Presley Ann/Getty Images Entertainment

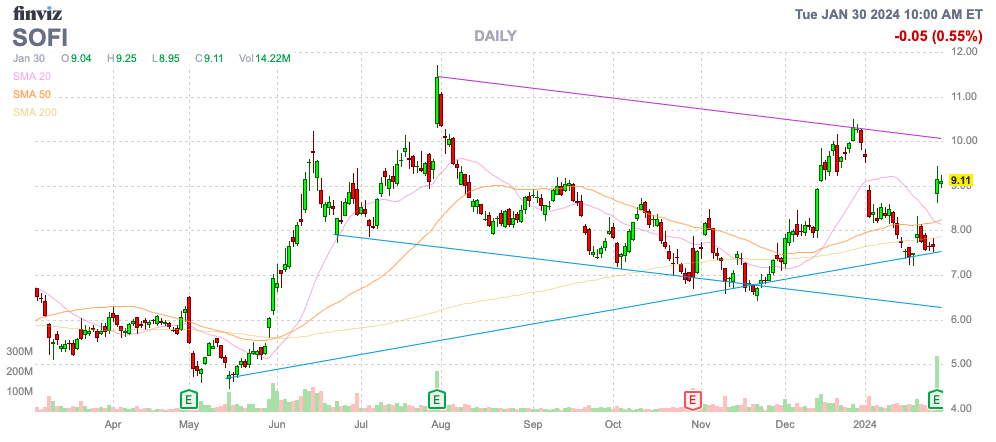

The market was so focused on whether SoFi Technologies, Inc. (NASDAQ:SOFI) was GAAP profitable in the December quarter, most people missed that the fintech was already a money machine. The company guided to massive tangible book value growth in 2024 with adjusted profits set to soar. My investment thesis remains ultra Bullish on the stock, still struggling to breakout above the original SPAC price of $10 announced all the way back in 2020.

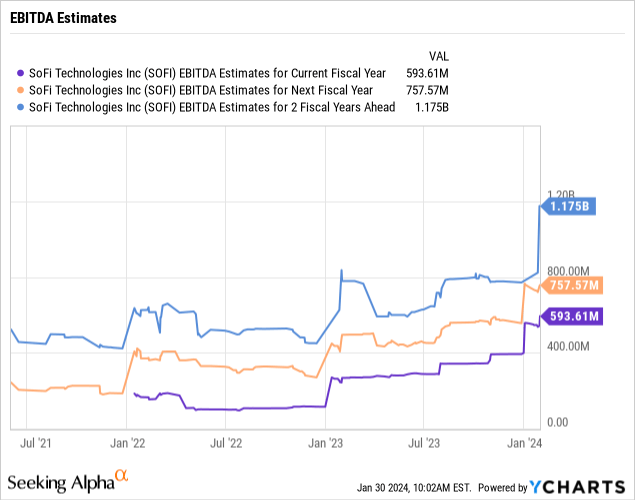

Source: Finviz

Profit Machine

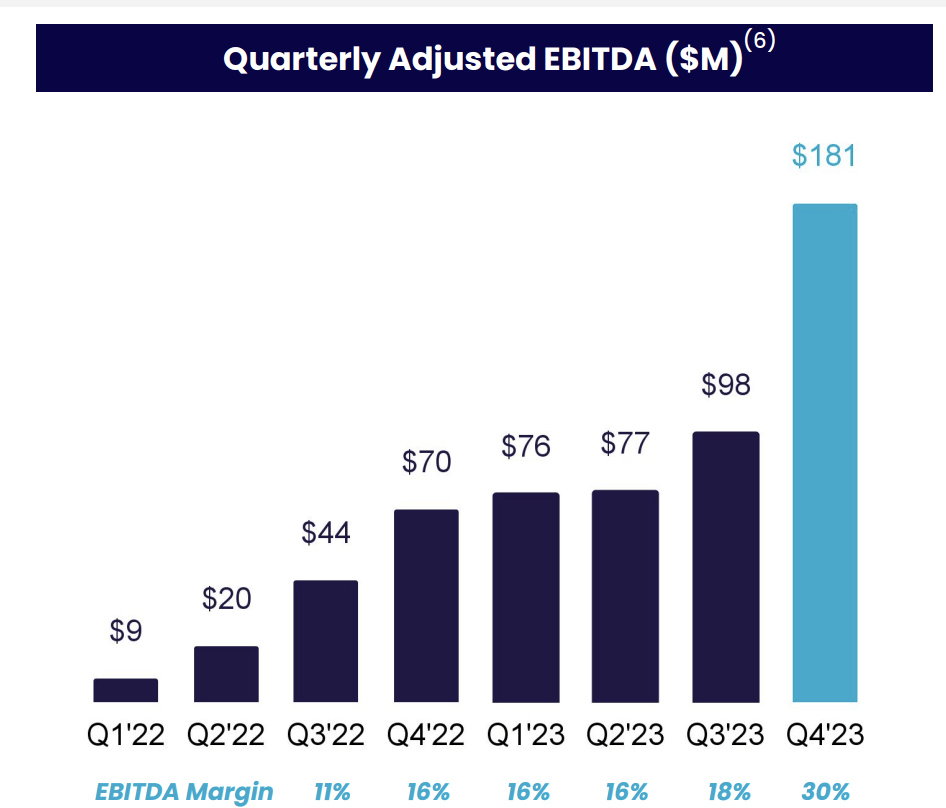

The stock has been very volatile since the SPAC deal, but the company continues to report blockbuster numbers. SoFi just reported Q4 ’23 revenues of $594.3 million, up an incredible 34% from last Q4.

While the top line revenue growth was remarkable considering the tough economic environment and limited demand for loans, the bigger boost came from the bottom line. SoFi reported Q4’23 adjusted EBITDA nearly doubled sequentially from Q3 to $181 million.

Source: SoFi Q4’23 presentation

The fintech reported increasing amounts of adjusted EBITDA over the last year, but the market mostly ignored this progress. The prime reason was the focus on GAAP profits, with SoFi reaching this milestone during Q4’23 with an EPS of $0.02.

Naturally, a minimal EPS isn’t impressive, but for numerous reasons, investors should focus more on the adjusted profits. The prime reason adjusted EBITDA is actually an adjusted profit metric is that the primary expenses excluded are non-cash charges.

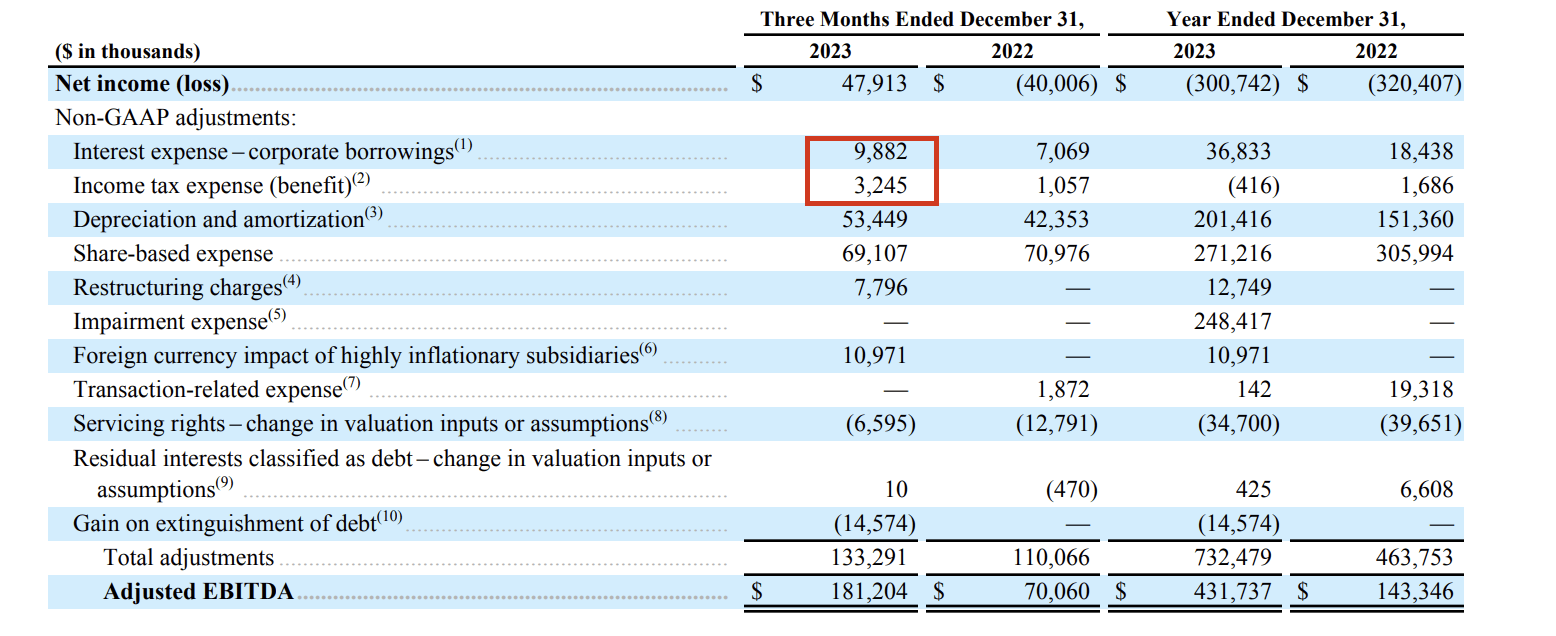

Outside of interest expenses and income taxes highlighted in the below EBITDA table, the other charges are generally non-charge. Of the $181 million in adjusted EBITDA, SoFi only had $13.2 million in normal expenses not excluded from an adjusted profit metric.

Source: SoFi Q4’23 earnings release

As highlighted before, the primary adjustments are for amortization charges and stock-based expense. The 2 charges combined for $122.6 million in reversible charges.

The amortization charges have nothing to do with the ongoing business and everything to do with writing off the excessive purchase price of acquisitions. The fintech even took a large goodwill impairment expense last quarter. The stock-based expense is factored into the EPS calculation with the diluted share counts.

With SoFi now reporting profits, the company now lists a diluted share count of 1.03 billion. The stock now has a $9 billion market cap, with the stock jumping to $9 following the strong Q4 results.

A prime example of the profit machine set up for SoFi is the guidance for tangible book value to grow by $300 to $500 million in the current year. The GAAP EPS target for the company is only $0.06, which amounts to just $60 million in net income for the year.

Big Guidance

SoFi enters 2024 as a sudden profit machine. The company guided to the following numbers for the year:

- Tech Platform and Financial Services growth of 50% or more versus 2023 levels

- Lending segment at 92-95% of 2023 revenue levels

- GAAP Net Income of $95 – $105 million

- Adj. EBITDA of $580 – 590 million

- EPS of $0.07 – $0.08 cents

- $300 – 500 million of Tangible Book Value growth.

The big key is that target for adjusted EBITDA to reach nearly $600 million in 2024, up from $432 million in 2023. SoFi continues to grow profits at a fast clip as the new banking products launched in the last couple of years are turning into profit machines after reaching scale.

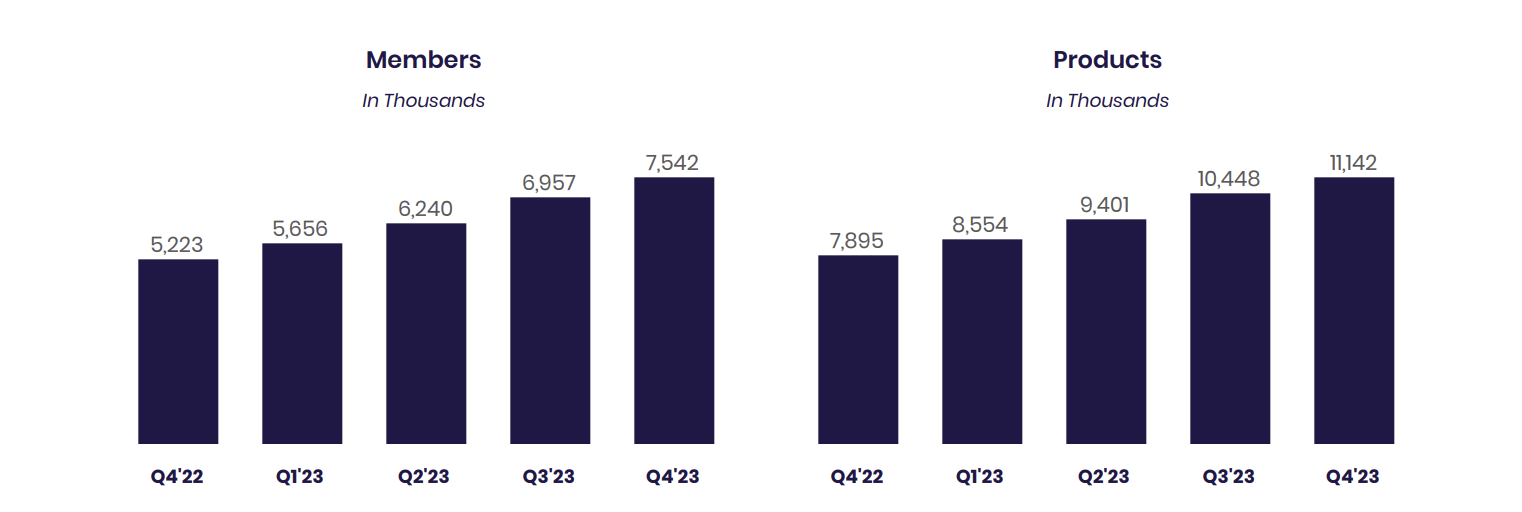

The company continues to add a substantial amount of new members, driving additional products’ growth. These new members and the expansion of the products utilized by existing members will drive growth for years ahead.

Source: SoFi Q4’23 earnings release

SoFi added 585K new members during the quarter for 44% growth. These members added 695K new products for 41% growth. The company grew products by 110K more than members in a sign of how members are adding more than the original product.

The company doesn’t even guide to a strong lending segment push due to dire economic guidance. SoFi set forth these weak economic metrics for 2024:

- Contraction in GDP in 2024

- Increase in unemployment to higher than 5%

- Continuation of uncertain capital markets activity and continued normalization of consumer credit

- Assuming four rate cuts with Fed funds rate reaching ~4.5% by Q4 2024.

The lending segment is only forecast to generate up to 95% of the revenues produced in 2023 due to a corporate desire to hold back lending activities below demand with the expectation for a recession. All of the growth is tied to the Financial Services business and Tech platform targets at growing a combined 50% during 2024 leading to ~$400 million in revenue growth compared to nearly $800 million worth of revenues in 2023.

The reality is likely that SoFi exceeds the guidance. While the company is slightly negative on the lending segment, the company is only now ramping up mortgage lending and the student loan lending market isn’t fully back to pre-Covid levels yet.

As mentioned above, the stock has a market cap of only $9 billion, while SoFi guided to nearly $600 million of adjusted EBITDA (profits) in 2024. The consensus analyst estimates are up at $756 million in 2025 suggesting more upside next year.

Assuming a new 2025 adjusted EBITDA target of $750 million, the stock only trades at 12x forward estimates. Once going back to the original 2023 EBITDA target of $270 million, SoFi likely smashes the 2024 estimates, again providing substantial upside to the 2025 estimates.

The fintech had originally guided to EBITDA numbers hitting nearly $1.5 billion by 2025 before some of the student loan moratoriums and the extra spending on Financial Services. In essence, the large gap in EBITDA numbers are likely to be closed over the next few years, all while an investor can actually get the stock at least $1 cheaper now than when the SPAC deal was agreed to with these financial targets.

Only last July, SoFi soared to nearly $12 following the big Q2’23 beat. Ironically, the stock ended up falling below $7 by mid-November despite the fintech guiding to a 2023 adjusted EBITDA at the time of $338 million and actually hitting $432 million, or 28% higher.

The stock market is oddly not trading stocks based on actual results, as normally a company beating targets by 28% over the course of 6 months would actually trade vastly higher. SoFi beats numbers and investors sell the stock off.

The common fears over the next few months will be teeth gnashing over the lack of Lending Segment growth. The market will attempt to convince investors the growth story is over here. In reality, lower interest rates will compress revenues, but SoFi will be far more profitable going forward. SoFi guided to annualized growth rates of 20% to 25% through 2026 and the market isn’t valuing the stock for any growth ahead.

Takeaway

The key investor takeaway is that the market remains too negative, with SoFi trading with a limited market cap in comparison to the corporate growth over the last few years as a public company. Even more amazing, SoFi appears far too negative with forecasts for GDP declines and unemployment surging to 5% providing potential upside with a boost in lending when the negative economic view changes.

Either way, SoFi Technologies, Inc. stock trades at only 12x adjusted EBITDA profits for 2025. Considering the fintech has constantly beat internal financial targets and the consistent strong growth rates, SoFi shouldn’t trade at a multiple far below the likely conservative growth rates.

Q2 2024 Earnings Call Transcript")