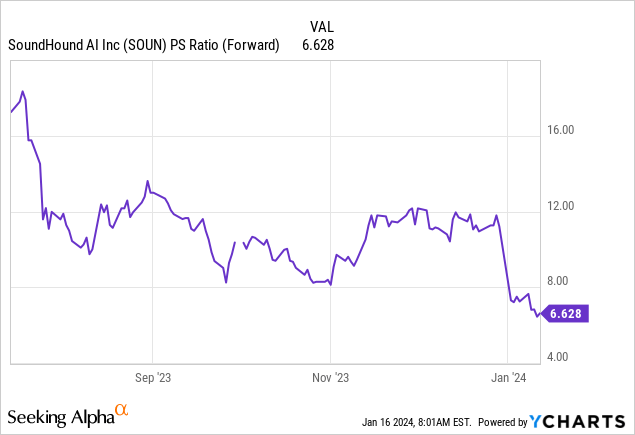

SOUN Stock Valuation — Not That Cheap At 7x Forward Sales

The graphic above requires a little interpretation. The reason why the multiple compresses significantly in the past couple of weeks is that the calendar year moved.

Nonetheless, the business is priced at more than 6x forward sales. Given that, in the current market, there are so many genuinely attractive businesses, with fewer blemishes also priced at around 6x to 10x forward sales, that I fail to get comfortable in recommending SoundHound AI.

The Bottom Line

Having conducted a thorough analysis of SoundHound AI’s recent performance and the prevailing market conditions, my bearish outlook on the stock remains intact.

Despite the company’s commendable efforts in advancing AI solutions for voice-based interactions and achieving revenue growth, there are noteworthy concerns that cast doubt on its future prospects.

The significant deceleration in backlog growth rates raises questions about sustained product demand. Financially, while the Q4 guidance is positive, the projection of $50 million in total revenues for 2023 closely mirrors the prior year’s forecast, signaling challenges in upward revisions.

The cumulative backlog figures suggest a slowdown in demand, potentially hampering robust growth in 2024. The financial position, marked by $100 million in debt against unrestricted cash, along with substantial interest payments, adds a layer of risk. Despite the current stock rating and valuation not being notably cheap at 7x forward sales, the amalgamation of these factors makes me hesitant to recommend SoundHound AI as an attractive investment.

Q2 2024 Earnings Call Transcript")